Happinet / 7552

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Vaitoskirjascientific MASCULINITY and NATIONAL IMAGES IN

Faculty of Arts University of Helsinki, Finland SCIENTIFIC MASCULINITY AND NATIONAL IMAGES IN JAPANESE SPECULATIVE CINEMA Leena Eerolainen DOCTORAL DISSERTATION To be presented for public discussion with the permission of the Faculty of Arts of the University of Helsinki, in Room 230, Aurora Building, on the 20th of August, 2020 at 14 o’clock. Helsinki 2020 Supervisors Henry Bacon, University of Helsinki, Finland Bart Gaens, University of Helsinki, Finland Pre-examiners Dolores Martinez, SOAS, University of London, UK Rikke Schubart, University of Southern Denmark, Denmark Opponent Dolores Martinez, SOAS, University of London, UK Custos Henry Bacon, University of Helsinki, Finland Copyright © 2020 Leena Eerolainen ISBN 978-951-51-6273-1 (paperback) ISBN 978-951-51-6274-8 (PDF) Helsinki: Unigrafia, 2020 The Faculty of Arts uses the Urkund system (plagiarism recognition) to examine all doctoral dissertations. ABSTRACT Science and technology have been paramount features of any modernized nation. In Japan they played an important role in the modernization and militarization of the nation, as well as its democratization and subsequent economic growth. Science and technology highlight the promises of a better tomorrow and future utopia, but their application can also present ethical issues. In fiction, they have historically played a significant role. Fictions of science continue to exert power via important multimedia platforms for considerations of the role of science and technology in our world. And, because of their importance for the development, ideologies and policies of any nation, these considerations can be correlated with the deliberation of the role of a nation in the world, including its internal and external images and imaginings. -

Models of Time Travel

MODELS OF TIME TRAVEL A COMPARATIVE STUDY USING FILMS Guy Roland Micklethwait A thesis submitted for the degree of Doctor of Philosophy of The Australian National University July 2012 National Centre for the Public Awareness of Science ANU College of Physical and Mathematical Sciences APPENDIX I: FILMS REVIEWED Each of the following film reviews has been reduced to two pages. The first page of each of each review is objective; it includes factual information about the film and a synopsis not of the plot, but of how temporal phenomena were treated in the plot. The second page of the review is subjective; it includes the genre where I placed the film, my general comments and then a brief discussion about which model of time I felt was being used and why. It finishes with a diagrammatic representation of the timeline used in the film. Note that if a film has only one diagram, it is because the different journeys are using the same model of time in the same way. Sometimes several journeys are made. The present moment on any timeline is always taken at the start point of the first time travel journey, which is placed at the origin of the graph. The blue lines with arrows show where the time traveller’s trip began and ended. They can also be used to show how information is transmitted from one point on the timeline to another. When choosing a model of time for a particular film, I am not looking at what happened in the plot, but rather the type of timeline used in the film to describe the possible outcomes, as opposed to what happened. -

BANDAI NAMCO Holdings Inc

BANDAI NAMCO Holdings Inc. Notice of the Fifteenth Ordinary General Meeting of Shareholders to be held on June 22, 2020 An English translation of the original notice in Japanese DISCLAIMER The following is an English translation of the Japanese original “Notice of the Fifteenth Ordinary General Meeting of Shareholders of BANDAI NAMCO Holdings Inc.” which meeting is to be held on June 22, 2020. The Company provides this translation for your reference and convenience only and does not guarantee its accuracy or otherwise. In the event of any discrepancies, the Japanese original notice shall prevail. These documents have been prepared solely in accordance with Japanese law and are offered here for informational purposes only. In particular, please note that the financial statements included in the following translation have been prepared in accordance with Japanese GAAP. * The English version of this Notice of the Fifteenth Ordinary General Meeting of Shareholders reflects the revisions announced in “Notice Regarding Partial Revision to the Notice of the Fifteenth Ordinary General Meeting of Shareholders” (in Japanese only) released on June 1, 2020 and June 10, 2020. 1 Securities code: 7832 June 5, 2020 5-37-8 Shiba, Minato-ku, Tokyo BANDAI NAMCO Holdings Inc. Mitsuaki Taguchi President and Representative Director Dear Shareholders, NOTICE OF THE FIFTEENTH ORDINARY GENERAL MEETING OF SHAREHOLDERS We would like to inform you that the Fifteenth Ordinary General Meeting of Shareholders of BANDAI NAMCO Holdings Inc. (“the Company”) will be held as set forth below. Although we will hold the General Meeting of Shareholders while being as thorough as possible in taking measures to prevent infection, for this fiscal year, we encourage you to exercise your voting rights in writing or via the Internet in advance instead of attending the meeting in order to prevent the spread of COVID-19. -

TOKYO GAME SHOW 2020 ONLINE Starts !

