Aviation Activity Forecasts

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Appendix 25 Box 31/3 Airline Codes

March 2021 APPENDIX 25 BOX 31/3 AIRLINE CODES The information in this document is provided as a guide only and is not professional advice, including legal advice. It should not be assumed that the guidance is comprehensive or that it provides a definitive answer in every case. Appendix 25 - SAD Box 31/3 Airline Codes March 2021 Airline code Code description 000 ANTONOV DESIGN BUREAU 001 AMERICAN AIRLINES 005 CONTINENTAL AIRLINES 006 DELTA AIR LINES 012 NORTHWEST AIRLINES 014 AIR CANADA 015 TRANS WORLD AIRLINES 016 UNITED AIRLINES 018 CANADIAN AIRLINES INT 020 LUFTHANSA 023 FEDERAL EXPRESS CORP. (CARGO) 027 ALASKA AIRLINES 029 LINEAS AER DEL CARIBE (CARGO) 034 MILLON AIR (CARGO) 037 USAIR 042 VARIG BRAZILIAN AIRLINES 043 DRAGONAIR 044 AEROLINEAS ARGENTINAS 045 LAN-CHILE 046 LAV LINEA AERO VENEZOLANA 047 TAP AIR PORTUGAL 048 CYPRUS AIRWAYS 049 CRUZEIRO DO SUL 050 OLYMPIC AIRWAYS 051 LLOYD AEREO BOLIVIANO 053 AER LINGUS 055 ALITALIA 056 CYPRUS TURKISH AIRLINES 057 AIR FRANCE 058 INDIAN AIRLINES 060 FLIGHT WEST AIRLINES 061 AIR SEYCHELLES 062 DAN-AIR SERVICES 063 AIR CALEDONIE INTERNATIONAL 064 CSA CZECHOSLOVAK AIRLINES 065 SAUDI ARABIAN 066 NORONTAIR 067 AIR MOOREA 068 LAM-LINHAS AEREAS MOCAMBIQUE Page 2 of 19 Appendix 25 - SAD Box 31/3 Airline Codes March 2021 Airline code Code description 069 LAPA 070 SYRIAN ARAB AIRLINES 071 ETHIOPIAN AIRLINES 072 GULF AIR 073 IRAQI AIRWAYS 074 KLM ROYAL DUTCH AIRLINES 075 IBERIA 076 MIDDLE EAST AIRLINES 077 EGYPTAIR 078 AERO CALIFORNIA 079 PHILIPPINE AIRLINES 080 LOT POLISH AIRLINES 081 QANTAS AIRWAYS -

363 Part 238—Contracts With

Immigration and Naturalization Service, Justice § 238.3 (2) The country where the alien was mented on Form I±420. The contracts born; with transportation lines referred to in (3) The country where the alien has a section 238(c) of the Act shall be made residence; or by the Commissioner on behalf of the (4) Any country willing to accept the government and shall be documented alien. on Form I±426. The contracts with (c) Contiguous territory and adjacent transportation lines desiring their pas- islands. Any alien ordered excluded who sengers to be preinspected at places boarded an aircraft or vessel in foreign outside the United States shall be contiguous territory or in any adjacent made by the Commissioner on behalf of island shall be deported to such foreign the government and shall be docu- contiguous territory or adjacent island mented on Form I±425; except that con- if the alien is a native, citizen, subject, tracts for irregularly operated charter or national of such foreign contiguous flights may be entered into by the Ex- territory or adjacent island, or if the ecutive Associate Commissioner for alien has a residence in such foreign Operations or an Immigration Officer contiguous territory or adjacent is- designated by the Executive Associate land. Otherwise, the alien shall be de- Commissioner for Operations and hav- ported, in the first instance, to the ing jurisdiction over the location country in which is located the port at where the inspection will take place. which the alien embarked for such for- [57 FR 59907, Dec. 17, 1992] eign contiguous territory or adjacent island. -

March 2018 REFLECTIONS the Newsletter of the Northwest Airlines History Center Dedicated to Preserving the History of a Great Airline and Its People

