American Antitrust Institute

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Joint Proxy Statement of CVS Corporation and Caremark Rx, Inc

MERGER PROPOSED YOUR VOTE IS VERY IMPORTANT The boards of directors of CVS Corporation and Caremark Rx, Inc. have each approved a merger agreement which provides for the combination of the two companies in a transaction structured as a merger of equals. The boards of directors of CVS and Caremark believe that the combination of the two companies will be able to create substantially more long-term stockholder value than either company could individually achieve. Following the completion of the merger, Caremark will be a wholly owned subsidiary of CVS and Caremark stockholders will own approximately 45.5% of the outstanding common stock of the combined company and CVS stockholders will own approximately 54.5% of the outstanding common stock of the combined company, in each case, on a fully diluted basis. CVS Corporation is referred to as CVS and Caremark Rx, Inc. is referred to as Caremark. The combined company will be named CVS/Caremark Corporation and the shares of the combined company will be traded on the New York Stock Exchange, or the NYSE, under the symbol CVS . If the merger is completed, Caremark s stockholders will receive 1.670 shares of common stock of CVS/Caremark, for each share of Caremark common stock that they own immediately before the effective time of the merger. Caremark stockholders will receive cash for any fractional shares which they would otherwise receive in the merger. Caremark stockholders will also receive a one-time special cash dividend in the amount of $2.00 per share of Caremark common stock held by each such holder on a record date to be set by the Caremark board of directors, which dividend will be conditioned on the completion of the merger and will be paid at or immediately following the effective time of the merger. -

INDEX Rx IPSA LOQUITUR Case-Of-The-Month Vol. 1, No. 4

INDEX Rx IPSA LOQUITUR Case-of-the-Month Vol. 1, No. 4 (12/74) Mahaffey v. Sandoz Duty to warn Vol. 2, No. 2 ( 2/75) Heling v. Carey Standard of care Vol. 2, No. 3 ( 3/75) Nelson v. Stadner Standard of care Vol. 2, No. 4 ( 4/75) Crocker v. Winthrop Manufacturer’s Liability Vol. 2, No. 6 ( 6/75) Tonneson v. Paul B. Elder Company Duty to warn Vol. 2, No. 10 (10/75) Shirley Terry v. California Board of Price advertising Pharmacy Vol. 2, No. 11 (11/75) Dobson v. Mulcare Expert testimony Vol. 2, No. 12 (12/75) Mississippi State Board of Price advertising Pharmacy v. Steele and Schub Vol. 3, No. 2 ( 2/76) State Board of Medical Examiners v. Chiropractors Olson Vol. 3, No. 4 ( 4/76) U.S. v. Moore Controlled Substances Vol. 3, No. 5 ( 5/76) Rutherford v. U.S. Laetrile Vol. 3, No. 6 ( 6/76) Davis v. Wyeth Labs Swine Flu Vaccine Vol. 3, No. 7 ( 7/76) Virginia State Board of Pharmacy v. Price advertising Virginia Citizens Consumer Council Vol. 3, No. 8 ( 8/76) Romanyk v. Longs Drug Stores Labeling Error Vol. 3, No. 9 ( 9/76) Anonymous Poison Prevention Packing Act Vol. 3, No. 11 (11/76) Texas State Board of Pharmacy v. Price advertising Gibson’s Discount Center Vol. 3, No. 12 (12/76) Davis v. Katz & Besthoff Contributory Negligence Vol. 4, No. 1 ( 1/77) Wilson v. City of Walla Walla and False arrest Payless Drug Stores Vol. 4, No. 2 ( 2/77) Population Services International v. -

