Latest Developments on Merger Enforcement

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Agenda for FTC Hearing #3: Competition and Consumer

Monday, October 15, 2018 9:00-9:05 am Welcome and Introductory Remarks Henry N. Butler George Mason University Antonin Scalia Law School 9:05-9:20 am Welcome and Introductory Remarks Rohit Chopra, Commissioner Federal Trade Commission 9:20-9:50 am The Economics of Multi-Sided Platforms David S. Evans Global Economics Group 9:50-10:10 am Network Effects in Multi-Sided Platforms Catherine Tucker Massachusetts Institute of Technology Sloan School of Management 10:10-10:20 am Break 10:20-12:20 pm The Current Economic Understanding of Multi-Sided Platforms Participants: David S. Evans Katja Seim Global Economics Group University of Pennsylvania Wharton School Joseph Farrell University of California, Berkeley Howard Shelanski Department of Economics Georgetown University Law Center Davis Polk & Wardwell LLP Marc S. Rysman Boston University Catherine Tucker Department of Economics Massachusetts Institute of Technology Sloan School of Management Michael A. Salinger Boston University Questrom School of Business Moderator: John M. Yun George Mason University Antonin Scalia Law School 12:20-1:30 pm Lunch Break 2 | Page 1:30-3:00 pm Multi-Sided Platforms in Action Participants: Elizabeth J. Altman Steven Tadelis University of Massachusetts Lowell University of California, Berkeley Manning School of Business Haas School of Business Scott Kupor Ben Thompson Andreessen Horowitz Stratechery, LLC Roger McNamee Elevation Partners Moderator: Jan Rybnicek George Mason University Antonin Scalia Law School Freshfields Bruckhaus Deringer LLP 3:00-3:15 pm Break 3:15-5:00 pm Defining Relevant Markets and Establishing Market Power in Cases Involving Multi-Sided Platforms Participants: Tasneem Chipty Michael A. -

Embargoed Until Delivered TESTIMONY of HOWARD

Embargoed Until Delivered EXECUTIVE OFFICE OF THE PRESIDENT OFFICE OF MANAGEMENT AND BUDGET WASHINGTON, D.C. 20503 www.whitehouse.gov/omb TESTIMONY OF HOWARD SHELANSKI ADMINISTRATOR FOR THE OFFICE OF INFORMATION AND REGULATORY AFFAIRS OFFICE OF MANAGEMENT AND BUDGET BEFORE THE HOUSE COMMITTEE ON OVERSIGHT AND GOVERNMENT REFORM SUBCOMMITTEE ON HEALTH CARE, BENEFITS AND ADMINISTRATIVE RULES AND THE SUBCOMMITTEE ON GOVERNMENT OPERATIONS UNITED STATES HOUSE OF REPRESENTATIVES March 3, 2015 Chairman Jordan, Ranking Member Cartwright, Chairman Meadows, Ranking Member Connolly and members of the Subcommittees: Thank you for the invitation to appear before you today. I am pleased to have this opportunity to discuss the activities and priorities of the Office of Information and Regulatory Affairs (OIRA). As the Administrator of OIRA, it is my privilege to work with the skilled and dedicated OIRA staff, the first-rate leadership team at the Office of Management and Budget, and our excellent colleagues throughout the Government. We are all working to continue our Nation’s economic recovery and employment growth while protecting the health, safety, and welfare of Americans, now and into the future. OIRA has a broad portfolio that ranges from coordination of Government-wide information and statistical policy to review of Executive Branch regulations to international regulatory cooperation. For example, under the Paperwork Reduction Act, OIRA is responsible for reviewing collections of information by the Federal Government to ensure that they are not unnecessarily burdensome. OIRA also develops and oversees the implementation of Government-wide statistical standards and policies, facilitates efficient and effective data sharing, and provides guidance on privacy and confidentiality policy to Federal agencies. -

