Skyscraper Indicator and Its Application in the UK

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Roman House Is a Rare Opportunity to Acquire a Luxury Apartment Or Penthouse in a Premier City of London Location

1 THE CITY’S PREMIER NEW ADDRESS 2 3 ROMAN HOUSE IS A RARE OPPORTUNITY TO ACQUIRE A LUXURY APARTMENT OR PENTHOUSE IN A PREMIER CITY OF LONDON LOCATION. THE SQUARE MILE’S RENOWNED RESTAURANTS, LUXURY SHOPS AND WORLD CLASS CULTURAL VENUES ARE ALL WITHIN WALKING DISTANCE; WHILE CHIC, SUPERBLY WELL PLANNED INTERIORS CREATE A BOUTIQUE HOTEL STYLE LIVING ENVIRONMENT. AT ROMAN HOUSE, BERKELEY OFFERS EVERYTHING THAT COSMOPOLITAN TASTES AND INTERNATIONAL LIFESTYLES DEMAND. 4 1 THE EPITOME THE CITY OF OF BOUTIQUE WESTMINSTER CITY LIVING THE CITY Contents 5 Welcome to a new style of City living 28 On the world stage 6 Welcome home 30 On the city borders 8 An unparalleled living experience 32 Be centrally located 11 Y 35 A world class business destination 12 Your personal oasis 37 Wealth and prestige 14 A healthy lifestyle right on your doorstep 38 London, the leading city 16 Café culture 41 London, the city for arts and culture 18 Find time for tranquillity 42 A world class education 20 Y 44 Zone 1 connections 23 Vibrant bars 46 Sustainable living in the heart of the city 25 Shop in Royal style 47 Designed for life 26 London, the global high street 48 Map 2 3 Computer Generated Image of Roman House is indicative only. Y Welcome to years, and is considered a classic of its time. Now, it is entering a prestigious new era, expertly refurbished by Berkeley to provide ninety exquisite new homes in the heart of the City, a new style with a concierge and gymnasium for residents’ exclusive use. -

22 Bishopsgate London EC2N 4BQ Construction of A

Committee: Date: Planning and Transportation 28 February 2017 Subject: Public 22 Bishopsgate London EC2N 4BQ Construction of a building arranged on three basement floors, ground and 58 upper floors plus mezzanines and plant comprising floorspace for use within Classes A and B1 of the Use Classes Order and a publicly accessible viewing gallery and facilities (sui generis); hard and soft landscaping works; the provision of ancillary servicing and other works incidental to the development. (201,449sq.m. GEA) Ward: Lime Street For Decision Registered No: 16/01150/FULEIA Registered on: 24 November 2016 Conservation Area: St Helen's Place Listed Building: No Summary The planning application relates to the site of the 62 storey tower (294.94m AOD) granted planning permission in June 2016 and which is presently being constructed. The current scheme is for a tower comprising 59 storeys at ground and above (272.32m AOD) with an amended design to the top. The tapering of the upper storeys previously approved has been omitted and replaced by a flat topped lower tower. In other respects the design of the elevations remains as before. The applicants advise that the lowering of the tower in the new proposal is in response to construction management constraints in relation to aviation safeguarding issues. The planning application also incorporates amendments to the base of the building, the public realm and to cycle space provision which were proposed in a S73 amendment application and which your Committee resolved to grant on 28 November 2016, subject to a legal agreement but not yet issued. The building would provide offices, retail at ground level, a viewing gallery with free public access at levels 55 and 56 and a public restaurant and bar at levels 57 and 58. -