Vol.16, no.1 nwahistory.org facebook.com/NorthwestAirlinesHistoryCenter March 2018 REFLECTIONS The Newsletter of the Northwest Airlines History Center Dedicated to preserving the history of a great airline and its people. NORTHWEST AIRLINES 1926-2010 ______________________________________________________________________________________________________ THE QUEEN OF THE SKIES Personal Retrospectives by Robert DuBert It's hard to believe that they are gone. Can it be possible that it was 50 years ago this September that this aircraft made its first public appearance? Are we really all so, ahem, elderly that we Photo: True Brand, courtesy Vincent Carrà remember 1968 as if it were yesterday? This plane had its origins in 1964, when Boeing began work on a proposal for the C-5A large military airlifter contract, and after Lockheed won that contest, Boeing considered a commercial passenger version as a means of salvaging the program. Urged on by Pan Am president Juan Trippe, Boeing in 1965 assigned a team headed by Chief Engineer Joe Sutter to design a large new airliner, although Boeing at the time was really more focused on its supersonic transport (SST) program. A launch customer order from Pan Am on April 13, 1966 for twenty five aircraft pushed Sutter's program into high gear, and in a truly herculian effort, Joe Sutter and his Boeing team, dubbed “The Incredibles,” brought the program from inception on paper to the public unveiling of a finished aircraft in the then unheard of time of 29 months. We're talking, of course, about the legendary and incomparable Boeing 747. THE ROLLOUT It was a bright, sunny morning on Monday, Sept. -

City of Phoenix Aviation Department Sky Harbor International Airport Financial Management Division Monthly Statistical Reports - November 2016 Table of Contents

City of Phoenix Aviation Department Sky Harbor International Airport Financial Management Division Monthly Statistical Reports - November 2016 Table of Contents Reports: Graphs: 1 Passengers, Cargo, and Aircraft Operations 1 Domestic Enplaned I Deplaned Passengers Terminal 2 2 Passenger Activity Report 2 Domestic Enplaned I Deplaned Passengers Terminal 3 3 Passenger and Activity Worksheet November 2016 3 Domestic Enplaned I Deplaned Passengers Terminal 4 4 Passenger and Activity Worksheet November 2015 4 Total Domestic Enplaned I Deplaned Passengers 5 Enplaned Passengers by Carrier for Fiscal Year 2016/17 5 Total International Enplaned I Deplaned Passengers 6 Deplaned Passengers by Carrier for Fiscal Year 2016/17 6 Total Enplaned I Deplaned Passengers 7 Total Passengers by Carrier for Fiscal Year 2016/17 7 Total Enplaned I Deplaned Cargo (in Tons) 8 Enplaned Passengers by Carrier for Calendar Year 2016 8 Sky Harbor International Airport Aircraft Operations 9 Deplaned Passengers by Carrier for Calendar Year 2016 9 Deer Valley Airport Aircraft Operations 10 Total Passengers by Carrier for Calendar Year 2016 1O Goodyear Airport Aircraft Operations 11 Airline Landing Weights -All Airlines for Fiscal Year 2016/17 12 Airline Landing Weights - Rates & Charges Airlines Only for Fiscal Year 2016/17 PASSENGERS, CARGO, AND AIRCRAFT OPERATIONS AT PHOENIX AIRPORTS: November 2016 Fis cal YTD Fis ca l YTD Calenda r YTD ___ _ _._ 2016 2015 %Cha ___. _. ___._. __ %Chg I I 201 6 T2 153,849 149,936 2.6% 646,914 592,535 9.2% 1,585,013 1,359,302 16.6% T3 -