Joint Proxy Statement of CVS Corporation and Caremark Rx, Inc

MERGER PROPOSED YOUR VOTE IS VERY IMPORTANT The boards of directors of CVS Corporation and Caremark Rx, Inc. have each approved a merger agreement which provides for the combination of the two companies in a transaction structured as a merger of equals. The boards of directors of CVS and Caremark believe that the combination of the two companies will be able to create substantially more long-term stockholder value than either company could individually achieve. Following the completion of the merger, Caremark will be a wholly owned subsidiary of CVS and Caremark stockholders will own approximately 45.5% of the outstanding common stock of the combined company and CVS stockholders will own approximately 54.5% of the outstanding common stock of the combined company, in each case, on a fully diluted basis. CVS Corporation is referred to as CVS and Caremark Rx, Inc. is referred to as Caremark. The combined company will be named CVS/Caremark Corporation and the shares of the combined company will be traded on the New York Stock Exchange, or the NYSE, under the symbol CVS . If the merger is completed, Caremark s stockholders will receive 1.670 shares of common stock of CVS/Caremark, for each share of Caremark common stock that they own immediately before the effective time of the merger. Caremark stockholders will receive cash for any fractional shares which they would otherwise receive in the merger. Caremark stockholders will also receive a one-time special cash dividend in the amount of $2.00 per share of Caremark common stock held by each such holder on a record date to be set by the Caremark board of directors, which dividend will be conditioned on the completion of the merger and will be paid at or immediately following the effective time of the merger. -

Law and Professor of Law

March 17, 2017 The Honorable Charles E. Grassley, Chairman Committee on the Judiciary United States Senate 224 Dirksen Senate Office Building Washington, D.C. 20510 The Honorable Dianne Feinstein, Ranking Member Committee on the Judiciary United States Senate 331 Hart Senate Office Building Washington, D.C. 20510 Dear Chairman Grassley and Ranking Member Feinstein: We are a group of law professors and legal scholars who write to urge the Senate to confirm Judge Neil M. Gorsuch as the next Associate Justice of the Supreme Court of the United States. We are a diverse group of scholars with a wide range of backgrounds, and we hold both liberal and conservative political views. We are united, however, in the belief that Judge Gorsuch will bring the highest judicial standards to the Court. Although we may not agree with each decision or vote he will cast, we all agree that Judge Gorsuch is eminently qualified to serve on the Court and that his jurisprudence is within the mainstream of contemporary legal thought. Taken together, these traits should ensure his confirmation. Judge Gorsuch’s credentials are first-rate. He holds an undergraduate degree from Columbia University, a law degree from Harvard University, and a doctorate in legal philosophy from Oxford University. His career has covered nearly every facet of the law. After law school, Judge Gorsuch served as a law clerk to Judge David Sentelle of the U.S. Court of Appeals for the D.C. Circuit and Justices Byron White and Anthony Kennedy of the Supreme Court. For ten years, he worked at the firm Kellogg, Huber, Hansen, Todd, Evans & Figel as both a trial and appellate lawyer, ultimately becoming a partner there. -

