Eqt Annual Review — 20 Years Edition

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Work in Progress (1999.03.07)

_________________________________________________________________ WORK IN PROGRESS by Cliff Holden ______________________________ Hazelridge School of Painting Pl. 92 Langas 31193 Sweden www.cliffholden.co.uk copyright © CLIFF HOLDEN 2011 2 for Lisa 3 4 Contents Foreword 7 1 My Need to Paint 9 2 The Borough Group 13 3 The Stockholm Exhibition 28 4 Marstrand Designers 40 5 Serigraphy and Design 47 6 Relating to Clients 57 7 Cultural Exchange 70 8 Bomberg's Legacy 85 9 My Approach to Painting 97 10 Teaching and Practice 109 Joseph's Questions 132 5 6 Foreword “This is the commencement of a recording made by Cliff Holden on December 12, 1992. It is my birthday and I am 73 years old. ” It is now seven years since I made the first of the recordings which have been transcribed and edited to make the text of this book. I was persuaded to make these recordings by my friend, the art historian, Joseph Darracott. We had been friends for over forty years and finally I accepted that the project which he was proposing might be feasible and would be worth attempting. And so, in talking about my life as a painter, I applied myself to the discipline of working from a list of questions which had been prepared by Joseph. During our initial discussions about the book Joseph misunderstood my idea, which was to engage in a live dialogue with the cut and thrust of question and answer. The task of responding to questions which had been typed up in advance became much more difficult to deal with because an exercise such as this lacked the kind of stimulus which a live dialogue would have given to it. -

Conference Programme of the 6 Th Edition

International Conference The Future of Education 6th Edition Conference Programme 30 June - 1 July 2016 Grand Hotel Mediterraneo Lungarno del Tempio, 44 – Florence – Italy Thursday 30 June Friday 1 July Room A Room B Room C Room D Room A Room B Room C Room D 9:35 – 10:50 9:35 – 10:50 9:35 – 10:50 9:35 – 10:50 9:00 – 10:40 9:00 – 10:40 9:00 – 10:40 9:00 – 10:40 Education and Studies on Sharing Education Studies on Second Education and New Education and Transnational Art Education Human Rights Education Language Technologies Sustainability Business Groups Acquisition Workshop Coffee Break Coffee Break Poster Session: 10:50 – 11:20 Poster Session: 10:40 – 11:20 Room A Room B Room C Room D Room A Room B Room C Room D 11:20 – 13:00 11:20 – 13:00 11:20 – 13:00 11:20 – 13:00 11:20 – 13:00 11:20 – 13:00 11:20 – 13:00 11:20 – 13:00 Education and Support Students’ Innovative Teaching Studies on Second Education and New Innovative Teaching Transnational Art Education Society Employability/Funding and Learning Language Technologies and Learning Business Groups Opportunities Methodologies Acquisition Methodologies Workshop Lunch 13:00 – 14:30 Lunch 13:00 – 14:30 Room A Room B Room C Room D Room A Room B Room C Room D 14:30 – 16:35 14:30 – 16:35 14:30 – 16:35 14:30 – 16:35 14:30 – 16:10 14:30 – 16:10 14:30 – 16:10 14:30 – 16:10 Education and E-Learning Teacher Training Studies on Second Higher Education Studies on Education and Studies on Special Needs Language Education Science Education Acquisition Coffee Break Coffee Break Poster Session: 16:35 – -