The Future Touches Gaming First. Press Release September 24, 2020 TOKYO GAME SHOW 2020 ONLINE Starts ! Official Program Streaming from 20:00, September 24 in JST/UTC+9 Computer Entertainment Supplier’s Association Computer Entertainment Supplier’s Association (CESA, Chairman: Hideki Hayakawa) announces that TOKYO GAME SHOW 2020 ONLINE (TGS2020 ONLINE: https://tgs.cesa.or.jp/) has opened for the five- day period from September 23 (Wed.) to 27 (Sun.), 2020. Online business matching started yesterday, and official program streaming will kick off with the Opening Event from 20:00, Thursday, September 24 (JST/ UTC+9) featuring the Official Supporter Hajime Syacho and other popular figures. The Official Program page offers 35 Exhibitor Programs delivering the latest news and 16 Organizer’s Projects including Keynote Speech, four competitions of e-Sports X, the indie game presentation event SENSE of WONDER NIGHT (SOWN), and the announcement and awarding for each category of Japan Game Awards. No pre-registration or log-in is required to enjoy viewing the programs for free of charge. Keynote Speech, Grand Award of Japan Game Awards 2020 and SOWN will be streamed in English as well as Japanese for global audience in Asia and other parts of the world. In TGS2020 ONLINE, 424 companies and organizations from 34 countries and regions exhibit in a virtual space, providing the updates on newly-released titles and services through streaming and each exhibitor’s page. By region, more companies and organizations from overseas (221) exhibit in this year’s TGS than those from Japan (203). Ten or more exhibitors participate from South Korea (46), China (22), Canada (20), Taiwan (19), the United States (17), Poland (13), and Colombia (10). -

Happinet / 7552

Happinet / 7552 COVERAGE INITIATED ON: 2014.03.06 LAST UPDATE: 2021.07.12 Shared Research Inc. has produced this report by request from the company discussed in the report. The aim is to provide an “owner’s manual” to investors. We at Shared Research Inc. make every effort to provide an accurate, objective, and neutral analysis. In order to highlight any biases, we clearly attribute our data and findings. We will always present opinions from company management as such. Our views are ours where stated. We do not try to convince or influence, only inform. We appreciate your suggestions and feedback. Write to us at [email protected] or find us on Bloomberg. Research Coverage Report by Shared Research Inc. Happinet / 7552 RCoverage LAST UPDATE: 2021.07.12 Research Coverage Report by Shared Research Inc. | https://sharedresearch.jp INDEX How to read a Shared Research report: This report begins with the trends and outlook section, which discusses the company’s most recent earnings. First-time readers should start at the business section later in the report. Key financial data ------------------------------------------------------------------------------------------------------------------------------------- 3 Recent updates ---------------------------------------------------------------------------------------------------------------------------------------- 4 Highlights ------------------------------------------------------------------------------------------------------------------------------------------------------------ 4 -

