Economic Bulletin Economic Bulletin June 2007

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Ftese Per Oferte

Invitation to quote INVITATION TO QUOTE Dear Sir/Madam, 1. You are invited to present your price quotation(s) for Property Insurance services. Please see attached Annex A “Financial Quotation”. Annex B “List of Tirana Bank Branches and ATM Networks”. Annex C “List of Tirana Bank Properties”. 2. You can provide to us an estimation cost for the mentioned services which will be subject of a separate review procedure and signature of the respective contract by parties included, for the best offers. Based on the “Invitation to Quote” you should present your offer, after you have read carefully each articles specified, as parts of your assessment. 3. Your quotation(s) should be addressed in a closed envelope, and submitted to: Procurement Unit Tirana Bank, Head Office Rr. "Ibrahim Rugova", Envelope should be superscribed with “Quotation for Tender” 4. THE DEADLINE The deadline for receipt your quotation (s) by the Purchaser at the address indicated above is: 24.01.2020 -12:00 a.m. 5. TECHNICAL SPECIFICATIONS - Your offer should include: a- Financial Offer (Price) b- Technical Offer c- Legal documentations - Contract duration will be for 1 year -Deductibles: 500,000All 6. PRICE You should deliver a financial quotation for: Your are requested to give your financial offer as described in Annex A. Price (% per Sum Insured ) should be VAT and every other taxes or expenses included. - 1 - Invitation to quote 7. Technical Offer Your offer should Include: a- Details on the reinsurance agreement i.e.: -reinsurance company, -minimum amount reinsured, -duration of the reinsurance agreement, - risk coverage of the reinsurance agreement, - Premium Return Policy (Policy Cancellations and Return Premiums/refund of premiums paid), in cases of cancelation of property insurance. -

Databaze E Burimeve Turistike – Qarku Fier

DATABAZE E BURIMEVE TURISTIKE - QARKU FIER NJ. Nr. EMËRTIMI STATUSI KATEGORIA NËNKATEGORIA FSHATI BASHKIA QARKU ADMINISTRATIVE Monument kulture i 1 KALAJA E MARGËLLICIT Turizmi i Kulturës Historik/Arkeologjik Margëlliç Patos Patos Fier kategorise I Monument kulture i 2 RRËNOJAT E KLOSIT Turizmi i Kulturës Historik/Arkeologjik Klos Hekal Mallakastër Fier kategorise I Monument kulture i 3 KALAJA E CFIRIT Turizmi i Kulturës Historik/Arkeologjik Cfir Hekal Mallakastër Fier kategorise I Monument kulture i 4 VENDBANIMI PREHISTORIK Turizmi i Kulturës Historik/Arkeologjik Cakran Cakran Fier Fier kategorise I Monument kulture i 5 QYTETI ILIR I BYLISIT Turizmi i Kulturës Historik/Arkeologjik Hekal Hekal Mallakastër Fier kategorise I Monument kulture i 6 QYTETI ANTIK I APOLLONISË Turizmi i Kulturës Historik/Arkeologjik Pojan Dërmenas Fier Fier kategorise I KALAJA E QYTEZA E Monument kulture i 7 Turizmi i Kulturës Historik/Arkeologjik Cakran Cakran Fier Fier CAKRANIT kategorise I Monument kulture i 8 QYTEZA E GURZEZES Turizmi i Kulturës Historik/Arkeologjik Cakran Cakran Fier Fier kategorise I Monument kulture i 9 QYTEZA E BABUNJËS Turizmi i Kulturës Historik/Arkeologjik Babunjë Gradishtë Divjakë Fier kategorise I Monument kulture i 10 VENDBANIMI I LASHTË Turizmi i Kulturës Historik/Arkeologjik Bishçukë Divjakë Divjakë Fier kategorise I Monument kulture i 11 NEKROPOLI Turizmi i Kulturës Historik/Arkeologjik Kryegjatë Dërmenas Fier Fier kategorise I VARREZAT ILIRE NË BAKAJ Monument kulture i 12 Turizmi i Kulturës Historik/Arkeologjik Aranitas Aranitës -

Cultural Tourism Goes Virtual: Audience Development in Southeast European Countries

