AGN SA Draft Plan 2021-26

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Standards Australia – Published Standards

Week Commencing 8 February Standards Australia – Published Standards Standards Australia has advised that the following Standards have been published. AS/NZS 5263.1.3:2021 Gas appliances, Part 1.3: Gas space heating appliances AS/NZS 5263.1.8:2021 Gas appliances, Part 1.8: Decorative effect gas appliances Hydrogen proposed for 40,000 customers in Albury-Wodonga Australian Gas Networks media release 4 February 2021 Australian Gas Infrastructure Group (AGIG) is proud to partner on two renewable hydrogen project bids to the Australian Renewable Energy Agency (ARENA), submitted last month. In Victoria, Australian Gas Networks (AGN) – part of AGIG – is partnering with global low- carbon energy company ENGIE to develop a renewable hydrogen project that will supply carbon-free hydrogen at volumes of up to 10 per cent, to around 40,000 existing residential, commercial and industrial connections. The 10MW Hydrogen Park Murray Valley (HyP Murray Valley) project will be co-located with the West Wodonga Wastewater Treatment Plant and supply renewable hydrogen blended with natural gas to customers on the existing Albury-Wodonga gas distribution network, with the facility also able to supply industry and transport markets. The HyP Murray Valley bid has been submitted alongside the Clean Energy Innovation Park (CEIP) project proposal, a joint venture between AGIG and international integrated energy group ATCO. The CEIP will be located alongside renewable electricity generation assets in Waradarge, Western Australia. It comprises a 10MW electrolyser and is capable of producing 4.0 tonnes of renewable hydrogen per day for use in gas networks, industry and transport. These projects add to AGIG’s current hydrogen developments in Hydrogen Park South Australia and Hydrogen Park Gladstone in Queensland and demonstrates AGIG’s commitment to target 10 per cent renewable gas in networks by no later than 2030. -

Australian Gas Infrastructure Group Annual Review 2018

Attachment 2.1 Australian Gas Infrastructure Group Annual Review 2018 January 2020 Delivering for Australians 2018 Annual Review We are Australian Gas Infrastructure Group (AGIG) One of Australia’s largest gas infrastructure Our portfolio of companies delivers for customers businesses. across Australia. Our vision is to Dampier Bunbury be the leading gas Pipeline Group (DBP) infrastructure Operates in Western Contents business in Australia. Australia and the Message from the Chairmen 03 We will achieve this Northern Territory. Message from the CEO 05 by delivering for our Multinet Gas Highlights 09 customers, being Networks (MGN) About AGIG 11 a good employer and Operates in Victoria. being sustainably Values and Vision 15 Australian Gas cost efficient. Our Role in the Gas Industry 17 Networks (AGN) Our Project Capabilities and Credentials 21 We own and operate Operates in Victoria, Delivering for Customers 27 infrastructure that South Australia, A Good Employer 39 delivers gas to Australian Queensland, New Sustainably Cost Efficient 43 homes, businesses, and South Wales and the Operational Statistics 59 communities. In 2018 Northern Territory. we surpassed two AGIG builds and million customers operates new pipelines on our distribution across the country. networks—more than any other gas distributor in the country. We also deliver and store gas that supports the Australian economy—for power generators, mines and manufacturers. Australian Gas Infrastructure Group Australian Gas Infrastructure Group 01 2018 Annual Review 2018 Annual Review 02 Message As the Chairmen of the companies that make up AGIG – DBP, MGN and AGN – from the we are proud of the achievements Chairmen of AGIG in working towards this vision. -

What's Inside

™ AUSTRALIA MARKET GUIDE WHAT’S INSIDE SECTION 1: General market overview SECTION 2: Viridian and Click Energy SECTION 3: How to sign up © 2016 Viridian. All rights reserved. Unauthorized copying or reproduction of this product, in whole or in part, is strictly prohibited. SEPTEMBER 2016 GENERAL MARKET OVERVIEW Brisbane Adelaide Sydney Canberra Melbourne ELECTRIC NATURAL GAS © 2016 Viridian. All rights reserved. Unauthorized copying or reproduction of this product, in whole or in part, VIRIDIAN • AUSTRALIA MARKET GUIDE 2 is strictly prohibited. Market Snapshot The National Electricity Market (NEM) is the wholesale electricity market that delivers electricity to almost 10 million homes and businesses in Australia. Established in December 1998, it’s one of the largest geographically interconnected power systems in the world, covering a distance of approximately 4,500 kilometres through New South Wales, Queensland, South Australia, Victoria, Tasmania and the Australian Capital Territory. The aim of the NEM is to make sure electricity is available when it’s needed, in a cost effective and reliable way. There are three main participants in the NEM: • Generators, which are coal, natural gas and renewable power stations that sell electricity to the market. • Distributors, who own and manage the infrastructure (poles and cables) which bring the electricity to residential and business customers. • Retailers, who buy electricity from the market. They then sell electricity on to residential and business customers. Click Energy is an Energy Retailer in Australia. Out of the 10 million residential consumers in Australia, the following percentages have switched to a market contract:1 • Victoria: 88% • South Australia: 84% • New South Wales: 69% • Queensland: 46% What is a distributor? Distributors are a core part of the constant supply of electricity and gas into homes and businesses. -

