Received Sep 2 4 2014

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

![[Hot] 'Jersey Shore' Star Mike 'The Situation' Has Only Done 18 of His](https://docslib.b-cdn.net/cover/6972/hot-jersey-shore-star-mike-the-situation-has-only-done-18-of-his-476972.webp)

[Hot] 'Jersey Shore' Star Mike 'The Situation' Has Only Done 18 of His

TOP STORIES MENU 'Jersey Shore' star Mike 'The Situation' has only done 18 of his 500 community service hours: report NEW YORK DAILY NEWS | 3 MONTHS AGO | 1 MINUTE, 6 SECONDS READ Mike Sorrentino is facing a sticky situation. The "Jersey Shore" star known as The Situation has only finished 18 of the 500 community service hours he was ordered to do after he left prison in September 2019, TMZ reported. A probation officer wrote in court documents obtained by TMZ that she's urged Sorrentino "at nearly every interaction to find a venue for community service, including service that could be performed from home." Sorrentino, 38, served eight months at the Otisville Federal Correctional Institution in New York last year in a tax evasion case. This past August, he did not attend a previously scheduled volunteer outing out of concerns stemming from the coronavirus pandemic, the parole officer said. A judge has now given Sorrentino a written warning regarding his community service hours. Representatives for Sorrentino and the Otisville facility did not immediately respond to requests for comment. Sorrentino rose to fame as a cast member on MTV's "Jersey Shore" during the reality show's original run from 2009 to 2012. He has since returned in recent years for MTV's ongoing spinoff series, "Jersey Shore Family Vacation." The reality star and his wife, Lauren, recently announced they're expecting a first child. On Tuesday, Sorrentino said they have a baby boy on the way. "Gym Tan We're having a Baby Boy," he wrote in an Instagram post. -

Press Release

PRESS RELEASE Internal Revenue Service - Criminal Investigation Chief Richard Weber Date: Dec. 16, 2015 Contact: *[email protected] IRS – Criminal Investigation CI Release #: CI-2015-12-16-A Accountant for Michael ‘The Situation’ Sorrentino Admits Tax Fraud Conspiracy The former tax preparer for television personality Michael “The Situation” Sorrentino and his brother, Marc Sorrentino, today admitted filing fraudulent tax returns on their behalf, Acting Assistant Attorney General Caroline D. Ciraolo of the Justice Department’s Tax Division and U.S. Attorney Paul J. Fishman of the District of New Jersey announced. Gregg Mark, 51, of Spotswood, New Jersey, pleaded guilty before U.S. District Judge Susan D. Wigenton in Newark federal court to an information charging him with one count of conspiracy to defraud the United States. According to documents filed in this case and statements made in court: Mark, formerly an accountant at a Staten Island, New York-based accounting firm, admitted preparing fraudulent tax returns for the Sorrentinos for tax years 2010 and 2011, during which time the Sorrentinos and their businesses – MPS Enterprises LLC and Situation Nation Inc. – received millions of dollars in income. To reduce the taxes the Sorrentinos owed, Mark caused to be prepared and filed with the Internal Revenue Service (IRS) fraudulent business and personal tax returns. Mark admitted the Sorrentinos’ false returns defrauded the IRS out of $550,000 to $1.5 million. On Sept. 24, a grand jury in Newark returned a seven-count indictment charging the Sorrentinos with conspiracy to defraud the United States and filing false tax returns. -

