Federal Student Loan Programs Data Book

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Types of Federal Student Aid 2021-2022

FAFSA Is Used to Determine Eligibility For These Programs Grants Program and Type of Aid Eligibility and Program Information Annual Award Amounts (subject to change) For undergraduates with financial need who have not earned bachelor's or professional degrees. Federal Pell Grant Amounts change annually Does not have to be repaid Visit studentaid.ed.gov/pell‐grant for more information A student can receive Pell for no more than 12 semesters or the equivalent. Federal Supplemental Educational Opportunity Grant Up to $4000, but varies with the school. For undergradates with exceptional financial need. Pell Grant recipients take priority. Schools may have limited funds. (FSEOG) Visit studentaid.gov/fseog for more information Does not have to be repaid For students who are not Pell‐eligible due to expected family contribution calculations whose parent or guardian died as a result of Amount can be up to the annual Pell Grant amount, but Iraq and Afghanistan Service military service in Iraq or Afghanistan after the events of 9/11. cannot exceeds the school's cost of attendance. Grant Visit studentaid.gov/iraq‐afghanistan for more Does not have to be repaid A student can receive this grant for nore more than 12 semesters or the equivalent information Teacher Education Assistance for College and Higher Education (TEACH) Grant For undergraduate, postbaccalaureate, and graduate students who are completing or plan to complete course work needed to begin a Does not have to be repaid career in teaching. As a condition of this grant, a student must sign a TEACH Grant Agreement to Serve. Up to $4000 unless converted to a Direct Visit studentaid.gov/teach for more information Unsubsidized Loan for failure to Check with school to determine what educational levels can apply. -

In Re: Fleetboston Financial Corporation Securities Litigation 02-CV

Case 2:02-cv-04561-GEB-MCA Document 28 Filed 04/23/2004 Page 1 of 36 NOT FOR PUBLICATION UNITED STATES DISTRICT COURT FOR THE DISTRICT OF NEW JERSEY Civ. No. 02-4561 (WGB) IN RE FLEETBOSTON FINANCIAL CORPORATION SECURITIES LITIGATION O P I N I O N APPEARANCES: Gary S. Graifman, Esq. Benjamin Benson, Esq. KANTROWITZ, GOLDHAMER & GRAIFMAN 210 Summit Avenue Montvale, New Jersey 07645 Liaison Counsel for Plaintiffs Samuel H. Rudman, Esq. CAULEY GELLER BOWMAN & COATES, LLP 200 Broadhollow Road, Suite 406 Melville, NY 11747 Co-Lead Counsel for Plaintiffs Joseph H. Weiss, Esq. WEISS & YOURMAN 551 Fifth Avenue, Suite 1600 New York, New York 10176 Co-Lead Counsel for Plaintiffs Jules Brody, Esq. Howard T. Longman, Esq. STULL, STULL & BRODY 6 East 45 th Street New York, New York 10017 Co-Lead Counsel for Plaintiffs 1 Case 2:02-cv-04561-GEB-MCA Document 28 Filed 04/23/2004 Page 2 of 36 David M. Meisels, Esq. HERRICK, FEINSTEIN LLP 2 Penn Plaza Newark, NJ 07105-2245 Mitchell Lowenthal, Esq. Jeffrey Rosenthal, Esq. CLEARY, GOTTLIEB, STEEN & HAMILTON One Liberty Plaza New York, NY 10006 Attorneys for Defendants BASSLER, DISTRICT JUDGE: This is a putative securities class action brought on behalf of all persons or entities except Defendants, who exchanged shares of Summit Bancorp (“Summit”) common stock for shares of FleetBoston Financial Corporation (“FBF”) common stock in connection with the merger between FBF and Summit. Defendants FBF and the individual Defendants 1 (collectively “Defendants”) move to dismiss Plaintiffs’ Consolidated Amended Complaint (“the Amended Complaint”) pursuant to Federal Rule of Civil Procedure Rule 12(b)(6). -