S116-Australian-Gas-Infrastructure

26 February 2021 Infrastructure Victoria Via online submission: https://engage.vic.gov.au/victorias-30-year-infrastructure-strategy/making- submission To whom it may concern, Victoria’s draft 30-Year Infrastructure Strategy Australian Gas Infrastructure Group (AGIG) welcomes the opportunity to make this submission on Infrastructure Victoria’s draft 30-year Infrastructure Strategy. It is important that the strategy recognise and remain open to consider all opportunities to achieve net zero emissions as required by Victoria’s Climate Change Act. In Victoria, where natural gas remains an important part of the energy mix, hydrogen represents a significant opportunity for Victoria to achieve its targets, while making use of Victoria’s extensive gas network and minimising costs. After introducing AGIG this letter will briefly outline our submission which focuses on the role of renewable hydrogen, the future of gas networks and also comments on Infrastructure Victoria’s upcoming work on the Gas Infrastructure Advice to the Victorian Treasurer. As owners of gas infrastructure in Victoria we are taking a leading role in the deployment of renewable hydrogen technologies and the development of Australia’s hydrogen industry. AGIG can provide valuable insights on the issues raised in the Gas Advice Terms of Reference, particularly on how the value of Victoria’s gas infrastructure can be optimised, including the extent to which gas infrastructure can be used for hydrogen. We therefore look forward to continuing and increasing our engagement with Infrastructure Victoria on these issues. About AGIG AGIG is the largest gas distribution business in Australia, serving more than 2 million customers through our networks in Victoria, Queensland, South Australia and several regional networks in New South Wales and the Northern Territory. -

Guide to Australia's Energy Networks

Energy Networks Australia Guide to Australia’s Energy Networks 1 Australia’s Energy Networks What are energy networks? Fast Facts Australia’s energy networks This vital infrastructure is owned and comprise the transmission towers, managed by a mix of private and Gas is delivered to Energy networks manage substations, poles, wires and pipes government-owned organisations customers through more more than 11 million electricity 918,000 than 96,000 km of gas customer connections and which supply gas and electricity which are responsible for the security networks throughout five million gas connections to almost every household and and reliability of Australia’s energy Australia to Australian homes and business in the country. supplies. km businesses The networks of Western Australia and The Australian electricity the Northern Territory are isolated from network extends about 16 the rest of the country, but even so, the 918,000 km and could circle >96,000 the equator 23 times electricity grid on the east coast (which km million forms the National Electricity Market) is one of the largest interconnected electricity networks in the world. About 28,000 energy network employees 99.95% provide essential frontline reliability and supporting services to 6 customers 24 hours a day, billion 365 days a year Energy networks provide customers with an Australia’s gas exceptionally reliable power infrastructure can store the service, adapting in real time same amount of energy to millions of changing 28,000 as 6 billion Powerwall demand and supply signals employees batteries. 2 1 Evolution of energy networks Ownership Structures The National Electricity Market (NEM) Gas networks have a long history of • There are 22 electricity and gas network businesses in Australia with a mix was created following the formal serving Australians. -

National Standard Complaints and Dispute Resolution Procedures

Australian Gas Networks Limited Group ACN 078 551 685 National Standard Complaints and Dispute Resolution Procedures Version: 3.0 Date: November 2014 Page 1 of 7 Contents 1. Purpose ...................................................................................................................................................... 3 2. Scope……………………………………………………………………………………………………………..3 3. General ....................................................................................................................................................... 3 4. Definitions ................................................................................................................................................... 3 5. Guiding principles in handling complaints and disputes ........................................................................... 4 6. Complaint handling and dispute resolution process ................................................................................. 4 7. Enquiries or complaints relating to the retailer……………………………………………………………....5 8. Contacting Australian Gas Networks …………………………………………………………………………6 9. Energy Ombudsman……………………………………………………………………………………………6 Page 2 of 7 1. Purpose This document outlines the set of procedures which Australian Gas Networks Limited (ACN 078 551 685) (and each of its subsidiaries) will apply to small customer complaints and disputes. In this document, a reference to “Australian Gas Networks” is a reference to Australian Gas Networks Limited or, where the complaint or dispute relates to a -

