Complex Mortgages

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

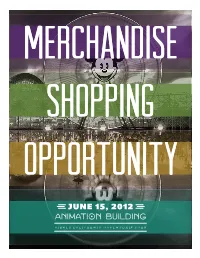

Animation Building June 15, 2012

MERCHandise Shopping opportunity JUNE 15, 2012 Anim Ation Building DISNEY CALIFORNIA ADventure® park © Disney/Pixar 3 7-11 12-1 6 ZONE1 commemorative dated collection 1 1 UNITED STATES POSTAL SERVICE POSTCARD CANCELLATION $3.95 Limit TWO (2) per Guest 2 2 BRONZE MAGNUM COIN Edition Size: 250 Dimensions: 2.5” diameter $75 Limit ONE (1) per Guest 4 3 EmbS OS ED WATCH $89.95 Limit ONE (1) per Guest 4 TumbER L $16.95 Limit TWO (2) per Guest BKAC 5 BA SEBALL CAP 5 $21.95 Limit TWO (2) per Guest FRONT 6 C ANVAS TOTE $34.95 Limit TWO (2) per Guest 6 7-11 L ADIES COMMEMORATIVE TEE $31.95 S (7), M (8), L (9), XL (10), XXL (11) Limit TWO (2) of each size per Guest 12-16 COMMEMORATIVE TEE (ADULT) $27.95 S (12), M (13), L (14), XL (15), XXL (16) Limit TWO (2) of each size per Guest 17 WALT & MICKEY “STORYTELLERS” STATUE Edition Size: 250 Dimensions: 91/4” H x 5” W x 3” D (with base) $195 17 Limit ONE (1) per Guest Paid admission is required to enter Disney Theme Parks. All events and information are subject to cancellation or change without notice including but not limited to dates, times, artwork, release dates, edition sizes and retails sizes. ©Disney/Pixar 1 5 ZONE2 PINS 1 “ I WAS THERE” – DISNEY CALIFORNIA ADVENTURE® PARK Edition size: 5,000 $13.95 Limit ONE (1) per Guest 2 “ I WAS THERE” – CARS LAND Edition Size: 2,000 $13.95 Limit ONE (1) per Guest 2 3 D ISNEY CALIFORNIA ADVENTURE® PARK COMMEMORATIVE Edition Size: 2,500 $13.95 6 Limit ONE (1) per Guest 4 WALT & MICKEY PORTRAIT Edition Size: 1,000 $15.95 Limit ONE (1) per Guest 5 WALT DEDICATION Edition Size: 2,000 $13.95 3 7 Limit ONE (1) per Guest 6 CDARS LAN GRAND OpENING Edition Size: 2,000 $13.95 Limit ONE (1) per Guest 7 R ADIATOR SPRING RACERS GRAND OpENING 8 Edition Size: 2,000 $11.95 Limit ONE (1) per Guest 8 Lu IGI’S FLYING TIRES G RAND OpENING Edition Size: 2,000 $11.95 4 Limit ONE (1) per Guest 9 9 MATER’S JUNKYARD JAMBOREE G RAND OpENING Edition Size: 2,000 $11.95 Limit ONE (1) per Guest Paid admission is required to enter Disney Theme Parks. -

OCF Disney BG 7375.Indd

DISNEYLAND RESORT EXPANSION questions for Disneyland President George A. Kalogridis 10We caught up with Disneyland Resort President George A. Kalogridis to get some insight into the thought behind this enormous expansion project, as well as some challenges and surprises over the last fi ve years. Here’s what he had to share. 1. Why did Disney make such a large investment to 6. You previously said that one of change Disney California Adventure? the things that had been missing from Disney Since opening in 2001, Disney California Adventure has California Adventure was nighttime entertainment? been the second most-visited theme park in the Western True. The park didn’t have a nighttime spectacular and United States, behind only Disneyland. Though many of World of Color has provided that one last memory as guests the highest-rated attractions are in California Adventure, leave our park. World of Color has entertained more than our guests told us they didn’t have the same emotional 5.5 million guests in just two years, and it has resulted in connection that they had to Disneyland. They wanted more increased park operating hours each evening… along with heart, more fantasy and more immersive experiences. sparking the addition of our nightly family dance parties. 2. How will you connect guests emotionally to Disney 7. What’s the concept behind the family dance parties? California Adventure? We created GlowFest to keep our guests engaged before As guests enter, they will be transported to the 1920s Los and after World of Color shows. We used the concept to Angeles that greeted Walt Disney when he arrived as a create ElecTRONica, a tribute to the movie TRON. -

