Audit Report on the Accounts of Assistant Director Local Government, Election & Rural Development Department and Selected Union Councils

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Water and Power Resources of West Pakistan

Water and Power Resources PAKISTAN "& of WEST I1158 Public Disclosure Authorized A Study in Sector Planning g' c - J) A N D e XJ ~~~~~~~ S >>)~~~~~TM RHELA AS H M I R Public Disclosure Authorized VISLAMABA > 2 t \ . Public Disclosure Authorized C ,,'_ o / z 'N ~~VOLUME g,_ -THE MAIN REPORT \ < ,pre~lppared by a World Bank Study Group Headed by X f .,/ ~~~PIETER LIEFTINCK t i '_z ~~~A. ROBERT SADOVE Public Disclosure Authorized tt I ~~~~~~~~~Deputy Hlead S n THOMAS-4 C.CREYKE ~~~~< < /r~~~~~~~~~~~trigation and Agr-icultut-e WATER AND POWER RESOURCES OF WEST PAKISTAN A Study in Sector Planning Volume I: The Main Report $10.00 Volume II: The Development of Irrigation and Agriculture $12.50 Volume III: Background and Methodology $ 12.50 $28.50 the set Prepared by a World Bank Study Group Headed by Pieter Lieftinck; A. Robert Sadove, Deputy Head; Thomas C. Creyke, Irrigation and Agriculture. Without doubt, the greatest single co- ordinated development operation in which the World Bank has been involved is the massive program for development of the Indus Basin. This pioneering study is an integral part of that project and is unique both in its conceptualization and its compre- hensiveness. It demonstrates the feasibility of a new and more rigorous approach to resource planning and development and will serve as an indispensible model for engi- neers, economists, and planners for years to come. Focal points of the Study are the Indus River, which runs the length of west Paki- stan, several of its tributaries, and a huge natural underground reservoir. -

Pakistan, Country Information

Pakistan, Country Information PAKISTAN ASSESSMENT April 2003 Country Information and Policy Unit I SCOPE OF DOCUMENT II GEOGRAPHY III ECONOMY IV HISTORY V STATE STRUCTURES VI HUMAN RIGHTS VIA. HUMAN RIGHTS ISSUES VIB. HUMAN RIGHTS - SPECIFIC GROUPS VIC. HUMAN RIGHTS - OTHER ISSUES ANNEX A: CHRONOLOGY OF MAJOR EVENTS ANNEX B: POLITICAL ORGANISATIONS AND OTHER GROUPS ANNEX C: PROMINENT PEOPLE ANNEX D: REFERENCES TO SOURCE MATERIAL 1. SCOPE OF DOCUMENT 1.1 This assessment has been produced by the Country Information and Policy Unit, Immigration and Nationality Directorate, Home Office, from information obtained from a wide variety of recognised sources. The document does not contain any Home Office opinion or policy. 1.2 The assessment has been prepared for background purposes for those involved in the asylum / human rights determination process. The information it contains is not exhaustive. It concentrates on the issues most commonly raised in asylum / human rights claims made in the United Kingdom. 1.3 The assessment is sourced throughout. It is intended to be used by caseworkers as a signpost to the source material, which has been made available to them. The vast majority of the source material is readily available in the public domain. These sources have been checked for currency, and as far as can be ascertained, remained relevant and up to date at the time the document was issued. 1.4 It is intended to revise the assessment on a six-monthly basis while the country remains within the top 35 asylum-seeker producing countries in the United Kingdom. 2. GEOGRAPHY file:///V|/vll/country/uk_cntry_assess/apr2003/0403_Pakistan.htm[10/21/2014 9:56:32 AM] Pakistan, Country Information General 2.1 The Islamic Republic of Pakistan lies in southern Asia, bordered by India to the east and Afghanistan and Iran to the west. -

