Measuring the Effects of Austin's Transit-Oriented Development

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

FY 2016 Operating & Capital Budget & 5 Year Capital Improvement Plan

PROPOSED FY 2016 Operating & Capital Budget & 5 Year Capital Improvement Plan Capital Metropolitan Transportation Authority | Austin, Texas Capital Metropolitan Transportation Authority Proposed FY 2016 Operating and Capital Budget and Five Year Capital Improvement Plan Table of Contents Organization of the Budget Document ....................................................................................... 1 Transmittal Letter ....................................................................................................................... 2 Introduction History and Service Area ..................................................................................................... 4 Capital Metro Service Area Map .......................................................................................... 4 Community Information and Capital Metro Involvement ..................................................... 5 Benefits of Public Transportation......................................................................................... 6 Governance ......................................................................................................................... 7 Management ........................................................................................................................ 8 System Facility Characteristics ............................................................................................ 9 MetroRail Red Line Service Map ...................................................................................... -

Center for Advanced Multimodal Mobility Solutions and Education

Center for Advanced Multimodal Mobility Solutions and Education Project ID: 2017 Project 03 Forecasting Ridership for Commuter Rail in Austin Final Report by Scott Kilgore, M.S. The University of Texas at Austin and Randy Machemehl, Ph.D., P.E. (ORCID ID: https://orcid.org/0000-0002-4045-2023) Professor, Department of Civil and Environmental Engineering The University of Texas at Austin 301 E. Dean Keeton Street, Stop C1761, Austin, TX 78712 Phone: 1-512-471-4541; Email: [email protected] for Center for Advanced Multimodal Mobility Solutions and Education (CAMMSE @ UNC Charlotte) The University of North Carolina at Charlotte 9201 University City Blvd Charlotte, NC 28223 September 2018 ii ACKNOWLEDGMENTS This project was funded by the Center for Advanced Multimodal Mobility Solutions and Education (CAMMSE @ UNC Charlotte), one of the Tier I University Transportation Centers that were selected in this nationwide competition, by the Office of the Assistant Secretary for Research and Technology (OST-R), U.S. Department of Transportation (US DOT), under the FAST Act. The authors are also very grateful for all of the time and effort spent by DOT and industry professionals to provide project information that was critical for the successful completion of this study. DISCLAIMER The contents of this report reflect the views of the authors, who are solely responsible for the facts and the accuracy of the material and information presented herein. This document is disseminated under the sponsorship of the U.S. Department of Transportation University Transportation Centers Program and Capital Metropolitan Transportation Authority in the interest of information exchange. The U.S. -

Work Your Way. Every Day

WORK YOUR WAY. EVERY DAY. AUSTIN, TEXAS HIGHLAND MALL BLVD A DIVERSE MIX. Residential ACC Future Phase Residential Office/ 1 Office/ Commercial A VIBRANT ECOSYSTEM. 2 Commercial WILL DAVIS DR Office/ ACC DENSON DR Commercial Phase 1 WAY KINSLOW STEPHEN JONATHAN DR JONATHAN Austin’s newest opportunity Highland By The Numbers HAGE DR 35 Office/ is on its way. Residential Commercial St. John’s ACC ACC ACC Encampment Phase 2 Future Phase Commons Y LAND AREA SIGNATURE OPEN SPACE A W Retail Below ACC HIGHLAND CAMPUS DR CAMPUS HIGHLAND ACC D L Office/ E An energetic, walkable and transit-friendly 3 I F T Commercial JACOB FONTAINE LN A H S HIGHLAND A mixed-use neighborhood is emerging in the WILHELMINA DELCO DR ACRES NEW PARKS M STATION O Proposed H 3 ACC T 81 relocation heart of Austin. Highland brings together a rich Phase 2 Retail Below mix of uses with 865,000+ square feet of Class ACC Future ACC Phase Duval St Residential Corporate MIDDLE FISKVILLE RD A office space, hundreds of new apartments NEW TRAILS RESIDENTIAL Academic and shops—and a new high-tech instructional MILES UNITS CLAYTON LN space built in partnership with ACC, one of Office/ 1.25 1,320 4 Office/Commercial Commercial Retail Below the nation’s most forward-thinking community TIRADO ST Residential AIRPORT BLVD college systems. At Highland, you’re not just Residential OFFICE ACC - HIGH TECH CAMPUS ACC doing business the smart way; you’re doing Potential Retail Below business your way. ACC SF SF HQ 1,065,000 1,300,000 Parking Garage CLAYTON LN RETAIL POTENTIAL POPULATION Highland 1 Highland 2 Highland 3 Highland 4 290 150,000 SF 28,600 150K - 500K SF 250K SF 250K SF 65K SF E KOENIG LN Developable Class A Office Space Developable Class A Office Space Developable Class A Office Space Developable Class A Office Space Structure Parked: 4/1,000 Structure Parked: 4/1,000 Structure Parked: 4/1,000 Structure Parked: 5/1,000 Conceptual Plan Subject to Change REINLI ST HIGHLAND 2 BUILT FOR BUSINESS ALL YOU NEED—AND THEN SOME. -

