El Nasr Housing and Development

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Egypt Real Estate Trends 2018 in Collaboration With

know more.. Egypt Real Estate Trends 2018 In collaboration with -PB- -1- -2- -1- Know more.. Continuing on the momentum of our brand’s focus on knowledge sharing, this year we lay on your hands the most comprehensive and impactful set of data ever released in Egypt’s real estate industry. We aspire to help our clients take key investment decisions with actionable, granular, and relevant data points. The biggest challenge that faces Real Estate companies and consumers in Egypt is the lack of credible market information. Most buyers rely on anecdotal information from friends or family, and many companies launch projects without investing enough time in understanding consumer needs and the shifting demand trends. Know more.. is our brand essence. We are here to help companies and consumers gain more confidence in every real estate decision they take. -2- -1- -2- -3- Research Methodology This report is based exclusively on our primary research and our proprietary data sources. All of our research activities are quantitative and electronic. Aqarmap mainly monitors and tracks 3 types of data trends: • Demographic & Socioeconomic Consumer Trends 1 Million consumers use Aqarmap every month, and to use our service they must register their information in our database. As the consumers progress in the usage of the portal, we ask them bite-sized questions to collect demographic and socioeconomic information gradually. We also send seasonal surveys to the users to learn more about their insights on different topics and we link their responses to their profiles. Finally, we combine the users’ profiles on Aqarmap with their profiles on Facebook to build the most holistic consumer profile that exists in the market to date. -

THE AMERICAN UNIVERSITY in CAIRO School of Humanities And

1 THE AMERICAN UNIVERSITY IN CAIRO School of Humanities and Social Sciences Department of Arab and Islamic Civilizations Islamic Art and Architecture A thesis on the subject of Revival of Mamluk Architecture in the 19th & 20th centuries by Laila Kamal Marei under the supervision of Dr. Bernard O’Kane 2 Dedications and Acknowledgments I would like to dedicate this thesis for my late father; I hope I am making you proud. I am sure you would have enjoyed this field of study as much as I do. I would also like to dedicate this for my mother, whose endless support allowed me to pursue a field of study that I love. Thank you for listening to my complains and proofreads from day one. Thank you for your patience, understanding and endless love. I am forever, indebted to you. I would like to thank my family and friends whose interest in the field and questions pushed me to find out more. Aziz, my brother, thank you for your questions and criticism, they only pushed me to be better at something I love to do. Zeina, we will explore this world of architecture together some day, thank you for listening and asking questions that only pushed me forward I love you. Alya’a and the Friday morning tours, best mornings of my adult life. Iman, thank you for listening to me ranting and complaining when I thought I’d never finish, thank you for pushing me. Salma, with me every step of the way, thank you for encouraging me always. Adham abu-elenin, thank you for your time and photography. -

Egypt Market Watch

JANUARY 2017 MARKETWATCH Information from Cartus on Relocation and International Assignment Trends and Practices. EMERGING MARKETS: EGYPT Egypt’s strong links with western countries instead of the Egyptian pound (EGP) due to the latter’s loss in has made it a popular destination for many value. However, the gap between US and Egyptian currency is now beginning to narrow, which means landlords are more multinational organisations wanting a foothold willing to accept payments in EGP. into Africa and the Middle East. Like most emerging markets, Egypt still remains a Cairo. Cairo is the most frequent expatriate destination in Egypt and as such there is a high demand for rental properties. Over challenging location for some international the past 15 years there has been an increase in new compounds assignees with housing and security issues to meet expatriate demand. These are mainly located in New currently highlighted as key areas of focus. Cairo in the east of the city and in 6th of October City to the west. With a large number of international organisations having Key Challenge Areas head offices in 6th of October City and New Cairo, many assignees and their families choose to live in these areas, which Input from Cartus’ Destination Service Provider on the ground in have good access to schools and nearby markets. Other popular Egypt, highlights the following key areas for assignees: neighbourhoods for assignees include Maadi, Zamalek, Dokki, Security Garden City and Rehab City. Housing Lease Conditions. Leases are typically for a minimum of one year, Transportation although bi-annual leases are available for a slightly higher cost. -