861 Sq Ft Headquarters Office Building Your Own Front Door

861 SQ FT HEADQUARTERS OFFICE BUILDING YOUR OWN FRONT DOOR This quite unique property forms part of the building known as Rotherwick House. The Curve comprises a self-contained building, part of which is Grade II Listed, which has been comprehensively refurbished to provide bright contemporary Grade A office space. The property — located immediately to the east of St Katharine’s Dock and adjoining Thomas More Square — benefits from the immediate area which boasts a wide variety of retail and restaurant facilities. SPECIFICATION • Self-contained building • Generous floor to ceiling heights • New fashionable refurbishment • Full-height windows • New air conditioning • Two entrances • Floor boxes • Grade II Listed building • LG7 lighting with indirect LED up-lighting • Fire and security system G R E A ET T THE TEA TRE E D S A BUILDING OL S T E R SHOREDITCH N S HOUSE OLD STREET T R E E T BOX PARK AD L RO NWEL SHOREDITCH CLERKE C I HIGH STREET T Y R G O O A S D W S F H A O E R L U A L R T AD T H I O R T R N A S STEPNEY D’ O O M AL G B N A GREEN P O D E D T H G O T O WHITECHAPEL A N N R R R O D BARBICAN W O CHANCERY E A FARRINGDON T N O LANE D T T E N H A E M C T N O C LBOR A D O HO M A IGH MOORGATE G B O H S R R U TOTTENHAM M L R LIVERPOOL P IC PE T LO E COURT ROAD NDON WA O K A LL R N R H STREET H C L C E E O S A I SPITALFIELDS I IT A A W B N H D L E W STE S R PNEY WAY T O J R U SALESFORCE A E HOLBORN B T D REE TOWER E ST N I D L XFOR E G T O W R E K G ES H ALDGATE I A H E N TE A O M LONDON MET. -

Liverpool Street Bus Station Closure

Liverpool Street bus station closed - changes to routes 11, 23, 133, N11 and N133 The construction of the new Crossrail ticket hall in Liverpool Street is progressing well. In order to build a link between the new ticket hall and the Underground station, it will be necessary to extend the Crossrail hoardings across Old Broad Street. This will require the temporary closure of the bus station from Sunday 22 November until Spring 2016. Routes 11, 23 and N11 Buses will start from London Wall (stop ○U) outside All Hallows Church. Please walk down Old Broad Street and turn right at the traffic lights. The last stop for buses towards Liverpool Street will be in Eldon Street (stop ○V). From there it is 50 metres to the steps that lead down into the main National Rail concourse where you can also find the entrance to the Underground station. Buses in this direction will also be diverted via Princes Street and Moorgate, and will not serve Threadneedle Street or Old Broad Street. Routes 133 and N133 The nearest stop will be in Wormwood Street (stop ○Q). Please walk down Old Broad Street and turn left along Wormwood Street after using the crossing to get to the opposite side of the road. The last stop towards Liverpool Street will also be in Wormwood Street (stop ○P). Changes to routes 11, 23, 133, N11 & N133 Routes 11, 23, 133, N11 & N133 towards Liverpool Street Routes 11 & N11 towards Bank, Aldwych, Victoria and Fulham Route 23 towards Bank, Aldwych, Oxford Circus and Westbourne Park T E Routes 133 & N133 towards London Bridge, Elephant & Castle, -

United States District Court Southern District of Florida

Case 1:20-cv-21964-CMA Document 118 Entered on FLSD Docket 03/08/2021 Page 1 of 7 UNITED STATES DISTRICT COURT SOUTHERN DISTRICT OF FLORIDA CASE NO. 20-cv-21964-CMA SECURITIES AND EXCHANGE COMMISSION, Plaintiff, v. TCA FUND MANAGEMENT GROUP, CORP., a Florida company, et al., Defendants. _____________________________________________/ RECEIVER’S MOTION TO COMPEL FINANCIAL INSTITUTIONS TO DISCLOSE THE INVESTMENT DETAILS OF BENEFICIAL OWNERS Jonathan E. Perlman, Esq., as court-appointed Receiver (“Receiver”) of the Receivership Entities1 files this Motion to Compel Financial Institutions to Disclose the Investment Details of Beneficial Owners (“Motion”) of TCA Global Credit Fund, LTD (“TCA LTD”) and TCA Global Credit Fund, LP (“TCA LP”). Introduction 1. The Receiver requests the Court order parties that facilitated putative investments and subscriptions in TCA LTD and TCA LP – principally financial institutions acting as nominees – to disclose the identity and other critical information regarding the beneficial owners2 as of January 21, 20203. This information is essential to the Receiver’s formulation and 1 All terms not specifically defined herein have the meaning ascribed to them in the SEC’s Motion for Appointment of Receiver [ECF No. 3] and the Court’s Appointment Order [ECF No. 5] (the “Appointment Order”), and the Court’s First Expansion Order [ECF No. 16]. 2 A beneficial owner, for purposes of this motion, includes any entity or person that has submitted a redemption request or has transferred funds to the Receivership Entities in connection with a subscription. Case 1:20-cv-21964-CMA Document 118 Entered on FLSD Docket 03/08/2021 Page 2 of 7 CASE NO. -

