Happinet / 7552

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Vaitoskirjascientific MASCULINITY and NATIONAL IMAGES IN

Faculty of Arts University of Helsinki, Finland SCIENTIFIC MASCULINITY AND NATIONAL IMAGES IN JAPANESE SPECULATIVE CINEMA Leena Eerolainen DOCTORAL DISSERTATION To be presented for public discussion with the permission of the Faculty of Arts of the University of Helsinki, in Room 230, Aurora Building, on the 20th of August, 2020 at 14 o’clock. Helsinki 2020 Supervisors Henry Bacon, University of Helsinki, Finland Bart Gaens, University of Helsinki, Finland Pre-examiners Dolores Martinez, SOAS, University of London, UK Rikke Schubart, University of Southern Denmark, Denmark Opponent Dolores Martinez, SOAS, University of London, UK Custos Henry Bacon, University of Helsinki, Finland Copyright © 2020 Leena Eerolainen ISBN 978-951-51-6273-1 (paperback) ISBN 978-951-51-6274-8 (PDF) Helsinki: Unigrafia, 2020 The Faculty of Arts uses the Urkund system (plagiarism recognition) to examine all doctoral dissertations. ABSTRACT Science and technology have been paramount features of any modernized nation. In Japan they played an important role in the modernization and militarization of the nation, as well as its democratization and subsequent economic growth. Science and technology highlight the promises of a better tomorrow and future utopia, but their application can also present ethical issues. In fiction, they have historically played a significant role. Fictions of science continue to exert power via important multimedia platforms for considerations of the role of science and technology in our world. And, because of their importance for the development, ideologies and policies of any nation, these considerations can be correlated with the deliberation of the role of a nation in the world, including its internal and external images and imaginings. -

Models of Time Travel

MODELS OF TIME TRAVEL A COMPARATIVE STUDY USING FILMS Guy Roland Micklethwait A thesis submitted for the degree of Doctor of Philosophy of The Australian National University July 2012 National Centre for the Public Awareness of Science ANU College of Physical and Mathematical Sciences APPENDIX I: FILMS REVIEWED Each of the following film reviews has been reduced to two pages. The first page of each of each review is objective; it includes factual information about the film and a synopsis not of the plot, but of how temporal phenomena were treated in the plot. The second page of the review is subjective; it includes the genre where I placed the film, my general comments and then a brief discussion about which model of time I felt was being used and why. It finishes with a diagrammatic representation of the timeline used in the film. Note that if a film has only one diagram, it is because the different journeys are using the same model of time in the same way. Sometimes several journeys are made. The present moment on any timeline is always taken at the start point of the first time travel journey, which is placed at the origin of the graph. The blue lines with arrows show where the time traveller’s trip began and ended. They can also be used to show how information is transmitted from one point on the timeline to another. When choosing a model of time for a particular film, I am not looking at what happened in the plot, but rather the type of timeline used in the film to describe the possible outcomes, as opposed to what happened. -

BANDAI NAMCO Holdings Inc

BANDAI NAMCO Holdings Inc. Notice of the Fifteenth Ordinary General Meeting of Shareholders to be held on June 22, 2020 An English translation of the original notice in Japanese DISCLAIMER The following is an English translation of the Japanese original “Notice of the Fifteenth Ordinary General Meeting of Shareholders of BANDAI NAMCO Holdings Inc.” which meeting is to be held on June 22, 2020. The Company provides this translation for your reference and convenience only and does not guarantee its accuracy or otherwise. In the event of any discrepancies, the Japanese original notice shall prevail. These documents have been prepared solely in accordance with Japanese law and are offered here for informational purposes only. In particular, please note that the financial statements included in the following translation have been prepared in accordance with Japanese GAAP. * The English version of this Notice of the Fifteenth Ordinary General Meeting of Shareholders reflects the revisions announced in “Notice Regarding Partial Revision to the Notice of the Fifteenth Ordinary General Meeting of Shareholders” (in Japanese only) released on June 1, 2020 and June 10, 2020. 1 Securities code: 7832 June 5, 2020 5-37-8 Shiba, Minato-ku, Tokyo BANDAI NAMCO Holdings Inc. Mitsuaki Taguchi President and Representative Director Dear Shareholders, NOTICE OF THE FIFTEENTH ORDINARY GENERAL MEETING OF SHAREHOLDERS We would like to inform you that the Fifteenth Ordinary General Meeting of Shareholders of BANDAI NAMCO Holdings Inc. (“the Company”) will be held as set forth below. Although we will hold the General Meeting of Shareholders while being as thorough as possible in taking measures to prevent infection, for this fiscal year, we encourage you to exercise your voting rights in writing or via the Internet in advance instead of attending the meeting in order to prevent the spread of COVID-19. -