Corporations with Matching Gift Programs

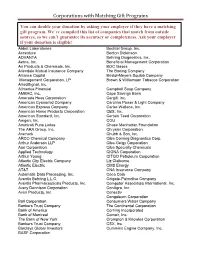

Corporations with Matching Gift Programs You can double your donation by asking your employer if they have a matching gift program. We’ve compiled this list of companies that match from outside sources, so we can’t guarantee its accuracy or completeness. Ask your employer if your donation is eligible! Abbot Laboratories Bechtel Group, Inc. Accenture Becton Dickinson ADVANTA Behring Diagnostics, Inc. Aetna, Inc. Beneficial Management Corporation Air Products & Chemicals, Inc. BOC Gases Allendale Mutual Insurance Company The Boeing Company Alliance Capital Bristol-Meyers Squibb Company Management Corporation, LP Brown & Williamson Tobacco Corporation AlliedSignal, Inc. Allmerica Financial Campbell Soup Company AMBAC, Inc. Cape Savings Bank Amerada Hess Corporation Cargill, Inc. American Cyanamid Company Carolina Power & Light Company American Express Company Carter-Wallace, Inc. American Home Products Corporation CBS, Inc. American Standard, Inc. Certain Teed Corporation Amgen, Inc. CGU Ammirati Puris Lintas Chase Manhattan Foundation The ARA Group, Inc. Chrysler Corporation Aramark Chubb & Son, Inc. ARCO Chemical Company Ciba Corning Diagnostics Corp. Arthur Anderson LLP Ciba-Geigy Corporation Aon Corporation Ciba Specialty Chemicals Applied Technology CIGNA Corporation Arthur Young CITGO Petroleum Corporation Atlantic City Electric Company Liz Claiborne Atlantic Electric CMS Energy AT&T CNA Insurance Company Automatic Data Processing, Inc. Coca Cola Aventis Behring L.L.C. Colgate-Palmolive Company Aventis Pharmaceuticals Products, Inc. Computer Associates International, Inc. Avery Dennison Corporation ConAgra, Inc. Avon Products, Inc. Conectiv Congoleum Corporation Ball Corporation Consumers Water Company Bankers Trust Company The Continental Corporation Bank of America Corning Incorporated Bank of Montreal Comair, Inc. The Bank of New York Crompton & Knowles Corporation Bankers Trust Company CSX, Inc. -

Federal Reserve Bulletin December 1991

VOLUME 77 • NUMBER 12 • DECEMBER 1991 FEDERAL RESERVE BULLETIN BOARD OF GOVERNORS OF THE FEDERAL RESERVE SYSTEM, WASHINGTON, D.C. PUBLICATIONS COMMITTEE Joseph R. Coyne, Chairman • S. David Frost • Griffith L. Garwood • Donald L. Kohn • J. Virgil Mattingly, Jr. • Michael J. Prell • Edwin M. Truman The Federal Reserve Bulletin is issued monthly under the direction of the staff publications committee. This committee is responsible for opinions expressed except in official statements and signed articles. It is assisted by the Economic Editing Section headed by S. Ellen Dykes, the Graphics Center under the direction of Peter G. Thomas, and Publications Services supervised by Linda C. Kyles. Table of Contents 967 AN UPDATE ON THE FARM ECONOMY believes that more sweeping changes are premature at this time, before the Subcommit- The latter part of the 1980s was a relatively tee on Telecommunications and Finance of the prosperous time for farmers. In 1990, how- House Committee on Energy and Commerce, ever, prices fell sharply in some parts of the October 25, 1991. farm economy, and in 1991, weakness in the sector has become more widespread. A soften- ing of the farm economy perhaps rekindles 992 ANNOUNCEMENTS memories of the farm financial stresses of the Final modifications of risk-based capital first half of the 1980s. But overall, imbalances guidelines. in the sector are far less pronounced than those of the early 1980s, and its vulnerability to Fee schedules of the Federal Reserve Banks financial setback has been reduced. for 1992. Publication of the revised Lists of Marginable 980 INDUSTRIAL PRODUCTION AND CAPACITY OTC Stocks and of Foreign Margin Stocks. -

School of Economics & Business Administration Master of Science in Management “MERGERS and ACQUISITIONS in the GREEK BANKI