CVS Distribution Center $22,875,000

The Kase Group CVS Distribution Center 43800 Gen Mar Novi, MI 48375 $22,875,000 22 Yr Absolute Bond Net Lease with 16+ Yrs Left Zero Landlord Responsibilities Investment Grade Credit Tenant S&P Rated BBB+ Credit - NYSE: CVS Presented By: Kase Abusharkh Brian Gordon 252 Abigail Circle Danville, CA 94506 (925)348-1844 The information listed above has been obtained from sources we believe to be reliable, however, we accept no responsibility for its correctness. Table of Contents 1 Financial Analysis Executive Summary Investment Information Rent Roll Summary 2 Tenant Overview 3 Additional Information Pictures The information listed above has been obtained from sources we believe to be reliable, however, we accept no responsibility for its correctness. 1 . Financial Analysis Executive Summary CVS Distribution Center 43800 Gen Mar Novi, MI 48375 List Price $22,875,000 Price per S.F. $52.09 CAP 6.15 % Building S.F. 439,150 Land Acres 22.32 CVS Distribution Center Cross Street Novi Drive Tax Parcel Number 22-22-276-008 Market Detroit MSA Sub Market Oakland County Year Built 1987 Year Renovated 1996 No. of Buildings 2 HVAC Yes Freeway Access Yes Rail Access Yes Airport Access Yes No. of Stories 1 Property Descriptions Area Novi, Michigan is located in southeastern Michigan in Oakland County, and just 25 minutes from downtown Detroit. Novi is one of the fastest-growing cities in Michigan. The construction of Twelve Oaks Mall in the 1970s made the city a major shopping destination in the Detroit metropolitan area and is often credited with ushering in an era of growth that continues to this day. -

The Power Of

A DSN SPECIAL REPORT n 2012, DSN presented an in-depth report on CVS Caremark’s integrated pharmacy business model — part big retail pharmacy chain, part big PBM, part big retail clinic operator — and the innova- tive products and solutions that were coming out of the organization, particularly where the three parts of Ithe business came together, its “integration sweet spots,” as company executives referred to them. It was clear at the time that the company had emerged as a “category of one,” which was the cover theme of that special issue. Now, a year later, as the company completes its 50th year in business and the country awaits a period of change in health care unlike anything seen in at least that time, CVS Caremark executives are quite confident that its unique hybrid structure and its ability to leverage the three core parts of its business — either individually or together, in varying combinations to serve a multitude of needs — aligns more effectively with the long-term trends in health care and puts the company in a unique position at a singular moment in history. In an exclusive interview with DSN, CVS Caremark president and CEO Larry Merlo talked about what that means, why it’s important to both public and private pay- ers of all sizes, health plans, patients and providers, as well as how the company is using behavioral economics and predictive analytics to more effectively engage clients and customers and how they are building new clinical capabilities to address the new models of care, new cus- tomers and new quality standards that will guide the new payment models that will emerge through health reform. -

AAI Filed Tunney Act Comments

December 17, 2018 Peter Mucchetti Chief, Healthcare and Consumer Products Section Antitrust Division Department of Justice 450 Fifth Street NW, Suite 4100 WashinGton, DC 20530 Re: United States v. CVS Health Corp., No. 1:18-cv-02340, Comments of the American Antitrust Institute Dear Mr. Mucchetti: The American Antitrust Institute (AAI) is an independent nonprofit organization devoted to promotinG competition that protects consumers, businesses, and society. It serves the public throuGh research, education, and advocacy on the benefits of competition and the use of antitrust enforcement as a vital component of national and international competition policy. See http://www.antitrustinstitute.org.1 AAI submits these comments pursuant to the Antitrust Procedures and Penalties Act, 15 U.S.C. § 16 (“APPA” or the “Tunney Act”), to object to the settlement in this case. AAI respectfully submits that the settlement does not resolve the competitive problems raised by the combination of CVS and Aetna because it does not address the vertical concerns raised by the transaction, which AAI set forth in a March 26, 2018 letter to the Antitrust Division (hereinafter “AAI Letter”). The AAI Letter is enclosed for further consideration by the Antitrust Division and consideration by the Court durinG the course of its Tunney Act review. AAI requests that the Antitrust Division withdraw and revise the consent aGreement to address the vertical concerns raised by the transaction. BarrinG withdrawal, AAI requests in the alternative that the Antitrust Division publicly explain the basis for its apparent conclusion that a vertical remedy is unnecessary to prevent the multiplicity of anticompetitive harms raised in the AAI Letter and to preserve competition in the market for the sale of individual Medicare Part D prescription druG plans (“individual PDPs”), which is the focus of the complaint. -

Highlights from the 12Th CEO/Innovators Roundtable May 18-19, 2017 Boston, Massachusetts