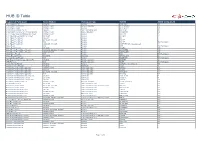

Gas HUB Participant ID Table

HUB ID Table Registered Participant Retail Market Participant Type HUB ID AEMO Company ID 1st Energy Pty Ltd VICGAS Retailer FIRSTNGY 298 ACTEWAGL Distribution NSWACTGAS Network Operator ACTEWNWO 161 ACTEWAGL Retail NSWACTGAS Retailer ACTEWUSR 140 ADCHEM (Australia) Pty Ltd SAGAS Self Contracting User ADCHEM 312 AEMO MIBB interface for CSV and aseXML NSWACTGAS Market Operator AEMOMIBB N/A AGL Energy Sales and Marketing Limited NSWACTGAS Retailer AGLUSR 45 AGL Sales (Queensland) Pty Limited QLDGAS Retailer AGLQLD 42 AGL Sales Pty Limited SAGAS Retailer AGL 4 AGL Sales Pty Limited QLDGAS, VICGAS Retailer PULSE 4 AGL Sales Pty Limited WA Retailer PULSE WA Participant AGL Sales Pty Limited QLDGAS, VICGAS Retailer AUSPWRGAS - Deregistered 80 Agora Retail WA Retailer AGR WA Participant Agora Retail Pty Ltd VICGAS Retailer AGORA 270 Alinta Energy Retail Sales Pty Ltd QLDGAS, SAGAS, VICGAS Retailer ALNTARES 192 Alinta Energy Retail Sales Pty Ltd NSWACTGAS Retailer ALINTAUSR 192 Alinta Sales Pty Ltd WA Retailer ALS WA Participant Allgas Energy Pty Ltd QLDGAS Distributor APTALLGAS 82 Amanda Energy Pty Ltd WA Retailer AMDENGY WA Participant APA Gasnet Australia (Operations) P/L VICGAS Pipeline Operator GASNET 14 APR Parmelia WA Pipeline Operator CMSR WA Participant Aurora Energy Pty Ltd VICGAS Retailer AURORA - Deregistered 159 Ausnet Services Pty Ltd VICGAS Distributor TXUN 11 Australian Energy Market Operator NSWACTGAS Market Operator NAGMO N/A Australian Energy Market Operator SAGAS Market Operator REMCo N/A Australian Energy Market Operator -

Gas and Pipeline Infrastructure Safety Management Report 2016–17

Gas and Pipeline Infrastructure Safety Management Report 2016–17 1 © Energy Safe Victoria. All rights reserved. Copyright in the whole or every part of this document belongs to Energy Safe Victoria and cannot be used, transferred, copied or reproduced in whole or in part in any manner or form or in any media to any person other than with the prior written consent of Energy Safe Victoria. Contents 3 Industry overview 15 Licensed pipelines 35 Non-licensed gas Infrastructure 51 Natural gas retail 59 Appendices 1 Industry Overview 3 Contents 5 Director’s report 6 General Manager’s report 7 1. Introduction 8 2. Ensuring compliance and the regulatory response 8 2.1. Educate 9 2.2. Encourage 9 2.3. Warn 9 2.4. Enforce 10 2.5. Prosecute 11 3. Reportable safety incidents 14 4. Priorities and the strategic audit plan review 14 5. The structure of the GPI Safety Management Report 4 Director’s report This is now the fourth year that Energy Safe Victoria (ESV) has produced the Gas and Pipeline Infrastructure (GPI) Safety Management Report. Forming part of ESV’s objective to deliver effective risk- based regulation, compliance and enforcement, the GPI Safety Management Report provides important information about the degree of technical compliance from gas and pipeline industry participants. This report also highlights the status of the sector’s safety framework documentation, and its responses to auditing, monitoring, and reporting, and ESV’s response in terms of its near-term priorities. In the last three years, the GPI Safety Management Report has been a platform for comparative analysis, providing industry and government with a synopsis of safety performance throughout the gas and pipeline industry in Victoria. -