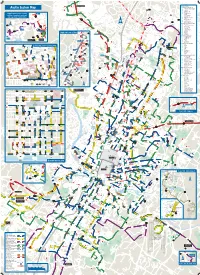

Austin System Map G 1L N

Leander Leander Park & Ride 983 986 987 183 S o u t h B e l l Bl vd 983 986 987 214 214 ne Blvd testo 1431 Whi r D n e re 214 rg e v E Main 214 St 1431 La ke li ne 214 B lv 983 Jonestown d Park & Ride 985 214 d el R ur a L 214 Bro nc o d R Bar-K anch L R n LeanderLeander Lago Vista HS Park & Ride 183 214 183 Rd ch Lakeline an Post Office 383 214 R K Co r- yo 983 987 Northwest a te B Tr 214 383 Park & Ride P a 214 383 s P 983 985 e e o d 985 983 985 987 c R 987 a d n e P d a r r k d V o lv a B F 214 B c l Lakeline v p a to n d es k a 383 a Mall L R d m Pace Bend h North Fork o Recreation Area L Plaza (LCRA-County) 1431 383 Forest North ES WalMart 983 1431 Lakeline Plaza 985 1 Jonestown 987 TOLL Park & Ride Target Lago Vista 214 Park & Ride D 183 aw Lakeline 214 n Rd Northwest Park & Ride ek ke Cre Routes 383, 983, 985 and 987 La Pkwy continue, see inset at left. Route Finder Grisham MS M i l Westwood HS l Local Service Routes (01-99) w 1 r i TOLL Austin System Map g 1L N. Lamar/S. Congress, via Lamar S Lago Vista h ho Anderson t r 1M N. -

TRANSIT ORIENTED DEVELOPMENT Opportunities for Affordability and Access in Austin

TRANSIT ORIENTED DEVELOPMENT Opportunities for Affordability and Access in Austin Image Credit: Endeavor Real Estate Group Transportation & Affordability Strategic Councils | AUGUST, 2020 Transit Oriented Development August 2020 Table of Contents Introduction ............................................................................................................. 1 Purpose ...................................................................................................................................... 1 ULI Austin .................................................................................................................................. 1 Strategic Councils ...................................................................................................................... 1 Methodology and Process ......................................................................................................... 1 Executive Summary .................................................................................................. 3 Background on Transit Oriented Development in Austin ........................................ 6 What Does TOD Include? ........................................................................................................... 6 Current Transit Service in Austin ................................................................................................ 6 Current Code and TOD Overlay .................................................................................................. 7 Current Affordable -

