How N26 Is Changing Its Expansion Strategy, Competing for US Customers

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

SPEAKER BIOS | in SPEAKING ORDER Greg Fairlie Broadcaster Dubai One Presenter, Broadcaster, Multi Tasked Video Journalist &

SPEAKER BIOS | IN SPEAKING ORDER Greg Fairlie Broadcaster Dubai One Presenter, Broadcaster, Multi tasked Video Journalist & Business Communications Expert with a wealth of experience in the UK, Australia, Europe & MENA region. Bringing a warm, personable, informative and friendly approach to presenting, interviewing and drawing out the best of people in many diverse fields. Fully experienced in a live studio environment and on location. Specialties: Facilitating business programming for both TV and Radio stations. Managing teams within a broadcast unit. Presenting, producing, directing, filming and editing live and recorded TV & Radio content. Experience of anchoring in a live environment. Specialist in media training and presentation on-air delivery. Moderator at events. Magazine and newspaper features writer. Voice Over artist and Voice imaging. Experienced in using AVID inews, Final Cut Pro X, Adobe Premiere, audio editing software including soundtrack pro and Twisted Wave. His Excellency Hani Al Hamli Secretary General Dubai Economic Council (DEC) H.E. Hani Rashid Al Hamli is the Secretary General of the Dubai Economic Council (DEC) since 2006. The Council envisioned acting as the strategic partner for the Government of Dubai in economic-decision making. It provides policy recommendations and initiatives that enhance the sustainable economic development in the Emirate of Dubai. Prior to his service at DEC, Mr. Al Hamli held a number of senior positions in various government and private entities in Dubai such as the Executive Council-Government of Dubai, Dubai Chamber of Commerce and Industry, Investment & Development Authority, and Emirates Bank Group. Under his management of the DEC Secretariat, Mr. Al Hamli has realized many achievements for the DEC, notably the establishment of Dubai Competitiveness Center (DCC) in 2008, and the DEC has embraced the stated center from 2008-2013. -

Pbfixedincomedailyjan1716.Pdf

mashreq Fixed Income Trading Daily Market Update Sunday, January 17, 2015 Quote of the Day "Wealth consists not in having great possessions, but in having few wants." (Epictetus) Market Update Iran sanctions lifted after IAEA confirms compliance with the nuclear deal, US firms set to miss out as US sanctions remain International sanctions on Iran have been lifted after IAEA, the UN nuclear watchdog confirmed the country had complied with a deal designed to prevent it developing nuclear weapons. The International Atomic Energy Agency concluded that the Islamic Republic had curbed its ability to develop an atomic weapon as required under an accord with world powers. The US and five other nations agreed in July’s accord to lift sanctions on Iran “simultaneously with the IAEA-verified implementation” of the deal. “Iran has undertaken significant steps that many people doubted would ever come to pass,” clearing the way for sanctions to end, US Secretary of State John Kerry said in Vienna late on Saturday after Iran’s compliance with the agreement was certified. Still, he said the accord “doesn’t wipe away all of the concerns” of the international community, and “verification remains, as it always has been, the backbone of this agreement." The EU foreign policy chief, Federica Mogherini, said the deal would contribute to improved regional and international peace and security. “Relations between Iran and the IAEA now enter a new phase. It is an important day for the international community,” Yukiya Amano, director general of the agency, said in a statement. “This paves the way for the IAEA to begin verifying and monitoring Iran’s nuclear-related commitments.” Ahead of the announcement Iran freed four Iranian-Americans as part of a prisoner exchange with the US that had been negotiated in secret for more than a year. -