CULTURAL TOURISM GOES VIRTUAL: AUDIENCE DEVELOPMENT IN SOUTHEAST EUROPEAN COUNTRIES 1 ddioio FFOREWORD.inddOREWORD.indd 1 44/7/09/7/09 11:32:47:32:47 PPMM This book has been published with the fi nancial support of the UNESCO Offi ce in Venice – UNESCO Regional Bureau for Science and Culture in Europe, City of Zagreb – City Offi ce for Education, Culture and Sports and Ministry of Science, Education and Sports The designations employed and the presentation of the material throughout this publication do not imply the expressing of any opinion whatsoever on the part of the UNESCO Secretariat concerning the legal status of any country or territory, city or area or of its authorities, the delimitations of its frontiers or boundaries. The authors are responsible for the choice and the presentation of the facts contained in this book and for the opinions expressed therein, which are not necessarily those of UNESCO and do not commit the organization. This book is a result of the research which has fi nancially been supported by the UNESCO Offi ce in Venice – UNESCO Regional Bureau for Science and Culture in Europe and Ministry of Culture of the Republic of Croatia 1 ddioio FFOREWORD.inddOREWORD.indd 2 44/7/09/7/09 11:32:50:32:50 PPMM Cultural Tourism Goes Virtual: Audience Development in Southeast European Countries Edited by Daniela Angelina Jelinčić Institute for International Relations Zagreb, 2009 1 ddioio FFOREWORD.inddOREWORD.indd 3 44/7/09/7/09 11:32:51:32:51 PPMM Culturelink Joint Publication Series No 13 Series editor Biserka Cvjetičanin Reviewers Nada Zgrabljić Rotar Nikša Alfi rević Language editing Charlotte Huntly Cover design Dragana Markanović Layout MEANDARMEDIA/Marina Belčić Printed and bound by KIKA GRAF, Zagreb Publisher Institute for International Relations Lj. -

Datë 06.03.2021

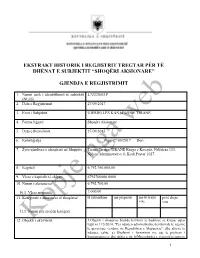

EKSTRAKT HISTORIK I REGJISTRIT TREGTAR PËR TË DHËNAT E SUBJEKTIT “SHOQËRI AKSIONARE” GJENDJA E REGJISTRIMIT 1. Numri unik i identifikimit të subjektit L72320033P (NUIS) 2. Data e Regjistrimit 27/09/2017 3. Emri i Subjektit UJËSJELLËS KANALIZIME TIRANË 4. Forma ligjore Shoqëri Aksionare 5. Data e themelimit 27/09/2017 6. Kohëzgjatja Nga: 27/09/2017 Deri: 7. Zyra qëndrore e shoqërisë në Shqipëri Tirane Tirane TIRANE Rruga e Kavajës, Ndërtesa 133, Njësia Administrative 6, Kodi Postar 1027 8. Kapitali 6.792.760.000,00 9. Vlera e kapitalit të shlyer: 6792760000.0000 10. Numri i aksioneve: 6.792.760,00 10.1 Vlera nominale: 1.000,00 11. Kategoritë e aksioneve të shoqërisë të zakonshme me përparësi me të drejte pa të drejte vote vote 11.1 Numri për secilën kategori 12. Objekti i aktivitetit: 1.Objekti i shoqerise brenda territorit te bashkise se krijuar sipas ligjit nr.l 15/2014, "Per ndarjen administrative-territoriale te njesive te qeverisjes vendore ne Republiken e Shqiperise", dhe akteve te ndarjes, eshte: a) Sherbimi i furnizimit me uje te pijshem i konsumatoreve dhe shitja e tij; b)Mirembajtja e sistemit/sistemeve 1 te furnizimit me ujë te pijshem si dhe të impianteve te pastrimit te tyre; c)Prodhimi dhe/ose blerja e ujit per plotesimin e kerkeses se konsumatoreve; c)Shërbimi i grumbullimit, largimit dhe trajtimit te ujerave te ndotura; d)Mirembajtja e sistemeve te ujerave te ndotura, si dhe të impianteve të pastrimit të tyre. 2.Shoqeria duhet të realizojë çdo lloj operacioni financiar apo tregtar që lidhet direkt apo indirect me objektin e saj, brenda kufijve tè parashikuar nga legjislacioni në fuqi. -

