Enrollment Audit Public Community/Junior and Technical College Table of Contents

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

For 2017-2018

GENERAL CATALOG FOR 2017-2018 Angelina County Junior College District (hereinafter: Angelina College) is accredited by the Southern Association of Colleges and Schools Commission on Colleges to award associate degree levels – Associate in Arts, Associate in Science, Associate in Applied Science, and certificates. Contact the Commission on Colleges at 1866 Southern Lane, Decatur, Georgia 30033-4097 or call 404-679-4500 for questions about the accreditation of Angelina College. Accreditation Review Council on Education in Surgical Technology and Surgical Assisting American Association of Collegiate Registrars and Admissions Officers American Medical Technologists American Registry for Diagnostic Medical Sonography American Society of Health System Pharmacists American Society of Phlebotomy Technicians Association of Texas Colleges and Universities Commission on Accreditation of Allied Health Educational Programs Committee on Accreditation for Respiratory Care Committee on Accreditation of Educational Programs for the Emergency Medical Services Professions Department of Transportation Joint Review Committee on Education in Radiologic Technology National Health Career Association National Healthcare Association National Restaurant Association Nurse Aide Competency Evaluation Service Texas Board of Nursing Texas Board of Private Security Texas Commission on Environmental Quality Texas Commission on Fire Protection Texas Commission on Law Enforcement Texas Commission on Private Security Texas Department of State Health Services Texas Department on Aging & Disability Services Texas Education Agency Texas Higher Education Coordinating Board Texas Real Estate Commission Texas State Board of Public Accountancy Texas State Fire Marshals Association Texas Workforce Commission U.S. Department of Health, Education and Welfare Angelina College does not discriminate on the basis of race, religion, color, gender, age, creed, national origin, veteran status, or disabilities, and is an equal opportunity/affirmative action employer. -

Student Achievement Summary 2017-2018

Student Achievement Summary 2017-2018 Laredo College is an institution committed to student success by providing comprehensive educational services that focus on the dynamic requirements and needs of its local, regional, and international community. The College assesses student achievement using a set of Key Performance Indicators (KPI) that are published annually in the institution’s Student Success Report Card. Results are compared to the College’s Peer Group as defined by the Texas Higher Education Coordinating Board, as shown in the Rank column. The status of each KPI is indicated by a color: = Target Met = Opportunity for Improvement = Attention Needed PEER KEY PERFORMANCE INDICATOR RESULT* STATUS GROUP RANK SATISFACTORY ACADEMIC PROGRESS SPRING SPRING SPRING 2016 2017 2018 The percentage of students who maintained a ‘C’ average after their first year at LCC. NA 81.70% 80.10% 77% FALL FALL FALL SUCCESS IN DEVELOPMENTAL COURSES 2013 2014 2015 Mathematics 2nd The percent of underprepared students attempting developmental education who 42.40% 47.90% 54.40% satisfied TSI obligation within 2 years. Reading 7th The percent of underprepared students attempting developmental education who 58.40% 48.10% 55.10% satisfied TSI obligation within 2 years. Writing 8th The percent of underprepared students attempting developmental education who 50.70% 47.40% 48.40% satisfied TSI obligation within 2 years. SUCCESS IN GATEWAY COURSES FALL FALL FALL 2013 2014 2015 Mathematics 3rd The percent of prepared and underprepared students who successfully 42.97% 43.78% 46.54% complete a college-level course in math, reading and writing. Reading 7th The percent of prepared and underprepared students who successfully 55.13% 58.11% 56.47% complete a college-level course in math, reading and writing. -

Institutional Resumes Accountability System Definitions Institution Home Page

Online Resume for Prospective Students, Parents and the Public CISCO COLLEGE Location: Cisco, Northwest Region Medium Accountability Peer Group: Alvin Community College, Angelina College, Brazosport College, Coastal Bend College, College of The Mainland, Grayson County College, Hill College, Kilgore College, Lee College, McLennan Community College, Midland College, Odessa College, Paris Junior College, Southwest Texas Junior College, Temple College, Texarkana College, Texas Southmost College, Trinity Valley Community College, Victoria College, Weatherford College, Wharton County Junior College Degrees Offered: Associate's, Certificate 1, Certificate 2 Institutional Resumes Accountability System Definitions Institution Home Page Enrollment Costs Institution Peer Group Avg. Average Annual Total Academic Costs for Resident Race/Ethnicity Fall 2016 % Total Fall 2016 % Total Undergraduate Student Taking 30 SCH, FY 2017 White 1,990 61.5% 2,498 46.4% Peer Group Hispanic 722 22.3% 1,992 37.0% Type of Cost Institution Average African American 318 9.8% 560 10.4% Asian/Pacific Isl. 78 2.4% 117 2.2% In-district Total Academic Cost $3,810 $2,564 International 37 1.1% 34 .6% Out-of-district Total Academic Cost $4,710 $3,977 Other & Unknown 93 2.9% 183 3.4% Off-campus Room & Board $4,438 $7,204 Total 3,238 100.0% 5,387 100.0% Cost of Books & Supplies $0 $1,591 Cost of Off-campus Transportation $5,776 $4,225 Financial Aid and Personal Expenses Total In-district Cost $14,024 $15,584 Institution Peer Group FY 2015 Percent Ave Amt Percent Avg Amt Total -