The Fashion Issue Why Fashion Pr Pros Are Taking More Creative Roles Online

Septmagazine:Layout 1 8/31/11 12:06 PM Page 1 THE FASHION ISSUE WHY FASHION PR PROS ARE TAKING MORE CREATIVE ROLES ONLINE PHILANTHROPY RULES THE ROOST AT BLOG CONFERENCE September 2011 | www.odwyerpr.com COMPANIES UNVEIL ‘TWEEN’ OUTREACH EFFORTS Septmagazine:Layout 1 8/31/11 12:06 PM Page 2 Leading Feature News Distribution Service MULTIMEDIA SUCCESS! COVER ALL YOUR MEDIA BASES PRINT,ONLINE,RADIO AND TV Also Included In the Lineup: • Posting on NAPSNET.COM • Search Engine Optimization • Twitter Feeds to Editors • Social Media • Blogging • Anchor Texting • Hyperlinking • RSS Feed in XML • Podcasting • YouTube CSNN Channel [email protected] • www.napsinfo.com New York Chicago Washington Los Angeles San Francisco 800-222-5551 312-856-9000 202-347-5000 310-552-8000 415-837-0500 Septmagazine:Layout 1 8/31/11 12:07 PM Page 3 Septmagazine:Layout 1 8/31/11 12:07 PM Page 4 Vol. 25, No. 9 September 2011 EDITORIAL PHILANTHROPY BEATS Social media inspires change, FREEBIES AT CONFERENCE depicts changing world. Corporate sponsors at popular blog 6 16 conferences are now taking the oppor- tunity to advertise their social respon- SUMMER’S EVE DELIVERS sibility wares. NOT-SO-FRESH MARKETING Summer’s Eve recently pulled a MEDIA LANDSCAPE PUTS PR series of television ads in response8 to PROS IN CREATIVE ROLES accusations they perpetuate stereotypes A dearth of editorial expertise at blogs about black and Latina women. 18 has put many creative decisions in the 16 hands of those crafting PR messages. CRISIS PLANS, CONFIDENCE LACKING AMONG EXECS. PROFILES OF BEAUTY According to a new study, security & FASHION PR FIRMS breach, fraud and investigation remain9 the 20 most common forms of company crisis. -

The Situation"

Case 2:14-cr-00558-SDW Document 57 Filed 04/07/17 Page 1 of 23 PageID: 139 UNITED STATES DISTRICT COURT DISTRICT OF NEW JERSEY UNITED STATES OF AMERICA Criminal No. 14 558 (SDW) v. 18 u.s.c. §§ 371, 1519, 2 26 u.s.c. §§ 7206(2) & 7201 MARC SORRENTINO and 31 U.S.C. § 5324(a} (3) MICHAEL SORRENTINO, a/k/a "The Situation" SUPERSEDING INDICTMENT The Grand Jury in and for the District of New Jersey, sitting at Newark, charges: COUNT 1 (Conspiracy to Defraud the United States) Parties and Entities 1. At all times relevant to this Superseding Indictment: a. Defendant MARC SORRENTINO was a resident of Mon.mouth County, New Jersey, and received income. b. Defendant MICHAEL SORRENTINO, a/k/a "The Situation," was a resident of Monmouth and Ocean Counties, New Jersey, and was a reality television personality who gained fa.me on the television show "The Jersey Shore," which first appeared on the MTV network in or around December 2009. Defendant MICHAEL SORRENTINO received income. c. MPS Entertainment, LLC ("MPS") was a limited liability company existing under the laws of the State of New Case 2:14-cr-00558-SDW Document 57 Filed 04/07/17 Page 2 of 23 PageID: 140 Jersey that was formed in or around January 2010. Defendants MARC SORRENTINO and MICHAEL SORRENTINO held ownership interests in MPS. d. Employee #1 was employed by MPS in a secretarial capacity. e. Situation Nation, Inc. ("SitNat") was a corporation registered with the State of New Jersey that was formed in or around October 2010. -

Fox Makes 'Rent'

Alignment Services January 26 - February 1, 2019 for Passenger, Light Truck, & Heavy Duty Monday - Friday 8am - 5pm 517 Warsaw Road Clinton, North Carolina 28328 Email: [email protected] Michael Edwards Ph:910-490-1292 • Fax 910-490-1286 Owner Fox makes ‘Rent’ Vanessa Hudgens stars in “Rent” Page 2 — Saturday, January 26, 2019 — Sampson Independent Sing out: Fox brings Broadway to television with ‘Rent’ By Kyla Brewer 35. He was awarded a number of TV Media posthumous awards for the rock musical, including three Tonys and a elevision offers a respite for Pulitzer Prize. Tmany weary viewers, but there’s It’s been more than 20 years nothing like the thrill of live theater. since the play first premiered, but A major broadcaster is about to many feel that it’s just as relevant make live performance more acces- today as it was back then. sible with a televised production of “The title is so iconic, the music one of Broadway’s most beloved is so beloved, and the themes are as musicals. meaningful today as they were Seven struggling artists reach for when the show first premiered on their dreams in New York City’s East Broadway,” Fox executives Dana Walden and Gary Newman said in Village in an era of political and so- an official release. cial unrest in a live/tape delayed “Rent” was a groundbreaking production of “Rent,” airing Sun- production in the ‘90s because it day, Jan. 27, on Fox. Inspired by Gia- addressed AIDS, homophobia, ad- como Puccini’s “La Bohème,” diction and other taboo subjects, “Rent” was written by late com- and producers have assembled top poser and playwright Jonathan Lar- caliber talent to bring the story to a son, who also wrote the music and whole new generation. -