INDEX Rx IPSA LOQUITUR Case-Of-The-Month Vol. 1, No. 4

INDEX Rx IPSA LOQUITUR Case-of-the-Month Vol. 1, No. 4 (12/74) Mahaffey v. Sandoz Duty to warn Vol. 2, No. 2 ( 2/75) Heling v. Carey Standard of care Vol. 2, No. 3 ( 3/75) Nelson v. Stadner Standard of care Vol. 2, No. 4 ( 4/75) Crocker v. Winthrop Manufacturer’s Liability Vol. 2, No. 6 ( 6/75) Tonneson v. Paul B. Elder Company Duty to warn Vol. 2, No. 10 (10/75) Shirley Terry v. California Board of Price advertising Pharmacy Vol. 2, No. 11 (11/75) Dobson v. Mulcare Expert testimony Vol. 2, No. 12 (12/75) Mississippi State Board of Price advertising Pharmacy v. Steele and Schub Vol. 3, No. 2 ( 2/76) State Board of Medical Examiners v. Chiropractors Olson Vol. 3, No. 4 ( 4/76) U.S. v. Moore Controlled Substances Vol. 3, No. 5 ( 5/76) Rutherford v. U.S. Laetrile Vol. 3, No. 6 ( 6/76) Davis v. Wyeth Labs Swine Flu Vaccine Vol. 3, No. 7 ( 7/76) Virginia State Board of Pharmacy v. Price advertising Virginia Citizens Consumer Council Vol. 3, No. 8 ( 8/76) Romanyk v. Longs Drug Stores Labeling Error Vol. 3, No. 9 ( 9/76) Anonymous Poison Prevention Packing Act Vol. 3, No. 11 (11/76) Texas State Board of Pharmacy v. Price advertising Gibson’s Discount Center Vol. 3, No. 12 (12/76) Davis v. Katz & Besthoff Contributory Negligence Vol. 4, No. 1 ( 1/77) Wilson v. City of Walla Walla and False arrest Payless Drug Stores Vol. 4, No. 2 ( 2/77) Population Services International v. -

1 STATEMENT of HOWARD SHELANSKI Nominee to Serve As

STATEMENT OF HOWARD SHELANSKI Nominee to Serve As Administrator of the Office of Information and Regulatory Affairs, Office of Management and Budget UNITED STATES SENATE COMMITTEE ON HOMELAND SECURITY AND GOVERNMENT AFFAIRS June 12, 2013 Thank you Chairman Carper, Ranking Member Coburn, and Members of the Committee for welcoming me today. It is an honor to be considered by this committee as the President’s nominee to be Administrator of the Office of Information and Regulatory Affairs. I would like to start off this morning by thanking my family for their support in taking on this challenge. I am glad to have Nicole Soulanille, our son Isaac Shelanski, and my parents Vivien and Michael Shelanski here with me today. I also want to thank the Members of the Committee and their staffs for meeting with me over the last few weeks. I appreciate the time many of you took from your busy schedules and thank you for sharing your insights and views as I prepared for this hearing. For those of you I have not yet had the opportunity to meet, I look forward to doing so in the future. If confirmed, I look forward to working with you and maintaining open communications. I would welcome your perspectives on the matters with which OIRA is concerned. The Office of Information and Regulatory Affairs, often referred to as OIRA, plays an essential role in developing and overseeing the implementation of Government-wide policies on regulation, information collection, information quality and technology, statistical standards, scientific evidence, and privacy. I am humbled by my nomination to lead such an important organization. -

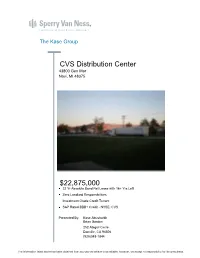

CVS Distribution Center $22,875,000

The Kase Group CVS Distribution Center 43800 Gen Mar Novi, MI 48375 $22,875,000 22 Yr Absolute Bond Net Lease with 16+ Yrs Left Zero Landlord Responsibilities Investment Grade Credit Tenant S&P Rated BBB+ Credit - NYSE: CVS Presented By: Kase Abusharkh Brian Gordon 252 Abigail Circle Danville, CA 94506 (925)348-1844 The information listed above has been obtained from sources we believe to be reliable, however, we accept no responsibility for its correctness. Table of Contents 1 Financial Analysis Executive Summary Investment Information Rent Roll Summary 2 Tenant Overview 3 Additional Information Pictures The information listed above has been obtained from sources we believe to be reliable, however, we accept no responsibility for its correctness. 1 . Financial Analysis Executive Summary CVS Distribution Center 43800 Gen Mar Novi, MI 48375 List Price $22,875,000 Price per S.F. $52.09 CAP 6.15 % Building S.F. 439,150 Land Acres 22.32 CVS Distribution Center Cross Street Novi Drive Tax Parcel Number 22-22-276-008 Market Detroit MSA Sub Market Oakland County Year Built 1987 Year Renovated 1996 No. of Buildings 2 HVAC Yes Freeway Access Yes Rail Access Yes Airport Access Yes No. of Stories 1 Property Descriptions Area Novi, Michigan is located in southeastern Michigan in Oakland County, and just 25 minutes from downtown Detroit. Novi is one of the fastest-growing cities in Michigan. The construction of Twelve Oaks Mall in the 1970s made the city a major shopping destination in the Detroit metropolitan area and is often credited with ushering in an era of growth that continues to this day. -