Anarchy in the Airways Joseph C

View metadata, citation and similar papers at core.ac.uk brought to you by CORE provided by DigitalCommons@Florida International University Hospitality Review Volume 5 Article 10 Issue 1 Hospitality Review Volume 5/Issue 1 1-1-1987 Anarchy In The Airways Joseph C. Von Kornfeld University of Nevada, Las Vegas, [email protected] Follow this and additional works at: http://digitalcommons.fiu.edu/hospitalityreview Recommended Citation Von Kornfeld, Joseph C. (1987) "Anarchy In The Airways," Hospitality Review: Vol. 5: Iss. 1, Article 10. Available at: http://digitalcommons.fiu.edu/hospitalityreview/vol5/iss1/10 This work is brought to you for free and open access by FIU Digital Commons. It has been accepted for inclusion in Hospitality Review by an authorized administrator of FIU Digital Commons. For more information, please contact [email protected]. Anarchy In The Airways Abstract In his dialogue - Anarchy In The Airways - Joseph C. Von Kornfeld, Assistant Professor, College of Hotel Administration, University of Nevada, Las Vegas initially states: “Deregulation of the airline industry has brought about financial vulnerability for the traveling public. The uthora analyzes the situation since that point in time and makes recommendations for some solutions.” In this article, Assistant Professor Von Kornfeld, first defines the airline industry in its pre-regulated form. Then he goes into the ramifications and results of deregulating the industry, both in regards to the consumer, and in deregulation’s impact on the airlines themselves. “The most dramatic consequence of the pressures and turbulence of airline deregulation has been the unprecedented proliferation of airline bankruptcies,” Von Kornfeld informs. -

Here Aspiring Pilots Are Well Prepared to Make the Critical Early Career and Lifestyle Choices Unique to the Aviation Industry

August 2021 Aero Crew News Your Source for Pilot Hiring and More.. START PREPARING FOR YOUR APPROACH INTO RETIREMENT Designed to help you understand some of the decisions you will need to make as you get ready for your approach into retirement, our free workbook includes 5 key steps to begin preparing for life after flying. You’ll discover more about: • How you will fund your retirement “paycheck” • What your new routine might look like • If your investment risk needs to be reassessed • And much more Dowload your free Retirement Workbook » 800.321.9123 | RAA.COM Aero Crew News 2021 PHOTO CONTEST Begins Now! This year’s theme is Aviation Weather! Submit your photos at https://rebrand.ly/ACN_RAA_Photo_Contest Official rules can be found at https://rebrand.ly/ACN-RAA-Rules. Jump to each section Below contents by clicking on the title or photo. August 2021 37 50 41 56 44 Also Featuring: Letter from the Publisher 8 Aviator Bulletins 11 Mortgage - The Mortgage Process Part 2 52 Careers - Routines and Repetition 54 4 | Aero Crew News BACK TO CONTENTS the grid US Cargo US Charter US Major Airlines US Regional Airlines ABX Air Airshare Alaska Airlines Air Choice One Alaska Seaplanes GMJ Air Shuttle Allegiant Air Air Wisconsin Ameriflight Key Lime Air American Airlines Cape Air Atlas Air/Southern Air Omni Air International Delta Air Lines CommutAir FedEx Express Ravn Air Group Frontier Airlines Elite Airways iAero Airways XOJET Aviation Hawaiian Airlines Endeavor Air Kalitta Air JetBlue Airways Envoy Key Lime Air US Fractional Southwest Airlines ExpressJet Airlines UPS FlexJet Spirit Airlines GoJet Airlines NetJets Sun Country Airlines Grant Aviation US Cargo Regional PlaneSense United Airlines Horizon Air Empire Airlines Key Lime Air Mesa Airlines ‘Ohana by Hawaiian Piedmont Airlines PSA Airlines Republic Airways The Grid has moved online. -

Empire Airlines, Inc. Contact: Colleen Hennessey Marketing & Sales Manager Empire Unmanned, LLC Tel: (208) 627-8041 Email: [email protected]