Spørsmål Til Skole-Norge

Rapport 2021:3 Spørsmål til Skole-Norge Analyser og resultater fra Utdanningsdirektoratets spørreundersøkelse til lærere høsten 2020 Karl Solbue Vika Rapport 2021:3 Spørsmål til Skole-Norge Analyser og resultater fra Utdanningsdirektoratets spørreundersøkelse til lærere høsten 2020 Karl Solbue Vika Forfatter Rapport 2021:3 Utgitt av Nordisk institutt for studier av innovasjon, forskning og utdanning (NIFU) Adresse Postboks 2815 Tøyen, 0608 Oslo. Besøksadresse: Økernveien 9, 0653 Oslo. Prosjektnr. 20715-3 Oppdragsgiver Utdanningsdirektoratet Adresse Postboks 9359, Grønland, 0135 Oslo Fotomontasje NIFU ISBN 978-82-327-0499-6 ISSN 1892-2597 Copyri ht NIFU: CC BY-NC 4.0 g www.nifu.no Forord Nordisk institutt for studier av innovasjon, forskning og utdanning (NIFU) har en rammeavtale for 2017–2020 med Utdanningsdirektoratet om å gjennomføre halv- årlige spørreundersøkelser rettet mot skoler og skoleeiere. Undersøkelsene er kjent som Utdanningsdirektoratets spørringer. Temaene for de enkelte undersøkelsene avtales fra gang til gang og skal dekke Utdanningsdirektoratets kunnskapsbehov til enhver tid. Resultatene fra undersø- kelsene offentliggjøres i NIFUs ordinære rapportserie og foreligger nedlastbare i PDF-format på Utdanningsdirektoratets og NIFUs hjemmesider. Dette er en ekstra spørring blant lærere om fagfornyelsen og korona-situasjo- nen, som ble gjennomført på oppdrag fra Utdanningsdirektoratet og Universitetet i Oslo. I undersøkelsen inngår to respondentgrupper som er spurt om i alt ti ulike te- maer. Rapporten er i første rekke en tabellrapport hvor det i liten grad gjøres mer inngående analyser. Det er ikke skrevet noe samlet sammendrag for denne rapp- orten, men leseren henvises til oppsummeringene ved slutten av hvert kapittel. Prosjektleder for Utdanningsdirektoratets spørringer til Skole-Norge er Roger André Federici og Cay Gjerustad. -

Transcript of Interview with Sir Roger Gifford

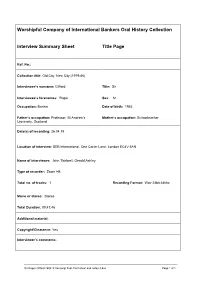

Worshipful Company of International Bankers Oral History Collection Interview Summary Sheet Title Page Ref. No.: Collection title: Old City, New City (1979-86) Interviewee’s surname: Gifford Title: Sir Interviewee’s forenames: Roger Sex: M Occupation: Banker Date of birth: 1955 Father’s occupation: Professor, St Andrew’s Mother’s occupation: Schoolteacher University, Scotland Date(s) of recording: 26.04.19 Location of interview: SEB International, One Carter Lane, London EC4V 5AN Name of interviewer: John Thirlwell, Gerald Ashley Type of recorder: Zoom H5 Total no. of tracks: 1 Recording Format: Wav 24bit 48khz Mono or stereo: Stereo Total Duration: 00:47:46 Additional material: Copyright/Clearance: Yes Interviewer’s comments: Sir Roger Gifford 260419 transcript final, front sheet and notes-3.doc Page 1 of 1 Introduction and biography #00:00:00# Graduate trainee at SG Warburg & Co Ltd; interviewed by #00:01:40# Siegmund Warburg #00:04:53# Banks’ graduate training schemes in the 1970’s i Move to Enskilda Securities (ES); ES’s ‘Big Bang’ structure; #00:06:38# relationship between ES and SEB and Wallenberg family Graduate training schemes in the 1970’s #00:10:15# Working in Enskilda Securities corporate finance #00:11:17# department Culture of the City – ‘the old school tie’; Americanisation of #00:12:38# the City - new capital, new structures Changes of business practice; conflicts of interest #00:19:32# Regulation by the Bank of England #00:21:26# Authorised banks and licensed deposit takers; funding and #00:23:07# growth of Enskilda Securities -

