Full Year Results 27 November 2015 Agenda

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Rns Over the Long Term and Critical to Enabling This Is Continued Investment in Our Technology and People, a Capital Allocation Priority

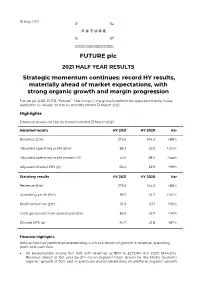

19 May 2021 FUTURE plc 2021 HALF YEAR RESULTS Strategic momentum continues: record HY results, materially ahead of market expectations, with strong organic growth and margin progression Future plc (LSE: FUTR, “Future”, “the Group”), the global platform for specialist media, today publishes its results for the six months ended 31 March 2021. Highlights Financial results for the six months ended 31 March 2021 Adjusted results HY 2021 HY 2020 Var Revenue (£m) 272.6 144.3 +89% Adjusted operating profit (£m)1 89.2 39.9 +124% Adjusted operating profit margin (%) 33% 28% +5ppt Adjusted diluted EPS (p) 65.4 32.9 +99% Statutory results HY 2021 HY 2020 Var Revenue (£m) 272.6 144.3 +89% Operating profit (£m) 59.7 24.7 +142% Profit before tax (£m) 56.9 27.1 +110% Cash generated from operations (£m) 85.9 35.7 +141% Diluted EPS (p) 40.7 21.8 +87% Financial highlights Robust first-half performance extending our track record of growth in revenue, operating profit and cash flow: An exceptionally strong first half, with revenue up 89% to £272.6m (HY 2020: £144.3m). Revenue ahead of last year by 21% on an organic2 basis, driven by the Media division’s organic2 growth of 30% and in particular digital advertising on-platform organic2 growth of 30% and eCommerce affiliates’ organic2 growth of 56%. US achieved revenue growth of 31% on an organic2 basis and UK revenues grew by 5% organically (UK has a higher mix of events and magazines revenues which were impacted more materially by the pandemic). -

Studiesineducation.Pdf

INDEX Foreword 1 Professor Cathy Nutbrown Special Educational Needs and Inclusive Education in Early Years: Teachers’ Views on 2 Practices for Effective Inclusion Pauline Mallia-Milanes How do Maltese Mothers of Children with Autistic Spectrum Disorder Perceive 15 Music as an Educational Intervention in Early Childhood? Julia Bianco Evaluating Young Children’s Science-Related Discourse whilst Engaging in Water Play 28 Activities Giselle Theuma Implementing the Maltese National Literacy Strategy in the Early and Primary Years: 42 Teachers’ and the Literacy Team’s Perspectives Joanne Falzon Zammit Munro Digital Literacy Practices at Home and School: Perceptions of 5 Year Old Children, their 56 Parents and their Teachers Alessandra Balzan The Impact of Digital Technologies on Emergent Readers 72 Rita Saliba Preparing for the Secondary Education Certificate Examination in Maltese through 88 Private Tuition Vanessa Saliba Mentoring Provision for Intending and Beginning Teachers in Malta 100 Tony Mizzi End Note 117 Sue Midolo Author Biographies 119 © 2017 The University of Sheffield and individual authors The University of Sheffield, School of Education, 388 Glossop Road, Sheffield, S10 2JA, UK email: [email protected] ii Foreword In 2009, by invitation of St Catherine’s High School Higher Education Tuition Centre the School of Education at The University of Sheffield launched an MA in Early Childhood Education. The first eBook Researching Early Childhood Education: Voices from Malta was published in 2012 and featured essays by the first 14 graduates of our programme. Since that time, the programme has expanded to include opportunities to study aspects of Languages in Education and Educational Studies. This eBook Studies in Education: Perspectives from Malta features the work of MA graduates who have focused on a range of educational topics with a particular interest policy and practice in Malta. -

110% Gaming 220 Triathlon Magazine 3D World Adviser

110% Gaming 220 Triathlon Magazine 3D World Adviser Evolution Air Gunner Airgun World Android Advisor Angling Times (UK) Argyllshire Advertiser Asian Art Newspaper Auto Car (UK) Auto Express Aviation Classics BBC Good Food BBC History Magazine BBC Wildlife Magazine BIKE (UK) Belfast Telegraph Berkshire Life Bikes Etc Bird Watching (UK) Blackpool Gazette Bloomberg Businessweek (Europe) Buckinghamshire Life Business Traveller CAR (UK) Campbeltown Courier Canal Boat Car Mechanics (UK) Cardmaking and Papercraft Cheshire Life China Daily European Weekly Classic Bike (UK) Classic Car Weekly (UK) Classic Cars (UK) Classic Dirtbike Classic Ford Classic Motorcycle Mechanics Classic Racer Classic Trial Classics Monthly Closer (UK) Comic Heroes Commando Commando Commando Commando Computer Active (UK) Computer Arts Computer Arts Collection Computer Music Computer Shopper Cornwall Life Corporate Adviser Cotswold Life Country Smallholding Country Walking Magazine (UK) Countryfile Magazine Craftseller Crime Scene Cross Stitch Card Shop Cross Stitch Collection Cross Stitch Crazy Cross Stitch Gold Cross Stitcher Custom PC Cycling Plus Cyclist Daily Express Daily Mail Daily Star Daily Star Sunday Dennis the Menace & Gnasher's Epic Magazine Derbyshire Life Devon Life Digital Camera World Digital Photo (UK) Digital SLR Photography Diva (UK) Doctor Who Adventures Dorset EADT Suffolk EDGE EDP Norfolk Easy Cook Edinburgh Evening News Education in Brazil Empire (UK) Employee -