Media Release Gas Group's Hydrogen Push Moves Into Queensland

27 February 2020 Media Release Gas group’s hydrogen push moves into Queensland Australian Gas Networks (AGN) has expanded its national hydrogen push into Queensland. The move will see the establishment of AGN’s A$4.2 million* hydrogen plant in Gladstone, on the State’s central coast. AGN is part of the Australian Gas Infrastructure Group (AGIG), and now sees hydrogen projects being developed across four Australian States. The Gladstone plant will be Australia’s first renewable hydrogen production facility able to deliver up to 10% blended hydrogen across the city’s total 770 residential, small commercial and industrial customer base. The project - part of AGIG’s push to use zero-carbon hydrogen initiatives to decarbonise its operations - has attracted A$1.78 million in grant funding from the Queensland Government’s $15 million Hydrogen Industry Development Fund (HIDF). Gladstone is already home to Queensland and Australia’s east coast Liquefied Natural Gas production, processing and export industry. The entry of hydrogen as another local energy arm will generate new job, education, workplace training and regional economic growth opportunities. It is anticipated that plant construction will commence in November this year with commissioning by October next year with the plant becoming fully operational in December, 2021. Australian Gas Network’s Chief Executive Officer, Mr Ben Wilson: “Australian Gas Networks, part of Australian Gas Infrastructure Group, is proud to partner with the Queensland Government on this ground breaking project. Gladstone will become the first entire city in Australia to be on a blend of natural gas and hydrogen. “The project supports Gladstone’s vision to be a key hub for Queensland’s domestic and hydrogen export industry, just as it is for natural gas today. -

Evoenergy and Australian Gas Networks (SA) Gas Access Arrangement Proposals 2021-26 Submission August 2020

Evoenergy and Australian Gas Networks (SA) Gas access arrangement proposals 2021-26 Submission August 2020 Contents Overview .........................................................................................................4 Introduction .................................................................................................4 Summary .....................................................................................................4 Our approach ..................................................................................................5 What consumers are telling us ...................................................................6 The future of gas .............................................................................................8 What is the problem to be solved? .............................................................8 Frameworks for thinking about the problem ...............................................8 Evoenergy ..............................................................................................9 AGN SA ............................................................................................... 11 The Oxford Scenario Planning Approach ............................................ 12 Analysis of the building blocks ..................................................................... 14 Conclusion .................................................................................................... 17 2 Energy Consumers Australia Evoenergy and Australian Gas Networks (SA) Gas -

Sustainably Growing Our Future 2020 Annual Review We Are Australian Gas Infrastructure Group (AGIG) One of Australia’S Largest Gas Infrastructure Businesses

Sustainably Growing our Future 2020 Annual Review We are Australian Gas Infrastructure Group (AGIG) One of Australia’s largest gas infrastructure businesses. We own and operate infrastructure that delivers gas to Australian homes, businesses, and communities. We also deliver and store gas that supports the Australian economy for power generators, mines and manufacturers. We are taking active steps towards sustainable gas delivery today, and tomorrow. In 2021 we delivered Australia’s largest renewable gas production facility: Hydrogen Park South Australia. Our vision is to be the leading gas infrastructure business in Australia. We will achieve this by delivering for our customers, being a good employer and being sustainably cost efficient. AGIG builds and operates energy infrastructure across the value chain and across the country. Our portfolio of companies delivers for customers across Australia. DBP operates Western Australia’s principal gas transmission Contents system. Australian Gas Infrastructure Developments (AGID) operates unregulated transmission pipelines, gas processing and storage in Western Australia and the Northern Territory. Message from the Chairmen 02 Message from the CEO 04 About AGIG 08 Vision and Values 10 Operates gas distribution infrastructure in Victoria. Our Role in the Gas Industry 12 Delivering for Customers 15 Highlights 30 A Good Employer 35 Operates gas infrastructure (distribution and transmission pipelines) in Victoria, South Australia, Sustainably Cost Efficient 45 Queensland, New South Wales and the -

Electricity Offers 16

Essential Services Commission Contents Introduction 2 1. Changes to the energy rules 3 2. Enforcing compliance and resolving disputes 6 3. Energy offers and prices in 2017–18 8 4. Licensing energy businesses 13 What’s next? 14 Appendix A: Electricity offers 16 Appendix B: Gas offers 21 Victorian Energy Market Snapshot 2017–18 1 Introduction Energy companies must regularly report to us on This report meets our reporting obligations under how they are performing in Victoria’s energy Sections 54V and 54W of the Essential Services market. This includes information on how many Commission Act 2001, Section 39A of the residential and small customers they have in Electricity Industry Act 2000 and Section 47 of the Victoria, and the number of customers Gas Industry Act 2001. participating in their hardship program. However, due to delays in reasonable assurance Unfortunately, in August 2018, AGL told us it on AGL’s performance data, this report does not could not submit their 2017–18 performance report on the performance of retailers against report by the required date of 31 August 2018. indicators such as disconnections and Although AGL provided us with the data on 31 reconnections, market share, customer service, October 2018, it was not provided with reasonable and hardship program participants and debt levels of assurance in time. This means we are levels.1 unable to provide our regular annual report by the We will publish our comprehensive 2017–18 end of this year, which includes information on the annual report on the Victorian energy market in performance of retailers in 2017-18.