College Named Top 10 in Nation 4Grads Celebrate, Tailgate Style 2Foundation Raises $360K for Students

WWW.SANJAC.EDU College named Foundation raises Grads celebrate, 2 Top 10 in nation 2 $360K for students 4 tailgate style SANJAC.EDU HOUSTON CHRONICLE CUSTOM ADVERTISING SECTION SUNDAY, JULY 5, 2020 2 <<< Houston Chronicle Custom Advertising Section | Opportunity News | Sunday | July 5, 2020 sanjac.edu News frOm YOur COllege San Jac 3-peats as critically important to our success,” said transportation support, child care Dr. Brenda Hellyer, San Jacinto College access, and tuition assistance, in Top 10 community Chancellor. “These generous donations addition to the food markets and coat college in the nation enhance our ability to help students in closet resources. According to the the ways they need it most. Some face National Alliance to End Homelessness San Jacinto College was named June 9 an unexpected emergency and need (NAEH), there were an estimated 25,310 as one of 10 finalists for the $1 million immediate help, and others are working homeless individuals in Texas in 2019, 2021 Aspen Prize for Community day in and day out to oVercome ongoing with nearly 1,400 unaccompanied College Excellence, the nation’s signature obstacles like food insecurity and young adults ages 18-24. San Jacinto recognition of high achieVement and homelessness. It’s our mission to help all College’s student population of performance among community colleges. students achieVe their educational goals, nearly 45,000 each year reflects the Photo courtesy of San Jacinto College Awarded eVery two years since 2011, and we are so grateful to the community, statewide demographics of these at-risk the Aspen Prize recognizes institutions our partners, and our employees for populations, and the College continues emergency aid grants through the that achieVe strong student outcomes helping us do that.” its mission to meet the needs of its Federal CARES Act. -

College Recognizes Most Outstanding Employees KC Kickoffin the Plaza

SEPTEMBER 2016 College recognizes most outstanding employees Kilgore College honored its Most Outstanding Employees at opening day ceremonies this year. Each year, KC employees vote for peers who they think are “most outstanding” at what they do. Categories include Executive/Management/ Supervisory; Professional/ CHRIS GORE MARY MARTIN KRISTI POWERS KENYA RAY Technical/Support; Director of Admissions Professional Support Assistant Human Resources Program Director/Instructor, Administrative/Office & Registrar Business, Tech. & Public Services Payroll & Benefits Manager Corrosion Tech Executive/Management/Supervisory Administrative/Office Support Professional/Technical/Support Faculty Support; and Faculty. KC Kickoff was held for the first time in the new Lee Mall/ Mike Miller Plaza Sept. 1. A record turnout of KC students KC Kickoff in the Plaza: and employees attended the event. Photo by Jamie Maldonado/KC Activities begin for reaffirmation of college As the new school year begins, it’s time to kick off activities related to KC’s Southern Association of Colleges and Schools Commission on Colleges (SACSCOC) reaffirmation of accreditation to be voted on in June 2019. A reaffirmation timeline was e-mailed to all employees Aug. 23. The timeline is broken down Four KC instructors awarded by NISOD for excellence into columns for general activities that relate to the Kilgore College is pleased compliance certification and to announce that four KC activities that relate to the instructors are recipients of Quality Enhancement Plan the annual National Institute (QEP). for Staff and Organizational Two important dates are submission of the Compliance Development (NISOD) Certification document in Excellence Award. March 2018 and the on-site Instructors honored RONDA HOWE JEANNE JOHNSON JULIE LEWIS TINA RUSHING committee visit in Fall 2018 with the award are Ronda Chemistry Music Mathematics Psychology (exact dates TBA). -

SOUTH TEXAS COLLEGE BOARD of TRUSTEES REGULAR MEETING Thursday, June 26, 2014 @ 5:30 P.M