Economic Bulletin Economic Bulletin September 2007

volume 10 volume 10 number 3 number 3 September 2007 Economic Bulletin Economic Bulletin September 2007 E C O N O M I C September B U L L E T I N 2 0 0 7 B a n k o f A l b a n i a PB Bank of Albania Bank of Albania 1 volume 10 volume 10 number 3 number 3 September 2007 Economic Bulletin Economic Bulletin September 2007 Opinions expressed in these articles are of the authors and do not necessarily reflect the official opinion of the Bank of Albania. If you use data from this publication, you are requested to cite the source. Published by: Bank of Albania, Sheshi “Skënderbej”, Nr.1, Tirana, Albania Tel.: 355-4-222230; 235568; 235569 Fax.: 355-4-223558 E-mail: [email protected] www.bankofalbania.org Printed by: Bank of Albania Printing House Printed in: 360 copies 2 Bank of Albania Bank of Albania 3 volume 10 volume 10 number 3 number 3 September 2007 Economic Bulletin Economic Bulletin September 2007 C O N T E N T S Quarterly review of the Albanian economy over the third quarter of 2007 7 Speech by Mr. Ardian Fullani, Governor of the Bank of Albania At the signing of the Memorandum of Understanding with the Competition Authority. Tirana, 17 July 2007 41 Speech by Mr. Ardian Fullani, Governor of the Bank of Albania At the seminar “Does Central Bank Transparency Reduce Interest Rates?” Hotel “Tirana International”. August 22, 2007 43 Speech by Mr. Ardian Fullani, Governor of the Bank of Albania At the conference organized by the Central Bank of Bosnia and Herzegovina September 13, 2007 46 Speech by Mr. -

Nr Prona Ne Shitje Vendndodhja 1 Ndertese+Truall (675M Katr) Pajove

NR PRONA NE SHITJE VENDNDODHJA 1 NDERTESE+TRUALL (675M KATR) PAJOVE - PEQIN 2 NDERTESE+TRUALL(130-308M KATR) PAJOVE PAJOVE - PEQIN 3 TRUALL 200M2 & NDERTESE 130M2, DOBER, MALESI E MADHE 4 TRUALL 5000M2 & NDERTESE 328.5M2 RUBIK - KURBIN 5 TRUALL 650 M2, NDERTESE 200 M2 NDERTESE / PIKE KARBURANTI DRAGOSTUNJE - LIBRAZHD 6 ARE 2790 M2, SALLMANE, DURRES 7 ARE 2810 M2, SALLMANE, DURRES 8 ARE 3750 M2, SALLMANE, DURRES 9 ARE 3880 M2, SALLMANE, DURRES 10 ARE 6320 M2, NGA KJO 500 M2 TRUALL & 275 M2 NDERTESE, BABAN DEVOLL 11 TRUALL 50 M2 + NDERTESE 50 M2, BERAT 12 NJESI SHERB 2KATE+APARTAMENT1 KAT(TRUALL142745&250M2NJ157&317&200&317M2,AP242M2,NDRT200M2 RR. "TRANSBALLKANIKE" - VLORE 13 ULLISHTE 1600 M2, SAUK, TIRANE 14 ARE 1000M2,NR.15/74,Z-K 3184, SEKTORI RINIA,(KATUND I RI), DURRES 15 ARE + TRUALL + BANESE 306 M2, DESHIRAN, ELBASAN 16 ARE 2939 M2, DESHIRAN, ELBASAN 17 ARE 4337 M2, DESHIRAN, ELBASAN 18 ARE 6937 M2, DESHIRAN, ELBASAN 19 GARAZH 176 M2, LGJ. H. MYSHKETA, DURRES 20 NJESI 90.17 M2, KORCE 21 PEMETORE 6600 M2, SHTODHER-HELMAS-KAVAJE, 22 TRUALL 250 M2 + NDERTESE 110 M2 MJULL BATHORE,TIRANE 23 ARE SIP. 12.600 M2, KARPEN, KAVAJE 24 NJESI, 23 M2, RR. A.GOGA, DURRES 25 TOKE - ARE, 400 M2, GOLEM, KAVAJE 26 TOKE - ARE, 4170 M2, VRINE, DURRES 27 TOKE - KULLOTE SIP. 10.000 M2, VIRUA, GJIROKASTER 28 TOKE - ULLISHTE, 250 M2, KRYEMEDHENJ, KAVAJE 29 ARE 3300 M2, GESHTENJAS - POGRADEC, 30 APARTAMENT 72.6 M2, LGJ. "LIRI GERO", FIER 31 NJESI 65 M2, RR.MARGARITA TUTULANI, TIRANE 32 ARE 3.300 M2, ROMANAT - DURRES, 33 ARE 3.600 M2, ROMANAT - DURRES, 34 TRUALL SIP 20240 M2 + NDERTESE SIP. -

