Federated Hermes Global Allocation Fund

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

MVIS United Kingdom Equal Weight Index

FACTSHEET MVIS United Kingdom Equal Weight Index The MVIS United Kingdom Equal Weight Index (MVGBEQ) index tracks the performance of the largest and most liquid companies incorporated in the United Kingdom of Great Britain and Northern Ireland, employing an equal weighting scheme. The index also includes non-local companies incorporated outside the United Kingdom and Northern Ireland that generate at least 50% of their revenues in the United Kingdom. MVGBEQ covers at least 80% of the investable universe. Key Features All Time High/Low 52-Week High/Low Total Return Net Index 1,143.74/375.85 1,143.74/782.80 Index Data INDEX PARAMETERS FUNDAMENTALS* ANNUALISED PERFORMANCE* Launch Date 01 Jun 2017 Components 107.00 Price/Earnings Trailing 21.32 1 Month -5.00% Type Country Volatility (1 year) 17.06 Price/Book 2.04 1 Year 33.01% Currency USD Full MCap bn USD 2,666.49 Price/Sales 1.47 3 Years 4.02% Base Date 29 Dec 2006 Float MCap bn USD 2,117.83 Price/Cash Flow 12.30 5 Years 4.55% Base Value 1,000.00 Correlation* (1 year) 0.96 Dividend Yield 2.54 Since Inception 0.48% * as of 30 Sep 2021 * MSCI United Kingdom IMI * Total Return Net Index Country and Size Weightings COUNTRY WEIGHTINGS EXCL. OFFSHORE* COUNTRY WEIGHTINGS INCL. OFFSHORE* SIZE WEIGHTINGS GB Large-Cap ES Mid-Cap IM GB LU Small-Cap BM Micro-Cap Others Country Count Weight Country Offshore Count Weight Size Count Weight United Kingdom 99 92.21% United Kingdom 8 107 100.00% Large-Cap ( > 6 bn) 98 91.93% Spain 1 1.12% Mid-Cap (1.5 bn - 6 bn) 9 8.07% Isle of Man 1 1.07% Small-Cap (0.2 bn - 1.5 bn) 0 0.00% Luxembourg 1 0.98% Micro-Cap (0.0 bn - 0.2 bn) 0 0.00% Bermuda 1 0.96% Others 4 3.66% *Companies incorporated outside of a certain region or country that generate at least 50.00% of their revenues (or, where applicable, have at least 50.00% of their assets) in that region or country. -

Kraneshares CICC China Leaders 100 Index ETF*

Contact us: +(1) 855 8KRANE8 [email protected] KFYP KraneShares CICC China Leaders 100 Index ETF* Investment Strategy: Fund Details Data as of 01/31/2021 KFYP tracks the CSI CICC Select 100 Index, which takes a smart-beta1 approach to systematically invest in companies listed in Mainland China. The strategy is based on Primary Exchange NYSE China International Capital Corporation (CICC)’s latest research on China’s capital markets. This quantitative approach reflects CICC’s top down and bottom up CUSIP 500767207 research process, seeking to deliver the 100 leading companies in Mainland China. ISIN US5007672075 KFYP Features: Total Annual Fund Operating Expense 0.69% 2 Smart beta strategy which seeks to deliver cost effective alpha . Inception Date 7/22/2013 Exposure to the top 100 industry leaders within China’s Mainland A-share market Distribution Frequency Annual identified through the CICC Research team’s quantitative methodology. Seeks to provide exposure to performance leaders through a Return on Equity Index Name CSI CICC Select 100 Index (ROE)3 filter which is further refined through bottom-line growth and valuation criteria. Number of Holdings 96 About CICC & CICC Research: CICC is a leading, publicly traded, Chinese financial services company with expertise in research, asset management, investment banking, private equity and Top 10 Holdings as of 01/31/2021 Ticker % wealth management. Holdings are subject to change. In 2019, the CICC Research Team ranked #1 in Institutional Investor’s All-China Research Category for the eighth year in a row.4 MIDEA GROUP CO LTD-A 000333 6.25 CICC has over 200 branches across Mainland China, with offices in Hong Kong, INNER MONG YIL-A 600887 6.05 Singapore, New York, San Francisco, and London. -