Ramlet Boulaq Cairo,Egypt

HFC 1425 RAMLET BOULAQ CAIRO,EGYPT What can design do to start to legitimize ramlet boulaq in the eyes of surrounding cairo without denying those existing internal The Nile City Towers sit directly across the street that bounds Ramlet Boulaq on its west relationships? side. The towers have come with a great deal of controversy for the slum dwellers, often bazaar wall fresh food market referring to it as “the shadow they are living under,” as the owner of the towers shares wall a complicated relationship with the slum dwellers. While continually trying to acquire the slum’ s land for his own financial gain, the tower owner has also acknowledged those financial uncertainties at play within the slum as he employed many of Ramlet Boulaq’s residents to act as security for the towers during the 2011 revolution in Cairo. ? ramlet boulaq existing barrier proposed sits condition market 35 ft west of the towers the nile city towers has “Taking me out of here is like taking a fish out its grey water of his pond. I am as loyal to this land as I am serviced 11.4 to my country, Egypt.” These words - spoken by miles away. Mohamed, a Ramlet Boulaq resident - tell the true story of a slum often viewed as ‘something within the shadow.’ The people here value their community above all else. They have fought and will continue to fight for the land that they own and call home. It was crucial to honor these values - these people - when attempting to relieve some of those day to day struggles made worse by those physical living conditions. -

Importers Address Telephone Fax Make(S)

Importers Address Telephone Fax Make(s) Alpha Auto trading Josef tito st. Cairo +20 02-2940330 +20 02-2940600 Citroën cars Amal Foreign Trade Heliopolis, Cairo 11Fakhry Pasha St +20 02-2581847 +20 02-2580573 Lada Artoc Auto - Skoda 2, Aisha Al Taimouria st. Garden city Cairo +20 02-7944172 +20 02-7951622 Skoda Asia Motors Egypt 69, El Nasr Road, New Maadi, Cairo +20 02-5168223 +20 02-5168225 Asia Motors Atic/Arab Trading & 21 Talaat Harb St. Cairo +20 02-3907897 +20 02-3907897 Renault CV Insurance Center of 4, Wadi Al nil st. Mohandessin Cairo +20 02-3034775 +20 02-3468300 Peugeot Development & commerce - CDC - Wagih Abaza Chrysler Egypt 154 Orouba St. Heliopolis Cairo +20 02-4151872 +20 02-4151841 Chrysler Daewoo Corp Dokki, Giza- 18 El-Sawra St. Cairo +20 02-3370015 +20 02-3486381 Daewoo Daimler Chrysler Sofitel Tower, 28 th floor Conish el Nil, +20 02-5263800 +20 02-5263600 Mercedes, Egypt Maadi, Cairo Chrysler Egypt Engineering Shubra, Cairo-11 Terral el-ismailia +20 02-4266484 +20 02-4266485 Piaggio Industries Egyptan Automotive 15, Mourad St. Giza +20 02-5728774 +20 02-5733134 VW, Audi Egyptian Int'l Heliopolice Cairo Ismailia Desert Rd: Airport +20 02-2986582 +20 02-2986593 Jaguar Trading & Tourism / Rolls Royce Jaguar Egypt Ferrari El-Alamia ( Hashim Km 22 First of Cairo - Ismailia road +20 02-2817000 +20 02-5168225 Brouda Kancil bus ) Engineering Daher, Cairo 11 Orman +20 02-5890414 +20 02-5890412 Seat Automotive / SMG Porsche Engineering 89, Tereat Al Zomor Ard Al Lewa +20 02-3255363 +20 02-3255377 Musso, Seat , Automotive Co / Mohandessin Giza Porsche SMG Engineering for Cairo 21/24 Emad El-Din St. -

Reserve Great Apartment in New Heliopolis Near El Shorouk City

Reserve great apartment in new Heliopolis near el shorouk city Reference: 21037 Property Type: Apartments Property For: Sale Price: 675,000 EGP Country: Egypt Region: Cairo City: New Heliopolis Property Address: New Heliopolis cairo Price: 675,000 EGP Completion Date: 1970-01-01 Surface Area: 135 Unit Type: Flat Floor No: 03 No of Bedrooms: 2 No of Bathrooms: 1 Flooring: Cement Facing: North View: landscabe view Maintenance Fees: 5 % Deposit Union landlords Year Built: 2018 Real Estate License: residential Ownership Type: Registered Description: [tag]New Heliopolis[/tag] The total area of the city is 5888 acres made up of comprehensive residential places, services, recreational, educational, commercial, administrative, medical, social clubs, green open areas and the Golf. The Heliopolis Company for Development and housing was and is still the godfather of the city, providing all the facilities and services for the residents of the city including: Internal map of the city * Security gates * Integrated electricity network * Educational areas (schools- Institutes - Universities) The city is connected by the Cairo-Ismailia road from the north and by the CairoSuez road from the south. It also borders Madinaty to the south, El Shorouk to the west and Badr to the east. The city benefits from its connection to the Regional Ring Road which links it to all of Greater Cairo. The city is located 25 minutes from the district of Heliopolis and Nasr City Features: Elevator Balcony + View Master Bedroom Garage Close to the city Terrace Near Transport Luxury building Residential Area Quiet Area Shopping nearby Security Services . -

