Annual Report 2009 3.3 Million Sq.Ft

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Major Investment Properties

Review of Operations – Business in Mainland China and Macau Major Investment Properties During the year, rental properties in mainland China generated business and will become a major source of steady income in a total gross rental income of HK$192.9 million, an increase mainland China. of HK$114.3 million over the previous year. With the gradual In order to better manage its property portfolio, in August 2007 completion of some of the above investment properties, which the Group increased its stakes in some of the rental properties, comprise mainly Grade-A offi ce space, rental income is set to which comprise commercial podia and car park basements: increase significantly during the years to come. The property investment business will complement the property development Major Completed Mainland Investment Properties Group’s share of developable gross fl oor area Group’s interest (million square Project name and location (%) feet) Commercial Podium & Car Parks Henderson Centre, Beijing 100 1.1 Skycity, Shanghai 75 0.3 Hengbao Plaza, Guangzhou 100 1.0 Sub-total: 2.4 Offi ce Offi ce Tower II, Grand Gateway, Shanghai 100 0.7 Sub-total: 0.7 Total: 3.1 Annual Report 2007 Henderson Land Development Company Limited 75 Review of Operations – Business in Mainland China and Macau Major Investment Properties Status of Major Completed Mainland Investment Properties Henderson Centre, Beijing (100% owned) Beijing Henderson Centre was completed in 1997. In order to offer a refreshing retail experience for shoppers and to promote sale for tenants, the atrium of its shopping mall has been undergoing a major renovation since March 2007. -

2020 Shanghai Foreign Investment Guide Shanghai Foreign Shanghai Foreign Investment Guide Investment Guide

2020 SHANGHAI FOREIGN INVESTMENT GUIDE SHANGHAI FOREIGN SHANGHAI FOREIGN INVESTMENT GUIDE INVESTMENT GUIDE Contents Investment Chapter II Promotion 61 Highlighted Investment Areas 10 Institutions Preface 01 Overview of Investment Areas A Glimpse at Shanghai's Advantageous Industries Appendix 66 Chapter I A City Abundant in 03 Chapter III Investment Opportunities Districts and Functional 40 Enhancing Urban Capacities Zones for Investment and Core Functions Districts and Investment Influx of Foreign Investments into Highlights the Pioneer of China’s Opening-up Key Functional Zones Further Opening-up Measures in Support of Local Development SHANGHAI FOREIGN SHANGHAI FOREIGN 01 INVESTMENT GUIDE INVESTMENT GUIDE 02 Preface Situated on the east coast of China highest international standards Secondly, the openness of Shanghai Shanghai is becoming one of the most At the beginning of 2020, Shang- SHFTZ with a new area included; near the mouth of the Yangtze River, and best practices. As China’s most translates into a most desired invest- desired investment destinations for hai released the 3.0 version of its operating the SSE STAR Market with Shanghai is internationally known as important gateway to the world, ment destination in the world char- foreign investors. business environment reform plan its pilot registration-based IPO sys- a pioneer of China’s opening to the Shanghai has persistently functioned acterized by increasing vitality and Thirdly, the openness of Shanghai is – the Implementation Plan on Deep- tem; and promoting the integrated world for its inclusiveness, pursuit as a leader in the national opening- optimized business environment. shown in its pursuit of world-lead- ening the All-round Development of a development of the YRD region as of excellence, cultural diversity, and up initiative. -

