Insightseries

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Skills and Services Directory Achieve More from Your Property Property

Skills and Services Directory Achieve more from your property Property. It’s what we do every day – and we love it. When you experience the difference we can make, we think you’ll really appreciate what we do… So how can we help you exactly? Well, we offer you expert advice and a comprehensive range of services to cover all your property needs. We can help you make the very best property decisions to get the result you’re after. We are ready to help you make sure you achieve more from your property right now. Contact us today on 0333 772 1235 or [email protected] Asset Experience Academic, Health and Land Community Property and Institutional Airfields Public Realm Day care facilities Barns Community centres Doctors’ surgeries Brownfield sites County farm estates Extra care development Common land Leisure centres Primary care centres Contaminated land Libraries and information centres Respite and Residential Country parks, national parks Markets and small business centres care facilities and public open spaces Police, fire and ambulance stations Schools, colleges and Crown land Public access universities Development land Sports centres Student accommodation Entitlement Social housing Supported housing ESAs, AONBs and SSSIs Town halls and administrative Equestrian offices Historical Estates Ancient Monuments Farm and accommodation land Residential Churches Foreshores and rivers Country houses Church houses Glebe land Residential investments Listed buildings Greenfield sites Horticulture Retail Industrial Landfill sites Banks -

March 2010 Annual Report

TR Property Investment Trust plc –TR Property Investment Trust ReportMarch 2010 & Accounts for the year ended 31 TR Property Investment Trust plc Report & Accounts for the year ended 31 March 2010 TR Property Investment Trust plc is managed by This document is printed on Revive Silk of which 75% of the furnish is made from 100% de-inked post consumer waste. The remaining 25% being mill broke and virgin fibres. This paper is bleached using a combination of Totally Chlorine Free (TCF) and Elemental Chlorine Free (ECF). The manufacturing mill is accredited with the ISO 14001 standard for environmental management. TR Property Investment Trust plc Directors’ Review Accounts 1 Overview 62 Independent Auditors’ Report 2 Statement of Investment Objective and Policy 63 Group Income Statement 4 Financial Highlights and Performance 64 Group and Company Statement of Changes in Equity 5 Historical Performance 65 Group and Company Balance Sheets 6 Chairman’s Statement 66 Group and Company Cash Flow Statements 10 Managers’ Report – Market Background and Outlook 67 Notes to the Financial Statements 15 Ordinary Shares – Financial Highlights and Performance Shareholder Information 16 Ordinary Shares – Manager’s Report 89 Notice of Annual General Meeting 21 Ordinary Shares – Portfolio Details 93 Notice of Separate Class Meeting of Ordinary 27 Ordinary Shares – Income Statement Shareholders 28 Ordinary Shares – Balance Sheet 94 Notice of Separate Class Meeting of Sigma Shareholders 29 Sigma Shares – Financial Highlights and Performance 95 Explanation of -

Taylor Woodrow Plc Report and Accounts 2006 Our Aim Is to Be the Homebuilder of Choice