Mints – MISR NATIONAL TRANSPORT STUDY

No. TRANSPORT PLANNING AUTHORITY MINISTRY OF TRANSPORT THE ARAB REPUBLIC OF EGYPT MiNTS – MISR NATIONAL TRANSPORT STUDY THE COMPREHENSIVE STUDY ON THE MASTER PLAN FOR NATIONWIDE TRANSPORT SYSTEM IN THE ARAB REPUBLIC OF EGYPT FINAL REPORT TECHNICAL REPORT 11 TRANSPORT SURVEY FINDINGS March 2012 JAPAN INTERNATIONAL COOPERATION AGENCY ORIENTAL CONSULTANTS CO., LTD. ALMEC CORPORATION EID KATAHIRA & ENGINEERS INTERNATIONAL JR - 12 039 No. TRANSPORT PLANNING AUTHORITY MINISTRY OF TRANSPORT THE ARAB REPUBLIC OF EGYPT MiNTS – MISR NATIONAL TRANSPORT STUDY THE COMPREHENSIVE STUDY ON THE MASTER PLAN FOR NATIONWIDE TRANSPORT SYSTEM IN THE ARAB REPUBLIC OF EGYPT FINAL REPORT TECHNICAL REPORT 11 TRANSPORT SURVEY FINDINGS March 2012 JAPAN INTERNATIONAL COOPERATION AGENCY ORIENTAL CONSULTANTS CO., LTD. ALMEC CORPORATION EID KATAHIRA & ENGINEERS INTERNATIONAL JR - 12 039 USD1.00 = EGP5.96 USD1.00 = JPY77.91 (Exchange rate of January 2012) MiNTS: Misr National Transport Study Technical Report 11 TABLE OF CONTENTS Item Page CHAPTER 1: INTRODUCTION..........................................................................................................................1-1 1.1 BACKGROUND...................................................................................................................................1-1 1.2 THE MINTS FRAMEWORK ................................................................................................................1-1 1.2.1 Study Scope and Objectives .........................................................................................................1-1 -

Igcse Schools Contacts Learn with the World’S English Experts

IGCSE SCHOOLS CONTACTS LEARN WITH THE WORLD’S ENGLISH EXPERTS www.britishcouncil.org.eg MAADI DESTINATION MAADI, MOKATAM AND MADINAT AL SALAM School Principal IGCSE/GCSE Address Phones e-mail/website Coordinator Al Bashaer Schools Karima Shbana Basma Mohamed 13th district, 29706626/5 [email protected] CIPP Coordinator: Zahraa Al Maadi www.albashaerschools.net Wafaa Azmy Al Amal Language Mahmoud Samy Hanan Ayoub 61 St. Road10, 23786110 [email protected] School Maadi Maadi Amgad Language Ghada Amer Eman Naeem Nasr St., Takseem El Lasilky - 2516 6619/ [email protected] School New Maadi- behind Caltex 2755 0826 www.amgadschools.com Gas station Aton Language Sayed Abd Magda A.Halim El Hadaba Elwosta, 2727 0541/ [email protected] Schools El Mohsen El Mokattam 2727 0630/ 0102913021 British Dr. Yasser Aly Debra Moore Area 5, Segment 13, Zahraa 01142066662 www.ims-schools.com International CIPP coordinator: El-Maadi, behind Carrefour Modern School Kariem El-Sayed Rashad Ma’adi Children’s Toby Hime Gina Smith Building 10, Road 77 2358 5911 [email protected] Study Centre (corner of road 10) Maadi [email protected] Manara Language Hanaa Rafea Mona El Ofq El Gedid 2520 0204 [email protected] School Maadi El Dessouky St-Zahraa El Maadi, Maadi 2754 3505 Mokatam Mrs. Nivene Salah Street 9 in front of El Nasr 25082082 [email protected] Language School Gihan Galal El Din Buildings Mokattam 25082782 P.O. Box 116 Maadi Narmer Hala Tawfik/ Menna Abolenin 126, Misr Helwan 27635891/ [email protected] School Reham El Kammah Agricultura Road, Maadi 691/822/711 New Horizon Aicha Wassef Celia Ramous Zahraa El Maadi City,Zone 01226986441 www.newhorizon-eg.com School Marian Salama no.3 P.O. -