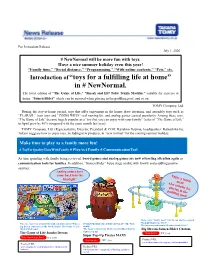

Introduction Of“Toys for a Fulfilling Life at Home” in # Newnormal

For Immediate Release July 1, 2020 # NewNormal will be more fun with toys. Have a nice summer holiday even this year! “Family time,” “Social distance,” “Programming,” “With online contents,” “Pets,” etc. Introduction of “toys for a fulfilling life at home” in # NewNormal. The latest edition of “The Game of Life,” “Smash and Hit! Table Tennis Machine” suitable for exercise at home, “Somen Slider” which can be enjoyed when playing in the paddling pool, and so on. TOMY Company, Ltd. During the stay-at-home period, toys that offer enjoyment in the house drew attention, and assembly toys such as “PLARAIL” train toys and “ZOIDS WILD” real moving kit, and analog games earned popularity. Among these toys, “The Game of Life” became hugely popular as a “toy that you can enjoy with your family” (sales of “The Game of Life” in April grew by 40% compared with the same month last year). TOMY Company, Ltd. (Representative Director, President & COO: Kazuhiro Kojima, headquarters: Katsushika-ku, Tokyo) suggests how to enjoy toys, including new products, in “new normal” for the coming summer holiday. Make time to play as a family more fun! # ToyForQualityTimeWithFamily # PlayAsAFamily # CommunicationTool As time spending with family being reviewed, board games and analog games are now attracting attention again as communication tools for families. In addition, “Somen Slider” helps stage a table with family and paddling pool in summer. Analog games have come back into the limelight! Make your “family meal” fun! It can also be enjoyed when playing in the -

ISSUE #163 February 2021 February CONTENTS 2021 163

The VOICE of the FAMILY in GAMING TM Final Fantasy XVI, Monster Hunter Rise, Slide Stars, and more this is- sue. Survey Says: “Fam- ily Feud Video Game for Fami- lies!” ISSUE #163 February 2021 February CONTENTS 2021 163 Links: Home Page Section Page(s) Editor’s Desk 4 Female Side 5 Comics 7 Sound Off 8 - 10 Look Back 12 Quiz 13 Devotional 14 In The News 16 - 23 We Would Play That! 24 Reviews 25 - 37 Sports 38 - 41 Developing Games 42 - 67 Now Playing 68 - 83 Last Minute Tidbits 84 - 106 “Family Friendly Gaming” is trademarked. Contents of Family Friendly Gaming is the copyright of Paul Bury, and Yolanda Bury with the exception of trademarks and related indicia (example Digital Praise); which are prop- erty of their individual owners. Use of anything in Family Friendly Gaming that Paul and Yolanda Bury claims copyright to is a violation of federal copyright law. Contact the editor at the business address of: Family Friendly Gaming 7910 Autumn Creek Drive Cordova, TN 38018 [email protected] Trademark Notice Nintendo, Sony, Microsoft all have trademarks on their respective machines, and games. The current seal of approval, and boy/girl pics were drawn by Elijah Hughes thanks to a wonderful donation from Tim Emmerich. Peter and Noah are inspiration to their parents. Family Friendly Gaming Page 2 Page 3 Family Friendly Gaming Editor’s Desk FEMALE SIDE million that got infected with it. That was one propaganda artist trying to do damage con- Ups and Downs third of the human population at the time. -

TOKYO GAME SHOW 2020 ONLINE Starts !