Albania: Average Precipitation for December

MA016_A1 Kelmend Margegaj Topojë Shkrel TRO PO JË S Shalë Bujan Bajram Curri Llugaj MA LËSI Lekbibaj Kastrat E MA DH E KU KË S Bytyç Fierzë Golaj Pult Koplik Qendër Fierzë Shosh S HK O D Ë R HAS Krumë Inland Gruemirë Water SHK OD RË S Iballë Body Postribë Blerim Temal Fajza PUK ËS Gjinaj Shllak Rrethina Terthorë Qelëz Malzi Fushë Arrëz Shkodër KUK ËSI T Gur i Zi Kukës Rrapë Kolsh Shkodër Qerret Qafë Mali ´ Ana e Vau i Dejës Shtiqen Zapod Pukë Malit Berdicë Surroj Shtiqen 20°E 21°E Created 16 Dec 2019 / UTC+01:00 A1 Map shows the average precipitation for December in Albania. Map Document MA016_Alb_Ave_Precip_Dec Settlements Borders Projection & WGS 1984 UTM Zone 34N B1 CAPITAL INTERNATIONAL Datum City COUNTIES Tiranë C1 MUNICIPALITIES Albania: Average Produced by MapAction ADMIN 3 mapaction.org Precipitation for D1 0 2 4 6 8 10 [email protected] Precipitation (mm) December kilometres Supported by Supported by the German Federal E1 Foreign Office. - Sheet A1 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 Data sources 7 8 9 0 1 2 3 4 5 6 7 8 9 0 1 2 - - - 1 1 1 1 1 1 1 1 1 1 2 2 2 The depiction and use of boundaries, names and - - - - - - - - - - - - - F1 .1 .1 .1 GADM, SRTM, OpenStreetMap, WorldClim 0 0 0 .1 .1 .1 .1 .1 .1 .1 .1 .1 .1 .1 .1 .1 associated data shown here do not imply 6 7 8 0 0 0 0 0 0 0 0 0 0 0 0 0 9 0 1 2 3 4 5 6 7 8 9 0 1 endorsement or acceptance by MapAction. -

Plani Investimeve OSHEE 2018

PLANI I INVESTIMEVE I DVSH PER VITIN 2018 A: Bulevardi “Gjergj Fishta”, Ndërtesa Nr. 88, H.1, Njësia Administrative Nr. 7, 1023, Tirana, Albania NIPT: 72410014H Faqe 1 deri 136 PERMBAJTJA 1. HYRJE................................................................................................................................................... 7 1.1 Parashikimi i Planit te investimeve per vitin 2018 .............................................................................. 9 Objektivat e Planit te Investimeve 2018........................................................................................ 9 1.2 Paraqitja e situates e vitit 2017.......................................................................................................... 11 1.3 Impakti ne humbjet e energjise elektrike te kompanise oshee sha bazuar ne investimet e parashikuara me fondet e saj per vitin 2018 ............................................................................................ 13 1.3.1 Humbjet Totale te Energjise........................................................................................................... 13 1.3.2 Humbjet Teknike ............................................................................................................................ 14 1.3.2.1 Humbjet Teknike te Energjise Elektrike ne Tension te Larte (TL)............................................ 14 1.3.2.2 Humbjet në rrjetin e Tensionit te Mesem (TM 6/10/20 kV) ................................................... 16 1.3.2.3 Humbjet e energjisë elektrike -