February 2019

The definitive source of news and analysis of the global fintech sector | February 2019 www.bankingtech.com SUPERSTRUCTURES Fintech reaches new heights CASE STUDY: CITIZENS BANK US heavyweight pivots for digital era FOOD FOR THOUGHT: CAREER CHOICES The Venn diagram of doom FINTECH FUTURES IN THIS ISSUE THEM US Contents NEWS 04 The latest fintech news from around the globe: the good, the bad and the ugly. 18 Banking Technology Awards The glamour, the winners and the celebrations. 23 Focus: intraday liquidity Are banks ready to meet the ECB’s latest expectations? 24 Interview: Pavel Novak, Zonky P2P lender on a “mission possible”. 26 Focus: data How DNB uses data to reconnect with customers. 30 Analysis: openfunds Admirable data standardisation efforts for the funds industry. 32 Case study: Citizens Bank US’s 13th largest bank embraces digital era. 38 Food for thought Making career choices and the Venn diagram of doom. They struggle with Fintech complexity. We see straight to your goal. We leverage proprietary knowledge and technology to solve complex regulatory challenges, create new products 40 Comment What would a recession mean for fintech? and build businesses. Our unique “one fi rm” approach brings to bear best-in-class talent from our 32 offi ces worldwide—creating teams that blend global reach and local knowledge. Looking for a fi rm that can help keep 42 Interview: Javier Santamaría, EPC your business moving in the right direction? Visit BCLPlaw.com to learn more. Happy one year anniversary, SEPA Instant Credit Transfer! REGULARS 44 -

SBFM Report 2021

Small Business Finance Markets 2020/21 british-business-bank.co.uk Contents Foreword 3 Part B: Market developments 54 Executive summary 6 Small businesses and their use Introduction 10 of finance Aggregate flow and stock of 2.1 Macro-economic developments 55 finance to smaller businesses 12 2.2 SME business population 61 2.3 Use of external finance 67 Part A: The impact of Covid-19 on small business finance markets Finance products and the implications for 2021 15 2.4 Bank lending 75 1.1 Demand and supply of SME 2.5 Challenger and specialist banks 82 finance during the pandemic 16 2.6 Equity finance 89 1.2 Expectations for demand and 2.7 Private debt 102 supply in 2021 29 2.8 Asset finance 111 1.3 Finance can help the UK build 2.9 Invoice finance and back better 41 asset-based lending 116 1.4 The importance of and 2.10 Marketplace lending 121 challenges faced by alternative finance providers in 2020 47 Glossary 126 Endnotes 132 2 0.0 The British Business Bank’s mission is Foreword to make finance markets work better so smaller businesses across the UK can prosper and grow. Small Business Finance Markets 2020/21 Foreword Our unique position at the intersection of Covid-19 has had a devastating effect on the UK government and financial markets enables economy, particularly on the all-important small business sector that accounts for 61% of private sector us to identify and reduce imbalances in employment. It has also had a profound influence on access to finance; create a more diverse the operation of the finance markets serving small market; and increase the supply of finance businesses. -

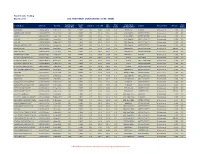

Fixed Income Trading May 10, 2016 USD INVESTMENT GRADE ISSUES (LONG TERM)

Fixed Income Trading May 10, 2016 USD INVESTMENT GRADE ISSUES (LONG TERM) Outstanding Coupon Indic. Offer Credit Rating Risk Security Name ISIN Code Maturity Coupon % Indic. Bid Country Payment Rank Min. Size Amount (Mio) Type Offer Yield % S&P/Moody/Fitch Rating AGRIUM INC US008916AP31 15-Mar-2025 550 FIXED 3.38 99.08 99.08 3.50 BBB/Baa2/- CANADA Sr Unsecured 2,000 P3 AMERICAN INTL GROUP US026874DD67 10-Jul-2025 1250 FIXED 3.75 101.42 101.42 3.56 A-/Baa1/BBB+ UNITED STATES Sr Unsecured 2,000 P3 AON PLC US00185AAF12 14-Jun-2024 600 FIXED 3.50 101.66 101.66 3.26 A-/Baa2/BBB+ UNITED STATES Sr Unsecured 2,000 P3 AT&T INC US00206RBN17 1-Dec-2022 1500 FIXED 2.63 99.33 99.33 2.74 BBB+/Baa1/A- UNITED STATES Sr Unsecured 2,000 P3 AT&T INC US00206RCN08 15-May-2025 5000 FIXED 3.40 101.43 101.43 3.21 BBB+/Baa1/A- UNITED STATES Sr Unsecured 2,000 P3 BANK OF AMERICA CORP US06051GEU94 11-Jan-2023 4250 FIXED 3.30 102.16 102.16 2.94 BBB+/Baa1/A UNITED STATES Sr Unsecured 2,000 P3 BARCLAYS PLC US06738EAE59 16-Mar-2025 2000 FIXED 3.65 97.62 97.62 3.97 BBB/Baa3/A UNITED KINGDOM Sr Unsecured 200,000 P3 BARCLAYS PLC US06738EAN58 12-Jan-2026 2500 FIXED 4.38 100.83 100.83 4.27 BBB/Baa3/A UNITED KINGDOM Sr Unsecured 200,000 P3 BARRICK GOLD CORP US067901AQ17 1-May-2023 730 FIXED 4.10 103.55 103.55 3.52 BBB-/Baa3/- CANADA Sr Unsecured 2,000 P3 BHP BILLITON FIN USA LTD US055451AQ16 24-Feb-2022 1000 FIXED 2.88 100.95 101.92 2.52 A/A3/A+ AUSTRALIA Sr Unsecured 2,000 P3 BP CAPITAL MARKETS PLC US05565QCB23 6-Nov-2022 1000 FIXED 2.50 98.26 98.26 2.80 A-/A2/A UNITED KINGDOM -