Instantaneous Electric Water Heater Series

Instantaneous Electric Water Heater Series 全機德國設計及製造 RENOWNED GERMAN CRAFTSMANSHIP 傳承德國工藝 品質享負盛名 German technology is renowned for refined 德國工藝以做工精細、持久耐用及講究實效而 craftsmanship, durability, and functionality. Designed 享譽世界,德國寶即熱式電熱水器研發及生產基 in Lüneburg, Northern Germany, German Pool’s 地均位於德國北部的呂訥堡,從研發、製造到 Instantaneous Electric Water Heaters are manufactured 質檢包裝,都全線在德國本土進行,每個部件的 to an exacting standard under the watchful eyes of 生產都由高素質工程師依照相關標準嚴格把關, our highly qualified German engineers. Nothing carries 盡得德國工藝精髓。優異的品質和技術的創新印 the German Pool label unless we are proud of it; and 證德國寶對精細做工孜孜不倦的追求。 頂尖德國科技始於 our Instantaneous Electric Water Heaters are proof of our commitment to exceptional craftsmanship and SINCE 1951 impeccable quality. 全機德國設計及製造 榮獲歐盟A級能源效益認證 2 | GERMAN POOL Instantaneous Electric Water Heater Series 德國寶即熱式電熱水器系列 | 3 單相電源 三相電源 GPI-M3 單相電源 Single-Phase Power Supply Three-Phase Power Supply 水壓控制 HYDRAULIC CONTROL 1-Phase Power Supply 迷你系列 Mini Series 洗手盆 鋅盆 洗手盆 Wash Basin Kitchen Sink Wash Basin 㷃⩢㔶⏅ 㷃⩢㔶⏅ ⋷梊ⳟ㔶⏅ Hydraulic Hydraulic Full Electronic Control Control Control GPI-M3 GPI-M6 GPI-M8 纖巧系列 Compact Series G & U LU SE P ⋷梊ⳟ㔶⏅ ⋷梊ⳟ㔶⏅ 鋅盆 洗手盆 淋浴 Full Electronic 浴盆 鋅盆 洗手盆 淋浴 Full Electronic Control Control Kitchen Sink Wash Basin Shower Bath Kitchen Sink Wash Basin Shower 一 插 即 用 CEX-9 CEX13 CEX21 > 迷你外型極致纖巧,配備13A插頭革命性 「一插即用」設計 Ultra-compact design, revolutionary 13A socket 'Plug & Use' design > 適合安裝於洗手盆 Specially designed for handwashing > 適用於辦公室、醫院、學校、商場等洗手盤 Great for facilities like offices, hospitals, schools, malls… CEX-9U -

A New Freshwater Psammodictyon Species in the Taihu Basin, Jiangsu Province, China

144 Fottea, Olomouc, 20(2): 144–151, 2020 DOI: 10.5507/fot.2020.005 A new freshwater Psammodictyon species in the Taihu Basin, Jiangsu Province, China Qi Yang1, Tengteng Liu1, Pan Yu1, Junyi Zhang2, J. Patrick Kociolek3, Quanxi Wang & Qingmin You1* 1 College of Life Sciences, Shanghai Normal University, Shanghai 200234, China; *Corresponding author e– mail: [email protected] 2 Jiangsu Wuxi Environmental Monitoring Center, Wuxi 214121, China 3 Museum of Natural History and Department of Ecology and Evolutionary Biology, University of Colorado, Boulder, CO 80309, USA Abstract: We describe a new species of diatom, Psammodictyon taihuensis sp. nov., collected from the Taihu Basin, Jiangsu Province, China. There are several features of this diatom that suggest it should be included in the genus Psammodictyon, notably the possession of panduriform valves characterized by a longitudinal fold near the apical axis, coarsely areolate striae, and a keeled raphe system present on the valve margin. This species is distinct from others in the genus by its small size, being only 16.5–25.0 μm long and 10.0–12.5 μm wide in the central region, and with the widest valve being 10.5–13.5 μm in width. There are 8–11 distinct fibulae per 10 μm and the striae are composed of 18–22 coarse areolae per 10 μm. This is the first report of a freshwater member of the genus Psammodictyon in China, which expands the known geographical and ecological distributions of the genus and enhances our understanding of freshwater diatom diversity in China. Key words: diatom, new species, Psammodictyon, Taihu Lake, taxonomy Introduction opposing sides of the valves of the frustule (similar to the diagonal symmetry of other members of the family The genus Psammodictyon D.G. -