Peshawar High Court, Peshawar Judicial Department Judgment

JUDGMENT SHEET PESHAWAR HIGH COURT, PESHAWAR JUDICIAL DEPARTMENT C.R No.289-P/2016 JUDGMENT Date of hearing…………30.10.2018....…………….. Petitioner: (Provincial Housing Authority through its Director General): By Mr. Amir Javed, Advocate. Respondent: No.1, Wazir Khan, by Mr. Tariq Khan Hoti, Advocate. Respondent No.4, Maqsad Ali, Girdawar Circle, Kohat in person. Respondent No.5, Farid Khan, Patwari Halqa Jarma, Kohat in person. **** QALANDAR ALI KHAN, J.- This civil revision by Provincial Housing Authority through its Director General (petitioner) is directed against judgments/orders/decrees dated 24.02.2016 by Additional District Judge-IV, Kohat, and also that of the Civil Judge-XI, Kohat, dated 06.09.2014, whereby decree of the latter Court dated 06.09.2014 was maintained by the former/appellate Court; and appeal of the petitioner dismissed vide impugned judgment and decree dated 24.02.2016. 2. The background, forming basis of the instant revision petition, briefly stated, is that originally the Provincial Government was recorded as owner; and Deputy Commissioner, Kohat, in Possession of the 2 land measuring 219 Kanal in Khasra No.1/1122/71 of village Jarma, according to the available record of owners from the year 2003/04. A total of 300 Kanal land, including the said land, was transferred from the Provincial Government to the Prime Minister National Housing Scheme Authority, vide Mutation No.1033 attested on 22.12.1999; but re-transferred to the Provincial Government from the Pakistan Housing Authority, Works Division, Kohat, vide Mutation No.1062 attested on 28.07.2000. The entire land measuring 300 Kanal , including the land in question measuring 219 Kanal (Banjar Jadeed) was transferred by the Provincial Government to the Provincial Housing Authority) Kohat i.e. -

Weekly Epidemiological Bulletin Disease Early Warning System and Response in Pakistan

Weekly Bulletin Epidemiological Disease early warning system and response in Pakistan Volume 2, Issue 30, Monday 1 August, 2011 Highlights Priority diseases under surveillance Epidemiological week no. 30 (22 - 28 July, 2011) in DEWS Acute Flaccid Paralysis (AFP) • 88 districts and 3 agencies provided surveillance data to the DEWS this week Acute Jaundice Syndrome (AJS) from 3,092 health facilities. Acute Respiratory Infections (Upper and Lower) (ARI) • A total of 1,010,892 consultations were reported through DEWS of which 17% were acute respiratory infections (ARI), 12% skin disease, 10% acute diar- Acute Watery Diarrhoea (AWD)/ Suspected Cholera rhoea, and 6% suspected Malaria. Acute Bloody Diarrhoea (BD) • A total of 131 alerts with 20 outbreaks were reported in week-30, 2011: Alto- Other Acute Diarrhoeas (AD) gether 50 alerts were for AWD; 38 for Measles; Eight for Neonatal tetanus Suspected Viral Hemorrhagic and Tetanus; Seven for Pertussis; Four for Leishmaniasis; Three for Malaria; Fever (VHF) Two for Acute jaundice syndrome; One for Bloody diarrhoea, and 18 were Suspected Malaria (Mal) for other suspected diseases. Suspected Measles (MS) Suspected Meningitis (MG) • National Polio Eradication Initiative reported no new confirmed polio case this week. Total 60 (59=type1, and 1=type3) confirmed polio cases have been Others reported in 2011 from 25 districts. Figure‐1: Three years trend of Acute diarrhoea in Pakistan (2009, 2010, and 2011) 20 2009 2010 2011 16 12 Percentage 8 4 0 1 4 7 10 13 16 19 22 25 28 31 34 37 40 43 46 49 52 Epi‐week Disease Wk-23 Wk-24 Wk-25 Wk-26 Wk-27 Wk-28 Wk-29 Wk-30 Other Acute Diarrhoea (Not Watery) 100,753 (10%) 102,217 (10%) 103,978 (10%) 107,924 (10%) 100,320 (10%) 104,413 (10%) 107,861 (10%) 103,341 (10%) Total consultation 1,009,254 1,028,090 1,019,724 1,087,368 994,345 1,025,647 1,034,504 1,010,892 Since July 29, 2010, approximately 38,413,010 patient consultations have been reported to the DEWS from the five provinces and three agencies and state of AJK. -