What Would You Do If You Met a Fairy

Disney•Pixar’s CARS Blu-ray™ Fact Sheet Film Synopsis: From the acclaimed creators of Toy Story, The Incredibles and Finding Nemo comes Disney•Pixar’s Cars, a high-octane adventure comedy that shows life is about the journey, not the finish line. Enjoy this landmark classic on both Disney Blu-ray™ hi-def and DVD in this sensational 2-Disc Blu-ray Combo Pack releasing on April 12, 2011. Hotshot rookie race car Lightning McQueen (Owen Wilson) is living life in the fast lane until he hits a detour on the way to the most important race of his life. Stranded in Radiator Springs, a forgotten town on the old Route 66, he meets Sally (Bonnie Hunt), Mater (Larry The Cable Guy), Doc Hudson (Paul Newman), and a variety of quirky characters who help him discover that there’s more to life than trophies and fame. U.S. Release Date: April 12, 2011 (Direct Prebook: February 15; Distributor Prebook: March 2) Rating: “G” Feature Run Time: Approximately 117-minutes Release Format: Blu-ray Combo Pack (Blu-ray + DVD) Suggested Retail Pricing: 2-Disc Blu-ray Combo Pack = $39.99 U.S. / $44.99 Canada Bonus Features: Carfinder Game Deleted Scenes Mater and the Ghostlight Short Radiators Springs Featurettes One Man Band Short Inspiration for Cars Cine-Explore Voice Talent: Owen Wilson (Wedding Crashers, Little Fockers) as Lightning McQueen; Paul Newman (Road To Perdition, The Sting) as Doc Hudson; Bonnie Hunt (TV’s “The Bonnie Hunt Show,” The Green Mile) as Sally Carrera; Larry the Cable Guy (TV’s “Only in America with Larry the Cable Guy; Larry the Cable Guy: Health Inspection) as Mater; Cheech Marin (The Perfect Game; TV’s “Nash Bridges”) as Ramone; Tony Shalhoub (TV’s “Monk,” “Wings”) as Luigi; George Carlin (Dogma, Bill & Ted’s Excellent Adventure) as Fillmore; Michael Keaton (The Other Guys, Batman, Toy Story 3) as Chick Hicks; Mario Andretti (Champion Racecar Driver) as himself; Bob Costas (TV Sportscaster) as Bob Cutlass; Dale Earnhardt, Jr. -

Disney California Adventure® Park 1-Day Hopper Plan

PAGE 1 PAR K PLAN Disney California Adventure® Park 1-Day Hopper Plan Disneyland® Park is the first theme park Walt Disney created and remains heavy on the nostalgia — with classic rides such as Pirates of the Caribbean, Jungle Cruise and Mr. Toad’s Wild Ride. Disney California Adventure® Park is the place to find popular Disney, Pixar and super hero attractions such asGuardians of the Galaxy - Mission: BREAKOUT!, Radiator Springs Racers and Incredicoaster. With so many attractions, we recommend planning at least two days to explore the parks. Plan to arrive at least 30 to 45 minutes ahead of opening so you are one of the first to enter the park (arrive an hour and 30 minutes early to park if you are driving). We suggest visiting the highest priority rides in the morning when waits are lowest. During the initial reopening phase at Disneyland® Resort, some services or benefits may be temporarily unavailable, as well as other entertainment and experiences (such as traditional character greetings). However, as of July 4, 2021, Mickey’s Mix Magic is back! Single Rider lines for popular attractions have returned, character cavalcades are popping up and modified character dining experiences are slowly coming back toDisneyland ® Resort. Additional experiences and rides may also be modified or temporarily unavailable during this time. There are several things to take into consideration that could affect your park plan: • Your callback time for Star Wars: Rise of the Resistance or WEB SLINGERS: A Spider-Man Adventure • Virtual queues for other attractions (when in use) • If you have reservations for restaurants or experiences, such as Savi’s Workshop • Ride closures • Park hours/crowd levels • Weather • Your own personal interests and ages, heights and interests of children Disneyland® Park and Disney California Adventure® Park Single Rider Attractions: Single Rider lines are an excellent choice for those guests who don’t mind splitting up their party in exchange for a shorter wait time. -