管理層之討論及分析 Management Discussion and Analysis

管理層之討論及分析 MANAGEMENT DISCUSSION AND ANALYSIS 本年主要事項 22 KEY EVENTS OF THE YEAR 業務概覽及策略 2 BUSINESS OVERVIEW AND STRATEGIES 香港物業租賃 26 HONG KONG PROPERTY LEASING 香港物業發展及銷售 36 HONG KONG PROPERTY DEVELOPMENT AND SALES 中國內地業務 2 MAINLAND CHINA OPERATIONS 業務展望 0 FROM STRATEGY TO REALITY : NEXT MOVES 集團主要物業 6 MAJOR GROUP PROPERTIES 62 財務業績及狀況回顧 REVIEW OF FINANCIAL RESULTS AND POSITION 財務回顧 6 FINANCIAL REVIEW 風險管理 66 RISK MANAGEMENT 得獎項目 68 PROJECT AWARDS 企業公民 7 CORPORATE CITIZENSHIP 僱員關係 78 EMPLOYEE RELATIONS 管理層之討論及分析 MANAGEMENT DISCUSSION AND ANALYSIS 本年主要事項 KEY EVENTS OF THE YEAR 07 與長沙市芙蓉區人民政府簽署意向書,於長沙市 發展一個具世界建築水平的大型綜合發展項目─ 2006 「長沙恒隆廣場」。 Signed a Memorandum of Understanding with the district government of Furong District, Changsha City to develop “Changsha Hang Lung Plaza” — a world class, large scale multi-complex in Changsha City. 08 11 2006 2006 以人民幣約8.95億元成功投得遼 我們以先舊後新方式配售4.1億股,配售 寧省瀋陽市市政府廣場南面、瀋 價每股港幣16.3元,集資額約達港幣67 河區青年大街旁一幅約92,000平 億元,並計劃將所得款項淨額用於核心物 方米土地,作為我們其中一項大 業發展及投資業務,特別是中國內地。 型綜合發展項目。 Raised approximately HK$6.7 billion Acquired a prime lot of about through a placement of 410 million 92,000 square metres on the shares at HK$16.30 per share. We south side of City Plaza, intend to apply such net proceeds along Qingnian Street, for our core property development Shenhe District of Shenyang and investment activities, City, Liaoning Province, for particularly in mainland China. approximately RMB 895 million. We intend to develop a grand scale multi-complex development. 22 恒 隆 地 產 有 限 公 司 二零零六 /零七年年報 12 2006 以約人民幣6.85億元成功投得無錫市崇安區人民中路一幅 面積約37,324平方米之黃金地塊,以發展一項大型綜合發 展項目,包括世界級購物中心及辦公室大樓。該項目將命名 為「無錫恒隆廣場」,總樓面面積約255,000平方米。 Acquired a prime lot of circa 37,324 square metres at Renmin Zhong Road, in the Chongan District of Wuxi City, for approximately RMB 685 million for development of a large-scale multi-complex project comprising a world-class shopping mall and office towers. -

Eriocheir Sinensis) Meat Using Electronic Tongue Analysis

Sensors and Materials, Vol. 33, No. 7 (2021) 2537–2547 2537 MYU Tokyo S & M 2637 Taste Profile Characterization of Chinese Mitten Crab (Eriocheir sinensis) Meat Using Electronic Tongue Analysis Hongbo Liu,1 Tao Jiang,1 Junren Xue,2 Xiubao Chen,1 Zhongya Xuan,2 and Jian Yang1,2* 1Key Laboratory of Fishery Ecological Environment Assessment and Resource Conservation in Middle and Lower Reaches of the Yangtze River, Freshwater Fisheries Research Center, Chinese Academy of Fishery Sciences, Wuxi 214081, China 2Wuxi Fisheries College, Nanjing Agricultural University, Wuxi 214081, China (Received May 27, 2021; accepted June 18, 2021) Keywords: Eriocheir sinensis, taste sensing system, taste-active value, food quality, authentication An SA402B taste sensing system (electronic tongue) was used to evaluate the meat taste characteristics of three groups of Chinese mitten crab Eriocheir sinensis (H. Milne Edwards, 1853): those from the native culture area in the Yangcheng Lake, Yangcheng Lake-labeled crabs from the market, and those from aquaculture ponds. The electronic tongue data showed that umami was the most predominant taste in the steamed meat, followed by sweetness. The aftertaste of umami was clearly observed in all crab meat samples. Saltiness and bitterness varied widely depending on the geographic origin. There was only a little aftertaste of bitterness and no discernable sourness, astringency, or aftertaste of astringency. Principal component analysis (PCA) exhibited a clear grouping trend among the three crab groups. Linear discriminant analysis revealed that the crab groups can be separated from each other with 100% accuracy on the basis of the aforementioned measurable taste values. The taste sensing system can accurately profile the taste characteristics of crabs native to Yangcheng Lake, those marketed as Yangcheng Lake-labeled crabs, and those of pond-cultured crabs. -