Wealth Management: Investment Views

Investment views Challenging the challengers Issue 7 | Second quarter 2020 Who are the challengers? Revolut, Monzo, Starling and N26 are becoming household names across Europe. These businesses are part of a new wave of challenger banks that have disrupted retail banking services, divided critics and amassed millions of users. They have attracted global headlines in the last two years as they enjoy compound annual growth rates nearing 45%1. In a recent conversation with our financial William Haggard Head of Investment Insights analyst Willis Palermo, we explored three key issues for Europe’s fintech fighters: 1. What does the emergence of challenger banks mean for established banks? 2. How are banks responding to the Covid-19 crisis? 3. Where do we stand on investing in challenger banks today? The following is an edited transcript of the interview, which you can listen to in full by clicking here. Willis Palermo Financial Analyst In with the new, out with the old? A key ingredient of challenger banks’ success has been their user-friendly mobile interfaces. Talk us through the user experience. Download the online app on your phone, create your login details, send over a picture of your ID card and you are up and running with a bank account. Many of us have joined this new wave of quick and easy challenger banks that have sprung up to facilitate everyday payments and foreign exchange transactions. The ease and simplicity of joining these banks (see Figure 1) is particularly popular with younger generations. In the UK, Monzo boasts 68% of users aged between 18 and 34, while the same age group makes up more than 50% of Revolut and N26’s customers. -

Svenska Handelsbanken

Annual Report 2001 Svenska Handelsbanken THE ANNUAL GENERAL MEETING OF SVENSKA HANDELSBANKEN will be held at the Grand Hôtel, Vinterträdgården, Royal entrance, Stallgatan 4, Stockholm, at 10.00 a.m. on Tuesday, 23 April 2002. NOTICE OF ATTENDANCE AT ANNUAL GENERAL MEETING Shareholders wishing to attend the Meeting must: • be entered in the Register of Shareholders kept by VPC AB (Swedish Central Securities Depository and Clearing Organisation), on or before Friday, 12 April 2002, and • give notice of attendance to the Chairman's Office at the Head Office of the Bank, Kungsträdgårdsgatan 2, SE-106 70 Stockholm, telephone +46 8 701 19 84, or via the Internet www.handelsbanken.se/bolagsstamma (Swedish only), by 3 p.m. on Wednesday, 17 April 2002. In order to be entitled to take part in the Meeting, any share- holders whose shares are nominee-registered must also request a temporary entry in the register of shareholders kept by the VPC. Shareholders must notify the nominee about this well before 12 April 2002, when this entry must have been effected. DIVIDEND The Board of Directors recommends that the record day for the dividend be Friday, 26 April 2002. If the Annual General Meeting votes in accordance with this recommendation, the VPC expects to be able to send the dividend to shareholders on Thursday, 2 May 2002. PUBLICATION DATES FOR INTERIM REPORTS January–March 22 April 2002 January–June 20 August 2002 January–September 22 October 2002 Svenska Handelsbanken AB (publ) Registered no. 502007-7862 www.handelsbanken.se Contents HIGHLIGHTS OF THE YEAR 2 THE GROUP CHIEF EXECUTIVE’S COMMENTS.......... -