School of Economics & Business Administration Master of Science in Management “MERGERS AND ACQUISITIONS IN THE GREEK BANKING SECTOR.” Panolis Dimitrios 1102100134 Teti Kondyliana Iliana 1102100002 30th September 2010 Acknowledgements We would like to thank our families for their continuous economic and psychological support and our colleagues in EFG Eurobank Ergasias Bank and Marfin Egnatia Bank for their noteworthy contribution to our research. Last but not least, we would like to thank our academic advisor Dr. Lida Kyrgidou, for her significant assistance and contribution. Panolis Dimitrios Teti Kondyliana Iliana ii Abstract M&As is a phenomenon that first appeared in the beginning of the 20th century, increased during the first decade of the 21st century and is expected to expand in the foreseeable future. The current global crisis is one of the most determining factors affecting M&As‟ expansion. The scope of this dissertation is to examine the M&As that occurred in the Greek banking context, focusing primarily on the managerial dimension associated with the phenomenon, taking employees‟ perspective with regard to M&As into consideration. Two of the largest banks in Greece, EFG EUROBANK ERGASIAS and MARFIN EGNATIA BANK, which have both experienced M&As, serve as the platform for the current study. Our results generate important theoretical and managerial implications and contribute to the applicability of the phenomenon, while providing insight with regard to M&As‟ future within the next years. Keywords: Mergers &Acquisitions, Greek banking sector iii Contents 1. Introduction ................................................................................................................ 1 2. Literature Review .......................................................................................................... 4 2.1 Streams of Research in M&As ................................................................................ 4 2.1.1 The Effect of M&As on banks‟ performance .................................................. -

January 17, 2011 Ms. Monica Jackson Office of the Executive Secretary

January 17, 2011 Ms. Monica Jackson Office of the Executive Secretary Consumer Financial Protection Bureau 1500 Pennsylvania Ave., NW (Attn: 1801 L Street) Washington, DC 20220 (sent via email to: [email protected]) Dear Ms. Jackson: These comments are in response to the “Request for Information Regarding Private Education Loans and Private Educational Lenders” (FR Doc. 2011–29737, Docket No. CFPB–2011–0037). We appreciate the opportunity to comment as the Consumer Financial Protection Bureau (Bureau) prepares its report on these topics, as required by Section 1077 of the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010. The Institute for College Access & Success (TICAS) is an independent, nonpartisan, nonprofit research and policy organization working to improve both educational opportunity and outcomes so that more underrepresented students complete meaningful post-secondary credentials and do so without incurring burdensome debt. Our Project on Student Debt, launched in 2005, focuses on increasing public understanding of rising student debt – including private student loan debt – and the implications for individuals, families, the economy and society. Publicly available data provide a troubling, but incomplete, picture of the private education lending market in the United States and its impact on students and families. The Bureau’s study represents an important opportunity to improve public understanding of what is at stake for consumers at all stages of the private loan process. We believe the information gathered and analyzed by this study will underscore the need for the Bureau to work with the Department of Education, Congress, colleges and others to strengthen consumer protections and provide consumers with the information they need to make sound decisions about how to pay for college. -

The MPN and the Stafford/PLUS Loan Process

VOLUME 4 Processing Aid & Managing FSA Funds Chapter 1: The MPN & the Stafford/PLUS Loan Process...... 4-1 STUDENT APPLIES FOR AID & COMPLETES THE MPN ................................................................................. 4-1 Required borrower information on MPN, Multiyear use of the MPN & when a new MPN is required PLUS MPN ................................................................................................................................................................. 4-6 PLUS certification specifying amount to be borrowed, Adverse credit history & use of endorser SCHOOL CERTIFIES/ORIGINATES LOAN ........................................................................................................... 4-7 Certifying eligibility, Submission of award & disbursement data (Direct Loans), Scheduling disbursements with an FFEL lender, Lender/guarantor approval (FFEL only), Review of the Stafford MPN process Chapter 2: Disbursing FSA Funds........................................... 4-13 NOTIFICATION OF DISBURSEMENT ................................................................................................................ 4-13 REQUIRED STUDENT/PARENT AUTHORIZATION ....................................................................................... 4-15 USING ELECTRONIC PROCESSES FOR AUTHORIZATIONS & NOTIFICATIONS .................................... 4-17 The E-Sign Act METHOD OF DISBURSEMENT ......................................................................................................................... -