The Future Touches Gaming First. Press Release September 24, 2020 TOKYO GAME SHOW 2020 ONLINE Starts ! Official Program Streaming from 20:00, September 24 in JST/UTC+9 Computer Entertainment Supplier’s Association Computer Entertainment Supplier’s Association (CESA, Chairman: Hideki Hayakawa) announces that TOKYO GAME SHOW 2020 ONLINE (TGS2020 ONLINE: https://tgs.cesa.or.jp/) has opened for the five- day period from September 23 (Wed.) to 27 (Sun.), 2020. Online business matching started yesterday, and official program streaming will kick off with the Opening Event from 20:00, Thursday, September 24 (JST/ UTC+9) featuring the Official Supporter Hajime Syacho and other popular figures. The Official Program page offers 35 Exhibitor Programs delivering the latest news and 16 Organizer’s Projects including Keynote Speech, four competitions of e-Sports X, the indie game presentation event SENSE of WONDER NIGHT (SOWN), and the announcement and awarding for each category of Japan Game Awards. No pre-registration or log-in is required to enjoy viewing the programs for free of charge. Keynote Speech, Grand Award of Japan Game Awards 2020 and SOWN will be streamed in English as well as Japanese for global audience in Asia and other parts of the world. In TGS2020 ONLINE, 424 companies and organizations from 34 countries and regions exhibit in a virtual space, providing the updates on newly-released titles and services through streaming and each exhibitor’s page. By region, more companies and organizations from overseas (221) exhibit in this year’s TGS than those from Japan (203). Ten or more exhibitors participate from South Korea (46), China (22), Canada (20), Taiwan (19), the United States (17), Poland (13), and Colombia (10). -

Happinet / 7552

R Happinet / 7552 COVERAGE INITIATED ON: 2014.03.06 LAST UPDATE: 2021.05.14 Shared Research Inc. has produced this report by request from the company discussed in the report. The aim is to provide an “owner’s manual” to investors. We at Shared Research Inc. make every effort to provide an accurate, objective, and neutral analysis. In order to highlight any biases, we clearly attribute our data and findings. We will always present opinions from company management as such. Our views are ours where stated. We do not try to convince or influence, only inform. We appreciate your suggestions and feedback. Write to us at [email protected] or find us on Bloomberg. Research Coverage Report by Shared Research Inc. Happinet / 7552 R LAST UPDATE: 2021.05.14 Research Coverage Report by Shared Research Inc. | https://sharedresearch.jp Coverage INDEX How to read a Shared Research report: This report begins with the trends and outlook section, which discusses the company’s most recent earnings. First-time readers should start at the business section later in the report. Key financial data ------------------------------------------------------------------------------------------------------------------------------------- 3 Recent updates ---------------------------------------------------------------------------------------------------------------------------------------- 4 Highlights ------------------------------------------------------------------------------------------------------------------------------------------------------------4 -

Over 570 Eligible Titles!