Taylor Woodrow plc Report and Accounts 2006 Our aim is to be the homebuilder of choice. Our primary business is the development of sustainable communities of high-quality homes in selected markets in the UK, North America, Spain and Gibraltar. We seek to add shareholder value through the achievement of profitable growth and effective capital management. Contents 01 Group Financial Highlights 54 Consolidated Cash Flow 02 Chairman’s Statement Statement 05 Chief Executive’s Review 55 Notes to the Consolidated 28 Board of Directors Financial Statements 30 Report of the Directors 79 Independent Auditors’ Report 33 Corporate Governance Statement 80 Accounting Policies 37 Directors’ Remuneration Report 81 Company Balance Sheet 46 Directors’ Responsibilities 82 Notes to the Company Financial Statement Statements 47 Independent Auditors’ Report 87 Particulars of Principal Subsidiary 48 Accounting Policies Undertakings 51 Consolidated Income Statement 88 Five Year Review 52 Consolidated Statement of 90 Shareholder Facilities Recognised Income and Expense 92 Principal Taylor Woodrow Offices 53 Consolidated Balance Sheet Group Financial Highlights • Group revenues £3.68bn (2005: £3.56bn) • Housing profit from operations* £469m (2005: £456m) • Profit before tax £406m (2005: £411m) • Basic earnings per share 50.5 pence (2005: 50.6 pence) • Full year dividend 14.75 pence (2005: 13.4 pence) • Net gearing 18.6 per cent (2005: 23.7 per cent) • Equity shareholders’ funds per share 364.7 pence (2005: 338.4 pence) Profit before tax £m 2006 405.6 2005 411.0 2004 403.9 Full year dividend pence (Represents interim dividends declared and paid and final dividend for the year as declared by the Board) 2006 14.75 2005 13.4 2004 11.1 Equity shareholders’ funds per share pence 2006 364.7 2005 338.4 2004 303.8 * Profit from operations is before joint ventures’ interest and tax (see Note 3, page 56). -

Please Download Our Brochure

“During 2020 the UK market saw £40Bn of commercial property investment transactions. £10.5Bn of this was in Central London and a significant proportion (almost c.30%) was from Asia – based capital.” Allsop LLP & Millennium Group UK property consultants Allsop LLP and Asia-based property advisors Millennium Group formed an alliance to strengthen their services to advise existing and new Asia-based investors looking to deploy capital into UK real estate. The alliance serves to leverage the long-standing relationships and understanding of Asian client needs with the experience, expertise and extensive local market knowledge of the UK markets. This international synergy enables us to create informed, sensible, bespoke strategies through the entire cycle of property investing that is tailored to individual or corporate requirements. Services we offer overseas clients with UK assets and aspirations include: Lease Advisory – Asset & Development Investment Advisory rent reviews & restructures Management Development Valuation Office Leasing Consultancy Residential Development Property Business Rates & Investment Management About About • Established in 1906 • Pride ourselves on our open, • Established in 1998 • Independent property friendly and honest business • Full Asia coverage approach consultancy (LLP) • Numerous long-standing relationships with • Market-leading reputation for high • 19 Equity Partners Asia’s most prominent property investors quality service, market knowledge, • 125 Fee Earners insight and expertise • Property management partnership -

Technology and the Future of Real Estate Investment Management

Technology and the Future of Real Estate Investment Management PI LABS X OXFORD FUTURE OF REAL ESTATE INITIATIVE: TECHNOLOGY AND THE FUTURE OF REAL ESTATE INVESTMENT MANAGEMENT 2 Contents Foreword 03 Executive summary 04 Introduction: the global property investment universe 07 Issues for the industry 08 The Investment Manager of the future 10 Technology and investment managers 13 Roundtable findings 16 The data standardisation problem 18 Start-up market map 22 Distribution and investor management 23 Capital raising 24 Investor relations and reporting 26 Operations, compliance, finance and fund structuring 27 Performance analysis 29 Manufacturing and the investment process 31 Sourcing 32 Appraisals 34 Negotiation 37 Transactions (acquisitions and disposals) 38 Portfolio management 39 Asset management 40 Conclusions 43 References 45 Figures 46 Tables 47 PI LABS X OXFORD FUTURE OF REAL ESTATE INITIATIVE: TECHNOLOGY AND THE FUTURE OF REAL ESTATE INVESTMENT MANAGEMENT 3 Foreword Against the macro-economic backdrop of climate change, rapid urbanisation and now COVID-19, the industry is facing challenges it has never seen before. Understanding how to negotiate these challenges will require collaboration, new industry standards and the application of technology. Those real estate investment managers best able to weather this storm will be those who are most innovative and best at adopting emerging technologies. While it is clear that the real estate investment management sector is at the beginning of a process of digital transition, there are many barriers inhibiting the widespread application of technology. This is most likely due to the lack of a regulatory framework and industry standards regarding the ownership and sharing of digital data, as well as a lack of knowledge of the available solutions. -