BANDAI NAMCO Group FACT BOOK 2019 BANDAI NAMCO Group FACT BOOK 2019

BANDAI NAMCO Group FACT BOOK 2019 BANDAI NAMCO Group FACT BOOK 2019 TABLE OF CONTENTS 1 BANDAI NAMCO Group Outline 3 Related Market Data Group Organization Toys and Hobby 01 Overview of Group Organization 20 Toy Market 21 Plastic Model Market Results of Operations Figure Market 02 Consolidated Business Performance Capsule Toy Market Management Indicators Card Product Market 03 Sales by Category 22 Candy Toy Market Children’s Lifestyle (Sundries) Market Products / Service Data Babies’ / Children’s Clothing Market 04 Sales of IPs Toys and Hobby Unit Network Entertainment 06 Network Entertainment Unit 22 Game App Market 07 Real Entertainment Unit Top Publishers in the Global App Market Visual and Music Production Unit 23 Home Video Game Market IP Creation Unit Real Entertainment 23 Amusement Machine Market 2 BANDAI NAMCO Group’s History Amusement Facility Market History 08 BANDAI’s History Visual and Music Production NAMCO’s History 24 Visual Software Market 16 BANDAI NAMCO Group’s History Music Content Market IP Creation 24 Animation Market Notes: 1. Figures in this report have been rounded down. 2. This English-language fact book is based on a translation of the Japanese-language fact book. 1 BANDAI NAMCO Group Outline GROUP ORGANIZATION OVERVIEW OF GROUP ORGANIZATION Units Core Company Toys and Hobby BANDAI CO., LTD. Network Entertainment BANDAI NAMCO Entertainment Inc. BANDAI NAMCO Holdings Inc. Real Entertainment BANDAI NAMCO Amusement Inc. Visual and Music Production BANDAI NAMCO Arts Inc. IP Creation SUNRISE INC. Affiliated Business -

AVDE Avantis International Equity ETF Gray Swan

ETF Risk Report: AVDE Buyer beware: Every ETF holds the full risk of its underlying equities Disclosures in the best interest of investors Avantis International Equity ETF Gray Swan Event Risks exist for every equity held by AVDE. Gray swan events include accounting fraud, management failures, failed internal controls, M&A problems, restatements, etc. These risks occur Gray Swan Event Factor for AVDE 1.10% infrequently, but consistently for all equities. Equities account for 94.19% of AVDE’s assets. Most investors ignore these risks until after they are disclosed; whereupon a stock’s price drops precipitously. Just as insurance companies can predict likely costs for a driver’s future car accidents based on the driver’s history, Watchdog Research contacts each ETF asking how they notify investors about we predict the likely cost (price drop) for AVDE following accounting governance risks in equities in their fund. We will publish their response gray swan disclosures within its holdings. The expected when received. price decrease across the AVDE equity portfolio is 1.10%. However, individual equity risks vary signicantly. This report helps investors know their risk exposure. Inception Date: 09/24/2020 Year-to-Date Return: 5.80% Actively managed, the fund seeks long-term capital appreciation by investing in a diverse group of non-U.S. Net Assets: $663m 1-Year Return: 55.03% companies across countries, market sectors, and industry groups. The fund seeks securities of companies that it Price: $60.51 3-Year Return: NA expects to have higher returns by placing an enhanced Net Asset Value (NAV): $60.30 5-Year Return: NA emphasis on securities of companies with smaller market capitalizations and securities of companies it denes as Net Expense Ratio: 0.23% Yield: 1.54% high protability or value companies. -

Happinet / 7552

R Happinet / 7552 COVERAGE INITIATED ON: 2014.03.06 LAST UPDATE: 2020.06.26 Shared Research Inc. has produced this report by request from the company discussed in the report. The aim is to provide an “owner’s manual” to investors. We at Shared Research Inc. make every effort to provide an accurate, objective, and neutral analysis. In order to highlight any biases, we clearly attribute our data and findings. We will always present opinions from company management as such. Our views are ours where stated. We do not try to convince or influence, only inform. We appreciate your suggestions and feedback. Write to us at [email protected] or find us on Bloomberg. Research Coverage Report by Shared Research Inc. Happinet / 7552 R LAST UPDATE: 2020.06.26 Research Coverage Report by Shared Research Inc. | https://sharedresearch.jp Coverage INDEX How to read a Shared Research report: This report begins with the trends and outlook section, which discusses the company’s most recent earnings. First-time readers should start at the business section later in the report. Key financial data ------------------------------------------------------------------------------------------------------------------------------------- 3 Recent updates ---------------------------------------------------------------------------------------------------------------------------------------- 4 Highlights ------------------------------------------------------------------------------------------------------------------------------------------------------------4 -