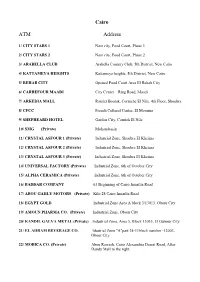

Cairo ATM Address

Cairo ATM Address 1/ CITY STARS 1 Nasr city, Food Court, Phase 1 2/ CITY STARS 2 Nasr city, Food Court, Phase 2 3/ ARABELLA CLUB Arabella Country Club, 5th District, New Cairo 4/ KATTAMEYA HEIGHTS Kattameya heights, 5th District, New Cairo 5/ REHAB CITY Opened Food Court Area El Rehab City 6/ CARREFOUR MAADI City Center – Ring Road, Maadi 7/ ARKEDIA MALL Ramlet Boulak, Corniche El Nile, 4th Floor, Shoubra 8/ CFCC French Cultural Center, El Mounira 9/ SHEPHEARD HOTEL Garden City, Cornish El Nile 10/ SMG (Private) Mohandessin 11/ CRYSTAL ASFOUR 1 (Private) Industrial Zone, Shoubra El Kheima 12/ CRYSTAL ASFOUR 2 (Private) Industrial Zone, Shoubra El Kheima 13/ CRYSTAL ASFOUR 3 (Private) Industrial Zone, Shoubra El Kheima 14/ UNIVERSAL FACTORY (Private) Industrial Zone, 6th of October City 15/ ALPHA CERAMICA (Private) Industrial Zone, 6th of October City 16/ BADDAR COMPANY 63 Beginning of Cairo Ismailia Road 17/ ABOU GAHLY MOTORS (Private) Kilo 28 Cairo Ismailia Road 18/ EGYPT GOLD Industrial Zone Area A block 3/13013, Obour City 19/ AMOUN PHARMA CO. (Private) Industrial Zone, Obour City 20/ KANDIL GALVA METAL (Private) Industrial Zone, Area 5, Block 13035, El Oubour City 21/ EL AHRAM BEVERAGE CO. Idustrial Zone "A"part 24-11block number -12003, Obour City 22/ MOBICA CO. (Private) Abou Rawash, Cairo Alexandria Desert Road, After Dandy Mall to the right. 23/ COCA COLA (Pivate) Abou El Ghyet, Al kanatr Al Khayreya Road, Kaliuob Alexandria ATM Address 1/ PHARCO PHARM 1 Alexandria Cairo Desert Road, Pharco Pharmaceutical Company 2/ CARREFOUR ALEXANDRIA City Center- Alexandria 3/ SAN STEFANO MALL El Amria, Alexandria 4/ ALEXANDRIA PORT Alexandria 5/ DEKHILA PORT El Dekhila, Alexandria 6/ ABOU QUIER FERTLIZER Eltabia, Rasheed Line, Alexandria 7/ PIRELLI CO. -