SOUTH TEXAS COLLEGE BOARD OF TRUSTEES REGULAR MEETING Thursday, June 26, 2014 @ 5:30 p.m. Ann Richards Administration Building Board Room Pecan Campus, McAllen, Texas 78501 AGENDA “At anytime during the course of this meeting, the Board of Trustees may retire to Executive Session under Texas Government Code 551.071(2) to confer with its legal counsel on any subject matter on this agenda in which the duty of the attorney to the Board of Trustees under the Texas Disciplinary Rules of Professional Conduct of the State Bar of Texas clearly conflicts with Chapter 551 of the Texas Government Code. Further, at anytime during the course of this meeting, the Board of Trustees may retire to Executive Session to deliberate on any subject slated for discussion at this meeting, as may be permitted under one or more of the exceptions to the Open Meetings Act set forth in Title 5, Subtitle A, Chapter 551, Subchapter D of the Texas Government Code. At this meeting, the Board of Trustees may deliberate on and take any action deemed appropriate by the Board of Trustees on the following subjects:” I. Call Meeting to Order II. Determination of Quorum III. Invocation IV. Public Comments V. Presentations ............................................................................................................ 1 - 10 A. Presentation on the JagExpress Expansion and Related Services Proposed by Valley Metro / Lower Rio Grande Valley Development Corporation VI. Consideration and Action on Consent Agenda A. Approval of Minutes 1. May 27, 2014 Regular Board Meeting ........................................................ 11 - 38 B. Approval and Authorization to Accept Grant Award(s) ...................................... 39 - 40 1. The “The Microsoft Excel Training” Contract from the Lower Rio Grande Valley Workforce Development Board 2. -

Success/Retention Activities

Success/Retention Activities Participation Summary Data for All Institutions as of January 2, 2008 Number of Participating Institutions: 87 out of 120 (or 72.5%) Total Funding for Participating Institutions for Academic Year 2006: $21,437,067 Total Funding for Participating Institutions for Academic Year 2007: $27,000,636 Combined Funding for Participating Institutions for Academic Years 2006-2007: $48,437,703 Highest Funded Program in Academic Year 2006: $2,000,000 at University of Houston-Downtown University of Houston-Downtown Highest Funded Program in Academic Year 2007: $1,750,000 at Sam Houston State University Number of Students Served by Participating Institutions for Academic Year 2006: 311,621 Number of Students Served by Participating Institutions for Academic Year 2007: 412,887 Combined Number of Students Served by Participating Institutions for Academic Years 2006-2007: 724,508 Participating Students Funding Institutions Served Academic Support 93 249,907 $16,993,054 Services Access to Faculty and 11 12,405 $1,261,653 Academic Advising Early-Alert Systems 15 43,245 $1,319,576 Extended Student 16 22,395 $1,875,975 Orientation Institution-Wide Diversity 7 25,702 $142,000 Programs/Activities Learner-Centered 12 41,374 $1,360,950 Teaching Qualitative and effective advisement and 20 72,588 $5,664,838 counseling system Student Success Courses 35 59,734 $6,491,587 or Bridge Programs Participating Institutions: Academic support services Alvin Community College Amarillo College Angelina College Angelo State University Brazosport College Cedar Valley College Clarendon College Del Mar College El Paso Community College District Frank Phillips College Hill College Howard College Howard College Lamar State College-Orange Lamar State College-Port Arthur Laredo Community College Midland College Midwestern State University Montgomery College North Lake College Odessa College Paris Junior College Ranger College Sam Houston State University San Antonio College St. -

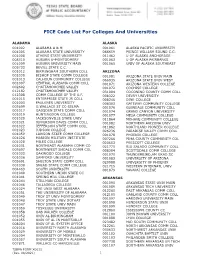

FICE Code List for Colleges and Universities (X0011)

