The Ldp and the Pembrokeshire Economy

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Long-Term Prospects for Northwest European Refining

LONG-TERM PROSPECTS FOR NORTHWEST EUROPEAN REFINING ASYMMETRIC CHANGE: A LOOMING GOVERNMENT DILEMMA? ROBBERT VAN DEN BERGH MICHIEL NIVARD MAURITS KREIJKES CIEP PAPER 2016 | 01 CIEP is affiliated to the Netherlands Institute of International Relations ‘Clingendael’. CIEP acts as an independent forum for governments, non-governmental organizations, the private sector, media, politicians and all others interested in changes and developments in the energy sector. CIEP organizes lectures, seminars, conferences and roundtable discussions. In addition, CIEP members of staff lecture in a variety of courses and training programmes. CIEP’s research, training and activities focus on two themes: • European energy market developments and policy-making; • Geopolitics of energy policy-making and energy markets CIEP is endorsed by the Dutch Ministry of Economic Affairs, the Dutch Ministry of Foreign Affairs, the Dutch Ministry of Infrastructure and the Environment, BP Europe SE- BP Nederland, Coöperatieve Centrale Raiffeisen-Boerenleenbank B.A. ('Rabobank'), Delta N.V., ENGIE Energie Nederland N.V., ENGIE E&P Nederland B.V., Eneco Holding N.V., EBN B.V., Essent N.V., Esso Nederland B.V., GasTerra B.V., N.V. Nederlandse Gasunie, Heerema Marine Contractors Nederland B.V., ING Commercial Banking, Nederlandse Aardolie Maatschappij B.V., N.V. NUON Energy, TenneT TSO B.V., Oranje-Nassau Energie B.V., Havenbedrijf Rotterdam N.V., Shell Nederland B.V., TAQA Energy B.V.,Total E&P Nederland B.V., Koninklijke Vopak N.V. and Wintershall Nederland B.V. CIEP Energy -

A40 St Clears to Haverfordwest Economic Active and Location (EALI)

A40 St Clears to Haverfordwest Economic Activity & Location Impacts (EALI) Study Final Report On behalf of Welsh Government Project Ref: 33459 | Rev: SC | Date: June 2015 Office Address: Exchange Place 3, 3 Semple Street. Edinburgh, EH3 8BL T: +44 (0)131 297 7010 E: [email protected] Final Report A40 St Clears to Haverfordwest Economic Activity & Location Impacts (EALI) Study Document Control Sheet Project Name: A40 St Clears to Haverfordwest Economic Activity & Location Impacts (EALI) Study Project Ref: 33459 Report Title: Final Report Date: 6th June 2015 Name Position Signature Date Stephen Principal Transport Prepared by: SC 09/05/2015 Canning Planner Reviewed by: Dr Scott Leitham Senior Associate SL 11/05/2015 Approved by: Dr Scott Leitham Senior Associate SL 11/05/2015 For and on behalf of Peter Brett Associates LLP Revision Date Description Prepared Reviewed Approved WG Minor amendments to take Stephen Dr Scott Dr Scott 05/06/2015 Comments account of WG comments Canning Leitham Leitham Peter Brett Associates LLP disclaims any responsibility to the Client and others in respect of any matters outside the scope of this report. This report has been prepared with reasonable skill, care and diligence within the terms of the Contract with the Client and generally in accordance with the appropriate ACE Agreement and taking account of the manpower, resources, investigations and testing devoted to it by agreement with the Client. This report is confidential to the Client and Peter Brett Associates LLP accepts no responsibility of whatsoever nature to third parties to whom this report or any part thereof is made known. -

Mineral Reconnaissance Programme Report

_..._ Natural Environment Research Council -2 Institute of Geological Sciences - -- Mineral Reconnaissance Programme Report c- - _.a - A report prepared for the Department of Industry -- This report relates to work carried out by the British Geological Survey.on behalf of the Department of Trade I-- and Industry. The information contained herein must not be published without reference to the Director, British Geological Survey. I- 0. Ostle Programme Manager British Geological Survey Keyworth ._ Nottingham NG12 5GG I No. 72 I A geochemical drainage survey of the Preseli Hills, south-west Dyfed, Wales I D I_ I BRITISH GEOLOGICAL SURVEY Natural Environment Research Council I Mineral Reconnaissance Programme Report No. 72 A geochemical drainage survey of the I Preseli Hills, south-west Dyfed, Wales Geochemistry I D. G. Cameron, BSc I D. C. Cooper, BSc, PhD Geology I P. M. Allen, BSc, PhD Mneralog y I H. W. Haslam, MA, PhD, MIMM $5 NERC copyright 1984 I London 1984 A report prepared for the Department of Trade and Industry Mineral Reconnaissance Programme Reports 58 Investigation of small intrusions in southern Scotland 31 Geophysical investigations in the 59 Stratabound arsenic and vein antimony Closehouse-Lunedale area mineralisation in Silurian greywackes at Glendinning, south Scotland 32 Investigations at Polyphant, near Launceston, Cornwall 60 Mineral investigations at Carrock Fell, Cumbria. Part 2 -Geochemical investigations 33 Mineral investigations at Carrock Fell, Cumbria. Part 1 -Geophysical survey 61 Mineral reconnaissance at the -