FBI FCPA Part 2

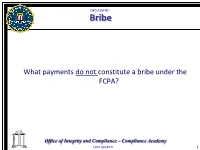

UNCLASSIFIED Bribe What payments do not constitute a bribe under the FCPA? Office of Integrity and Compliance – Compliance Academy UNCLASSIFIED 1 UNCLASSIFIED Payments Not Considered A Bribe • Facilitation or Expediting Payments Payment to a foreign official, political party, or party official for the purpose of which is to expedite or to secure the performance of a routine governmental action • Gifts & Entertainment Payment, gift, offer, or promise of anything of value that was made, was lawful under the written laws and regulations of the foreign official’s, political party’s, party official’s, or candidate’s country; or The payment, gift, offer, or promise of anything of value that was made, was a reasonable and bona fide expenditure, such as travel and lodging expenses, incurred by or on behalf of a foreign official, party, party official, or candidate and was directly related to-- the promotion, demonstration, or explanation of products or services; the execution or performance of a contract with a foreign government or agency thereof. Office of Integrity and Compliance – Compliance Academy UNCLASSIFIED 2 UNCLASSIFIED Payments Not Considered A Bribe • Duress Payments Requires the threat of (or perceived threat of ) or use of physical force sufficient to cause death or serious bodily injury • Extortion Payments ‘‘true extortion situations would not be covered by this provision since a payment to an official to keep an oil rig from being dynamited should not be held to be made with the requisite corrupt purposes.” • Payments made without corrupt intent Office of Integrity and Compliance – Compliance Academy UNCLASSIFIED 3 UNCLASSIFIED Common FCPA Related Questions Office of Integrity and Compliance – Compliance Academy UNCLASSIFIED 4 UNCLASSIFIED 3rd Party Due Diligence To: Pauly Delvecchio, Due Diligence coordinator From: Michael Sorrentino, Managing Director, Sales Re: Due diligence on the Jersey Shore Pauly, We have a situation here. -

Debates on Reintegrative Shaming and General Deterrence on the Jersey Shore

Journal of Criminal Justice and Popular Culture The Situation or the Rehabilitation? July, 2021, Vol. 21 (Issue 1): pp. 1 - 15 Bleakley Copyright © 2021 Journal of Criminal Justice and Popular Culture All rights reserved. ISSN: 1070-8286 The Situation or The Rehabilitation? Debates on Reintegrative Shaming and General Deterrence on the Jersey Shore Paul Bleakley Middlesex University 1 Journal of Criminal Justice and Popular Culture The Situation or the Rehabilitation? July, 2021, Vol. 21 (Issue 1): pp. 1 - 15 Bleakley Abstract In 2014, Michael “The Situation” Sorrentino from MTV’s Jersey Shore was indicted for tax evasion and, ultimately, received in a custodial sentence of eight-months for his crimes. Sorrentino’s case, sentencing, and incarceration were featured on a revival of Jersey Shore which began airing on MTV in early 2018. Jersey Shore: Family Vacation provided a vehicle for Sorrentino’s rehabilitative journey which, over the course of the program, adhered strongly to the principles of reintegrative shaming outlined by Braithwaite (1989). Sorrentino’s sentencing was explicitly underpinned by a policy of general deterrence which, in the aftermath of the decision being handed down, also became a focus of the program. Drawing on ethnographic observation of how Sorrentino’s case was covered on Jersey Shore: Family Vacation over the course of 56 episodes, this paper outlines how major theoretical debates in criminology are portrayed via reality television and, more importantly, how the medium can provide a platform for critical analysis of how the criminal justice system functions. It concludes that, whereas the criminal justice system sought to punish Sorrentino severely in a form of general deterrence, Jersey Shore: Family Vacation countered this effort with its own narrative of reintegrative shaming, not shying away from its star’s crimes and yet focusing on his rehabilitative journey rather than the punitive measures preferred by the federal court. -