Download Here

ISABEL SUN CHAO AND CLAIRE CHAO REMEMBERING SHANGHAI A Memoir of Socialites, Scholars and Scoundrels PRAISE FOR REMEMBERING SHANGHAI “Highly enjoyable . an engaging and entertaining saga.” —Fionnuala McHugh, writer, South China Morning Post “Absolutely gorgeous—so beautifully done.” —Martin Alexander, editor in chief, the Asia Literary Review “Mesmerizing stories . magnificent language.” —Betty Peh-T’i Wei, PhD, author, Old Shanghai “The authors’ writing is masterful.” —Nicholas von Sternberg, cinematographer “Unforgettable . a unique point of view.” —Hugues Martin, writer, shanghailander.net “Absorbing—an amazing family history.” —Nelly Fung, author, Beneath the Banyan Tree “Engaging characters, richly detailed descriptions and exquisite illustrations.” —Debra Lee Baldwin, photojournalist and author “The facts are so dramatic they read like fiction.” —Heather Diamond, author, American Aloha 1968 2016 Isabel Sun Chao and Claire Chao, Hong Kong To those who preceded us . and those who will follow — Claire Chao (daughter) — Isabel Sun Chao (mother) ISABEL SUN CHAO AND CLAIRE CHAO REMEMBERING SHANGHAI A Memoir of Socialites, Scholars and Scoundrels A magnificent illustration of Nanjing Road in the 1930s, with Wing On and Sincere department stores at the left and the right of the street. Road Road ld ld SU SU d fie fie d ZH ZH a a O O ss ss U U o 1 Je Je o C C R 2 R R R r Je Je r E E u s s u E E o s s ISABEL’SISABEL’S o fie fie K K d d d d m JESSFIELD JESSFIELDPARK PARK m a a l l a a y d d y o o o o d d e R R e R R R R a a S S d d SHANGHAISHANGHAI -

Report on the State of the Environment in China 2016

2016 The 2016 Report on the State of the Environment in China is hereby announced in accordance with the Environmental Protection Law of the People ’s Republic of China. Minister of Ministry of Environmental Protection, the People’s Republic of China May 31, 2017 2016 Summary.................................................................................................1 Atmospheric Environment....................................................................7 Freshwater Environment....................................................................17 Marine Environment...........................................................................31 Land Environment...............................................................................35 Natural and Ecological Environment.................................................36 Acoustic Environment.........................................................................41 Radiation Environment.......................................................................43 Transport and Energy.........................................................................46 Climate and Natural Disasters............................................................48 Data Sources and Explanations for Assessment ...............................52 2016 On January 18, 2016, the seminar for the studying of the spirit of the Sixth Plenary Session of the Eighteenth CPC Central Committee was opened in Party School of the CPC Central Committee, and it was oriented for leaders and cadres at provincial and ministerial -

Progress of Major Development Projects

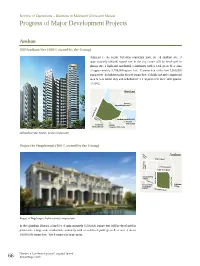

Review of Operations – Business in Mainland China and Macau Progress of Major Development Projects Anshan Old Stadium Site (100% owned by the Group) Adjacent to the scenic Yufoshan municipal park, an old stadium site of approximately 600,000 square feet in the city centre will be developed in phases into a high-end residential community with a total gross floor area of approximately 3,700,000 square feet. Construction of the first 1,200,000 square feet of residences plus 60,000 square feet of clubhouse and commercial area is now under way and scheduled for completion in the fourth quarter of 2013. Anshan Anshan International Hotel YuanlinHuaixiang Road Road Anshan Gateball Field Anshan Yufo Court Anshanshi Anshan Justice Bureau Laoganbu University Old Stadium Site, Anshan (artist’s impression) Project in Yingchengzi (100% owned by the Group) Hunan Street Anshan Yingcui Road Huihuayuan Road Yingcheng Cuijia North Road Gaoguanling Village Anxia Line Cuijia West Road West Cuijia Gaoguanling Cuijiatun Elementary Road Guihua Village School Kuanggong Road Project in Yingchengzi, Anshan (artist’s impression) In the Qianshan District, a land lot of approximately 5,500,000 square feet will be developed in phases into a large scale residential community with a total developable gross floor area of about 14,000,000 square feet. Site formation is in progress. Henderson Land Development Company Limited 66 Annual Report 2011 Review of Operations – Business in Mainland China and Macau • Progress of Major Development Projects Changsha The Arch of Triumph -