Preventivues Pergj.Sek.Projektimi Ing.Ademar QOSHJA Ing

DEPARTAMENTI INXHINIERIK MIRATOI SEKTORI I PROJEKTIMIT DREJTORI I PËRGJITHSHËM REDI MOLLA P R E V E N T I V TOTAL EMERTIMI I OBJEKTIT: SHERBIME TE INTEGRUARA DHE FURNIZIM VENDOSJE TE PAISJEVE ELEKTRONIKE INVESTITORI: U.K.T.Sh.a SIPERMARRESI: U.K.T.sh.a Furnizim me Sistem Energji Punime Nr. Emërtimi I Objektit Kamera+Siste Elektrike dhe Ndertimore+Puni m Alarmi Ndricim me te Ndryshme Territori 1 STP+Depo Picalle - - - 2 STP Hekal - - - 3 STP Shytqj - - - 4 STP Qeha - - - 5 STP+Depo Kacone - - - 6 STP+Depo Mullet - - - 7 Depo Daias - - - 8 Depo Barbas - - - 9 Depo Fikas - - - 10 Depo Qeha - - - 11 Depo Shytaj - - - 12 Depo Tagan - - - 13 Depo Mullet - - - 14 Depo Picalle - - - 15 Depo Petrele - - - 16 Depo Hekal - - - 17 Depo Gurre e Madhe - - - 18 Depo Vishnje - - - 19 STP Liqeni Thate - - - 20 Depo Liqeni Thate - - - 21 Depo Kala Preze - - - 22 STP Preze - - - 23 STP Preze 2 (Koder Preze) - - - 24 STP Fushe Preze - - - 25 Depom Kukunje - - - 26 Depo Arbane Vaqarr - - - 27 STP Vishnje - - - 28 Depo Sharre - - - 29 STP Zhurje - - - 30 STP Grece - - - 31 STP+Depo Lagje e Re - - - 32 STP+Depo Peze Celje - - - 33 STP+Depo Peze Helmes - - - 34 STP Vaqarr - - - 35 STP Bulltice Vaqarr (Arbane) - - - 36 Depo Peze e Vogel - - - 37 Depo Varrosh - - - 38 Depo Maknor - - - 39 Depo Pajan 1 - - - 40 Depo Pajan - - - 41 Depo Grece - - - 42 Depo Alshet - - - 43 Depo Gellbresh Lagjia Ceke - - - 44 Depo Curret Lagje e Re - - - 45 Depo Dedjet - - - 46 Depo Lagje e Re Pajont - - - 47 Depo Vaqarr 2 - - - 48 Depo Zhurje - - - 49 Depo Vaqarr - - - 50 Depo Bulqve -

Directory of Development Organizations

EDITION 2010 VOLUME III.A / EUROPE DIRECTORY OF DEVELOPMENT ORGANIZATIONS GUIDE TO INTERNATIONAL ORGANIZATIONS, GOVERNMENTS, PRIVATE SECTOR DEVELOPMENT AGENCIES, CIVIL SOCIETY, UNIVERSITIES, GRANTMAKERS, BANKS, MICROFINANCE INSTITUTIONS AND DEVELOPMENT CONSULTING FIRMS Resource Guide to Development Organizations and the Internet Introduction Welcome to the directory of development organizations 2010, Volume III: Europe The directory of development organizations, listing 63.350 development organizations, has been prepared to facilitate international cooperation and knowledge sharing in development work, both among civil society organizations, research institutions, governments and the private sector. The directory aims to promote interaction and active partnerships among key development organisations in civil society, including NGOs, trade unions, faith-based organizations, indigenous peoples movements, foundations and research centres. In creating opportunities for dialogue with governments and private sector, civil society organizations are helping to amplify the voices of the poorest people in the decisions that affect their lives, improve development effectiveness and sustainability and hold governments and policymakers publicly accountable. In particular, the directory is intended to provide a comprehensive source of reference for development practitioners, researchers, donor employees, and policymakers who are committed to good governance, sustainable development and poverty reduction, through: the financial sector and microfinance, -