American Indians & Route 66

American Indians & Route 66 AMERICAN INDIANS & ROUTE 66 | 01 ON OUR COVER: ‘SEEING THROUGH THE PATTERNS’ Geraldine Lozano is a conceptual artist based out of Brooklyn, New York. She works using photo, video performance, artist books, and public art in her practice. Her video installation work has been funded by the Creative Work Fund and the Zellerbach Foundation of San Francisco, California. Lozano’s public art can be seen in the architecturally integrated art of eco-resin screens set into the bus shelters of BRIO, Sun Metro’s new rapid transit system. Gera, as she as also known in the street art world, creates femenine artwork that is conscious and provocative. Her studio work and public art work reflect the spirit of culture and dreams. – www.geralozano.com American Indians & Route 66 AMERICAN INDIANS & ROUTE 66 | 01 MAP KEY Route 66 American Indian Reservation Tribal Jurisdictions (Oklahoma) Trust Land ABOUT THIS MAP Route 66 cartography provided by Pueblo of Sandia GIS Program, Pueblo of Sandia, Bernalillo, New Mexico Route 66 historic alignment information derived from National Park Service data and Rick Martin’s online resource, http://route66map. publishpath.com/ Tribal land status and base mapping provided by Bureau of Indian Affairs Office of Trust Services Division of Water and Power DID DIDYOU YOUKNOW? KNOW? DID YOU KNOW? INTRODUCTION AMERICAN INDIANS AND ROUTE 66 Route 66 was an officially commissioned highway from 1926 Route 66 begins in Grant Park, Chicago—or ends there— to 1985. During its lifetime, the road guided travelers through depending on which direction you’re traveling. At the intersection the lands of more than 25 tribal nations. -

Guide for Guests with Disabilities

GUIDE FOR MOBILITY VISUAL HEARING TIPS AND INFORMATION ACCESSIBILITY AND MOBILITY GUESTS WITH Disabilities Disabilities Disabilities Courtesy Wheelchairs Complimentary Dining and Shopping Locations DISABILITIES Guest Amenities Wheelchairs and Electric Conveyance Vehicles (ECVs) Braille Guides Printed in Braille and large print text Assistive Listening Utilizes Disney’s Handheld wheelchairs are available for travel to and from Some counter-service and merchandise Available for Rent available for rent. Available on a first-come, first- to provide an overview of the Theme Park. Device to amplify sound through headphones or induction Cut the wait time in easy the Downtown Disney tram load/unload area and locations have narrow queues formed by or Deposit served basis. Audio Description Utilizes Disney’s Handheld neck loop at specific attractions. 3 the Main Entrance Esplanade. These courtesy steps: railings that may be difficult for Guests Device to provide supplemental audio information Handheld Captioning Utilizes Disney’s Handheld wheelchairs are not permitted for use inside the and narration at specific attractions and outdoor using wheelchairs. At these locations, we Device to display text at select attractions. Theme Parks. See a Cast Member at tram load/ locations via an interactive audio menu. ® suggest that a member of your party order Check your Times Guide for a list of Disney FASTPASS attractions. unload area for additional information. and transport the food, or contact a Cast Portable Tactile Maps Provides a tactile Video Captioning Caption-ready monitors designated Ready to use the FASTPASS service on another attraction? Look at the bottom of representation of building boundaries, walkways, with a “CC” symbol can be activated by remote control. -

California Is a Garden of Eden, a Paradise to Live in Or See. — Woody Guthrie, Do Re Mi, 1937

TRAVEL PROMOTIONAL SERIES TRAVEL PROMOTIONAL SERIES A surfer at Huntington Beach Pier. california is a garden of eden, a paradise to live in or see. — woody guthrie, do re mi, 1937 he Mamas and the Papas dreamt of California on a winter’s day, and the Beach Boys wished every girl were from the Golden State. Beverly Hills was where Weezer want- ed to be, and Phantom Planet couldn’t wait to get to Orange County. Even Frank Sinatra couldn’t resist the lure of the United States’ third-largest state, singing that California was “a land that paradise could well be jealous of.” by melanie jarrett So just what is it about California that has inspired longing in everyone from early Span- ish missionaries to intrepid gold rushers to aspiring starlets and Silicon Valley entrepre- neurs? Our bet is on a diverse geography that ranges from the barren desert of the Mojave in the southeast to the towering Redwood forests of the northwest, to the snow-capped Sierra Nevada Mountains in the east and the sunny stretches of the Pacific Coast in the west. califor nia HUNTINGTON BEACH CONFERENCE AND VISITORS BUREAU 96 SPIRIT MAY 2012 MAY 2012 SPIRIT 97 TRAVEL PROMOTIONAL SERIES Cars Land is coming! You’ll feel like you’ve walked into the Disney•Pixar Cars movie, because Radiator Springs has been brought to life in this all-new land. LEFT Looking south across the Golden Gate Bridge with the San Francisco skyline in the distance. BELOW Sunset on Alcatraz island. san francisco We start up north in San Francisco, one of the biggest tourist destinations in scope, but smallest in area at only 49 square miles. -