Existing Electoral Arrangements

COUNTY OF PEMBROKESHIRE EXISTING COUNCIL MEMBERSHIP Page 1 2012 No. OF ELECTORS PER No. NAME DESCRIPTION ELECTORATE 2012 COUNCILLORS COUNCILLOR 1 Amroth The Community of Amroth 1 974 974 2 Burton The Communities of Burton and Rosemarket 1 1,473 1,473 3 Camrose The Communities of Camrose and Nolton and Roch 1 2,054 2,054 4 Carew The Community of Carew 1 1,210 1,210 5 Cilgerran The Communities of Cilgerran and Manordeifi 1 1,544 1,544 6 Clydau The Communities of Boncath and Clydau 1 1,166 1,166 7 Crymych The Communities of Crymych and Eglwyswrw 1 1,994 1,994 8 Dinas Cross The Communities of Cwm Gwaun, Dinas Cross and Puncheston 1 1,307 1,307 9 East Williamston The Communities of East Williamston and Jeffreyston 1 1,936 1,936 10 Fishguard North East The Fishguard North East ward of the Community of Fishguard and Goodwick 1 1,473 1,473 11 Fishguard North West The Fishguard North West ward of the Community of Fishguard and Goodwick 1 1,208 1,208 12 Goodwick The Goodwick ward of the Community of Fishguard and Goodwick 1 1,526 1,526 13 Haverfordwest: Castle The Castle ward of the Community of Haverfordwest 1 1,651 1,651 14 Haverfordwest: Garth The Garth ward of the Community of Haverfordwest 1 1,798 1,798 15 Haverfordwest: Portfield The Portfield ward of the Community of Haverfordwest 1 1,805 1,805 16 Haverfordwest: Prendergast The Prendergast ward of the Community of Haverfordwest 1 1,530 1,530 17 Haverfordwest: Priory The Priory ward of the Community of Haverfordwest 1 1,888 1,888 18 Hundleton The Communities of Angle. -

The DA GHGI Improvement Programme 2009-2010 Industry Sector Task

The DA GHGI Improvement Programme 2009-2010 Industry Sector Task DECC, The Scottish Government, The Welsh Assembly Government and the Northern Ireland Department of the Environment AEAT/ENV/R/2990_3 Issue 1 May 2010 DA GHGI Improvements 2009-2010: Industry Task Restricted – Commercial AEAT/ENV/R/2990_3 Title The DA GHGI Improvement Programme 2009-2010: Industry Sector Task Customer DECC, The Scottish Government, The Welsh Assembly Government and the Northern Ireland Department of the Environment Customer reference NAEI Framework Agreement/DA GHGI Improvement Programme Confidentiality, Crown Copyright copyright and reproduction File reference 45322/2008/CD6774/GT Reference number AEAT/ENV/R/2990_3 /Issue 1 AEA Group 329 Harwell Didcot Oxfordshire OX11 0QJ Tel.: 0870 190 6584 AEA is a business name of AEA Technology plc AEA is certificated to ISO9001 and ISO14001 Authors Name Stuart Sneddon and Glen Thistlethwaite Approved by Name Neil Passant Signature Date 20th May 2010 ii AEA Restricted – Commercial DA GHGI Improvements 2009-2010: Industry Task AEAT/ENV/R/2990_3 Executive Summary This research has been commissioned under the UK and DA GHG inventory improvement programme, and aims to research emissions data for a group of source sectors and specific sites where uncertainties have been identified in the scope and accuracy of available source data. Primarily this research aims to review site-specific data and regulatory information, to resolve differences between GHG data reported across different emission reporting mechanisms. The research has comprised: 1) Data review from different reporting mechanisms (IPPC, EU ETS and EEMS) to identify priority sites (primarily oil & gas terminals, refineries and petrochemicals), i.e. -