(2019). Bank X, the New Banks

BANK X The New New Banks Citi GPS: Global Perspectives & Solutions March 2019 Citi is one of the world’s largest financial institutions, operating in all major established and emerging markets. Across these world markets, our employees conduct an ongoing multi-disciplinary conversation – accessing information, analyzing data, developing insights, and formulating advice. As our premier thought leadership product, Citi GPS is designed to help our readers navigate the global economy’s most demanding challenges and to anticipate future themes and trends in a fast-changing and interconnected world. Citi GPS accesses the best elements of our global conversation and harvests the thought leadership of a wide range of senior professionals across our firm. This is not a research report and does not constitute advice on investments or a solicitations to buy or sell any financial instruments. For more information on Citi GPS, please visit our website at www.citi.com/citigps. Citi Authors Ronit Ghose, CFA Kaiwan Master Rahul Bajaj, CFA Global Head of Banks Global Banks Team GCC Banks Research Research +44-20-7986-4028 +44-20-7986-0241 +966-112246450 [email protected] [email protected] [email protected] Charles Russell Robert P Kong, CFA Yafei Tian, CFA South Africa Banks Asia Banks, Specialty Finance Hong Kong & Taiwan Banks Research & Insurance Research & Insurance Research +27-11-944-0814 +65-6657-1165 +852-2501-2743 [email protected] [email protected] [email protected] Judy Zhang China Banks & Brokers Research +852-2501-2798 -

HOW CHALLENGER BANKS CAN GROW PROFITABLY CONTENTS Introduction Challengers Everywhere

Challenge Accepted TOWARDS SUSTAINABILITY: HOW CHALLENGER BANKS CAN GROW PROFITABLY CONTENTS Introduction Challengers Everywhere Challenges Facing Challengers Data-Led Personalisation Products Challenger in Focus: tonik How Alternative Data Can Help Challengers Thrive Challenger Banking’s Future Many challengers made everyday banking as seamless Introduction and pain-free as posting on social media. And, from the middle part of the past decade, Challenger banks seemed to be on solid ground as the challenger banking took more and more accounts previous decade ended. away from traditional retail banks. The 2010s were an era where the adoption of digital Until the pandemic. channels skyrocketed, mobile networks vastly improved with the shift from 3G to 5G, and emerging middle classes grew across developing markets. By the middle of the decade, the shock of the GFC was beginning to wane, and innovators and consumers were implementing new practices that grew entire industries. Social media became a source of influence and impact across politics, economics, and cross- border commerce. And eCommerce grew in prominence and popularity, as Chinese manufacturing helped global retailers to reach shoppers in almost every corner of the globe. Challenger banking fitted nicely into this new era of speed, convenience, and aspirational commerce. It spoke to demographics who felt misunderstood by legacy banks. 1 There are over 200 challenger banks worldwide, who have raised $15 billion. — Singapore Fintech Association and Bain Consulting Group report popular challenger bank, with nearly 35 million CHALLENGERS customers on its books. Why have so many challenger banks emerged in such a short space of time? And what do consumers think EVERYWHERE about challenger banks? A recent Kearney survey of UK consumers offers some clues. -

SWIFT Gpi Delivering the Future of Cross-Border Payments, Today SWIFT Gpi SWIFT Gpi

SWIFT gpi Delivering the future of cross-border payments, today SWIFT gpi SWIFT gpi SWIFT gpi 4 SWIFT is an innovative The Concept 8 technology company. As an industry cooperative, we listen The Tracker 10 Delivering and respond to the evolving The Observer 12 needs of our Community. The Directory 14 Part of our core mission is to Market infrastructures 16 the future of bring the financial community The Roadmap 18 together to work collaboratively to shape market practice, Enable digital transformation 22 define standards and debate Explore new technology 24 cross-border issues of mutual interest. payments, Innovation is an ongoing process, and through our R&D programmes and initiatives such as SWIFTLab, Innotribe, today and the SWIFT Institute, SWIFT is ideally placed to offer insights into the future of global financial technology and work with our Community to make real world change really happen. 2 3 SWIFT gpi SWIFT gpi SWIFT gpi SWIFT global payments innovation (gpi) In its first phase, SWIFT gpi focuses on business-to-business At Citi, we welcome the launch of As an early member of SWIFT dramatically improves the customer payments. It is designed to help corporates grow their international SWIFT gpi – we see this as a key gpi, Bank of China successfully experience in cross-border payments business, improve supplier initiative in evolving how cross- completed the gpi pilot and by increasing the speed, transparency relationships, and achieve greater border payments are transacted. was one of the first banks to treasury efficiencies. Thanks to SWIFT The time is right for the industry to go live. -