The Power Of

A DSN SPECIAL REPORT n 2012, DSN presented an in-depth report on CVS Caremark’s integrated pharmacy business model — part big retail pharmacy chain, part big PBM, part big retail clinic operator — and the innova- tive products and solutions that were coming out of the organization, particularly where the three parts of Ithe business came together, its “integration sweet spots,” as company executives referred to them. It was clear at the time that the company had emerged as a “category of one,” which was the cover theme of that special issue. Now, a year later, as the company completes its 50th year in business and the country awaits a period of change in health care unlike anything seen in at least that time, CVS Caremark executives are quite confident that its unique hybrid structure and its ability to leverage the three core parts of its business — either individually or together, in varying combinations to serve a multitude of needs — aligns more effectively with the long-term trends in health care and puts the company in a unique position at a singular moment in history. In an exclusive interview with DSN, CVS Caremark president and CEO Larry Merlo talked about what that means, why it’s important to both public and private pay- ers of all sizes, health plans, patients and providers, as well as how the company is using behavioral economics and predictive analytics to more effectively engage clients and customers and how they are building new clinical capabilities to address the new models of care, new cus- tomers and new quality standards that will guide the new payment models that will emerge through health reform. -

ICN Unilateral Conduct Working Group

1 ICN Unilateral Conduct Working Group TELESEMINAR ON REMEDIES IN UNILATERAL CONDUCT CASES 11 MARCH 2010 Introductory Remarks by Operator 2 y Welcome by Operator y Panelists and Participants please note: { Audience will be muted during most parts of the teleseminar call („Audience Call“) { Audience will be be unmuted during Q&A { Teleseminar will be recorded y Operator will then turn over to UCWG Co-host Markus Lange (Bundeskartellamt, Germany) Welcome by UCWG Co-Chair Markus Lange 3 y ICN teleseminars have proven to be effective instruments to provide a forum for the sharing of experience and the fostering of consensus. y Today’s seminar is the second teleseminar held by the ICN Unilateral Conduct Working Group. The first seminar on Excessive Pricing was very well received and more than 150 participants joined. A recording is posted on the ICN website. y This seminar aims to promote the understanding of remedies in unilateral conduct cases. y The slides prepared will lead you through the seminar. They can be downloaded from the ICN website. Those of you that have registered in advance can also follow along by going on the link provided to you along with the confirmation. y The agenda for today’s teleseminar is as follows: Teleseminar Agenda 4 y I. Introduction by co-host Randy Tritell (U.S. Federal Trade Commission) y II. Presentation of Principles and Issues to Consider in Crafting Remedies by Howard Shelanski (U.S. Federal Trade Commission) y III. Panel Discussion of Hypothetical 1 y IV. Q & A with Audience regarding Hypothetical 1 y V. -