Over 570 eligible titles! Games Eligible for this Promotion - Last Updated 7/22/21 GAME NSW PS4 PS5 XB1 XBX 1-2-SWITCH 13 SENTIELS: AEGIS RIM 30 IN 1 GAME COLLECTION A HAT IN TIME NSW ADAMS VENTURE ORIGIN ADDAMS FAMILY MAN MAY AGE OF WONDERS PLANETFALL AI SOMNIUM FILES NIR IN AIR CONFLICTS DBL PK AIR MISSIONS HIND AKIBAS TRIP & HELLBOUND ALEX KIDD IN MIRACLE WD ALIENS FIRETEAM ELITE AMULET OF CHAOS DONJON ADV ANCESTORS LEGACY ANGRY BRDS 2 UNDR PRSR ANIMA: GATE OF MEMORIES ANIMAL CROSSING NEW HOR AO TENNIS 2 ARAGAMI 2 ARC OF ALCHEMIST ARMS ARY AND SECRET OF SEASONS ASSASSINS CREED VALHAL ASSETTO CORSA ASSETTO CORSA COMPETIZIONE ASTRAL CHAIN ATELIER LULUA SCION ARLND ATELIER RYZA 2 LOST LEGNDS ATELIER SECRET HIDEOUT ATELIER SOPHIE: ALCHMST ATTACK ON TITAN ATTACK ON TITAN2 FINAL BTL AVICII INVECTOR ENCORE ED AXIOM VERGE MULTIVERSE ED AZUR LANE CROSSWAVE BAKUGAN CHAMPN VEST DLX ED BALAN WONDERWORLD BALDURS GATE 1&2 ENH ED BASS PRO SHOP BAYONETTA & VANQ ANV REG Some Restrictions Apply. This is only a guide. Trade values are constantly changing. Please consult your local EB Games for the most updated trade values. Over 570 eligible titles! Games Eligible for this Promotion - Last Updated 7/22/21 GAME NSW PS4 PS5 XB1 XBX BAYONETTA & VNQUISH 10 ANV BAYONETTA 2 BEAST QUEST LE BEE SIMULATOR BIG RUMBLE BOXING CREED BIOMUTANT BLACKSAD UNDER THE SKIN LE BLADED FURY BLASPHEMOUS DEL ED BLASPHEMOUS DEL ED HG BLAZE & MONSTER MACH XCR BLOODSTAINED BLOODSTAINED COM BLUE FIRE BOUNTY BATTLE BRAVELY DEFAULT 2 BUGSNAX BUILDINGS HAVE FEELINGS BURGER TIME PARTY NSW BURNOUT REMASTERED CABELA HUNT CADENCE OF HYRULE NECRO CAFE ENCHANTE CALL OF CTHULHU NSW CANT DRIVE THIS HG CAPTAIN TOAD TT CATHERINE FULL BODY CHILDREN OF MORTA CHIVALRY 2 CLASSIC RACER ELITE CLOUDPUNK CLUBHOUSE GAMES COBRA KAI COD BLACK OPS COLD WAR COD MODERN WARFARE COD MW PRECISION ED CODE REALIZE FTR BLSSNG D1 CODE REALIZE FUTRE BLSSNGS CODE REALIZE GUARDN RBRTH CODE REALIZE WINTERTIDE COLLAR X MALICE Some Restrictions Apply. -

BANDAI NAMCO Group FACT BOOK 2019 BANDAI NAMCO Group FACT BOOK 2019

BANDAI NAMCO Group FACT BOOK 2019 BANDAI NAMCO Group FACT BOOK 2019 TABLE OF CONTENTS 1 BANDAI NAMCO Group Outline 3 Related Market Data Group Organization Toys and Hobby 01 Overview of Group Organization 20 Toy Market 21 Plastic Model Market Results of Operations Figure Market 02 Consolidated Business Performance Capsule Toy Market Management Indicators Card Product Market 03 Sales by Category 22 Candy Toy Market Children’s Lifestyle (Sundries) Market Products / Service Data Babies’ / Children’s Clothing Market 04 Sales of IPs Toys and Hobby Unit Network Entertainment 06 Network Entertainment Unit 22 Game App Market 07 Real Entertainment Unit Top Publishers in the Global App Market Visual and Music Production Unit 23 Home Video Game Market IP Creation Unit Real Entertainment 23 Amusement Machine Market 2 BANDAI NAMCO Group’s History Amusement Facility Market History 08 BANDAI’s History Visual and Music Production NAMCO’s History 24 Visual Software Market 16 BANDAI NAMCO Group’s History Music Content Market IP Creation 24 Animation Market Notes: 1. Figures in this report have been rounded down. 2. This English-language fact book is based on a translation of the Japanese-language fact book. 1 BANDAI NAMCO Group Outline GROUP ORGANIZATION OVERVIEW OF GROUP ORGANIZATION Units Core Company Toys and Hobby BANDAI CO., LTD. Network Entertainment BANDAI NAMCO Entertainment Inc. BANDAI NAMCO Holdings Inc. Real Entertainment BANDAI NAMCO Amusement Inc. Visual and Music Production BANDAI NAMCO Arts Inc. IP Creation SUNRISE INC. Affiliated Business -