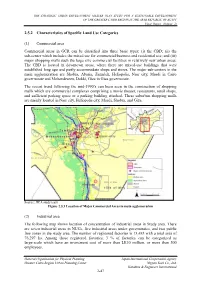

2.5.2 Characteristics of Specific Land Use Categories (1) Commercial

THE STRATEGIC URBAN DEVELOPMENT MASTER PLAN STUDY FOR A SUSTAINABLE DEVELOPMENT OF THE GREATER CAIRO REGION IN THE ARAB REPUBLIC OF EGYPT Final Report (Volume 2) 2.5.2 Characteristics of Specific Land Use Categories (1) Commercial area Commercial areas in GCR can be classified into three basic types: (i) the CBD; (ii) the sub-center which includes the mixed use for commercial/business and residential use; and (iii) major shopping malls such the large size commercial facilities in relatively new urban areas. The CBD is located in downtown areas, where there are mixed-use buildings that were established long ago and partly accommodate shops and stores. The major sub-centers in the main agglomeration are Shobra, Abasia, Zamalek, Heliopolis, Nasr city, Maadi in Cairo governorate and Mohandeseen, Dokki, Giza in Giza governorate. The recent trend following the mid-1990’s can been seen in the construction of shopping malls which are commercial complexes comprising a movie theater, restaurants, retail shops, and sufficient parking space or a parking building attached. These suburban shopping malls are mainly located in Nasr city, Heliopolis city, Maadi, Shobra, and Giza. Source: JICA study team Figure 2.5.3 Location of Major Commercial Areas in main agglomeration (2) Industrial area The following map shows location of concentration of industrial areas in Study area. There are seven industrial areas in NUCs, five industrial areas under governorates, and two public free zones in the study area. The number of registered factories is 13,483 with a total area of 76,297 ha. Among those registered factories, 3 % of factories can be categorized as large-scale which have an investment cost of more than LE10 million, or more than 500 employees. -

Directory of Development Organizations

EDITION 2010 VOLUME I.A / AFRICA DIRECTORY OF DEVELOPMENT ORGANIZATIONS GUIDE TO INTERNATIONAL ORGANIZATIONS, GOVERNMENTS, PRIVATE SECTOR DEVELOPMENT AGENCIES, CIVIL SOCIETY, UNIVERSITIES, GRANTMAKERS, BANKS, MICROFINANCE INSTITUTIONS AND DEVELOPMENT CONSULTING FIRMS Resource Guide to Development Organizations and the Internet Introduction Welcome to the directory of development organizations 2010, Volume I: Africa The directory of development organizations, listing 63.350 development organizations, has been prepared to facilitate international cooperation and knowledge sharing in development work, both among civil society organizations, research institutions, governments and the private sector. The directory aims to promote interaction and active partnerships among key development organisations in civil society, including NGOs, trade unions, faith-based organizations, indigenous peoples movements, foundations and research centres. In creating opportunities for dialogue with governments and private sector, civil society organizations are helping to amplify the voices of the poorest people in the decisions that affect their lives, improve development effectiveness and sustainability and hold governments and policymakers publicly accountable. In particular, the directory is intended to provide a comprehensive source of reference for development practitioners, researchers, donor employees, and policymakers who are committed to good governance, sustainable development and poverty reduction, through: the financial sector and microfinance, -

Egypt - Egypte

EGYPT - EGYPTE ADHERING ORGANIZATION Academy of Scientific Research and Technology 101 Kasr El-Eini Street Cairo NATIONAL COMMITTEE President: A. A.-A. TEALEB Secretary: N. M. H. ABOU-ASHOUR National Correspondents of the Associations IACS: D. M. AHMED IAG: M. M. M. IAGA: H. H. ODAH RABAH IAHS: N. M. H. ABOU- IAMAS: S. SHARAF EL IAPSO: S. SHARAF EL ASHOUR DIN DIN IASPEI: A. E. E. A. IAVCEI: A. A. BALDAWI MOHAMED ABOU-ASHOUR Ain Shams University T: 20 2 2287 0427 Prof. Dr. Nasser M. Hassan Faculty of Science T: 20 1 0510 7341 Member, IUGG Capacity Building & Geophysics Department F: 20 2 2484 2123 Education Committee Abbassia [email protected] Secretary, National Committee Cairo IAHS National Correspondent EGYPT AHMED General Director of Scientific Research T: 20 2 2682 0790 Mr. Darwish Mohamed Egyptian Meteorological Authority T: 20 2 183 513 4790 IACS National Correspondent P.O.B. 11784 [email protected] Kobry El Quobba Cairo EGYPT BALDAWI National Research Institute of Astronomy T: 20 1 00100 8089 Mr. Ahmed Ali and Geophysics F: 20 2 2554 8020 IAVCEI National Correspondent Helwan, Cairo [email protected] EGYPT MOHAMED National Research Institute of Astronomy T: 20 1 233669967 Mr. Abou El Ela Amin and Geophysics F: 20 2 25548020 IASPEI National Correspondent Helwan, Cairo [email protected] EGYPT ODAH National Research Institute of Astronomy T: 20 1 0698 10097 Mr. Hatem Hamdy and Geophysics F: 20 2 2554 8020 IAGA National Correspondent Helwan, Cairo [email protected] EGYPT RABAH National Research Institute of Astronomy T: 20 1 0106 2509 Mr.