Capital Metro Rail-With-Trail Feasibility Study Downtown Austin

Capital Metro Rail-with-Trail Feasibility Study Downtown Austin to Leander, Texas June 12, 2007 Acknowledgements Capital Metro Board of Directors BOARD OF DIRECTORS:: Lee Walker, Chairman Commissioner Margaret Gomez, Vice Chairperson Alderman Fred Harless, Secretary Council Member Lee Leffingwell Council Member Brewster McCracken Mayor Pro Tem John Trevino Mayor, City of Leander; John Cowman Board Liaison: Gina Estrada Capital Metro Staff Team Randy Hume, Commuter Rail Project Office Julie Martin, Community Involvement Team Coordinator Bill LeJeune, Rail Operations Manager Consultant Team Lockwood, Andrews & Newnam, Inc. Bowman-Melton Associates, Inc. Alta Planning + Design, Inc. BICYCLING AND PEDESTRIAN FACILITIES FEASIBILITY STUDY Page ii Table of Contents Executive Summary 4. Facility Design Elements I. Study Area Overview: Introduction and Background Overview Trail Tread Width Existing Conditions Choice of Surfaces Adjacent Land Uses Trail / Roadway Crossings Future Rail Operations Intersection Prototypes Synopsis of Capital Metro Safety Guidelines Trailheads Trail Amenities 2. Public Input and Project Selection Process Trail Safety and Security Facility Operations and Maintenance Public Input Alignment Evaluation Process 5. Implementation Time Line and Cost Estimates Connection Opportunities Connection Constraints and Challenges Implementation Phasing Strategy Existing Conditions Planning Level Unit Cost Estimates Evaluation Criteria Potential Funding Potential Project Benefits Appendices 3. Recommended Plan A. Opportunities and Constraints Maps System Overview B. Trail Alignments Alternatives Evaluation Matrix Development Strategies C. Tables of Estimates of Potential Costs by Section Type Recommended Projects in Priority Order D. Detailed Project Layouts – South through North Needed Rights-of-Way E. Estimated Potential Project Costs BICYCLING AND PEDESTRIAN FACILITIES FEASIBILITY STUDY Page iii Executive Summary placeholders for future trail connections when that plan is adopted and advances toward more expedited implementation. -

Capmetro REMAP Campaign Creative-Ffa63b77.Pdf

Cap Remap More frequent + More reliable + Better Connected WHAT’S HAPPENING? “We’re changing more than half of our routes.” –CapMetro’s (Evil) Planners { Insert mild freakout } What had to be done • Educate staff and customers • Work with/direct outside on the changes contractors • Create and update signage • Create Promotional Items • Draw new route maps • Talk to customers face-to-face • Design brochures • Create Web sub-site Bonus: Implement new branding • Advertisement Designs wherever possible. • Presentation Boards In Numbers 3,000+ 1,800 68 Unique Temporary Redesigned Permanent Individual Route Signs Created Signs Installed Maps Produced 3X 22,000 75,000 More Local Frequent Customer Service Calls Unique Page Views Routes Added on launch week (In April 2018 alone) Information Display Units (IDUs) 341 produced to be posted at-stations New Permanent Signs 311Monday–Sunday Monday–Sunday311 122Monday–Sunday Weekdays 311 Stassney Stassney Four Points Stassney Limited Southbound to Southbound to Southpark To Lakeline Station Southpark ACC Riverside Riverside ACC Riverside ACC Meadows Meadows Park & Ride Monday — Sunday 10 10 Monday — Sunday 474-12000 20 1 - 4 7 4 474-12000 20 1 - 4 7 4 Southbound to Southpark The routes that Southbound to Downtown Meadows Monday — Sunday will serve the stop Monday — Saturday 10 (Late-Night) beginning June 3 485 are shown here. Temporary Notification Signs Our new permanent bus stop signage STOP ID 5836 The routes STOP ID 5669 JUNE 2018 SERVICE CHANGE JUNE 2018 SERVICE CHANGE JUNE 2018 SERVICE CHANGE JUNE 2018 SERVICE CHANGE has improvements to the information that will displayed at most stops. This includes: serve the stop THIS STOP IS ¡MIRE HACIA LOOK UP! ARRIBA! THIS STOP IS THIS STOP IS Routes on the new signs Las rutas que se detallan 1. -