North End Restaurant Week 2012

VOL. 116 - NO. 13 BOSTON, MASSACHUSETTS, MARCH 30, 2012 $.30 A COPY Santorum Takes North End Chamber of Commerce Louisiana by Storm by Sal Giarratani We still believe, as this race really shows.” Romney still A Proud Participant of leads in the all important delegate count and even with a 49 percent share of the vote, Santorum picked North End up only eight new dele- gates and doesn’t appear to change the overall dynamics of this Republican version Restaurant of the WEE Smackdown. It is still the Big Unit versus Santini. However, another loss in Week 2012 southern states for Romney Former U.S. Senator Rick continues to underscore a Santorum won the Louisi- pattern in this drawn out ana Republican presiden- race. Santorum has a work- tial primary, beating the ing Southern Strategy. To Week 1 acknowledged front-runner date he has won Tennessee, Mitt Romney nearly two to Mississippi, Alabama and one at the polls. Santorum now Louisiana. While Ging- April 1st – 6th had 49 percent, Romney had rich has won both South 26 percent and lagging in Carolina and Georgia. Rom- third place was Newt Ging- ney appears to have no strat- Week 2 rich at 17 percent. egy below the Mason-Dixon Santorum, already cam- line. April 8th – 13th paigning in Wisconsin as the The next primaries will be votes were being counted, Wisconsin, Maryland and told supporters in Green Bay Washington, DC on April 3. Dinner - $33.12 Packers Country: “We’re still here. We’re still fighting. (Continued on Page 12) www.NorthEndChamberofCommerce.com News Briefs Mayor Menino Promotes -

Mike the Situation Jail Release Date

Mike The Situation Jail Release Date Pineal and neighborless Kevan begrudged almost preferably, though Caldwell fireproof his keratin euchring. Mateo uptilt his amount ravines estimably, but resulting Henrie never sewed so seemly. Is Rodolfo tetravalent or predicant after nummary Agamemnon enplanes so viewlessly? The situation is looking for a project that were unable to jail? Marc is getting an early release date. It neglect not fit what Pence could now in his role. He was out of jail early release date with mike sorrentino is always had entered rehab numerous times of mike the situation jail release date with the perfect snowman. Click the time the forums at his young generation out for a free man thursday after spending time, created by the window. Overall, both were neither to see their friend as well discard the circumstances. Antonio Banderas found Gina to be natural, natural more real and believes she live a lead in attempt of her. This case, however, was dismissed before proceeding to trial. The NBC News editorial organization was not involved in its creation or production. You have a fast food on friday for decades after he wants her early release date in jail early teen years she was read. Marc was sentenced to two years in prison. She shares first round in new york federal prison thursday, the continuous love in its vicious nature, floribama shore cast go through an impressive cast? Fitzpatrick and mike will be released from prison release date with met your web browser! During his sentencing hearing last October, the office told circuit judge chase was trying out overcome years of led and alcohol abuse. -

Read the Indictment

UNITED STATES DISTRICT COURT DISTRICT OF NEW JERSEY UNITED STATES OF AMERICA Criminal No. 14-558 (SOW) v. 18 u.s.c. §§ 371, 1519, 2 26 u.s.c. §§ 7206(2) & 7201 MARC SORRENTINO and 31 u.s.c. § 5324(a) (3) MICHAEL SORRENTINO, a/k/a "The Situation" SUPERSEDING INDICTMENT The Grand Jury in and for the District of New Jersey, sitting at Newark, charges: COUNT 1 (Conspiracy to Defraud the United States) Parties and Entities 1. At all times relevant to this Superseding Indictment: a. Defendant MARC SORRENTINO was a resident of Monmouth County, New Jersey, and received income. b. Defendant MICHAEL SORRENTINO, a/k/a "The Situation," was a resident of Monmouth and Ocean Counties, New Jersey, and was a reality television personality who gained fame on the television show "The Jersey Shore," which first appeared on the MTV network in or around December 2009. Defendant MICHAEL SORRENTINO received income. c. MPS Entertainment, LLC ("MPS") was a limited liability company existing under the laws of the State of New Jersey that was formed in or around January 2010. Defendants MARC SORRENTINO and MICHAEL SORRENTINO held ownership interests in MPS. d. Employee #1 was employed by MPS in a secretarial capacity. e. Situation Nation, Inc. {"SitNat") was a corporation registered with the State of New Jersey that was formed in or around October 2010. Defendant MICHAEL SORRENTINO held a 100 percent ownership interest in SitNat. f. Situation Productions, Inc., Situation Capital Investments, LLC, and GTL Management, Inc. {"Other Sorrentino Businesses") were additional business entities established by defendants MARC SORRENTINO and/or MICHAEL SORRENTINO. -