Chapter 2 China's Cars and Parts

Chapter 2 China’s cars and parts: development of an industry and strategic focus on Europe Peter Pawlicki and Siqi Luo 1. Introduction Initially, Chinese investments – across all industries in Europe – especially acquisitions of European companies were discussed in a relatively negative way. Politicians, trade unionists and workers, as well as industry representatives feared the sell-off and the subsequent rapid drainage of industrial capabilities – both manufacturing and R&D expertise – and with this a loss of jobs. However, with time, coverage of Chinese investments has changed due to good experiences with the new investors, as well as the sheer number of investments. Europe saw the first major wave of Chinese investments right after the financial crisis in 2008–2009 driven by the low share prices of European companies and general economic decline. However, Chinese investments worldwide as well as in Europe have not declined since, but have been growing and their strategic character strengthening. Chinese investors acquiring European companies are neither new nor exceptional anymore and acquired companies have already gained some experience with Chinese investors. The European automotive industry remains one of the most important investment targets for Chinese companies. As in Europe the automotive industry in China is one of the major pillars of its industry and its recent industrial upgrading dynamics. Many of China’s central industrial policy strategies – Sino-foreign joint ventures and trading market for technologies – have been established with the aim of developing an indigenous car industry with Chinese car OEMs. These instruments have also been transferred to other industries, such as telecommunications equipment. -

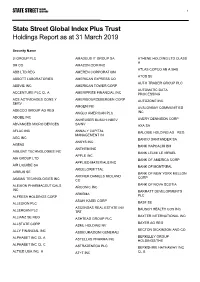

State Street Global Index Plus Trust Holdings Report As at 31 March 2019

1 State Street Global Index Plus Trust Holdings Report as at 31 March 2019 Security Name 3I GROUP PLC AMADEUS IT GROUP SA ATHENE HOLDING LTD CLASS A 3M CO AMAZON.COM INC ATLAS COPCO AB A SHS ABB LTD REG AMEREN CORPORATION ATOS SE ABBOTT LABORATORIES AMERICAN EXPRESS CO AUTO TRADER GROUP PLC ABBVIE INC AMERICAN TOWER CORP AUTOMATIC DATA ACCENTURE PLC CL A AMERIPRISE FINANCIAL INC PROCESSING ACS ACTIVIDADES CONS Y AMERISOURCEBERGEN CORP AUTOZONE INC SERV AMGEN INC AVALONBAY COMMUNITIES ADECCO GROUP AG REG ANGLO AMERICAN PLC INC ADOBE INC ANHEUSER BUSCH INBEV AVERY DENNISON CORP ADVANCED MICRO DEVICES SA/NV AXA SA AFLAC INC ANNALY CAPITAL BALOISE HOLDING AG REG MANAGEMENT IN AGC INC BANCO SANTANDER SA ANSYS INC AGEAS BANK HAPOALIM BM ANTHEM INC AGILENT TECHNOLOGIES INC BANK LEUMI LE ISRAEL APPLE INC AIA GROUP LTD BANK OF AMERICA CORP APPLIED MATERIALS INC AIR LIQUIDE SA BANK OF MONTREAL ARCELORMITTAL AIRBUS SE BANK OF NEW YORK MELLON ARCHER DANIELS MIDLAND CORP AKAMAI TECHNOLOGIES INC CO BANK OF NOVA SCOTIA ALEXION PHARMACEUTICALS ARCONIC INC INC BARRATT DEVELOPMENTS ARKEMA ALFRESA HOLDINGS CORP PLC ASAHI KASEI CORP ALLEGION PLC BASF SE ASCENDAS REAL ESTATE INV BAUSCH HEALTH COS INC ALLERGAN PLC TRT BAXTER INTERNATIONAL INC ALLIANZ SE REG ASHTEAD GROUP PLC BAYER AG REG ALLSTATE CORP ASML HOLDING NV BECTON DICKINSON AND CO ALLY FINANCIAL INC ASSICURAZIONI GENERALI ALPHABET INC CL A BERKELEY GROUP ASTELLAS PHARMA INC HOLDINGS/THE ALPHABET INC CL C ASTRAZENECA PLC BERKSHIRE HATHAWAY INC ALTICE USA INC A AT+T INC CL B 2 BEST BUY CO INC CHUBB -