Highlights from the 12th CEO/Innovators Roundtable May 18-19, 2017 Boston, Massachusetts By David G Anderson, PhD, Barbara Anderman, MA, and Larry Vernaglia, JD, MPH Table of Contents Introduction .................................................................................................................................................................3 Leveraging Culture to Propel Innovation ....................................................................................................................4 Innovative Responses to Payment Reform ..................................................................................................................6 Designing Health Care for the Consumer ....................................................................................................................8 Artificial Intelligence. How is it Being Leveraged Within Health Care? ................................................................... 10 Case Studies in Transformation: Success Stories .......................................................................................................12 2 Introduction Designed to bring together the most dynamic minds in health care, consumer empowerment, clinical integration, and many care, the CEO/Innovators Roundtable serves as an open and other innovations are still very much “in process.” robust forum to debate the latest challenges and opportunities The two days of the roundtable were divided into five panels, facing the industry. Over two days, health system and health each -

October/November 2014 Mergers and Acquisitions in U.S. Retail Pharmacy

October/November 2014 Mergers and Acquisitions in U.S. Retail Pharmacy PengCheng Zhu, Ph.D., CFA Assistant Professor of Finance School of Business Administration University of San Diego Peter E. Hilsenrath, Ph.D. Joseph M. Long Chair in Healthcare Management and Professor of Economics Eberhardt School of Business Thomas J. Long School of Pharmacy & Health Sciences University of the Pacific Journal of Health Care Finance www.HealthFinanceJournal.com Mergers and Acquisitions in U.S. Retail Pharmacy Abstract The retail pharmacy industry is the primary source of prescription medication for Americans. It has transformed away from a cottage industry of independent pharmacies and consolidated toward chain drug stores and mail order. This trend, its causes and consequences, are not fully understood. We use secondary data to study a sample of 87 large acquisitions in the industry. Findings indicate that in spite of rapid growth, profitability eroded. Stock investors respond positively to merger and acquisition announcements for both acquiring and acquired firms and negatively for rival firms not party to such transactions. We also show that the concentration of the retail pharmacy industry is negatively correlated with producer prices and positively correlated with profitability. Our findings are consistent with a view that retail pharmacies are merging to create countervailing power for bargaining leverage with other parties in the supply chain. The capital market perceives these mergers positively and shareholders benefit from these transactions. 2 I. INTRODUCTION There has been considerable scholarly interest in the pharmaceutical industry with focus on relatively high prices and profit margins as well as mergers and acquisitions (M&A’s) (Berndt, 2002; Danzon et al., 2012). -

CVS Aetna AAI Letter

March 26, 2018 Mr. Makan Delrahim Assistant Attorney General Antitrust Division U.S. Department of Justice 950 Pennsylvania Ave. NW Washington, DC 20530 Re: Competitive and Consumer Concerns Raised by the CVS-Aetna Merger Dear Assistant Attorney General Delrahim: The American Antitrust Institute (AAI) has long advocated for competition and consumers in healthcare, including the pharmaceutical, hospital, health insurance, and intermediary (i.e., group purchasing organization and pharmacy benefit manager (PBM)) sectors.1 AAI writes to express concern that the proposed merger of the retail pharmacy chain/PBM CVS Health and health insurer Aetna will potentially harm competition and consumers. This letter adds to the concerns raised by other important voices, including the American Medical Association (AMA) and Consumers Union.2 We note that at the time of this writing, the parallel merger of the PBM Express Scripts and health insurer Cigna was recently announced. We provide some additional analysis of the competitive implications of both mergers and the resulting restructuring of key segments of the health care industry that they would bring about. I. Overview CVS-Aetna would pair up the largest retail pharmacy chain and one of the two largest PBMs with the 3rd largest health insurer in the U.S.3 The proposed merger raises a number of questions for 1 The AAI is an independent non-profit education, research and advocacy organization. Its mission is to advance the role of competition in the economy, protect consumers, and sustain the vitality of the antitrust laws. For more information, see www.antitrustinstitute.org. Many thanks to David Balto for help in reviewing an earlier draft, Bill Comanor for important insight, and to AAI research Fellow Mark Angland for valuable research assistance. -