FICE Code List For Colleges And Universities ALABAMA ALASKA 001002 ALABAMA A & M 001061 ALASKA PACIFIC UNIVERSITY 001005 ALABAMA STATE UNIVERSITY 066659 PRINCE WILLIAM SOUND C.C. 001008 ATHENS STATE UNIVERSITY 011462 U OF ALASKA ANCHORAGE 008310 AUBURN U-MONTGOMERY 001063 U OF ALASKA FAIRBANKS 001009 AUBURN UNIVERSITY MAIN 001065 UNIV OF ALASKA SOUTHEAST 005733 BEVILL STATE C.C. 001012 BIRMINGHAM SOUTHERN COLL ARIZONA 001030 BISHOP STATE COMM COLLEGE 001081 ARIZONA STATE UNIV MAIN 001013 CALHOUN COMMUNITY COLLEGE 066935 ARIZONA STATE UNIV WEST 001007 CENTRAL ALABAMA COMM COLL 001071 ARIZONA WESTERN COLLEGE 002602 CHATTAHOOCHEE VALLEY 001072 COCHISE COLLEGE 012182 CHATTAHOOCHEE VALLEY 031004 COCONINO COUNTY COMM COLL 012308 COMM COLLEGE OF THE A.F. 008322 DEVRY UNIVERSITY 001015 ENTERPRISE STATE JR COLL 008246 DINE COLLEGE 001003 FAULKNER UNIVERSITY 008303 GATEWAY COMMUNITY COLLEGE 005699 G.WALLACE ST CC-SELMA 001076 GLENDALE COMMUNITY COLL 001017 GADSDEN STATE COMM COLL 001074 GRAND CANYON UNIVERSITY 001019 HUNTINGDON COLLEGE 001077 MESA COMMUNITY COLLEGE 001020 JACKSONVILLE STATE UNIV 011864 MOHAVE COMMUNITY COLLEGE 001021 JEFFERSON DAVIS COMM COLL 001082 NORTHERN ARIZONA UNIV 001022 JEFFERSON STATE COMM COLL 011862 NORTHLAND PIONEER COLLEGE 001023 JUDSON COLLEGE 026236 PARADISE VALLEY COMM COLL 001059 LAWSON STATE COMM COLLEGE 001078 PHOENIX COLLEGE 001026 MARION MILITARY INSTITUTE 007266 PIMA COUNTY COMMUNITY COL 001028 MILES COLLEGE 020653 PRESCOTT COLLEGE 001031 NORTHEAST ALABAMA COMM CO 021775 RIO SALADO COMMUNITY COLL 005697 NORTHWEST -

Wharton County Junior College

Wharton County Junior College PIONEER BASEBALL 2017 SCHEDULE DATE DAY OPPONENT LOCATION TIME GAME January 31 Tuesday Coastal Bend College Wharton 2:00 7/7 February 4 Saturday Baton Rouge Community College Baton Rouge, LA 12:00 9 4 Saturday Weatherford College Baton Rouge, LA 3:00 9 TOURNAMENT OF CHAMPIONS 10 Friday Howard College Beaumont 6:00 9 Lamar University 11 Saturday New Mexico Junior College Sugar Land 9:00 9 Constellation Field 11 Saturday Grayson College Huntsville 7:00 9 Sam Houston State University 12 Sunday Weatherford College Houston 4:00 9 San Jacinto College 14 Tuesday Coastal Bend College Beeville 2:00 9 18 Saturday Angelina College Wharton 1:00 7/7 23 Thursday Blinn College Wharton 6:00 9 25 Saturday Blinn College Brenham 3:00 7/9 27 Monday McLennan College Waco 2:00 9 March 2 Thursday San Jacinto College Houston 6:00 9 4 Saturday San Jacinto College Wharton 2:00 7/9 7 Tuesday St. Edward’s University Austin 1:30 9 10 Friday Laredo College Laredo 5:00 9 11 Saturday Laredo College Laredo 12:00 7/9 13 Monday Angelina College Lufkin 5:00 9 16 Thursday Alvin College Alvin 1:00 9 18 Saturday Alvin College Wharton 2:00 7/9 20 Monday St. Edward’s University Wharton 5:00 9 23 Thursday Galveston College Wharton 6:00 9 25 Saturday Galveston College Galveston 3:00 7/9 27 Monday Baton Rouge Community College Wharton 3:00 9 30 Thursday Blinn College Brenham 4:00 7/9 April 1 Saturday Blinn College Wharton 2:00 7/9 3 Monday McLennan College Wharton 3:00 9 6 Thursday San Jacinto College Wharton 3:00 7/9 8 Saturday San Jacinto College -