Department of International Trade Promotion Importer List (2C1)

DEPARTMENT OF INTERNATIONAL TRADE PROMOTION IMPORTER LIST (2C1) 1 ANDERYEE COMMERCIAL CO.,LTD. Attn: KHUN - - 208 BLDG. D, FANGQUN Import Product:- 27 NANSANHUAN RD, EAST - BEVERAGE SHANGHAI 100078 CHINA. - PREPARED FOOD TEL: 86-10 67606242 - SEASONING FAX: 86-10 67604248 - SNACK FOODS E-Mail: [email protected] Web Site: - 5 CHUNYUAN TRADE CO., LTD. Attn: KHUN DAI XINZHONG #1509,ELEVATOR A,LIHONGJI CENT Import Product:- NO.23,YUEJIN RD.,SHANTOU, GUAN - Biscuits and Wafers SHANTOU 515031 CHINA. TEL: +867548987918 2 B & S COMPANY FAX: +867548987913 1207-11, LEIGHTON CENTRE, E-Mail: [email protected] 77 LEIGHTON ROAD, CAUSEWAY BAY Web Site: HTTP://WWW.CHUNYUAN.CN HONG KONG CHINA. Attn: KHUN WU YIHAO TEL: 852-00 2893 2278 Import Product:- FAX: 2893 6632 - Snacks E-Mail: [email protected] Attn: KHUN STEPHEN CHAN 6 DONGGUAN HUABAO FOOD CO., LTD. Import Product:- XIAOQIAO IND. AREA, FUCHENG TOWN, - Fruit and Vegetable Products DONGGUAN, GUANGDONG 523112 CHINA. 3 BEIJING HUALIAN INTERNATIONAL COMMERCIAL TEL: 86-769 2269998, 86-769 2264998 NO.180 GUANG ANMENWAI GREAT STREET OF FAX: 86-769 2252623 XUANWU DISTRICT OF BEIJING Attn: KHUN HE SHAOGANG 100055 PR CHINA. Import Product:- TEL: +86-10 63280779 - CANDIES FAX: 63280779 - Cookies E-Mail: [email protected] - Eggs Attn: MS. PANG KUN RONG - Rice Cracker Import Product:- - Beverage 7 DONGGUAN SHILONG CANDY & BISCUIT FACTORY 20, BAIHUA RD. (N), SHILONG TOWN, 4 CARREFOUR DONGGUAN NO.10, XIN GUANG RD, CHENGDU, SICHUAN GUANGDONG 523321 CHINA. CHENGDU - CHINA. TEL: 86-0769 6611193 TEL: 86-28 8513835 FAX: 86-0769 6611193 FAX: 86-28 85138354 Attn: KHUN CHEN CHUAN Web Site: www.carrefour.com.cn, carrefour.com.cn/about/priva Import Product:- 1/5 12 September 2013 (13:17) - Biscuits and Wafers 11 GUANGZHOU S.B.C.TRADING CO.,LTD - Biscuits/Cakes RM.1406, NANFANG TIEDAU BLDG., - Box (Multi Purpose) NO.57 ZHONGSHAN 1RD.,MTR.A EXIT IN GUANGZHOU - Candy Box-Glass GUANGZHOU 510600 CHINA. -