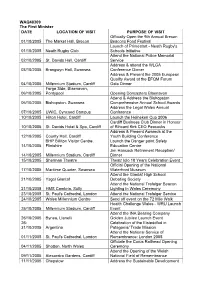

WAQ48309 the First Minister DATE LOCATION OF

WAQ48309 The First Minister DATE LOCATION OF VISIT PURPOSE OF VISIT Officially Open the 9th Annual Brecon 01/10/2005 The Market Hall, Brecon Beacons Food Festival Launch of Primestart - Neath Rugby's 01/10/2005 Neath Rugby Club Schools Initiative Attend the National Police Memorial 02/10/2005 St. Davids Hall, Cardiff Service Address & attend the WLGA 03/10/2005 Brangwyn Hall, Swansea Conference Dinner Address & Present the 2005 European Quality Award at the EFQM Forum 04/10/2005 Millennium Stadium, Cardiff Gala Dinner Forge Side, Blaenavon, 06/10/2005 Pontypool Opening Doncasters Blaenavon Attend & Address the Bishopston 06/10/2005 Bishopston, Swansea Comprehensive Annual School Awards Address the Legal Wales Annual 07/10/2005 UWIC, Cyncoed Campus Conference 10/10/2005 Hilton Hotel, Cardiff Launch the Heineken Cup 2006 Cardiff Business Club Dinner in Honour 10/10/2005 St. Davids Hotel & Spa, Cardiff of Rihcard Kirk CEO Peacocks Address & Present Awareds at the 12/10/2005 County Hall, Cardiff Youth Building Conference BHP Billiton Visitor Centre, Launch the Danger point Safety 14/10/2005 Flintshire Education Centre Jim Hancock Retirement Reception/ 14/10/2005 Millennium Stadium, Cardiff Dinner 15/10/2005 Sherman Theatre Theatr Iolo 18 Years Celebration Event Official Opening of the National 17/10/2005 Maritime Quarter, Swansea Waterfront Museum Attend the Glantaf High School 21/10/2005 Ysgol Glantaf Debating Society Attend the National Trafalgar Beacon 21/10/2005 HMS Cambria, Sully Lighting in Wales Ceremony 23/10/2005 St. Paul's Cathedral, London Attend the National Trafalgar Service 24/10/2005 Wales Millennium Centre Send off event on the 72 Mile Walk Health Challenge Wales - WRU Launch 25/10/2005 Millennium Stadium, Cardiff Event Attend the INA Bearing Company 26/10/2005 Bynea, Llanelli Golden Jubilee Launch Event 26- Celebration of the Eisteddfod in 31/10/2005 Argentina Patagonia/ Trade Mission Attend the National Service of 01/11/2005 St. -

Pembrokeshire Coast Pathtrailbl

Pemb-5 Back Cover-Q8__- 8/2/17 4:46 PM Page 1 TRAILBLAZER Pembrokeshire Coast Path Pembrokeshire Coast Path 5 EDN Pembrokeshire ‘...the Trailblazer series stands head, Pembrokeshire shoulders, waist and ankles above the rest. They are particularly strong on mapping...’ COASTCOAST PATHPATH THE SUNDAY TIMES 96 large-scale maps & guides to 47 towns and villages With accommodation, pubs and restaurants in detailed PLANNING – PLACES TO STAY – PLACES TO EAT guides to 47 towns and villages Manchester includingincluding Tenby, Pembroke, Birmingham AMROTHAMROTH TOTO CARDIGANCARDIGAN St David’s, Fishguard & Cardigan Cardigan Cardiff Amroth JIM MANTHORPE & o IncludesIncludes 9696 detaileddetailed walkingwalking maps:maps: thethe London PEMBROKESHIRE 100km100km largest-scalelargest-scale mapsmaps availableavailable – At just COAST PATH 5050 milesmiles DANIEL McCROHAN under 1:20,000 (8cm or 311//88 inchesinches toto 11 mile)mile) thesethese areare biggerbigger thanthan eveneven thethe mostmost detaileddetailed The Pembrokeshire Coast walking maps currently available in the shops. Path followsfollows aa NationalNational Trail for 186 miles (299km) o Unique mapping features – walking around the magnificent times,times, directions,directions, trickytricky junctions,junctions, placesplaces toto coastline of the Pembroke- stay, places to eat, points of interest. These shire Coast National Park are not general-purpose maps but fully inin south-westsouth-west Wales.Wales. edited maps drawn by walkers for walkers. Renowned for its unspoilt sandy beaches, secluded o ItinerariesItineraries forfor allall walkerswalkers – whether coves, tiny fishing villages hiking the entire route or sampling high- and off-shore islands rich lightslights onon day walks or short breaks inin birdbird andand marinemarine life,life, thisthis National Trail provides o Detailed public transport information some of the best coastal Buses, trains and taxis for all access points walking in Britain. -