Empire Airlines, Inc. Contact: Colleen Hennessey Marketing & Sales Manager Empire Unmanned, LLC Tel: (208) 627-8041 Email: [email protected] For Immediate Release Tim Komberec, CEO Named Executive of the Year by Pacific Northwest Aerospace Alliance Hayden, ID [March 2, 2018] Tim Komberec, President & CEO of Empire Airlines, Inc., has received the prestigious award of Executive of the Year from the Pacific Northwest Aerospace Alliance./p The award was presented to Mr. Komberec on February 13, 2018 at the 17th annual conference held by the Pacific Northwest Aerospace Alliance at the Lynwood, Washington Convention Center. The Executive of the Year award is given annually by the organization in recognition of the executive that has made a significant contribution to the advancement of the Pacific Northwest aerospace industry./p “It is truly an honor to receive this award and to be recognized by peers in the industry. The credit really goes to our wonderful employees and great customers.” says Tim Komberec./p “PNAA is excited to present Tim Komberec the Executive of the Year Award,” said PNAA’s Chairman Ted Croft. “His leadership has taken the company to incredible heights and has launched ventures to carry them through the future.”/p Mr. Komberec has been President & CEO of Empire Airlines, a commercial carrier services company, since 2000. He has overseen the successful operations of not only Empire Airlines, but the company’s subsidiaries: Empire Aerospace, LLC; Empire Unmanned, LLC; and Ohana Airlines passenger services in Hawaii. Any of Empire Airlines’ employees will readily verify that Mr. Komberec is an executive leader that leads by example, espousing to his teams integrity, accountability, dependability, innovation and excellence in customer service./p In addition, Mr. -

Ted Stevens Anchorage International Airport 2014 MASTER PLAN UPDATE

Ted Stevens Anchorage International Airport 2014 MASTER PLAN UPDATE APPENDIX I - AIRFIELD SIMULATION FINAL DECEMBER 2014 IN ASSOCIATION WITH: HDR DOWL HKM RIM Architects ATAC Photo credit: Vanessa Bauman TED STEVENS ANCHORAGE INTERNATIONAL AIRPORT MASTER PLAN UPDATE APPENDIX I AIRFIELD SIMULATION December 2014 FINAL Prepared for: Ted Stevens Anchorage International Airport State of Alaska Department of Transportation & Public Facilities Prepared by: In association with: HDR DOWL HKM RIM Architects ATAC AKSAS Project No.: 54320 RS&H Project No. 226-2566-000 “The preparation of this document was financed in part through a planning grant from the Federal Aviation Administration (FAA) as provided under Section 505 of the Airport and Airways Improvement Act of 1982, as amended by the Airway Safety and Capacity Expansion Act of 1987. The contents do not necessarily reflect the official views or policy of the FAA. Acceptance of this report by the FAA does not in any way constitute a commitment on the part of the United States to participate in any development depicted therein, nor does it indicate that the proposed development is environmentally acceptable in accordance with applicable public laws.” PREFACE The Ted Stevens Anchorage International Airport (Airport) Master Plan Update (Master Plan Update) provides Airport management and the Alaska Department of Transportation & Public Facilities (DOT&PF) with a strategy to develop the Ted Stevens Anchorage International Airport. The intent of the Master Plan Update is to provide guidance that will enable Airport management to strategically position the Airport for the future by maximizing operational efficiency and business effectiveness, as well as by maximizing property availability for aeronautical development through efficient planning. -

Predation, Competition and Antitrust Law: Turbulence in the Airline Industry Paul Stephen Dempsey

Journal of Air Law and Commerce Volume 67 | Issue 3 Article 4 2002 Predation, Competition and Antitrust Law: Turbulence in the Airline Industry Paul Stephen Dempsey Follow this and additional works at: https://scholar.smu.edu/jalc Recommended Citation Paul Stephen Dempsey, Predation, Competition and Antitrust Law: Turbulence in the Airline Industry, 67 J. Air L. & Com. 685 (2002) https://scholar.smu.edu/jalc/vol67/iss3/4 This Article is brought to you for free and open access by the Law Journals at SMU Scholar. It has been accepted for inclusion in Journal of Air Law and Commerce by an authorized administrator of SMU Scholar. For more information, please visit http://digitalrepository.smu.edu. PREDATION, COMPETITION & ANTITRUST LAW: TURBULENCE IN THE AIRLINE INDUSTRY* PAUL STEPHEN DEMPSEY** TABLE OF CONTENTS I. INTRODUCTION .................................. 688 II. EMPIRICAL EVIDENCE OF PREDATION ......... 692 A. HUB CONCENTRATION .......................... 692 B. MEGACARRIER ALLIANCES ....................... 700 C. EXAMPLES OF PREDATORY PRICING By MAJOR AIRLINES ........................................ 702 1. Major Network Airline Competitive Response To Entry By Another Major Network Airline ...... 715 a. Denver-Philadelphia: United vs. U SA ir .................................. 716 b. Minneapolis/St. Paul - Cleveland: Northwest vs. Continental ............. 717 2. Major Network Airline Competitive Response To Entry By Southwest Airlines .................. 718 a. St. Louis-Cleveland: TWA vs. Southwest .............................. 719 * Copyright © 2002 by the author. The author would like to thank Professor Robert Hardaway for his contribution to the portion of this essay addressing the essential facility doctrine. The author would also like to thank Sam Addoms and Bob Schulman, CEO and Vice President, respectively, of Frontier Airlines for their invaluable assistance in reviewing and commenting on the case study contained herein involving monopolization of Denver. -