Annually Compounded Rate, 46–47 Annual Percentage Rate (APR

Index Note: Page numbers followed by n subprime mortgage crisis, 13, 168, Annually compounded rate, 46–47 indicate notes. 328–329, 355–356, 779–780 Annual percentage rate (APR), 35–38 transparency and, 861–862 Annuities, 28–33. See also Equivalent A Aggarwal, R., 307, 831n annual cost Aghion, P., 841n defined, 28 Aabar Investments, 853 AGL Resources Inc., 84 equivalent annual cash flow, Abandonment option, 254–256, 561–566 Agnblad, I., 856n 141–145 project life and, 564–565 Agrawal, D., 585n, 586n growing, 33–35 temporary, 565–566 AIG, 13, 355, 581 valuation of, 28–33 valuation of, 562–564 Airbus, 253, 567–569, 568n annual mortgage payments, 31–32 ABB, 856, 857 Aivasian, V., 462n annuities due, 31–32 Abnormal return, 318–319 Alcan, 793 future value, 32–33 Absolute priority, 451–452 Alcoa, 806 growing annuities, 33–35 Accelerated depreciation, 136–138, 139 Allayanis, G., 697 installment plan costing, 30 Accelerated underwritings, 377n Allen, Franklin, 163, 226n, 242, 329n, lottery winnings, 30–31 Accenture, 129 358, 409n, 410n, 412, 747–748, Anthony, R., 300n Accounting income, tax income 846n, 860n, 864, 869, 871n, 875n Antikarov, R. S., 572 versus, 137–138 Allen, J., 844 Antitrust law, mergers and, 805–806 Accounting rates of return, 711–713 Allen, L., 594 Aoki, M., 852n nature of, 711–712 Alliant, 834 AOL, 335, 793, 828 problems with, 712–713 Allied Crude Vegetable Oil Refining A&P, 681 Accounting standards, 705 Corporation, 780 Apex One, 793 Accounts payable, 134–135, 738, 740 Allman-Ward, M., 784 Apollo Management, 823 Accounts receivable, 134–135, Allocated overhead, in net present Apple Computer Inc., 369n, 555 733, 737–738, 757 value analysis, 131 Appropriation requests, 241–242 Accrued interest, 600 Alltel, 793 Aramark, 367 Acharya, V. -

Europeana DSI-3 B.2 Periodic Report M10.Pdf

Deployment and Maintenance of Europeana DSI core services - SMART 2016/1019 CONTRACT NUMBER - 30 - CE - 0885387/00-80 DELIVERABLE B.2 Periodic report 5 Revision 1.0 Date of submission 30 June 2018 (M10) Author(s) Victor-Jan Vos, Europeana Foundation Julia Schellenberg, Europeana Foundation Dissemination Level Public REVISION HISTORY AND STATEMENT OF ORIGINALITY Revision History Revision Date Author Organisation Description No. 0.1 25-06-2018 Julia Schellenberg Europeana Foundation First draft 1.0 29-06-2018 Victor-Jan Vos, Europeana Foundation Final version Julia Schellenberg Statement of originality: This deliverable contains original unpublished work except where clearly indicated otherwise. Acknowledgement of previously published material and of the work of others has been made through appropriate citation, quotation or both. The sole responsibility of this publication lies with the author. The European Union is not responsible for any use that may be made of the information contained therein. ‘Europeana DSI-3 is co-financed by the European Union's Connecting Europe Facility’. Europeana DSI-3 Deliverable B.2 Periodic Report M10 2 TABLE OF CONTENTS 1. Introduction 4 2. Highlights 5 3. Progress against objectives 10 A. Discovery, use and engagement for users in defined target groups, against user feedback 10 B. Optimise data and aggregation infrastructure 15 C. Improve content distribution mechanisms 21 D. Improve/widen distribution channels through partnerships 32 E. Coordinate, sustain and grow the network of data partners and experts 45 F. Maintain an international interoperable licensing framework 52 G. Implement and develop new strategies, services and business models 53 H. -