Pembrokeshire County Council Cyngor Sir Penfro

Pembrokeshire County Council Cyngor Sir Penfro Freedom of Information Request: 10679 Directorate: Community Services – Infrastructure Response Date: 07/07/2020 Request: Request for information regarding – Private Roads and Highways I would like to submit a Freedom of Information request for you to provide me with a full list (in a machine-readable format, preferably Excel) of highways maintainable at public expense (including adopted roads) in Pembrokeshire. In addition, I would also like to request a complete list of private roads and highways within the Borough. Finally, if available, I would like a list of roads and property maintained by Network Rail within the Borough. Response: Please see the attached excel spreadsheet for list of highways. Section 21 - Accessible by other means In accordance with Section 21 of the Act we are not required to reproduce information that is ‘accessible by other means’, i.e. the information is already available to the public, even if there is a fee for obtaining that information. We have therefore provided a Weblink to the information requested. • https://www.pembrokeshire.gov.uk/highways-development/highway-records Once on the webpage click on ‘local highways search service’ The highway register is publicly available on OS based plans for viewing at the office or alternatively the Council does provide a service where this information can be collated once the property of interest has been identified. A straightforward highway limit search is £18 per property, which includes a plan or £6 for an email confirmation personal search, the highway register show roads under agreement or bond. With regards to the list of roads and properties maintained by Network Rail we can confirm that Pembrokeshire County Council does not hold this information. -

Report No. 08/19 Operational Review Committee

Report No. 08/19 Operational Review Committee REPORT OF THE BIODIVERSITY OFFICER SUBJECT: CONSERVATION REPORT 2018 – 2019 1. The attached report set out the outcomes achieved for this National Park through our conservation work during the financial year 2018-2019. 2. The report sets out: . The land management monitoring results for 2018 to 2019. Specific examples of achievements under the ‘Conserving the Park’ scheme . Progress made on the management of Pembrokeshire Coast National Park Authority owned sites . A report on partnership projects and collaboration . Stitch in Time progress . Species monitoring results and interpretation 3. The report illustrates the substantial amount of work the Authority undertakes across a range of activities. The main contributors internally are the officers in Park Direction, the Warden Teams and the Ranger Service. RECOMMENDATION: Members are requested to RECEIVE and COMMENT on the Report. (For further information contact Sarah Mellor on extension 4829) Pembrokeshire Coast National Park Operational Review Committee – 25th Sept 2019 Page 9 Page 10 Conservation Report 2018 to 2019 Pembrokeshire Coast National Park Authority Operational Review Committee 25th September 2019 Page 11 Contents 1. Conservation Land Management 3 2. Collaboration and Joint Projects 12 3. Species Monitoring 14 Appendix 1 - Conservation Land 16 Management Sites – Monitoring Methodology Appendix 2 ‘Conserving the Park’ Scheme 19 2 Page 12 1. Conservation Land Management 1. As part of Pembrokeshire Coast National Park Authority’s -

THE NEWS of DINAS 1894 – 1900 Transcribed from the COUNTY ECHO

THE NEWS OF DINAS 1894 – 1900 transcribed from THE COUNTY ECHO DINAS HISTORY SERIES his book is a transcription of all the Dinas news items from The County Echo, a Fishguard-based newspaper, for the years 1894, Twhen the newspaper commenced publication, to 1900 inclusive. The content is remarkable for its comprehensive coverage of village life. The correspondent(s), perhaps unwittingly, produced a social history of Dinas in the last seven years of the nineteenth century, one which almost reads, without editorial help, as a connected narrative. A picture emerges of a lively, sometimes controversial, but confident community in the far-south-western fringe of Wales at the very end of the Victorian era. The way of life recorded is both rural and truly parochial, but always tempered with the globe-trotting adventures and tragedies of the many sailors and master mariners from the village. This was still the age of the horse and cart, with bicycles being a novelty. Chapel and church life, along with deferential accounts of the clergy involved, inevitably take a prominent part in the narrative as do the fulsome accounts of funerals and tragedies; however, social innovation in the form of a Regatta in 1899 is proudly recorded. The Temperance Movement, so vitally important at the turn of the century, is faithfully described in its manifestations from hayfield to chapel. The text is presented without editing or alteration, variable spellings and local usage being preserved; where some doubt exists over the original, then the editorial convention of square brackets is used. Only one comment is made and that to explain a deliberate policy of concealment by the correspondent. -