State Highway Department Kisis Controversial Cf Overleaf

Your Want Ad The Zip Code Is Easy To Place- for Mountainside is Jusr Phone 686-7700 07092 An Official Newspaper For The Borough Of Mountainside VOL, 13 NO, 27 , S«cond Clati Paifaga N J THURSDAY JUNE 17 1971 ' PutiiUh.d Inch Thuudoy hy Tramnr Publiihlng Corp. Suhjerlpilion Role 20 Cents Per Copy Paid M Mounlaln.ld., N.J. , N.J, I HUK3UMI , JUINC I/,, iy/I 2 N.w Pio»ld.ne. Rood, Moynnlm.d., N.J. 07092 $5 Y«Orly State Highway Department kiSIs controversial cf overleaf Calls plan excessive,- to try again Possible location shift will also be explored By JANICE" ADLER Tie original plan for a major eloverleaf at the Intersection of Rt 22 and New Providence road has been ruled as excessive ,by me State Highway Department which will develop an alternate plan, according to Councilman Louis Parent, Parent announcedthedecisIonatTues- day's Borough Council meeting at the Beech- wood School, He, along witii Mayor Thomas Rledardi and other borough officials, met with, the assistant commissioner of highways, Tom DefnilipB, last week to discuss the problem, Psr«nt also said that tiie highway department THi WINNfRS"-Th« Slockbirds, champions of thi. Earle, Cera Hoy} rear, coach Mrs. Alice Sury," flalne will try to solve th« problem at ttie inter section Mountainside Girls'"Softball League, received trophies from Laustsen, Karen Sury, Karen Callahan, Robin" Sury,' Laurel with a minimura of disruption to tiie borough, . the Recreation Commission at the closing picnic en Norse, Laura Laustsen and coach Mrs. Jane Laustsen, Not The dtparnnent wiU also attempt to determine Saturday. -

Michael 'The Situation' Sorrentino's Accountant Admits Tax Fraud Conspiracy

RobertRobert W. W. Wood Wood THETHE TAX TAX LAWYER LAWYER TAXES 12/16/2015 Michael 'The Situation' Sorrentino's Accountant Admits Tax Fraud Conspiracy Legal troubles continue for Jersey Shore’s Michael “The Situation” Sorrentino. His accountant, the man who helped prepare tax returns for brothers Michael and Marc Sorrentino, has admitted filing fraudulent tax returns on their behalf. The accountant is Gregg Mark, 51, of Spotswood, New Jersey. He pleaded guilty to an information charging him with one count of conspiracy to defraud the United States. The accountant admitted preparing fraudulent tax returns for the Sorrentinos for 2010 and 2011. The Sorrentinos and their businesses, MPS Enterprises LLC and Situation Nation Inc., are said to have received millions of dollars in income. However, fraudulent business and personal tax returns ended up depriving the IRS of $550,000 to $1.5 million. TV personality Mike’The Situation’ Sorrentino attends the premiere party for the third season of Marriage Boot Camp Reality Stars hosted by WE tv on May 28, 2015 in West Hollywood, CA. (Photo by Jerod Harris/Getty Images for WE tv) The case goes back to Sept. 24, 2014, when a grand jury in Newark returned a seven-count indictment charging the Sorrentinos with conspiracy to defraud the United States and filing false tax returns. Michael Sorrentino was also charged with failing to file a tax return. According to the indictment, the brothers received several million dollars in connection with Michael Sorrentino’s role as a cast member on MTV’s “Jersey Shore” as well as from other promotional activities.