Catalogue Record

___________________________________________________________________________ 2021/CTI/WKSP2/009 Day 1 Session 2 Specific Aspects of Copyright and Related Rights Protection on the Internet Submitted by: Content Overseas Distribution Association Workshop on Protection of Intellectual Property Rights in Digital Content Trade 20-21 April 2021 Specific aspects of copyright and related rights protection on the Internet April 20th, 2021 Content Overseas Distribution Association (CODA) About CODA 1 • Name: Content Overseas Distribution Association (Abbreviation: CODA) http://www.coda-cj.jp • Purpose: CODA was founded to actively promote the international distribution of Japanese content, such as music, films, animation, TV programs and video games, as well as to help all the entities in contents industry make a concerted effort to reduce piracy around the world. • History: August 2002 Founded as a voluntary organization in response to a call by the Ministry of Economy, Trade and Industry (METI) and the Agency for Cultural Affairs (ACA) April 2009 Registered as a general incorporated association About CODA 2 >> Members: (as of April 1, 2021) Corporate members: 32 companies ■Animation 10 companies ■Music 5 companies ■TV programs 8 companies • Aniplex Inc. • Avex Inc. • TOKYO BROADCASTING • ADK Emotions Inc. • FWD Inc. SYSTEM TELEVISION, INC. • Sunrise Inc. • KING RECORD CO., LTD. • TV Asahi Corporation • Shogakukan-Shueisha Productions Co., • PONY CANYON INC. • Nippon Television Network Ltd. • UNIVERSAL MUSIC LLC Corporation • STUDIO GHIBLI INC. • Japan Broadcasting Corporation • Toei Animation Co., Ltd. (NHK) • TMS ENTERTAINMENT CO.,LTD. • Fuji Television Network, Inc. • NIPPON ANIMATION CO., LTD. • YOMIURI TELECASTING • HAPPINET CORPORATION CORPORATION • BANDAI NAMCO Arts Inc. • WOWOW Inc. • TV TOKYO Corporation ■Others 1 companies ■Films 4 companies ■Publishing 4 companies • YOSHIMOTO KOGYO CO.,LTD. -

9781517904029.Pdf

Interpreting Anime This page intentionally left blank Interpreting Anime Christopher Bolton University of Minnesota Press Minneapolis London An earlier version of chapter 1 was previously published as “From Ground Zero to Degree Zero: Akira from Origin to Oblivion,” Mechademia 9 (Minneapolis: University of Minnesota Press, 2014), 295–315. An earlier version of chapter 2 was previously published as “The Mecha’s Blind Spot: Patlabor 2 and the Phenomenology of Anime,” Science Fiction Studies 29, no. 3 (November 2002): 453– 74, and in Robot Ghosts and Wired Dreams: Japanese Science Fictions from Origins to Anime, ed. Christopher Bolton, Istvan Csicsery-Ronay Jr., and Takayuki Tatsumi (Minneapolis: University of Minnesota Press, 2007), 123– 47. An earlier version of chapter 3 was pre- viously published as “From Wooden Cyborgs to Celluloid Souls: Mechanical Bodies in Anime and Japanese Puppet Theater,” positions: east asia cul- tures critique 10, no. 3 (Winter 2002): 729–71. An earlier version of chap- ter 4 was previously published as “Anime Horror and Its Audience: 3x3 Eyes and Vampire Princess Miyu,” in Japanese Horror Cinema, ed. Jay McRoy (Edinburgh: Edinburgh University Press, 2005), 66– 76. An earlier version of chapter 6 was previously published as “The Quick and the Undead: Visual and Political Dynamics in Blood: The Last Vampire,” Mechademia 2 (Minneapolis: University of Minnesota Press, 2007), 125– 42. Copyright 2018 by the Regents of the University of Minnesota All rights reserved. No part of this publication may be reproduced, stored in a retrieval system, or transmitted, in any form or by any means, electronic, mechanical, photocopying, recording, or otherwise, without the prior writ- ten permission of the publisher. -