Threadneedles You Will Find Us in the Heart of the City of London

Welcome to Threadneedles Our meeting spaces You will find us in the heart of the City of London – a former Three state-of-the-art meeting rooms, Capital, Sterling Victorian banking hall dating back to 1856, cleverly converted and Traders, are equipped to accommodate up to 35 into a five-star boutique hotel. Be it for a meeting, dining or delegates. Room facilities vary with LCD projector and a special celebration, our private rooms cater for all group sizes screen or plasma TV, conference phone, flipchart and pens, and are complemented with modern British cuisine, created pads and pencils, white board and lighting syst em control by head chef Stephen Smith. The highest levels of quality and making them suitable for a variety of events including sales service guarantee a successful event every time. presentations and roadshows. In the heart of the city Exclusive hire Threadneedles is located in ’The City of London’ the most Marco Pierre White Wheeler’s of St. James’s Oyster Bar & Grill historic part of the capital and home to some of its most Room is available for exclusive hire. Combining the two spaces iconic buildings such as the Bank of England, the Gherkin, for a stand-up reception offers a capacity for up to 200 guests the Shard, St Pauls Cathedral, Tate Modern and Tower Bridge. while up to 80 guests can be accommodated for a seated Many of the world’s leading finance, law and insurance firms dinner. For a sophisticated Champagne reception or lavish have offices located in this ‘Square Mile’ and Threadn eedles cocktail party, the dome lounge offers the perfect setting for is located a few minutes walk away from most. -

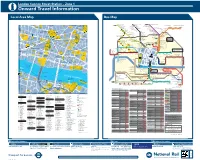

London Cannon Street Station – Zone 1 I Onward Travel Information Local Area Map Bus Map

London Cannon Street Station – Zone 1 i Onward Travel Information Local Area Map Bus Map Palmers Green North Circular Road Friern Barnet Halliwick Park 149 S GRESHAM STREET 17 EDMONTON R 141 1111 Guildhall 32 Edmonton Green 65 Moorgate 12 A Liverpool Street St. Ethelburga’s Centre Wood Green I 43 Colney Hatch Lane Art Gallery R Dutch WALTHAMSTOW F for Reconcilation HACKNEY 10 Church E Upper Edmonton Angel Corner 16 N C A R E Y L A N E St. Lawrence 17 D I and Peace Muswell Hill Broadway Wood Green 33 R Mayor’s 3 T 55 ST. HELEN’S PLACE for Silver Street 4 A T K ING S ’S ARMS YARD Y Tower 42 Shopping City ANGEL COURT 15 T Jewry next WOOD Hackney Downs U Walthamstow E E & City 3 A S 6 A Highgate Bruce Grove RE 29 Guildhall U Amhurst Road Lea Bridge Central T of London O 1 E GUTTER LANE S H Turnpike Lane N St. Margaret G N D A Court Archway T 30 G E Tottenham Town Hall Hackney Central 6 R O L E S H GREEN TOTTENHAM E A M COLEMAN STREET K O S T 95 Lothbury 35 Clapton Leyton 48 R E R E E T O 26 123 S 36 for Whittington Hospital W E LOTHBURY R 42 T T 3 T T GREAT Seven Sisters Lea Bridge Baker’s Arms S T R E E St. Helen S S P ST. HELEN’S Mare Street Well Street O N G O T O T Harringay Green Lanes F L R D S M 28 60 5 O E 10 Roundabout I T H S T K 33 G M Bishopsgate 30 R E E T L R O E South Tottenham for London Fields I 17 H R O 17 Upper Holloway 44 T T T M 25 St. -