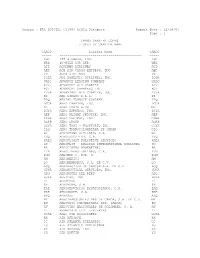

FAA DOT/TSC CY1997 ACAIS Database Report Date : 12/18/97 Page : 1

Source : FAA DOT/TSC CY1997 ACAIS Database Report Date : 12/18/97 Page : 1 CARGO CARRIER CODES LISTED BY CARRIER NAME CARCD Carrier Name CARCD ----- ------------------------------------------ ----- KHC 135 AIRWAYS, INC. KHC WRB 40-MILE AIR LTD. WRB ACD ACADEMY AIRLINES ACD AER ACE AIR CARGO EXPRESS, INC. AER VX ACES AIRLINES VX IQDA ADI DOMESTIC AIRLINES, INC. IQDA UALC ADVANCE LEASING COMPANY UALC ADV ADVANCED AIR CHARTER ADV ACI ADVANCED CHARTERS INT ACI YDVA ADVANTAGE AIR CHARTER, INC. YDVA EI AER LINGUS P.L.C. EI TPQ AERIAL TRANSIT COMPANY TPQ DGCA AERO CHARTER, INC. DGCA ML AERO COSTA RICA ML DJYA AERO EXPRESS, INC. DJYA AEF AERO FLIGHT SERVICE, INC. AEF GSHA AERO FREIGHT, INC. GSHA AGRP AERO GROUP AGRP CGYA AERO TAXI - ROCKFORD, INC. CGYA CLQ AERO TRANSCOLOMBIANA DE CARGA CLQ G3 AEROCHAGO AIRLINES, S.A. G3 EVQ AEROEJECUTIVO, C.A. EVQ XAES AEROFLIGHT EXECUTIVE SERVICES XAES SU AEROFLOT - RUSSIAN INTERNATIONAL AIRLINES SU AR AEROLINEAS ARGENTINAS AR LTN AEROLINEAS LATINAS, C.A. LTN ROM AEROMAR C. POR. A. ROM AM AEROMEXICO AM QO AEROMEXPRESS, S.A. DE C.V. QO ACQ AERONAUTICA DE CANCUN S.A. DE C.V. ACQ HUKA AERONAUTICAL SERVICES, INC. HUKA ADQ AERONAVES DEL PERU ADQ HJKA AEROPAK, INC. HJKA PL AEROPERU PL 6P AEROPUMA, S.A. 6P EAE AEROSERVICIOS ECUATORIANOS, C.A. EAE KRE AEROSUCRE, S.A. KRE ASQ AEROSUR ASQ MY AEROTRANSPORTES MAS DE CARGA, S.A. DE C.V. MY ZU AEROVAIS COLOMBIANAS LTD. (ARCA) ZU AV AEROVIAS NACIONALES DE COLOMBIA, S. A. AV ZL AFFRETAIR LTD. (PRIVATE) ZL UCAL AGRO AIR ASSOCIATES UCAL RK AIR AFRIQUE RK CC AIR ATLANTA ICELANDIC CC LU AIR ATLANTIC DOMINICANA LU AX AIR AURORA, INC. -