550 Light Rail Time Schedule & Line Route

550 light rail time schedule & line map 550 Metro Rail Red Line View In Website Mode The 550 light rail line (Metro Rail Red Line) has 6 routes. For regular weekdays, their operation hours are: (1) 550 To Downtown: 5:41 AM - 5:30 PM (2) 550 To Howard: 7:20 AM - 11:22 AM (3) 550 To Kramer: 8:45 AM - 9:52 AM (4) 550 To Kramer: 3:50 PM - 7:00 PM (5) 550 To Lakeline: 8:19 AM - 12:22 PM (6) 550 To Leander: 6:55 AM - 7:21 PM Use the Moovit App to ƒnd the closest 550 light rail station near you and ƒnd out when is the next 550 light rail arriving. Direction: 550 To Downtown 550 light rail Time Schedule 9 stops 550 To Downtown Route Timetable: VIEW LINE SCHEDULE Sunday 9:15 PM - 11:05 PM Monday 5:41 AM - 5:30 PM Leander Park & Ride 800 N Us 183, Leander Tuesday 5:41 AM - 5:30 PM Lakeline Park & Ride Wednesday 5:41 AM - 5:30 PM 13625 Lyndhurst St, Austin Thursday 5:41 AM - 5:30 PM Howard Station Park & Ride Friday 5:41 AM - 11:09 PM Kramer Station Saturday 9:52 AM - 11:09 PM 2425 Kramer Ln, Austin Crestview Station 6932 N Lamar Blvd, Austin 550 light rail Info Highland Station Direction: 550 To Downtown 6404 1/2 Airport Blvd, Austin Stops: 9 Trip Duration: 62 min Mlk Jr Station Line Summary: Leander Park & Ride, Lakeline Park & 1702 Alexander Ave, Austin Ride, Howard Station Park & Ride, Kramer Station, Crestview Station, Highland Station, Mlk Jr Station, Plaza Saltillo Station Plaza Saltillo Station, Downtown Station 1501 5th St, Austin Downtown Station 505 E 4th St, Austin Direction: 550 To Howard 550 light rail Time Schedule 7 stops 550 To -

Park & Ride/Station Maps & Locations

Park & Ride/Station Maps & Locations 2243 Parking Available At Location 1 35 LEANDER 1 LEANDER STATION 183 PARK & RIDE HUTTO U.S. 183/FM 2243 79 800 U.S. 183 N 183A 550 MetroRail Red Line 1431 TOLL ROUND ROCK 620 2 CEDAR 985 Leander/Lakeline Direct PARK 987 Leander/Lakeline Express 3 2 ROUND ROCK PFLUGERVILLE TRANSIT CENTER 300 W. Bagdad Ave. 50 Round Rock/Howard Station 5 6 Ho 51 Round Rock Circulator 4 wa 620 1 rd 152 Round Rock Tech Ridge Limited 183 7 L n 980 North MoPac Express 8 d 35 2222 lv B 3 LAKELINE STATION r 360 9 a m PARK & RIDE a y L w MANOR p Lakeline Blvd./Lyndhurst St. y x E 290 w H c 14 13701 Lyndhurst St. s a 10 a P 11 x o e 214 Northwest Feeder T M 12 f o l 13 383 Research a 290 pit Ca 14 550 MetroRail Red Line 985 Leander/Lakeline Direct 183 973 987 Leander/Lakeline Express UT MLK Blvd CARTS Marble Falls 16 1 17 AUSTIN 4 PAVILION PARK & RIDE 360 18 vd 71 Bl U.S. 183/Oak Knoll ar 35 m 19 La 183 12400 U.S. 183 290 20 Congress 290 383 Research 21 B vd en Whit e Bl 71 981 Oak Knoll Express Austin- 982 Pavilion Express Bergstrom International Airport 5 HOWARD STATION 22 PARK & RIDE 3710 Howard Lane 50 Round Rock La Frontera 150 Round Rock La Frontera NORTHWEST AUSTIN 1431 ELGIN Whitestone 243 Wells Branch Blvd 95 550 MetroRail Red Line 1431 23 25 Main St 6 NEW LIFE PARK & RIDE d R 3200 Century Park Blvd d JONESTOWN r Main St o F 980 North MoPac Express s n 24 a 290 m h VOLENTE Volente Rd o L LAGO VISTA Destinations | Effective September 19, 2021 | capmetro.org | GO Line 512-474-1200 7 TECH RIDGE PARK & RIDE 12 CRESTVIEW STATION 19 PINNACLE PARK & RIDE 900 Center Ridge Dr. -