Investor Presentation

Investor Presentation HY 2020 Our Investment Case 1 2 3 4 Our distinctive The scale and A well-positioned Our operational business model & quality of our development expertise & clear strategy portfolio pipeline customer insight Increasing our focus 22.5m sq ft of Development pipeline Expertise in on mixed use places high quality assets aligned to strategy managing and leasing our assets based on our customer insight Growing London Underpinned by our Provides visibility campuses and resilient balance sheet on future earnings Residential and refining and financial strength Drives incremental Retail value for stakeholders 1 British Land at a glance 1FA, Broadgate £15.4bn Assets under management £11.7bn Of which we own £521m Annualised rent 22.5m sq ft Floor space 97% Occupancy Canada Water Plymouth As at September 2019 2 A diverse, high quality portfolio £11.7bn (BL share) Multi-let Retail (26%) London Campuses (45%) 72% London & South East Solus Retail (5%) Standalone offices (10%) Retail – London & SE (10%) Residential & Canada Water (4%) 3 Our unique London campuses £8.6bn Assets under management £6.4bn Of which we own 78% £205m Annualised rent 6.6m sq ft Floor space 97% Occupancy As at September 2019 4 Canada Water 53 acre mixed use opportunity in Central London 5 Why mixed use? Occupiers Employees want space which is… want space which is… Attractive to skilled Flexible Affordable Well connected Located in vibrant Well connected Safe and promotes Sustainable and employees neighbourhoods wellbeing eco friendly Tech Close to Aligned to -

Proptech 3.0: the Future of Real Estate

University of Oxford Research PropTech 3.0: the future of real estate PROPTECH 3.0: THE FUTURE OF REAL ESTATE WWW.SBS.OXFORD.EDU PROPTECH 3.0: THE FUTURE OF REAL ESTATE PropTech 3.0: the future of real estate Right now, thousands of extremely clever people backed by billions of dollars of often expert investment are working very hard to change the way real estate is traded, used and operated. It would be surprising, to say the least, if this burst of activity – let’s call it PropTech 2.0 - does not lead to some significant change. No doubt many PropTech firms will fail and a lot of money will be lost, but there will be some very successful survivors who will in time have a radical impact on what has been a slow-moving, conservative industry. How, and where, will this happen? Underlying this huge capitalist and social endeavour is a clash of generations. Many of the startups are driven by, and aimed at, millennials, but they often look to babyboomers for money - and sometimes for advice. PropTech 2.0 is also engineering a much-needed boost to property market diversity. Unlike many traditional real estate businesses, PropTech is attracting a diversified pool of talent that has a strong female component, representation from different regions of the world and entrepreneurs from a highly diverse career and education background. Given the difference in background between the establishment and the drivers of the PropTech wave, it is not surprising that there is some disagreement about the level of disruption that PropTech 2.0 will create. -