BANDAI NAMCO Group

BANDAI NAMCO Group INTEGRATED REPORT 2018 The BANDAI NAMCO Group develops entertainment-related products and services in a wide range of fields, including toys, network content, home video games, amusement machines, amusement facilities, and visual and music content. Under the Mid-term Plan, which was launched in April 2018, the Group aims to achieve “CHANGE” to progress to the next stage, with a Mid-term Vision of CHANGE for the NEXT: Empower, Gain Momentum, and Accelerate Evolution. OUR MISSION STATEMENT Dreams, Fun and Inspiration “Dreams, Fun and Inspiration”are the Engine of Happiness. Through our entertainment products and services, BANDAI NAMCO will continue to provide “Dreams, Fun and Inspiration” to people around the world, based on our boundless creativity and enthusiasm. OUR VISION The Leading Innovator in Global Entertainment As an entertainment leader across the ages, BANDAI NAMCO is constantly exploring new areas and heights in entertainment. We aim to be loved by people who have fun and will earn their trust as “the Leading Innovator in Global Entertainment.” CONTENTS 04 THE BANDAI NAMCO Group — 1 Year of Results ( FY2018.3) 06 UNITS — 1 Year of Results ( FY2018.3) 08 THE GROUP’S GREATEST STRENGTH — The IP Axis Strategy 10 MAJOR IP IN GROUP PRODUCTS AND SERVICES 12 BOARD OF DIRECTORS AND AUDIT & SUPERVISORY BOARD MEMBERS 14 OVERVIEW OF THE MIDTERM PLAN 16 PRESIDENT’S MESSAGE 20 MESSAGES FROM THE PRESIDENTS OF UNIT CORE COMPANIES 25 SPECIAL FEATURE: MAIN STRATEGIES IN THE MIDTERM PLAN 40 DISCUSSION AMONG OUTSIDE DIRECTORS 44 CORPORATE GOVERNANCE 51 CSR INITIATIVES 55 FINANCIAL SECTION 95 CORPORATE DATA 96 OVERVIEW OF MAIN GROUP COMPANIES About Integrated Report 2018 In editing this report, we made reference to the International Integrated Reporting IR CSR Framework of the International Integrated Reporting Council ( IIRC). -

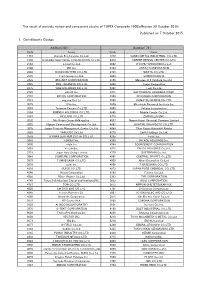

Published on 7 October 2015 1. Constituents Change the Result Of

The result of periodic review and component stocks of TOPIX Composite 1500(effective 30 October 2015) Published on 7 October 2015 1. Constituents Change Addition( 80 ) Deletion( 72 ) Code Issue Code Issue 1712 Daiseki Eco.Solution Co.,Ltd. 1972 SANKO METAL INDUSTRIAL CO.,LTD. 1930 HOKURIKU ELECTRICAL CONSTRUCTION CO.,LTD. 2410 CAREER DESIGN CENTER CO.,LTD. 2183 Linical Co.,Ltd. 2692 ITOCHU-SHOKUHIN Co.,Ltd. 2198 IKK Inc. 2733 ARATA CORPORATION 2266 ROKKO BUTTER CO.,LTD. 2735 WATTS CO.,LTD. 2372 I'rom Group Co.,Ltd. 3004 SHINYEI KAISHA 2428 WELLNET CORPORATION 3159 Maruzen CHI Holdings Co.,Ltd. 2445 SRG TAKAMIYA CO.,LTD. 3204 Toabo Corporation 2475 WDB HOLDINGS CO.,LTD. 3361 Toell Co.,Ltd. 2729 JALUX Inc. 3371 SOFTCREATE HOLDINGS CORP. 2767 FIELDS CORPORATION 3396 FELISSIMO CORPORATION 2931 euglena Co.,Ltd. 3580 KOMATSU SEIREN CO.,LTD. 3079 DVx Inc. 3636 Mitsubishi Research Institute,Inc. 3093 Treasure Factory Co.,LTD. 3639 Voltage Incorporation 3194 KIRINDO HOLDINGS CO.,LTD. 3669 Mobile Create Co.,Ltd. 3197 SKYLARK CO.,LTD 3770 ZAPPALLAS,INC. 3232 Mie Kotsu Group Holdings,Inc. 4007 Nippon Kasei Chemical Company Limited 3252 Nippon Commercial Development Co.,Ltd. 4097 KOATSU GAS KOGYO CO.,LTD. 3276 Japan Property Management Center Co.,Ltd. 4098 Titan Kogyo Kabushiki Kaisha 3385 YAKUODO.Co.,Ltd. 4275 Carlit Holdings Co.,Ltd. 3553 KYOWA LEATHER CLOTH CO.,LTD. 4295 Faith, Inc. 3649 FINDEX Inc. 4326 INTAGE HOLDINGS Inc. 3660 istyle Inc. 4344 SOURCENEXT CORPORATION 3681 V-cube,Inc. 4671 FALCO HOLDINGS Co.,Ltd. 3751 Japan Asia Group Limited 4779 SOFTBRAIN Co.,Ltd. 3844 COMTURE CORPORATION 4801 CENTRAL SPORTS Co.,LTD.