D10441 2018 年第 47 期憲報第 4 號特別副刊 S. S. No. 4 to Gazette

2018 年第 47 期憲報第 4 號特別副刊 S. S. NO. 4 TO GAZETTE NO. 47/2018 D10441 G.N. (S.) 62 of 2018 Employment Ordinance (Chapter 57) Employment Agency Regulations ISSUE OF EMPLOYMENT AGENCY LICENCES/CERTIFICATES OF EXEMPTION Pursuant to regulation 16 of the Employment Agency Regulations, the Commissioner for Labour hereby publishes the names of the persons and agencies to whom licences were issued during the period 1 January 2017 to 31 December 2017 and certificates of exemption that have been issued and remained valid during the same period. The data published in this gazette shall ONLY be used for the purpose of ascertaining whether a person or an employment agency has been granted a licence/certificate of exemption. (a) Employment Agency Licences Issued Licensee Employment Agency Remarks LEE Miu-ha Cindy Good Jobs Personnel & Secretarial Services Room 701, 7th floor, Dannies House, 20 Luard Road, Wan Chai, Hong Kong. CHUI Siu-yee Smartech Consultants Center Room 1202, 12th floor, 655 Nathan Road, Mong Kok, Kowloon. Sonmass Limited Sonmass Limited Room 609, 6th floor, David House, 8-20 Nanking Street, Yau Ma Tei, Kowloon. KWEE Kei Alexander Gracia Trading & Services Co. 16th floor, Kam Fung Commercial Building, 2-4 Tin Lok Lane, Wan Chai, Hong Kong. WONG Wing-yi C & Y PERSONNEL CONSULTANTS Room A105, 1st floor, New East Sun Industrial Building, 18 Shing Yip Street, Kwun Tong, Kowloon. Executive Access Limited Executive Access Limited Room 1302-1308, 13th floor, Prince’s Building, 10 Chater Road, Central, Hong Kong. Nation Employment Nation Employment Agency Limited Agency Limited Shop 73, 1st floor, Fu Fai Shopping Centre, 28 On Shing Street, Ma On Shan, New Territories. -

List of Radio Dealer (Unrestricted) Licensees (As at 16/08/2021)

List of Radio Dealer (Unrestricted) Licensees 無線電商(放寬限制)持牌商名單 ( As at 16/09/2021) (截至 16/09/2021) Licensee Address Telephone Licence No. (Ex-Licence No.) 持牌商 地址 電話 牌照號碼 (原有牌照號碼) RM. G87, G/F, SINCERE PODIUM, , MONG KOK 1 + 1 九龍旺角先達廣場地下G87號舖 55926692 RU00231996-RU 188 TELECOM GROUP LIMITED RU00119316-RU 188 電訊集團有限公司 G/F, 188 APLIU ST, SHAM SHUI PO 35860072 (11931) 188 TELECOM O/B 188 TELECOM GROUP LIMITED 188電訊 O/B 188電訊集團有限公司 G/F, 209 APLIU ST, SHAM SHUI PO 23207788 RU00180442-RU 2626 LIMITED RM. /FLAT 1, 5/F, BLK A, HOI LUEN INDUSTRIAL CENTRE, 55 HOI YUEN ROAD, KWUN TONG 97804506 RU00158065-RU 28 FOOD (HK) LIMITED G/F, 204 FA YUEN STREET, MONG KOK 易發食品(香港)有限公司 九龍旺角花園街204號地下 26939008 RU00222985-RU 2DEEP INTERNATIONAL LIMITED 泰森國際貿易有限公司 RM. /FLAT A, 12/F, ZJ 300, 300 LOCKHART ROAD, WAN CHAI 51731646 RU00230817-RU 360 KIDS GUARD CO. LIMITED 2/F, YAU TAK BUILDING, 167 LOCKHART ROAD, WAN CHAI 21563920 RU00216069-RU 365 DAYS FREIGHT SERVICES (HK) LIMITED 5/F, BLK F, COMFORT BUILDING, 86-88A NATHAN ROAD, TSIM SHA TSUI +852 62213657 RU00220056-RU 3M HONG KONG LTD RU00132097-RU 三M香港有限公司 38/F, MANHATTAN PLACE, 23 WANG TAI ROAD, KOWLOON BAY 28066111 (13209) 4&6 TELECOM LIMITED RM. /FLAT 01, 11/F, HANG SENG CASTLE PEAK RD BLDG, 339 CASTLE PEAK RD, CHEUNG SHA WAN +852 66493320 RU00202666-RU 409 SHOP RU00128365-RU 409專門店 RM. /FLAT D-E, 11/F, FLOURISH FOOD MFY CTR, 18 TAI LEE STREET, YUEN LONG 35860967 (12836) 4PX EXPRESS CO., LIMITED RU00129432-RU 遞四方速遞有限公司 G/F, 167-169 HOI BUN ROAD, KWUN TONG 29772988 (12943) 5 CELL RM.