Annex 1: Parker Review Survey Results As at 2 November 2020

Annex 1: Parker Review survey results as at 2 November 2020 The data included in this table is a representation of the survey results as at 2 November 2020, which were self-declared by the FTSE 100 companies. As at March 2021, a further seven FTSE 100 companies have appointed directors from a minority ethnic group, effective in the early months of this year. These companies have been identified through an * in the table below. 3 3 4 4 2 2 Company Company 1 1 (source: BoardEx) Met Not Met Did Not Submit Data Respond Not Did Met Not Met Did Not Submit Data Respond Not Did 1 Admiral Group PLC a 27 Hargreaves Lansdown PLC a 2 Anglo American PLC a 28 Hikma Pharmaceuticals PLC a 3 Antofagasta PLC a 29 HSBC Holdings PLC a InterContinental Hotels 30 a 4 AstraZeneca PLC a Group PLC 5 Avast PLC a 31 Intermediate Capital Group PLC a 6 Aveva PLC a 32 Intertek Group PLC a 7 B&M European Value Retail S.A. a 33 J Sainsbury PLC a 8 Barclays PLC a 34 Johnson Matthey PLC a 9 Barratt Developments PLC a 35 Kingfisher PLC a 10 Berkeley Group Holdings PLC a 36 Legal & General Group PLC a 11 BHP Group PLC a 37 Lloyds Banking Group PLC a 12 BP PLC a 38 Melrose Industries PLC a 13 British American Tobacco PLC a 39 Mondi PLC a 14 British Land Company PLC a 40 National Grid PLC a 15 BT Group PLC a 41 NatWest Group PLC a 16 Bunzl PLC a 42 Ocado Group PLC a 17 Burberry Group PLC a 43 Pearson PLC a 18 Coca-Cola HBC AG a 44 Pennon Group PLC a 19 Compass Group PLC a 45 Phoenix Group Holdings PLC a 20 Diageo PLC a 46 Polymetal International PLC a 21 Experian PLC a 47 -

Portfolio of Investments

PORTFOLIO OF INVESTMENTS Variable Portfolio – Partners International Value Fund, September 30, 2020 (Unaudited) (Percentages represent value of investments compared to net assets) Investments in securities Common Stocks 97.9% Common Stocks (continued) Issuer Shares Value ($) Issuer Shares Value ($) Australia 4.2% UCB SA 3,232 367,070 AMP Ltd. 247,119 232,705 Total 13,350,657 Aurizon Holdings Ltd. 64,744 199,177 China 0.6% Australia & New Zealand Banking Group Ltd. 340,950 4,253,691 Baidu, Inc., ADR(a) 15,000 1,898,850 Bendigo & Adelaide Bank Ltd. 30,812 134,198 China Mobile Ltd. 658,000 4,223,890 BlueScope Steel Ltd. 132,090 1,217,053 Total 6,122,740 Boral Ltd. 177,752 587,387 Denmark 1.9% Challenger Ltd. 802,400 2,232,907 AP Moller - Maersk A/S, Class A 160 234,206 Cleanaway Waste Management Ltd. 273,032 412,273 AP Moller - Maersk A/S, Class B 3,945 6,236,577 Crown Resorts Ltd. 31,489 200,032 Carlsberg A/S, Class B 12,199 1,643,476 Fortescue Metals Group Ltd. 194,057 2,279,787 Danske Bank A/S(a) 35,892 485,479 Harvey Norman Holdings Ltd. 144,797 471,278 Demant A/S(a) 8,210 257,475 Incitec Pivot Ltd. 377,247 552,746 Drilling Co. of 1972 A/S (The)(a) 40,700 879,052 LendLease Group 485,961 3,882,083 DSV PANALPINA A/S 15,851 2,571,083 Macquarie Group Ltd. 65,800 5,703,825 Genmab A/S(a) 1,071 388,672 National Australia Bank Ltd. -

191220 Industrial Property Sector Overview QD

QuotedData Sector overview | Real estate 20 December 2019 Industrial property market The gift that keeps on giving Companies covered in this report: The industrial and logistics sector has been on a Aberdeen Standard ASLI LN European Logistics tremendous run over the past five years or so. It is hard Income to think now, given the current dynamics in the property LondonMetric LMP LN industry, that retail and offices were the sectors of Property SEGRO SGRO LN choice for investors for many years with industrial cast Stenprop STP LN aside by most. St Modwen SMP LN Properties All that changed, primarily off the back of a fundamental shift in Tritax Big Box REIT BBOX LN consumer buying habits. Amazon has become a behemoth and Tritax Eurobox EBOX LN online-only retailers have popped up and taken significant market Urban Logistics REIT SHED LN share from their high street rivals – operating from a network of Warehouse REIT WHR LN warehouses across the country. The trend towards ecommerce, and its effect on both the industrial and retail sectors, is well-known. Consumer spending online has been growing dramatically to the point Industrial property performance1 now where just under 20% of all retail transactions in the UK are made Time period 30/11/2014 to 30/11/2019 on the internet. 130 This has meant that traditional retailers, as well as their online-only 120 peers, have been scrambling to get their distribution networks 110 functioning efficiently. Long gone are the days of one huge warehouse in the middle of the country that served a retailer’s shops. -