LIDHJA 1 Qarku Bashkia Njësia Administrative ZAZ Nr Zyra KZAZ-Ve

LIDHJA 1 Qarku Bashkia Njësia Administrative ZAZ Nr Zyra KZAZ-ve Koplik Gruemirë KOPLIK Kastrat MALËSI E MADHE 01 Drejtoria e Bujqesise Kelmend (Kati i dyte) Qendër Shkrel Ana Malit Bërdicë Dajç Gur i zi Postribë SHKODER 02 Pult Konvikti i shkolles pyjore Shosh Rrethinat Shalë Velipojë Shkodër (zona QV 0235 deri 0245, SHKODER Shkodër zona QV 0269, zona QV 0279, zona QV 0280, zona QV 0282, zona QV 03 Shkolla 9-vjecare SHKODËR 0284, zona QV 0286 deri 0297, dhe "Ismail Dervishi" zona QV 0299 deri 0304) Shkodër (zona QV 0246 deri 0263, zona QV 0265 deri 0268, zona QV SHKODER 0270, zona QV 0276, zona QV 0316, 04 Shkolla 9-vjecare zona QV 0318, zona QV 0319 dhe "Xheladin Fishta" zona QV 0321) Shkodër (zona QV 0271 deri 0275, zona QV 0277, zona QV 278, zona QV 281, zona QV 0283, zona QV SHKODER 0285, zona QV 0298, zona QV 0305 05 Shkolla Pyjore deri 0315, zona QV 0317, zona QV (Konvikti) 0320, zona QV 0322 dhe zona QV 0323) Vau - Dejës Temal BUSHAT Shkolla e Mesme Bushat VAU - DEJËS 06 Profesionale Hajmel “Ndre Mjeda” Vig-Mnelë ( Palestra) Shllak Pukë Pukë Rrapë Shkolla e Mesme e PUKË Gjegjan 07 Bashkuar Shkodër Qerret (Palestra) Qelëz Fushë-Arrëz Blerim Fushë Arrëz FUSHË ARRËZ Qafë Mali 08 Qendra e Kultures se Fierzë Femijeve Iballë Miratuar me Vendim të KQZ-së Nr.85, datë 07.04.2015 LIDHJA 1 Qarku Bashkia Njësia Administrative ZAZ Nr Zyra KZAZ-ve Bajram Curri Bujan KOPLIK Bytyc MALËSI E MADHE 01 Drejtoria e Bujqesise Fierzë Bajram Curri TROPOJË 09 (Kati i dyte) Lekbibaj Shkolla e Mesme Llugaj Margegaj Tropojë Krumë Krumë Gjinaj HAS 10 Zyra -

ADRESA E E-MAIL Ilir Domi [email protected]

Nr. SHKOLLA Lloji Drejtori ADRESA E E-MAIL 1 AHMETAQ 9-vjeçare Ilir Domi [email protected] 2 ARBANE 9-vjeçare Enkelejda Topalli [email protected] 3 BASTAR I MESEM 9-vjeçare Sadete Duka [email protected] 4 BERXULL 9-vjeçare Zyra Prençi [email protected] 5 BERZHITE 9-vjeçare Beqir Hyka [email protected] 6 FARKE E VOGEL 9-vjeçare Xhelal Qoku [email protected] 7 FERRAJ 9-vjeçare Dorina Llalla [email protected] 8 FUSHAS 9-vjeçare Dëfrim Aga [email protected] 9 FUSHE PREZE 9-vjeçare Dashamir Shamku [email protected] 10 GJOKAJ 9-vjeçare Fatmir Çali [email protected] 11 GROPAJ 9-vjeçare Artan Allgjata [email protected] 12 HAKI SHEHU 9-vjeçare Endri Hamzaraj [email protected] 13 IBE SIPER 9-vjeçare Alma Asllani [email protected] 14 KASEM SHIMA 9-vjeçare Hasime Lamaj [email protected] 15 KASHAR-KODER 9-vjeçare Rajmonda Halili [email protected] 16 KATUND I RI 9-vjeçare Arjan Gjoka [email protected] 17 KOÇAJ 9-vjeçare Erald Dapi [email protected] 18 KUS 9-vjeçare Enver Hidri [email protected] 19 LAGJE E RE 9-vjeçare Arben Rexhepi [email protected] 20 LALM 9-vjeçare Agron Banushi [email protected] 21 LUNDER 9-vjeçare Alma Kaziu [email protected] 22 MANGULL 9-vjeçare Saimir Qordja [email protected] 23 MARQINET 9-vjeçare Agim Korriku [email protected] 24 MEZEZ-FUSHE 9-vjeçare Valbona Jahja [email protected] 25 MJULL BATHORE 9-vjeçare Edmond Sogani [email protected] 26