Highlights May J U N E /J U

m is “Honoring Tradition, Celebrating Diversity, and Building a Jewish Future” da U form J Re on for I Un E h t r of hIghlIghts be m E Thursday, May 3 at 7:30 pm—PErspectIves on ISraEl. First of a series on Israel and its challenges from viewpoints across the political spectrum. a m This presentation is by Matthew Gabe, AIPAC East Bay Director. See Page 8. is Sunday, May 6 at 10:00 am—annUal MeetIng of thE CongrEgatIon. th El E This event will include election of new officers for the Beth El Board B and a review of the synagogue’s finances. See Page 6 for more details. on I gat Friday, May 11 at 6:15 pm (for appetizers)—CElebratIon of EducatIon honoring Beth El’s E B’nei Mitzvah class, Confirmation class and high school (Midrasha) graduates. Dinner at 6:30 pm with the Shabbat service at 7:30 pm. Join us in celebrating May our students as they lead us in prayer and share with us their insights and reflections. Congr Please sign up for dinner at: https://bethelyouthed.wufoo.com/forms/z7x2s9/ Sunday, May 20 at 10:15 am—MidraSha gradUatIon. Celebrate with the 15 high school students from eight different synagogues who will be graduating this year. For more details, see Page 17. Friday, June 1 at 8:00 pm--CommEmoratIon of thE 100th birthday of raoUl WallEnberg, as one of the Righteous Gentiles who saved a large number of Hungarian Jewish children, including our Emeritus Rabbi Raj, during the Holocaust. -

How Does Family Control Influence a Firm's Acquisition and Divestiture

How Does Family Control Influence a Firm’s Acquisition and Divestiture Behavior? Evidence from Swedish Listed Firms Tim Käsbach∗ Christian Ludwigs† Stockholm School of Economics May 2014 Abstract This paper investigates how family control affects a firm’s propensity to undertake acquisitions and divestitures as well as the performance consequences of these transactions. Making use of manually collected data on 242 Swedish listed companies during the period 2003-2012, we do not find evidence that family firms are less likely to engage in acquisitions than non-family firms. However, we show that family firms have a higher aversion towards equity-financed acquisitions, especially when the amount of voting rights held by the family owner is not sufficient to ensure the preservation of control. The willingness of family firms to overcome this aversion is well received by investors as reflected in higher announcement returns. Although divestitures are on average value-enhancing, we find that family controlled firms are associated with a lower likelihood of divesting. Finally, we provide evidence that family firms are more likely to undertake diversifying acquisitions and less likely to divest unrelated businesses. Keywords: Family firms, acquisitions, divestitures, corporate diversification *[email protected] †[email protected] Acknowledgements: We would like to thank our tutor Michael Halling, Assistant Professor of Finance at the Stockholm School of Economics, for his insightful comments and guidance. Table of Content 1 Introduction -

Statement of Terrence J. Collins

Statements in Support of Petition for Rulemaking Statement Exhibit (w/ Hyperlink) Statement of Terrence J. Collins ....................................................................................................... Exhibit A Statement of Miriam L. Diamond ..................................................................................................... Exhibit B Statement of David A. Eastmond ...................................................................................................... Exhibit C Statement of David Epel ................................................................................................................... Exhibit D Statement of Rolf Halden .................................................................................................................. Exhibit E Statement of Kim Harley ................................................................................................................... Exhibit F Statement of Julie Herbstman .......................................................................................................... Exhibit G Statement of Susan Kasper ............................................................................................................... Exhibit H Statement of Donald Lucas ................................................................................................................ Exhibit I Statement of Sharyle Patton .............................................................................................................. Exhibit J Statement -

Wallenberg Sphere and Samsung Group Hwa-Jin Kim University of Michigan Law School, [email protected]