AAI Filed Tunney Act Comments

December 17, 2018 Peter Mucchetti Chief, Healthcare and Consumer Products Section Antitrust Division Department of Justice 450 Fifth Street NW, Suite 4100 WashinGton, DC 20530 Re: United States v. CVS Health Corp., No. 1:18-cv-02340, Comments of the American Antitrust Institute Dear Mr. Mucchetti: The American Antitrust Institute (AAI) is an independent nonprofit organization devoted to promotinG competition that protects consumers, businesses, and society. It serves the public throuGh research, education, and advocacy on the benefits of competition and the use of antitrust enforcement as a vital component of national and international competition policy. See http://www.antitrustinstitute.org.1 AAI submits these comments pursuant to the Antitrust Procedures and Penalties Act, 15 U.S.C. § 16 (“APPA” or the “Tunney Act”), to object to the settlement in this case. AAI respectfully submits that the settlement does not resolve the competitive problems raised by the combination of CVS and Aetna because it does not address the vertical concerns raised by the transaction, which AAI set forth in a March 26, 2018 letter to the Antitrust Division (hereinafter “AAI Letter”). The AAI Letter is enclosed for further consideration by the Antitrust Division and consideration by the Court durinG the course of its Tunney Act review. AAI requests that the Antitrust Division withdraw and revise the consent aGreement to address the vertical concerns raised by the transaction. BarrinG withdrawal, AAI requests in the alternative that the Antitrust Division publicly explain the basis for its apparent conclusion that a vertical remedy is unnecessary to prevent the multiplicity of anticompetitive harms raised in the AAI Letter and to preserve competition in the market for the sale of individual Medicare Part D prescription druG plans (“individual PDPs”), which is the focus of the complaint. -

2016-03-15 Howard Shelanski OMB Testimony

EMBARGOED UNTIL DELIVERED EXECUTIVE OFFICE OF THE PRESIDENT OFFICE OF MANAGEMENT AND BUDGET WASHINGTON, D.C. 20503 www.whitehouse.gov/omb TESTIMONY OF HOWARD SHELANSKI ADMINISTRATOR FOR THE OFFICE OF INFORMATION AND REGULATORY AFFAIRS OFFICE OF MANAGEMENT AND BUDGET BEFORE THE HOUSE COMMITTEE ON OVERSIGHT AND GOVERNMENT REFORM SUBCOMMITTEE ON GOVERNMENT OPERATIONS UNITED STATES HOUSE OF REPRESENTATIVES March 15, 2016 Chairman Meadows, Ranking Member Connolly, and members of the Subcommittee: Thank you for the invitation to appear before you today. I am pleased to have this opportunity to discuss the role that the Office of Information and Regulatory Affairs (OIRA) plays in the transparency and accountability of the federal regulatory process. As the Administrator of OIRA, it is my privilege to work with the dedicated OIRA staff, the first-rate leadership team at the Office of Management and Budget (OMB), and our excellent colleagues throughout the Government. We are all working to promote economic growth and job creation while protecting the health, safety, and welfare of Americans, now and into the future. OIRA has a broad portfolio, but the largest area of OIRA’s work is the review of regulations promulgated by Executive Branch departments and agencies. A set of Executive Orders (E.O.s)—most significantly E.O. 12866 and E.O. 13563—provides the principles and procedures for OIRA’s regulatory reviews. Regulatory process in the United States is premised to an unrivaled degree on two principles: transparency and accountability. One of my priorities as OIRA Administrator has been to increase the transparency of the regulatory process by improving notice and predictability for the 1 public. -

Antitrust Enforcement, Regulation, and Digital Platforms

ARTICLE ANTITRUST ENFORCEMENT, REGULATION, AND DIGITAL PLATFORMS WILLIAM P. ROGERSON† & HOWARD SHELANSKI†† INTRODUCTION ........................................................................... 1912 I. GOING BEYOND ADJUDICATION FOR ANTITRUST ENFORCEMENT ...................................................................... 1917 A. Case-by-Case, Fact-Specific Approach ........................................... 1917 B. Slow, Usually Predictable Doctrinal Development ........................... 1918 C. Market-Driven Case Selection .................................................... 1919 D. Generalists versus Industry Experts ............................................. 1920 E. Tradeoffs Inherent in the Adjudicatory Approach to Antitrust ........... 1921 F. A Regulatory Alternative ........................................................... 1924 II. LIGHT HANDED PRO-COMPETITIVE (LHPC) REGULATION .... 1924 A. Introduction ............................................................................. 1924 B. Potential Types of Regulation ...................................................... 1927 1. Interconnection/Interoperability Requirements and Common Standards .......................................................... 1927 2. Limits on Discrimination ................................................. 1930 3. Data Portability ............................................................... 1933 4. Line-of-Business Restrictions ........................................... 1934 5. Additional Restrictions on Business Practices Currently †