Height Vs. History Tall Buildings in the Heart of London Controversy Over Tall Buildings in Central London Is Not a Recent Phenomenon

Height vs. history Tall buildings in the heart of London Controversy over tall buildings in central London is not a recent phenomenon. Peter Stewart explains how heated debates on the issue began as long ago as the late nineteenth century. The proposal for a 250m (820ft) tall residential France, Westminster, completed in 1888 (demolished tower to be built next to Paddington Station – in 1973). Crude and joyless in its design, it was the ‘Paddington Pole’ – is the latest in a line of considerably taller than any other London residential controversial tall-building projects to come forward in building at the time and prompted widespread central London over the last two decades. Designed complaints, including one from Queen Victoria, whose by Renzo Piano, the architect of the ‘Shard’ at London view of the Palace of Westminster from Buckingham Bridge (completed in 2012), and promoted by its Palace was obstructed by the block. Several developer Irvine Sellar, the project has provoked generations of royals later, Prince Charles has proved protests from lay commentators and architects alike. just as vociferous a defender of London’s skyline. Journalist Simon Jenkins, a serial opponent of tall The development of the passenger lift had buildings, complained that the scheme flies in the made tall buildings possible from around 1870 but, face of established planning policies which set out while maximum buildings heights in New York and where tall buildings should and should not be built in Chicago increased rapidly, reaching 240m (787ft) London; and architect Sir Terry Farrell has criticised the with the Woolworth Building in New York by 1913, scheme as piecemeal and opportunistic. -

Tower 42 25 Old Broad Street, London EC2N 1HQ

AVAILABLE TO LET Tower 42 25 Old Broad Street, London EC2N 1HQ Office for rent, 2,758 - 20,178 sq ft, p.o.a George Haworth [email protected] To request a viewing call us on +44 (0)20 7029 3610 Anna Biggin For more information visit https://www.realla.co.uk/m/2059-tower-42-25-old-broad-street [email protected] Tower 42 25 Old Broad Street, London EC2N 1HQ To request a viewing call us on +44 (0)20 7029 3610 Tower 42 is a landmark building, offering 324,000 sq ft of high quality office More information space spread over 42 floors in the heart of the City of London. Tower 42 lies on the east side of Old Broad Street amongst the City high rise Visit microsite cluster, within close proximity of The Bank of England and The Royal Exchange. https://www.realla.co.uk/m/2059-tower-42-25-old-broad-street Bank (Central and Northern Line), Moorgate (Northern, Circle, Metropolitan, Hammersmith and City lines) and Liverpool Street (Northern & Central) Contact us Underground and Mainline stations are just a short walk away. Ingleby Trice The Elizabeth Line (Crossrail) will be available from both Liverpool Street and 10 Foster Lane, London EC2V 6HR Moorgate stations once open. www.tower42.com www.inglebytrice.co.uk Property details +44 (0)20 7029 3610 [email protected] Rent P.O.A Est. S/C £15.59 psf George Haworth S/C Details PPM Charge: estimated at £2.35 per sq ft per Ingleby Trice annum 020 7029 3625 [email protected] Estate charge £2.49 psf James Heyworth-Dunne Est. -