Schedule B 8 Employment Verification Fees

Employer Name Alternate Name City State Fee 1St Tennessee And 1St Horizon Memphis TN 1998 $9.00 3Com $10.00 3M Corporation St. Paul MN $9.00 7-Up $10.00 711 $10.00 76 Products Unocal 1998 $9.00 A&W Yorkshire Global Restaurants $9.00 AAA Auto Blug Roup $9.00 AAFES $9.00 AAFIS $9.00 Abbott Laboratories $9.00 Abercroman Fitch $9.00 Abn Amro - North America Chicago IL 1996 $9.00 Acapulco Acquisition Corp $10.00 Accor $15.00 Accredo Health Service $9.00 Ace Cash Express $10.00 Acme Steel $9.00 Adecco "Tad Technical" San Francisco CA $9.00 Adecco Employment Services $9.00 Adecco -Olsten $9.00 ADM Milling Inc $9.00 Admiral Trucking Dow Chemical Co. 1991 $9.00 Adt Security Services, Inc. Aurora CO $9.00 Advance Auto Parts Roanoke VA $9.00 Advanced Micro Devices Sunnyvale CA 1998 $9.00 Advanced Pcs Inc $10.00 Advanced Sterilization Products Johnson & Johnson 1994 $9.00 Advanta Horsham PA 1998 $9.00 Advest, Inc. $10.00 Advocate Health Care Oakbrook IL 1991 $9.00 Advocate Medical Group Advocate Health Care 1991 $9.00 Aero Products Litton Aero Products 1991 $9.00 Aetna Hartford CT 1990 $9.00 Afc/ Churches EVS $15.00 Afsa Data Corporation FleetBoston 1994 $9.00 After Thoughts Foot Locker 1997 $9.00 Aga Gas $9.00 Agilent Tech $9.00 Agl Resources, Inc $9.00 Agouron Puerto Rico $9.00 Agricultural Marketing Service State of California $9.00 Ahold Financial Services Ahold $9.00 Aimco (Authorization Required For All Levels) $9.00 Air Force (Civilian Employees) $9.00 Airborne Express Seattle WA 1985 $9.00 Revised January 1, 2004 1 of 40 Employer Name Alternate Name City State Fee Ajilon $9.00 Ajs Supermarket Llc $9.00 Akn Ncs $9.00 Akron City Hospital Summa Health Systems 1996 $9.00 Akron General Medical Center Akron OH 1996 $9.00 Alabama Power $9.00 Albertsons $9.00 Alcoa, Inc. -

CVS Pharmacy - Wikipedia, the Free Encyclopedia CVS Pharmacy from Wikipedia, the Free Encyclopedia

4/2/2016 CVS Pharmacy - Wikipedia, the free encyclopedia CVS Pharmacy From Wikipedia, the free encyclopedia CVS Pharmacy (styled as CVS/pharmacy or simply CVS) is an American pharmacy retailer and currently CVS Pharmacy stands as the second largest pharmacy chain, after Walgreens, in the United States,[1] with more than 7,600 stores,[2] and is the second largest US pharmacy based on total prescription revenue.[3] As the retail pharmacy division of CVS Health, it ranks as the 12th largest company in the world according to Fortune 500 in 2014.[4] CVS Pharmacy's leading competitor Walgreens ranked 37th. CVS sells prescription drugs and a wide assortment of A newer CVS Pharmacy storefront in St. Louis, general merchandise, including over-the-counter drugs, Missouri beauty products and cosmetics, film and photo finishing services, seasonal merchandise, greeting cards, and Formerly Consumer Value Stores (1963- convenience foods through their CVS Pharmacy and called 1996) Longs Drugs retail stores and online through CVS.com. It Type Subsidiary also provides healthcare services through its more than Industry Retail 1,000 MinuteClinic medical clinics [5] as well as their Founded May 8, 1963 Diabetes Care Centers. Most of these clinics are located Lowell, Massachusetts, U.S. within CVS stores. Founders Stanley Goldstein CVS is incorporated in Delaware, and is based in Sidney Goldstein Ralph Hoagland Woonsocket, Rhode Island.[6] As of 2008, CVS Caremark Headquarters 1 CVS Drive, Woonsocket, Rhode was the largest for-profit employer in Rhode Island.[6] It Island, United States was founded on Merrimack Street in Lowell, Massachusetts, in 1963, under the name Consumer Value Number of 7,600 stores (2014 estimate) locations Store.[7] It was founded by Sid Goldstein, Stanley Area served Nationwide Goldstein, and Ralph Hoagland, as a discount health and beauty aid store. -