HB Chapter 3

a a a a a a a a a a a a aaa a a aaa a aa aa a a a The Case Study Worksheets WITHDRAWAL RECORD (WR) Completed properly when a student withdraws, this document provides all the data needed to calculated refunds and repayments REFUND CALCULATION and organizes it so that it's easy to use. WORKSHEET WITHDRAWAL RECORD Completed using the figures from the a a a a a a a a a 1. Studenta a Informationa aaa a a aaa a aa aa a a a WR, this Worksheet calculates unpaid Name Start Date Withdrawal Date/LDA Social Security Number Length of Enrollment Period Date of WD/LDA Determination charges and refunds, and can be used a a a a a a a a a a a a USE TOTALS FOR PERIOD aaa a a aaa a aa aa a a a 2. Program Costs CHARGED* for nonpro rata refund policies (except non- non- inst. inst. inst. inst. TOTAL Tuition/Fees Personal/Living Inst. Costs: the Federal Refund Calculation. Administrative Fee Dependent Care A Room & Board Disability Costs TOTAL Noninst. Costs: Books & Supplies Miscellaneous REFUND CALCULATION WORKSHEET a a a a a a a a a a a a a a a B a aa a a a a a a a a a a a a a aa aa a a a Transportation Miscellaneous a aa aa a a a aaaa a a a a a aa a a a a a aaa a a a a a a a a a a a a TOTAL Aid Paid Total Institutional Costs a a a a a a a aa a a a a aa aa a a a a a 3. -

Stafford/PLUS Loan Periods and Amounts

CHAPTER Stafford/PLUS Loan 5 Periods and Amounts The rules for awarding Stafford and PLUS Loans are different than for Pell Grants and other FSA programs. Annual loan limits vary by grade level, and there are aggregate limits on the total amount that may be borrowed at one time. Also, the loan period, payment period, and the disbursements within that period may not always correspond to the payment periods that you’re using for Pell Grants. Finally, the requirement to prorate Stafford loan limits is different than the requirements for calculating Pell Grants. CHAPTER 5 HIGHLIGHTS: To request Stafford or PLUS Loan funds for a student, a school must n Measurements of academic and loan certify that the borrower is eligible for the loan award, and must provide periods specific amounts and dates for each disbursement of the loan award. ➔ Loan periods, academic terms, & program length A borrower’s eligibility for a Stafford or PLUS Loan is calculated ➔ Scheduled Academic Year (SAY) may differently than for a Pell Grant. There are no fixed tables such as the Pell be used for credit-hour programs with standard terms and certain nonstandard Grant Payment and Disbursement Schedules that determine award amounts. term programs Stafford Loans have annual and aggregate limits that are the same for all ➔ Borrower-Based Academic Year (BBAY) students at a given grade level and dependency status. In general, you may may be used as an alternative to an SAY for not originate a loan for more than the: programs also offered in an SAY ➔ BBAY must be used for clock-hour, nonterm, and nonstandard-term programs, • amount the borrower requests, and for standard-term credit-hour programs • borrower’s cost of attendance (see Chapter 2), without an SAY • borrower’s maximum borrowing limit as described in this ➔ “SE9W” (a program with terms substantially equal in length, with each chapter), or term comprised of 9 or more weeks of • borrower’s unmet financial need (as determined using the rules instructional time) in Chapter 7 of this volume). -

Westminster College FAMILY GUIDE to FINANCIAL AID

Westminster College FAMILY GUIDE TO FINANCIAL AID 1 FAMILY GUIDE TO FINANCIAL AID CONTENTS STEPS TO APPLY 3 Step-by-step Guidelines School Code: 002523 WE'RE HERE TO HELP 4 Aimee Bristow Sandra Coffman Teresa White IMPORTANT DATES 5 Visit Days SOAR Move-In Week First day of Classes ACADEMIC SCHOLARSHIPS 7 Freshman Merit-Based The Robert G. Muehlhauser Award of Excellence Transfer Merit-Based Other Westminster Awards/Aid Outside Scholarship Opportunities Participation Scholarships GRANTS Federal Grants 9 Missouri Grants LOANS 10 Federal Loans Federal Aid Programs Total Cost of Attendance Payment Policies Notes 19 WHAT SETS WESTMINSTER APART 2 FAMILY GUIDE TO FINANCIAL AID Guideline for Financial Aid It’s the goal of our financial aid office to make Westminster affordable for everyone. Every year we award more than $10.5 million in institutional aid to talented, hard-working students. There are four main types of financial aid available: scholarships, grants, loans, and work-study programs. Financial aid packages generally include a blend of these aid types and are awarded based on merit and/or need. Each student’s award package is based on a number of factors. One of the most important is the Free Application for Federal Student Aid (FAFSA). All students who wish to be considered for need-based financial aid must complete the FAFSA, which helps us understand students’ level of need and determine eligibility for federal grants, loans, and work-study programs. SO, NOW WHAT? 1. Apply for Admission to Westminster WCMO.edu/Apply 2. Once accepted, apply for an FSAID at fsaid.ed.gov Both student and parent will need an ID as they are used to electronically sign your FAFSA and other financial aid online documents. -