A Comparative Study of Directly Selected, In-Service Promoted and Online Selected Subject Specialists Regarding Teaching Effectiveness in Kohat Division, Pakistan

Journal of Education and Practice www.iiste.org ISSN 2222-1735 (Paper) ISSN 2222-288X (Online) Vol.6, No.10, 2015 A Comparative Study of Directly Selected, In-Service Promoted and Online Selected Subject Specialists Regarding Teaching Effectiveness in Kohat Division, Pakistan Qaiser Suleman PhD (Education) Scholar, Institute of Education & Research, Kohat University of Science & Technology Kohat, Khyber Pakhtunkhwa, (Pakistan) Email: [email protected] Rizwana Gul M.Phil (Education) Scholar, Institute of Education & Research, Kohat University of Science & Technology Kohat, Khyber Pakhtunkhwa, (Pakistan) Abstract The main objective of the study was to compare the teaching effectiveness of directly selected, in-service promoted and online selected subject specialists teaching at higher secondary school level in Kohat Division, Pakistan. The target population of the study was the higher secondary school students in Kohat Division, Pakistan. A sample of 600 students randomly selected from 10 out of 20 higher secondary schools in Kohat Division was used in this study. The design of this research study was survey. A self-developed structured questionnaire was used a research instrument for data collection. Statistical tools i.e., mean, standard deviation, ANOVA and Post-hoc t-tests were used. After statistical analysis, it was concluded that the teaching performance of the directly selected subject specialists was highly appreciable and excellent. On the other hand, teaching performance of in-service promoted subject specialists was found satisfactory while teaching performance of online selected subject specialists was poor and unsatisfactory. Based on findings, it was recommended that at least 75% of the total subject specialists should be recruited through Khyber Pakhtunkhwa Public Service Commission only. -

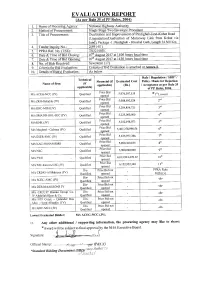

EVALUATION REPORT (As Ner Llule 35 of Pl' Rules.2004)

EVALUATION REPORT (As ner llule 35 of Pl' Rules.2004) l. Nameof ProcuringAgency: NationalHighway Authority 2. Methodof Pfocurement: SinqleStage Two EnvelopeProcedure 3, Titleof Procurement: Dualizationand Improvementof Pindigheb-Jand-KohatRoad qUpgradalioniDLralization of Motorway Link frorn Kohatvia Jand).Package -l: Pindigheb- Khushal Garh, Length 34.560 Km 4. Tendellnquiry No.: 21491-01) 5. PPRARef. No. (TSE): TS3?1403E 6. Date& Timeof Bid Closing: 07"'Ausust2017 at 1400hours local time 1. Date& Tirneof Bid Opening: 07'nAuetst 2017 at 1430hours localtime 8. No. of BidsReceived: Seventeen(17) Criteriafor Bid Evaluation: Cliteria olBid Evaluationis attachedat Annex-L 10. Detailsof Bid(s) Evalualion: As below Rule / Regulation/ SBD* / Tcchllical Financial (if Evaluated Cost Policy / Basisfor Rejection Name of firm (if rpplicrble) (Rs.) / Acceptancers per Rule35 applicable) of PP Rules,2004. PriceBid ACEC.NCC(JV) 5,076,307,t35 * 1" Lowest M/s Qualilied opened t'jriceBid M/s ZKlS-ReLiable(JV) 5,088,602,524 2u'r Qualifiecl oDened PficeBid MisKRC-MIM (JV) 5,204,854,721 3,.I Qudified opened PdceBid M/sSMADB-l ItlL-SEC (JV) 5,225,000,000 Qualified opencd PriceBid KNK (JV) 5,352,t98,013 5'l' M/s Qualifled oDencd PriceBid Calsons(JV) 5,407,378,998.56 6'h IVl/sMaqbool- Qualilied ooened PriceBicl (JV) 5,6'7 5,977 ,386 1'1' M/sESER-SN4C Qualified opened PficaBid M/s KAC-HASAS-RMS 5,890,.r00,635 g'h Qualified oDened PriceBid g'r' NLC 5,900,000,000 M/s QuaLifled oDgned PrioeBid 6,013,944,478.12 l0'r' Vl/sl-WO Qurlilied opcned PliceBid NICI-l(afcon-UJC(JV) 6,ts2,952,340 I l" M/s Qualilied opcncd Dis- PriceBid not PPRARule M/sCR20C-Al Mahreeu (JV) Qualified opened 36(b)(v) Dis- PriceBid not -do- (JV) ]vl/sSCDC-AMC Oualilied opened Dis- PliceBid not -do- JV M/s DES-MAAKSONS Oualilied opencd MA CRCCITBurcau Group Co PriceBid not -do- .lVAbdulLah Khan & Co. -