A New Chapter for Willesden Green

A COLLECTION OF EXCLUSIVE 1 AND 2 BEDROOM APARTMENTS A NEW CHAPTER FOR WILLESDEN GREEN WILLESDEN GREEN IS ONE OF NORTH London’s LIVELIEST AND MOST COSMOPOLITAN AREAS, WHOSE EXCELLENT ZONE 2 JUBILEE LINE CONNECTIONS REALLY SET IT APART. AT THE LIBRARY, A NEW COLLECTION OF CONTEMPORARY APARTMENTS, ADJACENT TO THE PRESTIGIOUS NEW WILLESDEN GREEN CULTURAL CENTRE, THE LIFESTYLE OF THIS VIBRANT NEIGHBOURHOOD CAN BE ENJOYED IN FULL. IT OPENS A NEW CHAPTER FOR WILLESDEN GREEN, AND IS A REMARKABLE OPPORTUNITY FOR THE DISCERNING LONDON INVESTOR. A NEW CHAPTER FOR NORTHWEST LONDON The Library is Grosvenor International’s new landmark development in perennially popular Willesden Green, London NW10, and is being created in conjunction with Linden Homes, one of the UK’s most respected developers. The Library takes a prominent position on Willesden High Road, and sets new standards in contemporary accommodation for the area. This exciting scheme comprises four buildings, offering ninety-five highly specified 1 and 2 bedroom apartments, many with balconies or terraces. The development is gated and has underground parking for residents: always a bonus in London. All of the units are for private sale. The forthcoming Cultural Centre, next door to The Library, will be a prestigious addition to the local area and an important focal point. High quality public and private realm, with landscaping and seating, will surround the buildings, completing the theme of well designed residential and community space. PRESTIGIOUS DEVELOPMENT OF 1 AND 2 BEDROOM APARTMENTS HIGH SPECIFICATION PaRT OF A NEW CULTURAL QUARTER GATED, WITH UNDERGROUND PARKING ZONE 2 JUBILEE LINE CONNECTIONS WEST END IN 15 MINUTES VIBRANT LOCAL AREA Computer enhanced image, indicative only. -

High Rise Buildings in London – from 1066 up to Today

John Harvey, IRIS Consulting, Article on Tall Buildings in London Based on a talk given to the Society of Quantity surveyors in June 2015 This article reviews the history of high rise buildings in London – from 1066 up to today. First it provides some basic facts and history about London’s tallest buildings Secondly it looks back at trends and developments affecting high rise construction over the past 100 years or so Finally it assesses what has happened in the last decade or so and looks ahead to the 250 high rise buildings that currently have been approved or are in the pipeline So first some historical perspectives starting with the Norman invasion in 1066 and the construction of the Tower of London by William the Conqueror and his successors. So this history of tall buildings in London begins with the completion of the White Tower, a part of the Tower of London, in 1098. For over a hundred years between 1098 and 1310 the White Tower in the Tower of London was London’s tallest structure. It was 90 feet high or 27 metres (of course in those days the French were not using metres!) The White Tower’s claim to be the tallest building only fell when the old St Paul’s Cathedral was built and completed. Although there is some debate and no absolutely authentic measurement records there are reports that the spire of the old St Paul’s was 493 feet high (160 metres). That spire was destroyed by lightning in 1561 100 years before the Great Fire of London. -

Berkeley-Homes-One-Tower-Bridge

CGI of One Tower Bridge One Tower Bridge sits on the South Bank of the River Thames, in one of the most privileged positions in London. Overview A unique location The clearest sign of how special this location is comes with the address: One Tower Bridge. This is a unique location neighbouring London’s most famous landmark. A place where the past, present and future of this great city meet. A new landmark One Tower Bridge occupies a prime position on London’s South Bank, between three of the city’s most important icons: Tower Bridge, the River Thames and the Tower of London. It is an exceptional new development of contemporary residences, thoughtfully designed and luxuriously appointed throughout. It marks the next stage in the development of one of London’s most exciting and desirable districts, between the signature brickwork and distinctive heritage of Shad Thames, and the sharp, clean, ultra-modern lines of More London. Within walking distance of the City’s financial heart, close to Canary Wharf, next to a string of world-class cultural attractions and enjoying first-rate transport connections, One Tower Bridge justifies the description ‘extraordinary’. This is a London address like no other. CGI of One Tower Bridge An exceptional development of apartments and penthouses, luxuriously appointed to the very highest standard. 5 01 Bank of England 12 Millennium Bridge 23 Shad Thames Road Distances 02 Borough Market 13 Monument 24 The Shard Tower Hill 0.9 km (9 mins) 03 Canary Wharf 14 More London 25 Southwark Cathedral Tower Gateway 1.1