Federal Student Loan Amounts and Terms for Loans Issued in 2021-22

FEDERAL STUDENT LOAN AMOUNTS AND TERMS FOR LOANS ISSUED IN 2021-22 This chart summarizes the interest rates, loan limits, and other terms for federal student loans issued from July 1, 2021 through June 30, 2022. U.S. citizens or permanent residents, enrolled at least half time in a qualified program at a participating school, not in Basic Eligibility default on a prior federal student loan, and not previously convicted of a drug offense while receiving federal financial aid. Requirements Total aid, including student loans, cannot exceed the school’s total cost of attendance (tuition and fees, room and board, transportation, personal and miscellaneous expenses). FAFSA required. Subsidized Stafford Loan: Available only to undergraduate students on the basis of financial need. No credit check required. The federal government covers the interest on these loans while borrowers are enrolled at least half time and for six months after they are no longer enrolled at Types least half time. Monthly payments are not required until six months after leaving school. Unsubsidized Stafford Loan: Available to undergraduate and graduate students regardless of financial need. No credit check required. Interest is charged throughout the life of the loan. Monthly payments are not required until six months after leaving school. Dependent undergraduates (most students under the age of 24): $5,500 as freshmen (including up to $3,500 subsidized); $6,500 as sophomores (including up to $4,500 subsidized); $7,500 as juniors and seniors (including up to $5,500 subsidized). Independent undergraduates (students age 24 or older) and dependent students whose Annual Loan Limits parents are unable to obtain PLUS Loans: $9,500 as freshmen (including up to $3,500 subsidized); $10,500 as sophomores (including up to $4,500 subsidized); $12,500 as juniors and seniors (including up to $5,500 subsidized). -

IN-SCHOOL DEFERMENT REQUEST OMB No

IN-SCHOOL DEFERMENT REQUEST OMB No. 1845-0011 Form Approved William D. Ford Federal Direct Loan (Direct Loan) Program / Federal Family Exp. Date 8/31/2021 Education Loan (FFEL) Program / Federal Perkins Loan (Perkins Loan) Program WARNING: Any person who knowingly makes a false statement or misrepresentation on this form or on SCH any accompanying document is subject to penalties that may include fines, imprisonment, or both, under the U.S. Criminal Code and 20 U.S.C. 1097. SECTION 1: BORROWER INFORMATION Please enter or correct the following information. Check this box if any of your information has changed. SSN Name Address City State Zip Code Telephone - Primary Telephone - Alternate Email (Optional) SECTION 2: BORROWER DETERMINATION OF DEFERMENT ELIGIBILITY Carefully read the entire form before completing it. You are eligible for this deferment only if you are enrolled at least half time at an eligible school (see Section 6). SECTION 3: BORROWER REQUESTS, UNDERSTANDINGS, CERTIFICATIONS, AND AUTHORIZATION I request: • To defer repayment of my loans for the period during which I meet the eligibility criteria outlined in Section 2 and as certified by the authorized official in Section 4. • If checked, to make interest payments on my loans during my deferment. • If checked, to defer repayment on my PLUS Loan first disbursed on or after July 1, 2008 for the 6-month period after I graduate, withdraw, or am no longer enrolled on at least a half-time basis. I understand that: • I am not required to make payments of loan principal or interest during my deferment. • My deferment will begin, as certified by the authorized official, on the date I became eligible for the deferment.