Annual Report and Accounts 2012 2012 8493 1 Report 2012 Report 2012 01 to 96 31/05/2012 14:41 Page 3

8493 1 Report 2012_Report 2012 01 to 96 31/05/2012 14:41 Page 2 The British Land Company DELIVERING PERFORMANCE PLC Annual Report and Accounts Annual Report and Accounts Annual Report and Accounts 2012 2012 8493 1 Report 2012_Report 2012 01 to 96 31/05/2012 14:41 Page 3 BRITISH LAND IS ONE OF EUROPE’S LARGEST REAL ESTATE INVESTMENT TRUSTS (REITs) AND OUR VISION IS TO BE THE BEST. We provide investors with access to a diverse range of quality property assets which we actively manage, finance and develop. We focus mainly on prime UK retail and London office properties and have a reputation for delivering industry-leading customer service. Our properties and our approach attracts high-quality occupiers committed to long leases, so we can provide shareholders with security of income as well as capital growth. Our size and substance demands a responsible approach to business. We believe achieving leading levels of efficiency and sustainability in our buildings helps drive our performance. This is also of increasing importance to occupiers and central to our aim to create environments in which businesses and local communities can thrive. Corporate responsibility information is integrated throughout our Annual Report and Accounts. This reflects how managing our environmental, economic and social impacts is central to the way we do business. It also provides readers with insights into the critical linkages in our thinking and activity, and greater clarity on the relationship between our financial and non-financial key performance indicators. Why go online? For more information Our corporate website contains detailed information You’ll find links throughout this Report, about the Company and is frequently updated as to guide you with further reading or relevant additional details become available. -

FTSE Factsheet

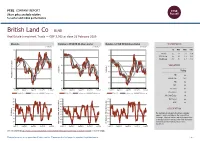

FTSE COMPANY REPORT Share price analysis relative to sector and index performance Data as at: 21 February 2020 British Land Co BLND Real Estate Investment Trusts — GBP 5.562 at close 21 February 2020 Absolute Relative to FTSE UK All-Share Sector Relative to FTSE UK All-Share Index PERFORMANCE 21-Feb-2020 21-Feb-2020 21-Feb-2020 6.5 105 115 1D WTD MTD YTD Absolute -2.0 -5.4 0.3 -12.9 110 Rel.Sector -2.0 -4.0 -1.8 -12.3 100 Rel.Market -1.6 -5.3 -1.5 -11.6 6 105 95 VALUATION 100 5.5 Trailing 95 RelativePrice RelativePrice 90 PE -ve Absolute Price (local (local Absolute currency)Price 90 5 EV/EBITDA 28.1 85 85 PB 0.6 PCF 8.4 4.5 80 80 Div Yield 5.0 Feb-2019 May-2019 Aug-2019 Nov-2019 Feb-2020 Feb-2019 May-2019 Aug-2019 Nov-2019 Feb-2020 Feb-2019 May-2019 Aug-2019 Nov-2019 Feb-2020 Price/Sales 5.8 Absolute Price 4-wk mov.avg. 13-wk mov.avg. Relative Price 4-wk mov.avg. 13-wk mov.avg. Relative Price 4-wk mov.avg. 13-wk mov.avg. Net Debt/Equity 0.4 90 100 90 Div Payout -ve 80 90 80 ROE -ve 70 80 70 70 Index) Share Share Sector) Share - 60 - 60 60 DESCRIPTION 50 50 50 40 40 The Company is a property investment company 40 RSI RSI (Absolute) 30 30 based in London and listed on the London Stock 30 Exchange.