RECOMMENDED ALL-SHARE OFFER for VIRGIN MONEY HOLDINGS (UK) PLC by CYBG PLC Summary

THE INFORMATION CONTAINED WITHIN THIS ANNOUNCEMENT IS DEEMED BY CYBG AND VIRGIN MONEY TO CONSTITUTE INSIDE INFORMATION AS STIPULATED UNDER THE MARKET ABUSE REGULATION NO 596/2014. UPON THE PUBLICATION OF THIS ANNOUNCEMENT VIA REGULATORY INFORMATION SERVICE, THIS INSIDE INFORMATION IS NOW CONSIDERED TO BE IN THE PUBLIC DOMAIN NOT FOR RELEASE, PUBLICATION OR DISTRIBUTION, IN WHOLE OR IN PART, IN, INTO OR FROM ANY JURISDICTION WHERE TO DO SO WOULD CONSTITUTE A VIOLATION OF THE RELEVANT LAWS OF THAT JURISDICTION THIS ANNOUNCEMENT IS AN ADVERTISEMENT AND NOT A PROSPECTUS OR PROSPECTUS EQUIVALENT DOCUMENT AND INVESTORS SHOULD NOT MAKE ANY INVESTMENT DECISION IN RELATION TO THE NEW CYBG SHARES EXCEPT ON THE BASIS OF INFORMATION IN THE PROSPECTUS AND THE SCHEME DOCUMENT WHICH ARE PROPOSED TO BE PUBLISHED IN DUE COURSE FOR IMMEDIATE RELEASE 18 JUNE 2018 RECOMMENDED ALL-SHARE OFFER FOR VIRGIN MONEY HOLDINGS (UK) PLC BY CYBG PLC Summary The Boards of CYBG PLC ("CYBG") and Virgin Money Holdings (UK) plc ("Virgin Money") are pleased to announce that they have agreed the terms of a recommended all-share offer to be made by CYBG for Virgin Money (the "Offer") to create the UK's first true national banking competitor to the status quo. Under the terms of the Offer, Virgin Money Shareholders will receive: 1.2125 New CYBG Shares in exchange for each Virgin Money Share Based on the Closing Price of 306 pence per CYBG Share on 15 June 2018 (being the last Business Day before the date of this Announcement), the Offer values each Virgin Money Share at 371 pence and Virgin Money's ordinary shares on a fully diluted basis at approximately £1.7 billion, representing a premium of: ‒ 19 per cent. -

Participant List

Participant List 10/20/2019 8:45:44 AM Category First Name Last Name Position Organization Nationality CSO Jillian Abballe UN Advocacy Officer and Anglican Communion United States Head of Office Ramil Abbasov Chariman of the Managing Spektr Socio-Economic Azerbaijan Board Researches and Development Public Union Babak Abbaszadeh President and Chief Toronto Centre for Global Canada Executive Officer Leadership in Financial Supervision Amr Abdallah Director, Gulf Programs Educaiton for Employment - United States EFE HAGAR ABDELRAHM African affairs & SDGs Unit Maat for Peace, Development Egypt AN Manager and Human Rights Abukar Abdi CEO Juba Foundation Kenya Nabil Abdo MENA Senior Policy Oxfam International Lebanon Advisor Mala Abdulaziz Executive director Swift Relief Foundation Nigeria Maryati Abdullah Director/National Publish What You Pay Indonesia Coordinator Indonesia Yussuf Abdullahi Regional Team Lead Pact Kenya Abdulahi Abdulraheem Executive Director Initiative for Sound Education Nigeria Relationship & Health Muttaqa Abdulra'uf Research Fellow International Trade Union Nigeria Confederation (ITUC) Kehinde Abdulsalam Interfaith Minister Strength in Diversity Nigeria Development Centre, Nigeria Kassim Abdulsalam Zonal Coordinator/Field Strength in Diversity Nigeria Executive Development Centre, Nigeria and Farmers Advocacy and Support Initiative in Nig Shahlo Abdunabizoda Director Jahon Tajikistan Shontaye Abegaz Executive Director International Insitute for Human United States Security Subhashini Abeysinghe Research Director Verite