40% More Gigabytes in Spite of the Pandemic

Industry analysis #3 2020 Mobile data – first half 2020 40% more gigabytes in spite of the pandemic But revenue negatively affected: -0.5% 140% Average +51% Average +54% th 120% Tefficient’s 28 public analysis on the 100% development and drivers of mobile data ranks 116 80% operators based on average data usage per 60% SIM, total data traffic and revenue per gigabyte in 40% the first half of 2020. y growth in mobile data usage data mobile in y growth - o - 20% Y The data usage per SIM grew for basically every 0% Q1 2020 Q2 2020 operator. 42% could turn -20% that data usage growth into ARPU growth. It’s a bit lower than in our previous reports and COVID-19 is to blame; many operators did report negative revenue development in Q2 2020 when travelling stopped and many prepaid subscriptions expired. Mobile data traffic continued to grow, though: +40%. Although operators in certain markets were giving mobile data away to mitigate the negative consequences of lockdowns, most of the global traffic growth is true, underlying, growth. Data usage actually grew faster in Q2 2020 than in Q1 2020 even though lockdowns mainly affected Q2. Our industry demonstrated resilience, but now needs to fill the data monetisation toolbox with more or sharper tools. tefficient AB www.tefficient.com 3 September 2020 1 27 operators above 10 GB per SIM per month in 1H 2020 Figure 1 shows the average mobile data usage for 116 reporting or reported1 mobile operators globally with values for the first half of 2020 or the full year of 2019. -

Annex 1: Parker Review Survey Results As at 2 November 2020

Annex 1: Parker Review survey results as at 2 November 2020 The data included in this table is a representation of the survey results as at 2 November 2020, which were self-declared by the FTSE 100 companies. As at March 2021, a further seven FTSE 100 companies have appointed directors from a minority ethnic group, effective in the early months of this year. These companies have been identified through an * in the table below. 3 3 4 4 2 2 Company Company 1 1 (source: BoardEx) Met Not Met Did Not Submit Data Respond Not Did Met Not Met Did Not Submit Data Respond Not Did 1 Admiral Group PLC a 27 Hargreaves Lansdown PLC a 2 Anglo American PLC a 28 Hikma Pharmaceuticals PLC a 3 Antofagasta PLC a 29 HSBC Holdings PLC a InterContinental Hotels 30 a 4 AstraZeneca PLC a Group PLC 5 Avast PLC a 31 Intermediate Capital Group PLC a 6 Aveva PLC a 32 Intertek Group PLC a 7 B&M European Value Retail S.A. a 33 J Sainsbury PLC a 8 Barclays PLC a 34 Johnson Matthey PLC a 9 Barratt Developments PLC a 35 Kingfisher PLC a 10 Berkeley Group Holdings PLC a 36 Legal & General Group PLC a 11 BHP Group PLC a 37 Lloyds Banking Group PLC a 12 BP PLC a 38 Melrose Industries PLC a 13 British American Tobacco PLC a 39 Mondi PLC a 14 British Land Company PLC a 40 National Grid PLC a 15 BT Group PLC a 41 NatWest Group PLC a 16 Bunzl PLC a 42 Ocado Group PLC a 17 Burberry Group PLC a 43 Pearson PLC a 18 Coca-Cola HBC AG a 44 Pennon Group PLC a 19 Compass Group PLC a 45 Phoenix Group Holdings PLC a 20 Diageo PLC a 46 Polymetal International PLC a 21 Experian PLC a 47 -

Constituents & Weights

2 FTSE Russell Publications 19 August 2021 FTSE 100 Indicative Index Weight Data as at Closing on 30 June 2021 Index weight Index weight Index weight Constituent Country Constituent Country Constituent Country (%) (%) (%) 3i Group 0.59 UNITED GlaxoSmithKline 3.7 UNITED RELX 1.88 UNITED KINGDOM KINGDOM KINGDOM Admiral Group 0.35 UNITED Glencore 1.97 UNITED Rentokil Initial 0.49 UNITED KINGDOM KINGDOM KINGDOM Anglo American 1.86 UNITED Halma 0.54 UNITED Rightmove 0.29 UNITED KINGDOM KINGDOM KINGDOM Antofagasta 0.26 UNITED Hargreaves Lansdown 0.32 UNITED Rio Tinto 3.41 UNITED KINGDOM KINGDOM KINGDOM Ashtead Group 1.26 UNITED Hikma Pharmaceuticals 0.22 UNITED Rolls-Royce Holdings 0.39 UNITED KINGDOM KINGDOM KINGDOM Associated British Foods 0.41 UNITED HSBC Hldgs 4.5 UNITED Royal Dutch Shell A 3.13 UNITED KINGDOM KINGDOM KINGDOM AstraZeneca 6.02 UNITED Imperial Brands 0.77 UNITED Royal Dutch Shell B 2.74 UNITED KINGDOM KINGDOM KINGDOM Auto Trader Group 0.32 UNITED Informa 0.4 UNITED Royal Mail 0.28 UNITED KINGDOM KINGDOM KINGDOM Avast 0.14 UNITED InterContinental Hotels Group 0.46 UNITED Sage Group 0.39 UNITED KINGDOM KINGDOM KINGDOM Aveva Group 0.23 UNITED Intermediate Capital Group 0.31 UNITED Sainsbury (J) 0.24 UNITED KINGDOM KINGDOM KINGDOM Aviva 0.84 UNITED International Consolidated Airlines 0.34 UNITED Schroders 0.21 UNITED KINGDOM Group KINGDOM KINGDOM B&M European Value Retail 0.27 UNITED Intertek Group 0.47 UNITED Scottish Mortgage Inv Tst 1 UNITED KINGDOM KINGDOM KINGDOM BAE Systems 0.89 UNITED ITV 0.25 UNITED Segro 0.69 UNITED KINGDOM -