Guidelines for Selling Your Collection

Brian's Toys www.brianstoys.com/sellyourtoys Disney - Pixar Car's Buy List Buy List QTY You Product Name UPC Series Class Total Notes Price Have to Sell Last Updated: April 14, 2017 Full Name: Address: Delivery W730 State Road 35 Phone: Address: Fountain City, WI 54629 Tel: 608.687.7572 ext. 3 E-mail: How did you hear about us? (please fill in) Fax: 608.687.7573 E-mail: [email protected] Note: Buylist prices on this sheet Guidelines for Selling Your Collection may change after 30 days Brian’s Toys will require a list of your items if you are interested in receiving a price quote on your collection. It is very important that we have an accurate description of your items so that we can give you an accurate price quote. By following the below format, you will help ensure an accurate quote for your collection. As an alternative to this excel form, we have a webapp available for http://buylist.brianstoys.com/lines/Cars/toys The buy list prices reflect items mint in their original packaging. STEP 1 Before we can confirm your quote, we will need to know what items you have to sell. The below list is sorted by different categories for Cars, starting with Cars 2. Search for each of your items and enter the quantity you want to sell in column with the red arrow. STEP 2 Once the list is complete, send the list to us by either fax, mail, or e-mail. STEP 3 If you use this form, we will confirm your quote within 1-2 business days upon receipt. -

Lake Powell View Estates Community Development

ABOUT THE AUTHOR Nancy Theken! Nancy Theken is the marke0ng manager at Lake Powell View Estates community development. She works with real estate agents in support of sales, social media marke0ng, and 0mely, relave content. Follow her Blog at: www.lakepowellviewestates.com Nancy may Be contacted at [email protected] PAGE 2 TABLE OF CONTENTS 4 Introduction 5 Travel To Lake Powell Via The Mother Road - Route 66 8 Standin’ on the Corner in Winslow, Arizona 11 Continuing West to Williams 14 On to Peach Springs 16 Last Stop – Oatman 17 About Lake Powell View Estates PAGE 3 Introduction Thank you for downloading our eBook. There are several routes that will lead you to the beauty and serenity of the Lake Powell area, but if you enjoy road trips, then a trip down memory lane via historic Route 66 is just what you need! We’ve mapped out this nostalgic and spectacularly scenic journey through Arizona to inspire you to get out and enjoy one of the most famous roads in America. From Holbrook to Oatman, this helpful guide highlights the must-see stops along the way and provides some insight and historical background as you pass from town to town. Enjoy! Nancy Theken PAGE 4 Travel To Lake Powell Via The Mother Road - Route 66 Lake Powell, Arizona is one of the most favorite vacaon des0naons in the country. People come from near and far to rent houseBoats and explore the never-ending coves and Bays that surround the lake. RememBer the old saying – “geng there is half the fun?” Well, perhaps the person that coined that phrase traveled to Lake Powell on historic Route 66. -

1 “I Grew up Loving Cars and the Southern California Car Culture. My Dad Was a Parts Manager at a Chevrolet Dealership, So V

“I grew up loving cars and the Southern California car culture. My dad was a parts manager at a Chevrolet dealership, so ‘Cars’ was very personal to me — the characters, the small town, their love and support for each other and their way of life. I couldn’t stop thinking about them. I wanted to take another road trip to new places around the world, and I thought a way into that world could be another passion of mine, the spy movie genre. I just couldn’t shake that idea of marrying the two distinctly different worlds of Radiator Springs and international intrigue. And here we are.” — John Lasseter, Director ABOUT THE PRODUCTION Pixar Animation Studios and Walt Disney Studios are off to the races in “Cars 2” as star racecar Lightning McQueen (voice of Owen Wilson) and his best friend, the incomparable tow truck Mater (voice of Larry the Cable Guy), jump-start a new adventure to exotic new lands stretching across the globe. The duo are joined by a hometown pit crew from Radiator Springs when they head overseas to support Lightning as he competes in the first-ever World Grand Prix, a race created to determine the world’s fastest car. But the road to the finish line is filled with plenty of potholes, detours and bombshells when Mater is mistakenly ensnared in an intriguing escapade of his own: international espionage. Mater finds himself torn between assisting Lightning McQueen in the high-profile race and “towing” the line in a top-secret mission orchestrated by master British spy Finn McMissile (voice of Michael Caine) and the stunning rookie field spy Holley Shiftwell (voice of Emily Mortimer). -