Islamist Militancy in the Pakistan-Afghanistan Border Region and U.S. Policy

= 81&2.89= .1.9&3(>=.3=9-*=&0.89&38 +,-&3.89&3=47)*7=*,.43=&3)=__=41.(>= _=1&3=74389&)9= 5*(.&1.89=.3=4:9-=8.&3=++&.78= *33*9-=&9?2&3= 5*(.&1.89=.3=.))1*=&89*73=++&.78= 4;*2'*7=,+`=,**2= 43,7*88.43&1= *8*&7(-=*7;.(*= 18/1**= <<<_(78_,4;= -.10-= =*5479=+47=43,7*88 Prepared for Members and Committees of Congress 81&2.89= .1.9&3(>=.3=9-*=&0.89&38+,-&3.89&3=47)*7=*,.43=&3)=__=41.(>= = :22&7>= Increasing militant activity in western Pakistan poses three key national security threats: an increased potential for major attacks against the United States itself; a growing threat to Pakistani stability; and a hindrance of U.S. efforts to stabilize Afghanistan. This report will be updated as events warrant. A U.S.-Pakistan relationship marked by periods of both cooperation and discord was transformed by the September 2001 terrorist attacks on the United States and the ensuing enlistment of Pakistan as a key ally in U.S.-led counterterrorism efforts. Top U.S. officials have praised Pakistan for its ongoing cooperation, although long-held doubts exist about Islamabad’s commitment to some core U.S. interests. Pakistan is identified as a base for terrorist groups and their supporters operating in Kashmir, India, and Afghanistan. Since 2003, Pakistan’s army has conducted unprecedented and largely ineffectual counterterrorism operations in the country’s Federally Administered Tribal Areas (FATA) bordering Afghanistan, where Al Qaeda operatives and pro-Taliban insurgents are said to enjoy “safe haven.” Militant groups have only grown stronger and more aggressive in 2008. -

Pakistan National Nutrition Cluster Preparedness and Response Plan

National Nutrition Cluster 3 July 2013 Pakistan National Nutrition Cluster Preparedness and Response Plan The National Nutrition Cluster Preparedness and Response Plan is a common framework to guide the actions of all partners in the nutrition sector in the event of a disaster. It does not replace the need for planning by individual agencies in relation to their mandate and responsibilities within clusters, but provides focus and coherence to the various levels of planning that are required to respond effectively. It is envisioned that the Preparedness and Response Plan is a flexible and dynamic document that will be updated based on lessons learnt in future emergency responses. Each Provincial Nutrition Cluster will develop a Provincial Nutrition Cluster Preparedness and Response Plan, in cooperation with the Provincial Disaster Management Authority (PDMA) and the Department of Health (DoH). The Provincial Plans are stand-alone documents, however are linked and consistent with the National Plan. 1. Background The 2011 Pakistan National Nutrition Survey confirmed that Pakistan’s population still suffers from high rates of malnutrition and that the situation has not improved for several decades. Two out of every five (44 percent) of children under five are stunted, 32 percent are underweight and 15 percent suffer from acute malnutrition.1 Maternal malnutrition is also a significant problem; 15 percent of women of reproductive age have chronic energy deficiency. Women and children in Pakistan also suffer from some of the world’s highest levels of vitamin and mineral deficiencies. The malnutrition rates are very high by global standards and are much higher than Pakistan’s level of economic development should warrant. -