UFTAA Congress Kuala Lumpur 2013

UFTAA Congress Kuala Lumpur 2013 Duncan Bureau Senior Vice President Global Sales & Distribution The Airline industry is tough "If I was at Kitty Hawk in 1903 when Orville Wright took off, and would have been farsighted enough, and public-spirited enough -- I owed it to future capitalists -- to shoot them down…” Warren Buffet US Airline Graveyard – A Only AAXICO Airlines (1946 - 1965, to Saturn Airways) Air General Access Air (1998 - 2001) Air Great Lakes ADI Domestic Airlines Air Hawaii (1960s) Aeroamerica (1974 – 1982) Air Hawaii (ceased Operations in 1986) Aero Coach (1983 – 1991) Air Hyannix Aero International Airlines Air Idaho Aeromech Airlines (1951 - 1983, to Wright Airlines) Air Illinois AeroSun International Air Iowa AFS Airlines Airlift International (1946 - 81) Air America (operated by the CIA in SouthEast Asia) Air Kentucky Air America (1980s) Air LA Air Astro Air-Lift Commuter Air Atlanta (1981 - 88) Air Lincoln Air Atlantic Airlines Air Link Airlines Air Bama Air Link Airways Air Berlin, Inc. (1978 – 1990) Air Metro Airborne Express (1946 - 2003, to DHL) Air Miami Air California, later AirCal (1967 - 87, to American) Air Michigan Air Carolina Air Mid-America Air Central (Michigan) Air Midwest Air Central (Oklahoma) Air Missouri Air Chaparral (1980 - 82) Air Molakai (1980) Air Chico Air Molakai (1990) Air Colorado Air Molakai-Tropic Airlines Air Cortez Air Nebraska Air Florida (1972 - 84) Air Nevada Air Gemini Air New England (1975 - 81) US Airline Graveyard – Still A Air New Orleans (1981 – 1988) AirVantage Airways Air -

January 2015

THE SOURCE FOR AIRFREIGHT LOGISTICS International Edition • AirCargoWorld.com • Dec. 2014/Jan. 2015 OLIVER EVANS CHIEF CARGO OFFICER SWISS INTERNATIONAL AIR LINES AIR CARGO EXECUTIVE OF THE YEAR p.20 GAME CHANGERS: THREE TOP EXECS SHAPING THE INDUSTRY’S FUTURE p.24 Contents AIR CARGO EXECUTIVE OF THE YEAR Volume 17 • Number 11 • December 2014/January 2015 OLIVER EVANS A LEADER IN ANY LANGUAGE p.20 News Inside: 7 UpFront IATA’s five-year prediction, TNT hits the road and more 8 Asia Cargolux eyes new trans-Pacific venture 12 Africa & Middle East Cargo carriers continue service in hot zones GAME CHANGERS 14 Europe Three top airfreight executives shaping the industry’s future IAG Cargo launches EuroConnector service 17 Americas Could JFK’s freight move upstate? Departments 4 Publisher’s Note 10 Cargo Chat: Martin Drew 40 Bottom Line p.28 WORLD AIRFREIGHT DIRECTORY 42 Classifieds Our annual reference guide for airlines, airports, forwarders 44 People and other airfreight professionals from around the globe 45 Events / Advertiser’s Index 46 Forwarders’ Forum Air Cargo World (ISSN 1933-1614) is published monthly and owned by Royal Media. Air Cargo World is located at 1080 Holcomb Bridge Rd., Suite 255, Roswell, GA 30076. Production office is located at 2033 Sixth Avenue, Suite 830, Seattle WA 98121; telephone 206-587-6537. Air Cargo World is a registered trademark. Periodicals postage paid at Downers Grove, IL and at additional mailing offices. Subscription rates: 1 year, $80; 2 year $128; outside USA surface mail/1 year $120; 2 year $216. Single copies $20. Express Delivery Guide, Carrier Guide, Freight Forwarder Directory and Airport Directory single copies $14.95 domestic; $21.95 overseas.