Disney California Adventure® GENERAL MAP

PAGE 5 Disney California Adventure® GENERAL MAP ENTRANCE Red Car Trolley Buena Vista Street Soarin' Around the World Monsters, Inc. Mike & Sulley to the Rescue! Mortimer’s Smokejumpers Market Sunset Studio Grill Showcase Catering Co. Theater BUENA VISTA STREET Schmoozies Clarabelle’s Hand- Scooped Ice Cream Fiddler, Fifer & Practical Cafe Award Red Car Weiners Fairfax Market HOLLYWOOD LAND Trolley Sorcerer's GRIZZLY PEAK News Boys Workshop Anna & Elsa's Hyperion Carthay Circle Royal Welcome Theater Restaurant Red Car Turtle Talk Trolley Disney Junior with Crush Grizzly Carthay Circle Carthay Circle Lounge Live on Stage! River Run Animation Academy Flik's Flyers Francis' Walt Disney Ladybug Wine Country Imagineering Boogie Guardians of the Blue Sky Galaxy — Mission: Redwood Creek Trattoria Princess Dot Breakout! Challenge Trail Cellar Puddle Park Corn Dog Red Car Castle Mendocino A BUGS LIFE Trolley - Goofy's Sky Sunset The Little Mermaid - Terrace Boulevard School Ariel's Undersea Adventure Mater's Junkyard Jamboree The Bakery Sonoma Tour, Fillmore's Heimlich's Jumpin' Taste-In Chew Chew Jellyfish Golden Terrace Tuck and Roll's Zephyr Train Drive 'Em Paradise Garden Buggies Grill Pacific Wharf Ghirardelli® Soda Café Cozy Cone PARADISE PIER Fountain and Motel Bayside Chocolate Shop Brews Silly Symphony PACIFIC WHARF Swings Lucky Fortune Boardwalk World Rita's Baja Cookery Flo's V8 Luigi’s Rollickin’ Pizza & Pasta of Color Blenders Café Roadstersn Ariel's Grotto Cocina Cucamonga Mexican Grill Mickey's Fun Wheel Cove Bar Paradise Pier Radiator Springs Ice Cream Racers Games of Company the Boardwalk CARS LAND Toy Story King Triton's Midway Mania!® Carousel' IncrediCoaster opening summer 2018 VISIT ANYTIME TABLE SERVICE DINING VISIT WITHIN FIRST HR OR QUICK RESTAURANTS WITH FASTPASS RESTROOMS VISIT IN FIRST OR LAST 2 HRS MEET THE CHARACTER VISIT AFTER 11 AM FIRST AID SMOKING AREA WWW.UNDERCOVERTOURIST.COM 1.800.846.1302. -

Free Racing for Good (Disney/Pixar Cars) Pdf

FREE RACING FOR GOOD (DISNEY/PIXAR CARS) PDF Ruth Homberg | 32 pages | 22 Jul 2014 | Random House Disney | 9780736432177 | English | United States Трасса Disney Pixar Cars Race Around Radiator Springs Aspiring champion race car Lightning McQueen is on the fast track to success, fame, and everything he's ever hoped for—until he takes an unexpected detour on dusty Route His have-it-all-now attitude is thrown into a tailspin when a small-town community that time forgot shows McQueen what he's been missing in his high-octane life. The filmmakers wanted the cars to look and feel authentic, so that the audience would relate to them as characters. A hotshot racecar was the early choice for lead character Lightning McQueen, and a rusty real-life tow truck found off Route 66 came to life as Mater. The Pixar team chose other cars to reflect people they had met on the road during Racing for Good (Disney/Pixar Cars) research for the film. Lightning McQueen is a hotshot, rookie race car, poised to become the youngest car ever to win the Piston Cup Championship. He has just two things on his mind: winning and the perks that come with it. But when Racing for Good (Disney/Pixar Cars) in-advertently gets lost in the town of Radiator Springs, he meets a new group of friends who challenge him to reconsider the car he wants to be. Mater is a good ol' boy tow truck with a big heart and a lovable laugh to match. Though a little rusty, he has the quickest towrope in Carburetor County and is always the first to lend a helping hand.