2011 No. 683 (W.101) LLYWODRAETH LEOL, LOCAL GOVERNMENT, CYMRU WALES

OFFERYNNAU STATUDOL WELSH STATUTORY CYMRU INSTRUMENTS 2011 Rhif 683 (Cy.101) 2011 No. 683 (W.101) LLYWODRAETH LEOL, LOCAL GOVERNMENT, CYMRU WALES Gorchymyn Sir Benfro The Pembrokeshire (Communities) (Cymunedau) 2011 Order 2011 NODYN ESBONIADOL EXPLANATORY NOTE (Nid yw'r nodyn hwn yn rhan o'r Gorchymyn) (This note is not part of the Order) Mae'r Gorchymyn hwn wedi'i wneud yn unol ag This Order is made in accordance with section 58(2) adran 58(2) o Ddeddf Llywodraeth Leol 1972. Mae'n of the Local Government Act 1972. It gives effect to rhoi effaith i gynigion gan y Comisiwn Ffiniau proposals of the Local Government Boundary Llywodraeth Leol i Gymru ("y Comisiwn") a Commission for Wales ("the Commission") which gyflwynodd adroddiad ym mis Ebrill 2010 ar ei reported in April 2010 on its review of community adolygiad o ffiniau cymunedol yn Sir Benfro. Yr oedd boundaries in the County of Pembrokeshire. The adroddiad y Comisiwn yn argymell newid ffiniau Commission's report recommended changes to cymunedau yn Sir Benfro a newidiadau canlyniadol i'r community boundaries in the County of Pembrokeshire trefniadau etholiadol. and consequential changes to electoral arrangements. Mae'r Gorchymyn hwn yn rhoi eu heffaith i This Order gives effect to the Commission’s argymhellion y Comisiwn gydag addasiadau. recommendations with modifications. Mae printiau o'r mapiau sy'n dangos y ffiniau wedi'u Prints of the maps showing the boundaries are hadneuo a gellir eu harchwilio yn ystod oriau swyddfa deposited and may be inspected during normal office arferol yn swyddfeydd Cyngor Sir Penfro yn Neuadd y hours at the offices of Pembrokeshire County Council Sir, Hwlffordd, SA61 1TP ac yn swyddfeydd at County Hall, Haverfordwest, SA61 1TP and at the Llywodraeth Cynulliad Cymru ym Mharc Cathays, offices of the Welsh Assembly Government at Cathays Caerdydd CF10 3NQ (yr Is-adran Polisi Llywodraeth Park, Cardiff CF10 3NQ (Local Government Policy Leol). -

Coastal Cottages 2019 Collection

COASTAL COTTAGES 2019 COLLECTION PEMBROKESHIRE CEREDIGION CARMARTHENSHIRE Contents 2 Welcome 4 Places 6 Explore The Park 8 Beach Life 10 Child Friendly Holidays 12 Pet Friendly Holidays 14 Pembrokeshire In Four Seasons 16 Spring 18 Summer 20 Autumn 22 Winter 24 Go Wild In The West 26 Coastal Concierge 30 Waterwynch House 32 North Pembrokeshire 70 North West Pembrokeshire 108 West Pembrokeshire 160 South Pembrokeshire & Carmarthen 236 FAQ’s 238 Insurance & Booking Conditions 241 Here to Help Guide Welcome to the Coastal Cottages 2019 collection. As always, we have the very best properties of Pembrokeshire, Carmarthenshire and Ceredigion, all set in breathtaking locations along the coast, throughout the National Park and Welsh countryside. Providing memories #TheCoastalWay For almost 40 years we have been providing unique and traditional cottage holidays throughout West Wales for generations of guests. In this time we have grown but we still devote the same personal care, attention to detail and time to each of our guests as we did when we launched with just a hand full of properties back in 1982. What sets us apart from your everyday online only operator is our team and their personal knowledge. We all live right here in Pembrokeshire. We walk the beaches and hills, eat in the restaurants, enjoy the area with our children and pets and know the best places to explore whatever the weather. The Coastal Concierge team are always looking for the latest “Pembrokeshire thing” whether it’s local farmers launching a new dairy ice cream or the latest beachside pop up restaurant. Rest assured that if you stay with us, you will have an unrivalled experience from the moment you pick up the phone .