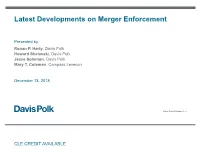

Latest Developments on Merger Enforcement

Latest Developments on Merger Enforcement Presented by Ronan P. Harty, Davis Polk Howard Shelanski, Davis Polk Jesse Solomon, Davis Polk Mary T. Coleman, Compass Lexecon December 13, 2018 Davis Polk & Wardwell LLP CLE CREDIT AVAILABLE Agenda 1. Recent Trends in Antitrust M&A in the U.S. 2. Vertical Merger Enforcement & The Planned Guidelines 3. Recent Developments Regarding Merger Remedies 4. FTC Hearings on Competition and Consumer Protection & The Rise of Populist Antitrust 5. Implications of Change of Control in U.S. House on Antitrust M&A 6. International Developments 1 Presented by Ronan P. Harty Howard Shelanski Jesse Solomon Mary T. Coleman 2 Recent Trends in Antitrust M&A in the U.S. Antitrust Merger Enforcement in the Trump Administration 4 Antitrust Merger Enforcement Transactions reported 1,450 1,429 1,326 1,663 1,801 1,832 2,052 under the HSR Act (FY) In FY 2018, 2,110 transactions were reported under the HSR Act. The number of Second Requests issued during the year has not yet been publicly reported. 5 Antitrust Merger Enforcement (cont.) Total Outcomes 28 28 22 28 37 33 27 13 6 Recent Trends . Aggressive enforcement and willingness to challenge deals under the Trump Administration . E.g., Walgreens/RiteAid, DraftKings/FanDuel, AT&T/Time Warner . Including consummated mergers . E.g., Otto Bock/FIH, TransDigm/Takata . Parker-Hannifin/CLARCOR: parties cleared HSR but DOJ subsequently opened an investigation in response to customer complaints and required a divestiture . Focus on innovation competition at both agencies, even before the Trump Administration . FTC: e.g., Nielsen/Arbitron; Verisk Analytics/EagleView; Steris/Synergy . -

CVS Distribution Center 500 Lansdowne Road Fredericksburg, VA 22408

www.TheKaseGroup.com CVS Distribution Center 500 Lansdowne Road Fredericksburg, VA 22408 $25,800,000 Long Term Absolute Bond Net Lease Zero Landlord Responsibilities Investment Grade Credit | S&P Rating of BBB+ Washington D.C. Metropolitan Area Presented By: Kase Abusharkh 252 Abigail Circle Danville, CA 94506 (925)348-1844 The information listed above has been obtained from sources we believe to be reliable, however, we accept no responsibility for its correctness. Table of Contents 1 Financial Analysis 2 Tenant Corporate Stock Information 3 Tenant Corporate Growth Summary 4 Area Demographics Summary 5 Additional Site Information 6 Property Photos The information listed above has been obtained from sources we believe to be reliable, however, we accept no responsibility for its correctness. 1 . Financial Analysis Executive Summary CVS Distribution Center 500 Lansdowne Road Fredericksburg, VA 22408 List Price $25,800,000 Price per S.F. $52.88 CAP 6.01 % Building S.F. 487,897 No. of Dock High Doors 65 Land Acres 39.40 CVS Distribution Center Cross Street Shannon Drive Tax Parcel Number 024-A-00-102A Market Washington D.C. MSA Sub Market Spotsylvania County Year Built 1985 Year Renovated 1995 Roof Type Standing Seam Roof Zoning Type Commercial No. of Buildings 1 Percent Office Space 3.00 % Mezzanine Yes HVAC Yes Freeway Access Yes Rail Access Yes Airport Access Yes No. of Stories 1 Clear Height 39 Feet Sprinkler Type Wet Pipe ESFR Property Descriptions Area The property is located immediately south of the City of Fredericksburg in Spotsylvania County. Spotsylvania is one of Virginia's fastest-growing counties, largely because of its location along Interstate 95, midway between the United States capital of Washington D.C.