Approved FY2021 Operating and Capital Budget-Capital Metro

Capital Metropolitan Transportation Authority Approved FY2021 Operating and Capital Budget and Five-Year Capital Improvement Plan Table of Contents Organization of the Budget Document..................................................................................... i Introduction and Overview....................................................................................................... 1 Transmittal Letter.............................................................................................................. 2 Austin Area Information, History, and Economy ............................................................... 5 COVID-19 Impact.............................................................................................................. 7 Service Area and Region.................................................................................................. 9 Capital Metro System Map................................................................................................ 10 Community Information and Capital Metro Engagement.................................................. 11 Benefits of Public Transportation...................................................................................... 12 Governance....................................................................................................................... 13 Management..................................................................................................................... 14 System Facility Characteristics........................................................................................ -

Work Your Way. Every Day

WORK YOUR WAY. EVERY DAY. AUSTIN, TEXAS HIGHLAND MALL BLVD A DIVERSE MIX. Residential ACC Future Phase Residential Office/ 1 Office/ Commercial A VIBRANT ECOSYSTEM. 2 Commercial WILL DAVIS DR Office/ ACC DENSON DR Commercial Phase 1 WAY KINSLOW STEPHEN JONATHAN DR JONATHAN Austin’s newest opportunity Highland By The Numbers HAGE DR 35 Office/ is on its way. Residential Commercial St. John’s ACC ACC ACC Encampment PROPOSED CITY Phase 2 Future Phase Commons Y LAND AREA SIGNATURE OPEN SPACE A W OF AUSTIN PLANNING Retail Below ACC HIGHLAND CAMPUS DR CAMPUS HIGHLAND ACC D L Office/ E An energetic, walkable and transit-friendly I & DEVELOPMENT F T Commercial JACOB FONTAINE LN A H CENTER S HIGHLAND A mixed-use neighborhood is emerging in the WILHELMINA DELCO DR ACRES NEW PARKS M STATION O Proposed H 3 ACC T 81 relocation heart of Austin. Highland brings together a rich Phase 2 Retail Below mix of uses with 865,000+ square feet of Class ACC Future ACC Phase Duval St Residential Corporate MIDDLE FISKVILLE RD A office space, hundreds of new apartments NEW TRAILS RESIDENTIAL Academic and shops—and a new high-tech instructional MILES UNITS CLAYTON LN space built in partnership with ACC, one of Office/ 1.25 1,320 4 Office/Commercial Commercial Retail Below the nation’s most forward-thinking community TIRADO ST Residential AIRPORT BLVD college systems. At Highland, you’re not just Residential OFFICE ACC - HIGH TECH CAMPUS ACC doing business the smart way; you’re doing Potential Retail Below business your way. ACC SF SF HQ 1,065,000 1,300,000 Parking Garage CLAYTON LN RETAIL POTENTIAL POPULATION Highland 1 Highland 2 Highland 4 290 150,000 SF 28,600 150K - 500K SF 250K SF 65K SF E KOENIG LN Developable Class A Office Space Developable Class A Office Space Developable Class A Office Space Structure Parked: 4/1,000 Structure Parked: 4/1,000 Structure Parked: 5/1,000 Conceptual Plan Subject to Change REINLI ST HIGHLAND 2 BUILT FOR BUSINESS ALL YOU NEED—AND THEN SOME.