Satellite Backhaul Architecture for Next-Generation Cellular Networks: Necessity and Opportunities

High Technology Letters ISSN NO : 1006-6748 Satellite Backhaul Architecture for Next-Generation Cellular Networks: Necessity and Opportunities Dimov Stojce Ilcev Space Science Centre (SSC), Durban University of Technology (DUT), Durban, South Africa, E-mail: [email protected] Abstract: In this paper is introduced a new 5G cellular communication systems and their possible integration with other radio or satellite networks, such as Digital Video Broadcasting-Return Channel via Satellite (DVB-RCS) standards as backhaul for rural, remote cellular networks. Within the next generation 5G framework, the Terrestrial Telecommunication Network (TTN) can be augmented with the backhaul of the development of High Throughput Satellite (HTS) and modern mega DVB-RCS constellations meeting 5G requirements, such as high bandwidth, low latency, and increased coverage for rural, remote and mobile environments. This integration of 5G with DVB-RCS standards will upgrade satellite Internet and IPTV for urban, remote, and mobile applications for ships, road, rails, and aeronautical applications via Geostationary Erath Orbit (GEO) satellites. Mobile Satellite Internet aims at providing the backbone for next-generation 5G broadcasting service through C, Ku and Ka-band DVB-S2 standard for ground and mobile subscribers. It is de facto a mobile interactive broadcast satellite access system, which provides both IPTV broadcasting and high-speed Internet broadband based on DVB-S/DVB-RCS standards, Internet Protocol (IP) network, World Wide Web, and E-solutions globally. Key Words: DVB-RCS, TTN, HTS, GEO, LTE, MIMO, eMBB, mMTC, LEO, MEO, URLLC, VSAT, HTS ISDN, ATM, UMTS, GPRS 1. Introduction Since the predominant Japanese cellular phone operator Nippon Telegraph and Telephone Public Corporation (NTT) DoCoMo Inc. -

BTS Group Fast Comment

Equity Research – 04 January 2021 09:31 CET BTS Group Fast comment Acquires Bates Communications in the US Company-sponsored research: Not rated Bates had USD 7m sales in 2020, adds 3% to BTS (‘21e) Share price (SEK) 30/12/2020 217.0 Strong client portfolio with limited overlap Services, Sweden No price disclosed: cash & share payment (~2% dilution) BTSB.ST/BTSB SS Bates Communications adds 3% to 2021e sales MCap (SEKm) 4,192 BTS acquires Boston based Bates Communications, a team of 23 MCap (EURm) 416 employees and USD 7m in sales in 2020. This adds 3% to both the Net debt (EURm) -16 employee base (Q3’20) and 2021e sales. Bates Communications will be integrated in the segment BTS North America. Founder Suzanne Bates No. of shares (m) 19.3 and all members of her leadership team have agreed to stay on with BTS Free float (%) 43 for a minimum of 3 years to accelerate the integration and growth Av. daily volume (k) 31 strategy. Next event Q4 report: 24 Feb Focuses on top management leadership Bates Communications is helping some of the top companies in the world execute their strategies through C-Suite Advisory, Executive Coaching, Team Performance, Leader Communications, Executive Presence Leadership Development and Executive Succession and Onboarding, primarily in the USA. All of these services, including related solutions and proprietary IP, will strengthen and expand current BTS offerings, according to the company. The client portfolio looks strong, with for example AIG, American Express and Fidelity in the financial sector, SAP and Intel in the tech sector, Kraft Foods in retail and Bristol-Myers Squibb and Merck in the healthcare sector, among other clients (see full disclosure on next page). -