Family Friendly Magazine 159 in PDF Format

The VOICE of the FAMILY in GAMING TM Crash Bandicoot Paw Patrol 4, Ben 10 Power Mighty Pups Trip, NBA 2K21, Save Adventure and more this is- Bay is coming sue. for kids. ISSUE #159 October 2020 October CONTENTS 2020 159 Links: Home Page Section Page(s) Editor’s Desk 4 Female Side 5 Comics 7 Sound Off 8 - 10 Look Back 12 Quiz 13 Devotional 14 In The News 16 - 23 We Would Play That! 24 Reviews 25 - 37 Sports 38 - 41 Developing Games 42 - 67 Now Playing 68 - 83 Last Minute Tidbits 84 - 106 “Family Friendly Gaming” is trademarked. Contents of Family Friendly Gaming is the copyright of Paul Bury, and Yolanda Bury with the exception of trademarks and related indicia (example Digital Praise); which are prop- erty of their individual owners. Use of anything in Family Friendly Gaming that Paul and Yolanda Bury claims copyright to is a violation of federal copyright law. Contact the editor at the business address of: Family Friendly Gaming 7910 Autumn Creek Drive Cordova, TN 38018 [email protected] Trademark Notice Nintendo, Sony, Microsoft all have trademarks on their respective machines, and games. The current seal of approval, and boy/girl pics were drawn by Elijah Hughes thanks to a wonderful donation from Tim Emmerich. Peter and Noah are inspiration to their parents. Family Friendly Gaming Page 2 Page 3 Family Friendly Gaming Editor’s Desk FEMALE SIDE for doing videos as well. I keep working on social media. Using the Opportunity getting better with each video. Just like I keep Growth working on getting better with each issue of Growth also means we attract the attention There are all kinds of memes bemoaning 2020. -

AVDE Avantis International Equity ETF Gray Swan

ETF Risk Report: AVDE Buyer beware: Every ETF holds the full risk of its underlying equities Disclosures in the best interest of investors Avantis International Equity ETF Gray Swan Event Risks exist for every equity held by AVDE. Gray swan events include accounting fraud, management failures, failed internal controls, M&A problems, restatements, etc. These risks occur Gray Swan Event Factor for AVDE 1.10% infrequently, but consistently for all equities. Equities account for 94.19% of AVDE’s assets. Most investors ignore these risks until after they are disclosed; whereupon a stock’s price drops precipitously. Just as insurance companies can predict likely costs for a driver’s future car accidents based on the driver’s history, Watchdog Research contacts each ETF asking how they notify investors about we predict the likely cost (price drop) for AVDE following accounting governance risks in equities in their fund. We will publish their response gray swan disclosures within its holdings. The expected when received. price decrease across the AVDE equity portfolio is 1.10%. However, individual equity risks vary signicantly. This report helps investors know their risk exposure. Inception Date: 09/24/2020 Year-to-Date Return: 5.80% Actively managed, the fund seeks long-term capital appreciation by investing in a diverse group of non-U.S. Net Assets: $663m 1-Year Return: 55.03% companies across countries, market sectors, and industry groups. The fund seeks securities of companies that it Price: $60.51 3-Year Return: NA expects to have higher returns by placing an enhanced Net Asset Value (NAV): $60.30 5-Year Return: NA emphasis on securities of companies with smaller market capitalizations and securities of companies it denes as Net Expense Ratio: 0.23% Yield: 1.54% high protability or value companies. -

Happinet / 7552

R Happinet / 7552 COVERAGE INITIATED ON: 2014.03.06 LAST UPDATE: 2020.06.26 Shared Research Inc. has produced this report by request from the company discussed in the report. The aim is to provide an “owner’s manual” to investors. We at Shared Research Inc. make every effort to provide an accurate, objective, and neutral analysis. In order to highlight any biases, we clearly attribute our data and findings. We will always present opinions from company management as such. Our views are ours where stated. We do not try to convince or influence, only inform. We appreciate your suggestions and feedback. Write to us at [email protected] or find us on Bloomberg. Research Coverage Report by Shared Research Inc. Happinet / 7552 R LAST UPDATE: 2020.06.26 Research Coverage Report by Shared Research Inc. | https://sharedresearch.jp Coverage INDEX How to read a Shared Research report: This report begins with the trends and outlook section, which discusses the company’s most recent earnings. First-time readers should start at the business section later in the report. Key financial data ------------------------------------------------------------------------------------------------------------------------------------- 3 Recent updates ---------------------------------------------------------------------------------------------------------------------------------------- 4 Highlights ------------------------------------------------------------------------------------------------------------------------------------------------------------4