University of Michigan Law School University of Michigan Law School Scholarship Repository Articles Faculty Scholarship 2014 Concentrated Ownership and Corporate Control: Wallenberg Sphere and Samsung Group Hwa-Jin Kim University of Michigan Law School, [email protected] Available at: https://repository.law.umich.edu/articles/1763 Follow this and additional works at: https://repository.law.umich.edu/articles Part of the Business Organizations Law Commons, Comparative and Foreign Law Commons, and the Law and Economics Commons Recommended Citation Kim, Hwa-Jin. "Concentrated Ownership and Corporate Control: Wallenberg Sphere and Samsung Group." J. Korean L. 14, no. 1 (2014): 39-59. This Article is brought to you for free and open access by the Faculty Scholarship at University of Michigan Law School Scholarship Repository. It has been accepted for inclusion in Articles by an authorized administrator of University of Michigan Law School Scholarship Repository. For more information, please contact [email protected]. Journal of Korean Law | Vol. 14, 39-59, December 2014 Concentrated Ownership and Corporate Control: Wallenberg Sphere and Samsung Group* Hwa-Jin Kim** Abstract Samsung Group’s success cannot be attributed to its corporate governance structure, at least thus far. The corporate governance of Samsung has been rather controversial. As the group faces the succession issue the corporate governance has become as crucial as their new products and services. Samsung has discovered a role model on the other side of the planet, Wallenberg Sphere in Sweden. Much effort has been made to learn about Wallenberg’s arrangements and key to its success. However, a fundamental difference between the institutions in Sweden and Korea has made the corporate structures of the two groups radically different. -

Raoul Wallenberg a Story of Courage and Resistance During the Holocaust

Raoul Wallenberg A Story of Courage and Resistance During the Holocaust “We’re fighting … and that’s the main thing” ymark w photo: Ewa Memorial stone in Gothenburg of Raoul Wallenberg by the artist Charlotte Gyllenhammar. The monument was unveiled in 2007. In 1944, Raoul Wallenberg saved and protected thousands of Jews in Budapest from abuse at the hands of the Nazis and members of the Hungarian Arrow Cross Party. People throughout the world know about his efforts. He is an honorary citizen of three countries. Monuments in his honour have been built in many cities. Schools, squares and buildings bear the Wallenberg name. The memory of his historical deeds lives on in books, music and film. raoul Wallenberg For Ching sear To: Timony and pho Tes e VaT pri To: “My brother Gustav was an errand boy at Raoul Wallenberg’s office. He got the job since my family had business contacts yad Vashem | pho Timony: Tes were attacking our house, a so-called Swedish Kate (now Wacz), 12 years old, and her brother “One night when the Arrow Cross soldiers seriously wounded but, as luck would have it, in Sweden. Mother, I and my brother all received I was taken care of andsafe received house, treatment I was struck in by a bullet. I was Esther Schlesinger, 7 years old. Gustav Kadelburger, 15 years old. under the protection of “We lived in a house the Swedish Embassy” protective passports.” the ghetto.” raoul wallenberg my mother, father and brothers lived. All the Jews were chased out into Danube River where they were murdered. -

Power Politics and the Empire of Economics: an Introduction

Power Politics and the Empire of Economics: An Introduction By: Andrew Gavin Marshall The President sat and listened to his closest adviser as they plotted a strategy to maintain Western domination of the world economy. The challenge was immense: divisions between industrial countries were growing as the poor nations of the world were becoming increasingly united in opposition to the Western world order. From Africa, across the Middle East, to Asia and Latin America, the poor (or ‘developing’) countries were calling for the establishment of a ‘New International Economic Order,’ one which would not simply serve the interests of the United States, Western Europe, and the other rich, industrial nations, but the world as a whole. It was on the 24th of May 1975 when President Gerald Ford was meeting with his Secretary of State and National Security Adviser, Henry Kissinger, easily the two most powerful political officials in the world at the time. Kissinger told the President: “The trick in the world now is to use economics to build a world political structure.”1 Ford and Kissinger agreed that the United States could not accept a new ‘economic order’ that would undermine American and Western power throughout the world. Uprisings, revolutions and liberation movements across Africa, Asia and beyond had largely thrown off the shackles of European colonial domination, establishing themselves as independent political nation-states with their own interests and objectives. Chief among those goals was for economic independence to follow political independence, to take control of their own resources and economies from the Europeans and Americans, to determine their own economic policies and help to redistribute global wealth along equal and just lines.