Infotainment & Telema$Cs

November 2, 2015 Strategy Analy6cs, Inc 1 Kevin Li Strategy Analy6cs GENIVI 13th All-Member Mee6ng & AMM OPEN DAYS November 2, 2015 Strategy Analy9cs, Inc 2 AGENDA 1 Telema9cs Market Situa9on in China 2 Soware Topics-Smartphone GW & OS 3 Internet Company's Automo9ve Prac9ce 4 HMI & Consumer Interest 5 Aersales Market November 2, 2015 Strategy Analy9cs, Inc 3 HIGH LEVEL CHINA MARKET OVERVIEW Source: Strategy Analy6cs • 154 mIllIon cars by the end • 8% passenger cars sold In 2014 154 Mil of 2014 8% were connected In the OEM market • 17 mIllIon cars net growth • 30% passenger cars sold In the OEM 17 Mil from 2013 to 2014 30% market wIll be connected In 2018 November 2, 2015 Strategy Analy9cs, Inc 4 CHINA TELEMATICS MARKET LEADERSHIP Typical Players in OEM Market Network OEM Speed TSP Carrier In-vehicle OS Free Trial Qoros 3G MicrosoY ChIna UnIcom MicrosoY QorosQloud Lifeme BMW QNX ChIna UnIcom ConnectedDrIve 3G ChIna UnIcom GENIVI 3+7 Years Volvo ChIna UnIcom MicrosoY Sensus 3G WIrelessCar 3+7 Years Lexus ChIna Telecom QNX G-BOOK 2.5G YESWAY 4-6 Years Volkswagen VerIzon MicrosoY ChIna UnIcom Car-Net 3G Telemacs ChIna QNX 4 Years Mercedes-Benz VerIzon MicrosoY ChIna Telecom CONNET 3G Telemacs ChIna QNX 3 Years Audi ChIna UnIcom QNX AudI connect 3G WIrelessCar 3 Years SAIC 3G PATEO ChIna UnIcom AndroId InkaNet 2 Years BYD MicrosoY 3G/2.5G BYD All three 2 Years BYD Cloud AndroId Embedded telema%cs is evolving to longer free trial period. November 2, 2015 Strategy Analy9cs, Inc 5 INDUSTRY CHALLENGES: CHINA CONVERGENCE OF INFO-TELEMATICS & SAFETY -

New Synchronization Requirements for 4G Backhaul & Fronthaul

White Paper New Synchronization Requirements for 4G Backhaul & Fronthaul Prepared by Patrick Donegan Chief Analyst, Heavy Reading www.heavyreading.com on behalf of www.veexinc.com December 2014 Introduction With industry leaders such as Ericsson claiming that "spectrum is the new oil" driving the emerging digital economy, there can be no doubt as to the weight of expec- tation on mobile operators where network capacity is concerned. Year after year, customers expect mobile operators to somehow keep at least one step ahead of the acceleration in mobile data consumption. Operators must some- how deliver on a long-term capacity roadmap that will allow customers to consume whatever high-bandwidth services they want, wherever and whenever they want them. And investors expect them to do all this without increasing the total cost of ownership of the network, taking account of both capex and opex. This white paper examines the available options for operators with Long Term Evo- lution (LTE), LTE-Advanced (LTE-A) and the various small cell and centralized radio access network (C-RAN) architecture options for implementing them. The paper provides examples of early deployments of these techniques and architectures and discusses the associated requirements for network synchronization and synchroni- zation testing as these capacity enhancements are rolled out. Efficient Use of Spectrum & Network Assets Consistent with a "spectrum is the new oil" perspective, mobile operators continue to value radio spectrum above any other asset. The mobile communications indus- try is already gearing up for upcoming World Radiocommunications Conferences (WRC) to see what spectrum can be secured for 5G below 5 GHz at WRC 2015 and above 10 GHz at the next WRC in 2018 or 2019. -

February 2021 7 Mile Advisors

7 Mile Advisors Sectorwatch: Management Consulting February 2021 Management Consulting 7 Mile Advisors appreciates the opportunity to present this confidential information to the Company. This document is meant to be delivered only in conjunction with a verbal presentation, and is not authorized for distribution. Please see the Confidentiality Notice & Disclaimer at the end of the document. All data cited in this document was believed to be accurate at the time of authorship and came from publicly available sources. Neither 7 Mile Advisors nor 7M Securities make warranties or representations as to the accuracy or completeness of third-party data contained herein. This document should be treated 2 as confidential and for the use of the intended recipient only. Please notify 7 Mile Advisors if it was distributed in error. Overview DASHBOARD • Summary metrics on the sector • Commentary on market momentum by comparing the most recent 12-month performance against the last 3- year averages. PUBLIC BASKET PERFORMANCE • Summary valuation and operating metrics for a basket of We advise on M&A and private capital transactions and provide market comparable public companies. assessments and benchmarking. As a close-knit team with a long history together and a laser focus on our target markets, we help our clients sell their companies, raise capital, grow through acquisitions, and evaluate new markets. VALUATION COMPARISON We publish our sectorwatch, a review of M&A and operational trends in • Graphical, detailed comparison of valuation multiples