Weekly Epidemiological Bulletin Disease Early Warning System and Response in Pakistan

Weekly Bulletin Epidemiological Disease early warning system and response in Pakistan Volume 3, Issue 15, Wednesday 18 April 2012 Highlights Priority diseases under surveillance Epidemiological week no. 15 (8 to 14 April 2012) in DEWS Acute (Upper) Respiratory Infection • In week 15, 2012, total 82 districts including 3 agencies provided surveillance data to the Pneumonia DEWS on weekly basis from around 2,010 health facilities. Data from mobile teams is reported Suspected Diphtheria through sponsoring BHU or RHC. Suspected Pertussis Acute Watery Diarrhoea Bloody diarrhoea • A total of 684,278 consultations were reported through DEWS of which 19% were acute Other Acute Diarrhoea respiratory infections (ARI); 8% were acute diarrhoea; 4% were suspected malaria; while 4% were Suspected Enteric/Typhoid Fever Skin disease. Suspected Malaria Suspected Meningitis Suspected Dengue fever • A total of 247 alerts reported while 27 outbreaks were identified in week 15, 2012: Alto‐ Suspected Viral Hemorrhagic Fever gether 142 alerts for Measles; 30 for Leishmaniasis; 16 for NNT and Tetanus; 12 for Typhoid; 11 Pyrexia of Unknown Origin for Pertussis; 9 for acute diarrhoea; 7 for Scabies; 5 for ARI; 4 for Acute jaundice syndrome; 3 for Suspected Measles Suspected Acute Viral Hepatitis AWD; 2 each for Bloody diarrhoea and Diphtheria; while 1 each for CCHF, HF, Food poisoning and Chronic Viral Hepatitis Chicken Pox. Neonatal Tetanus Acute Flaccid Paralysis • In this week no new polio cases was reported. As of 16 April 2012, the total number of polio Scabies Cutaneous Leishmaniasis cases confirmed by the laboratory is 15 from 10 districts/towns/tribal agencies and areas. -