Four Finalists Named for President's Position

NOVEMBER 2015 Four finalists named for president’s position After reviewing a large pool of qualified candidates, the presidential search committee has named four finalists for the president’s job at Kilgore College. The search committee is comprised of Board Dr. Brenda Kays Dr. Lynn Moore Dr. Mark Smith Dr. Kyle Wagner Secretary Karol Current position: Current position: Current position: Current position: VP of Pruett; Board VP President, Stanly President, Southeast Vice President of Instruction & Economic James Walker; trustee Community College, Kentucky Community & Educational Services at Development, Coastal Joe Carrington and North Carolina Technical College Temple College Bend College, Texas college employees D’Wayne Shaw and Education: Education: Education: Education: Ed.D. from University of Ph.D. from The Univ. of Ph.D. from Capella Ph.D. from Capella Brandon Walker. North Texas in Denton Texas at Austin There will be two University University open forums on each Interview & Interview & Interview & Interview & interview day where Public Forum Date: Public Forum Date: Public Forum Date: Public Forum Date: the public will have Thursday, Nov. 12 Monday, Nov. 16 Tuesday, Nov. 10 Thursday, Nov. 5 an opportunity to ask 1:15-2pm, 2:15-3pm 1:15-2pm, 2:15-3pm 1:15-2pm, 2:15-3pm 1:15-2pm, 2:15-3pm questions. Administration Bldg. Administration Bldg. Administration Bldg. Administration Bldg. Rangers will play for SWJCFC Spradlin dies at age 85 Championship Saturday in Corsicana Kilgore College’s longest- serving board member, R.E. The Kilgore College football “Sonny” Spradlin Jr., passed away team picked off five Trinity Saturday, Oct. 17. -

Joanna Clark Laws

JOANNA CLARK LAWS TEACHING EXPERIENCE Ranger College, Ranger TX Instructor of English – January 2021- present Western Texas College, Snyder, TX Instructor of English – August 2019 – December 2020 Abilene Christian University, Abilene, TX Adjunct Instructor of English – August 2015- May 2019 Cisco College, Cisco, TX Professor of English – Tenure Awarded Spring, 2009 – August 2004 to July 2012 Tarleton State University, Stephenville, TX Adjunct Faculty - Taught English 1113 (Freshman Composition) (Fall 2003) Graduate Teaching Assistant (Academic Year 1999-2000) Graduate Assistant of English (Academic Year 1998-1999) EDUCATION Sam Houston State University, Huntsville, TX Master of Arts in History – program in progress Old Dominion University, Norfolk, VA Additional graduate study Texas Tech University, Lubbock, TX Certified Public Manager Program – completed June 6, 2015 University of Texas at Dallas, Richardson, TX Additional graduate study Tarleton State University, Stephenville, TX Master of Arts in English - May 19, 2000 Directed Research Area: Holocaust & Youth Creativity Supervisor: Dr. Marilyn Robitaille Tarleton State University, Stephenville, TX Bachelor of Arts in English - August 7, 1998 - Magna cum laude Cisco Junior College, Cisco, TX Associate of Arts - May 1994 - with highest honors ADMINISTRATIVE EXPERIENCE City of Abilene, Abilene, TX Employee Development Manager – June 17, 2013 to August 9, 2019 Odessa College, Odessa, TX Dean of Arts & Sciences – August 1, 2012 to June 6, 2013 Cisco College, Cisco, TX Director of Developmental Education & QEP – December 2011 to July 25, 2012 Director of Assessment & Developmental Studies – May 1, 2010 to December 2011 Chair, Language & Communication Division – November 1, 2006 to May 1, 2010 PUBLICATIONS Forthcoming – “Anne E. Davis Roark.” We Did It: Biographical Studies of African American Women in Texas History. -

List of State Agencies and Higher Education Institutions

List of State Agencies and Institutions of Higher Education (List may not be all inclusive) Abilene State Supported Living Center Civil Commitment Office, Texas Fire Protection, Commission on Accountancy, Board of Public Clarendon College Forest Service, Texas Administrative Hearings, Office of Coastal Bend College Frank Phillips College Affordable Housing Corporation College of the Mainland Funeral Service Commission Aging and Disability Services, Dept. of Collin County Community College Galveston College Agriculture, Department of Competitive Government, Council on Geoscientists, Board of Professional AgriLife Extension Service, Texas Comptroller of Public Accounts Governor, Office of the AgriLife Research, Texas Consumer Credit Commissioner, Office of Grayson County College Alamo Community College District Corpus Christi State Supported Groundwater Protection Committee Alcoholic Beverage Commission County and District Retirement System Guadalupe-Blanco River Authority Alvin Community College Court Administration, Office of Gulf Coast Waste Disposal Authority Amarillo College Credit Union Department Headwaters Groundwater Conservation Anatomical Board Criminal Appeals, Court of Health and Human Services Commission Angelina and Neches River Authority Criminal Justice, Department of Health Professions Council Angelina College Dallas County Community College Health Services, Department of State Angelo State University Deaf, School for the High Plains Underground Water Conserv. Animal Health Commission Del Mar College Higher Education Coordinating