Part-I: Post Code Directory of Delivery Post Offices

PART-I POST CODE DIRECTORY OF DELIVERY POST OFFICES POST CODE OF NAME OF DELIVERY POST OFFICE POST CODE ACCOUNT OFFICE PROVINCE ATTACHED BRANCH OFFICES ABAZAI 24550 Charsadda GPO Khyber Pakhtunkhwa 24551 ABBA KHEL 28440 Lakki Marwat GPO Khyber Pakhtunkhwa 28441 ABBAS PUR 12200 Rawalakot GPO Azad Kashmir 12201 ABBOTTABAD GPO 22010 Abbottabad GPO Khyber Pakhtunkhwa 22011 ABBOTTABAD PUBLIC SCHOOL 22030 Abbottabad GPO Khyber Pakhtunkhwa 22031 ABDUL GHAFOOR LEHRI 80820 Sibi GPO Balochistan 80821 ABDUL HAKIM 58180 Khanewal GPO Punjab 58181 ACHORI 16320 Skardu GPO Gilgit Baltistan 16321 ADAMJEE PAPER BOARD MILLS NOWSHERA 24170 Nowshera GPO Khyber Pakhtunkhwa 24171 ADDA GAMBEER 57460 Sahiwal GPO Punjab 57461 ADDA MIR ABBAS 28300 Bannu GPO Khyber Pakhtunkhwa 28301 ADHI KOT 41260 Khushab GPO Punjab 41261 ADHIAN 39060 Qila Sheikhupura GPO Punjab 39061 ADIL PUR 65080 Sukkur GPO Sindh 65081 ADOWAL 50730 Gujrat GPO Punjab 50731 ADRANA 49304 Jhelum GPO Punjab 49305 AFZAL PUR 10360 Mirpur GPO Azad Kashmir 10361 AGRA 66074 Khairpur GPO Sindh 66075 AGRICULTUR INSTITUTE NAWABSHAH 67230 Nawabshah GPO Sindh 67231 AHAMED PUR SIAL 35090 Jhang GPO Punjab 35091 AHATA FAROOQIA 47066 Wah Cantt. GPO Punjab 47067 AHDI 47750 Gujar Khan GPO Punjab 47751 AHMAD NAGAR 52070 Gujranwala GPO Punjab 52071 AHMAD PUR EAST 63350 Bahawalpur GPO Punjab 63351 AHMADOON 96100 Quetta GPO Balochistan 96101 AHMADPUR LAMA 64380 Rahimyar Khan GPO Punjab 64381 AHMED PUR 66040 Khairpur GPO Sindh 66041 AHMED PUR 40120 Sargodha GPO Punjab 40121 AHMEDWAL 95150 Quetta GPO Balochistan 95151 -

DHIS Khyber Pakhtunkhwa Rapid Assessment 2013.Pdf

Rapid Assessment of District Health Information System 2013 2 Rapid Assessment of District Health Information System 2013 Table of Contents Acknowledgement ........................................................................................................................................ 6 Survey Team ................................................................................................................................................. 8 Abbreviations ................................................................................................................................................ 9 1 Introduction and background .............................................................................................................. 10 1.1 Data and Management Information System (MIS) ..................................................................... 10 1.2 Background ................................................................................................................................. 10 1.3 Gaps of HMIS ............................................................................................................................. 11 1.4 District Health Information System (DHIS) ............................................................................... 11 1.5 Role of DHIS in Khyber Pakhtunkhwa ....................................................................................... 11 1.6 Comparison between HMIS and DHIS ...................................................................................... -

Government of Khyber Pakhtunkhwa

GOVERNMENT OF KHYBER PAKHTUNKHWA COMMUNICATION AND WORK DEPARTMENT TENDER NOTICE (Single stage two envelope procedure) C&W Department (C&W Division Kohat) Government of Khyber Pakhtunkhwa invites electronic Bids from the eligible firms/bidders in accordance with KPPRA Procurement rules 2014 on single stage two envelope procedure for the following works. S.N Name of work. Required Estimated Bid security Period of Last date of Date of Date of category Cost i/c Stamp Completion submission opening of opening of of PEC & duty and time. Technical Financial relevant Bid. Bid. codes/ enlistmen t category ADP No. 1703/200248 (2020- 21) Construction of 1. Technically & Economically Feasible 60-KMs Roads in Kohat Division. S.H: Construction/ Improvement/ 21.12.2020 On the i. Widening of Lachi Dartapi C-5/PK-5 46.860 0.956 (M) As per at 12.00 same day (M) work order Hours & time. Road (3.3-KM) PK-81 District Kohat. Construction of Black Topped ii. Road from Fazal Abad to C-6/PK-6 21.345 0.446 -do- -do- -do- Momin Abad UC Jarma (1.76- (M) (M) KM) PK-81 District Kohat. Date of Construction/ Improvement/ opening of Widening of Black Topped financial C-6/PK-6 bid will be iii. Road from Speena Bangla to 24.581 0.511 -do- -do- -do- (M) (M) announced Haji Dawood Khan Koroona after the (2-KM) PK-81 District Kohat. approval Construction of Black Topped of iv. C-5/PK-5 25.076 0.502 -do- -do- -do- technical Road from Highway to Surgul bid from (M) (M) (2-KM) PK-81 District Kohat.