Pressreader Magazine Titles

PRESSREADER: UK MAGAZINE TITLES www.edinburgh.gov.uk/pressreader Computers & Technology Sport & Fitness Arts & Crafts Motoring Android Advisor 220 Triathlon Magazine Amateur Photographer Autocar 110% Gaming Athletics Weekly Cardmaking & Papercraft Auto Express 3D World Bike Cross Stitch Crazy Autosport Computer Active Bikes etc Cross Stitch Gold BBC Top Gear Magazine Computer Arts Bow International Cross Stitcher Car Computer Music Boxing News Digital Camera World Car Mechanics Computer Shopper Carve Digital SLR Photography Classic & Sports Car Custom PC Classic Dirt Bike Digital Photographer Classic Bike Edge Classic Trial Love Knitting for Baby Classic Car weekly iCreate Cycling Plus Love Patchwork & Quilting Classic Cars Imagine FX Cycling Weekly Mollie Makes Classic Ford iPad & Phone User Cyclist N-Photo Classics Monthly Linux Format Four Four Two Papercraft Inspirations Classic Trial Mac Format Golf Monthly Photo Plus Classic Motorcycle Mechanics Mac Life Golf World Practical Photography Classic Racer Macworld Health & Fitness Simply Crochet Evo Maximum PC Horse & Hound Simply Knitting F1 Racing Net Magazine Late Tackle Football Magazine Simply Sewing Fast Bikes PC Advisor Match of the Day The Knitter Fast Car PC Gamer Men’s Health The Simple Things Fast Ford PC Pro Motorcycle Sport & Leisure Today’s Quilter Japanese Performance PlayStation Official Magazine Motor Sport News Wallpaper Land Rover Monthly Retro Gamer Mountain Biking UK World of Cross Stitching MCN Stuff ProCycling Mini Magazine T3 Rugby World More Bikes Tech Advisor -

How to Get Away with Copyright Infringement: Music Sampling As Fair Use

THIS VERSION MAY CONTAIN INACCURATE OR INCOMPLETE PAGE NUMBERS. PLEASE CONSULT THE PRINT OR ONLINE DATABASE VERSIONS FOR THE PROPER CITATION INFORMATION. NOTE HOW TO GET AWAY WITH COPYRIGHT INFRINGEMENT: MUSIC SAMPLING AS FAIR USE SAM CLAFLIN1 CONTENTS I. INTRODUCTION ............................................................................................ 102 II. BACKGROUND ............................................................................................ 104 A. History ............................................................................................ 104 i. Foundations of Copyright Law with Respect to Music ............ 104 ii. Music Sampling and Copyright ............................................... 105 B. The Fair Use Doctrine .................................................................... 107 i. Fair Use and Appropriation Art ................................................ 110 III. A CONTEMPORARY PERSPECTIVE ON MUSIC SAMPLING AND FAIR USE: ESTATE OF SMITH V. CASH MONEY RECORDS, INC. ................................ 113 A. Background ..................................................................................... 113 B. Analysis – An In-Depth Look at the Court’s Fair Use Approach in Estate of Smith ........................................................ 114 i. Factor One .............................................................................. 115 ii. Factor Two ............................................................................. 118 iii. Factor Three .......................................................................... -

Distribution List Page - 1

R56891A Gordon and Gotch (NZ) Limited 29/05/2018 8:57:12 Distribution List Page - 1 =========================================================================================================================================================== N O R T H I S L A N D ( M i d w e e k ) Issues invoiced in week 27/05/2018 - 2/06/2018 =========================================================================================================================================================== Invoice Recall Trade Retail Title Details Issue Details Date Date Price Price 2000 AD WEEKLY 105030 100080 NO. 2075 31/05/2018 11/06/2018 5.74 8.80 500 SUDOKU PUZZLES 239580 100010 NO. 39 31/05/2018 9/07/2018 4.53 6.95 A/F AEROPLANE MNTHLY 818005 100010 June 31/05/2018 25/06/2018 15.00 23.00 A/F AIRLINER WRLD 818020 100020 June 31/05/2018 25/06/2018 15.59 23.90 A/F AUTOCAR 818030 100080 9 May 31/05/2018 11/06/2018 12.72 19.50 A/F CLASSIC MOTORCYCLE 915600 100010 June 31/05/2018 2/07/2018 11.41 17.50 A/F GUITARIST 818155 100010 June 31/05/2018 25/06/2018 17.93 27.50 A/F INSIDE UNITED 896390 100010 June 31/05/2018 25/06/2018 12.72 19.50 A/F LINUX FORMAT DVD 818185 100010 June 31/05/2018 25/06/2018 18.20 27.90 A/F MATCH OF THE DAY 818215 100080 NO. 504 31/05/2018 11/06/2018 8.80 13.50 A/F MONOCLE> 874655 100020 June 31/05/2018 25/06/2018 16.30 25.00 A/F MOTORSPORT 818245 100010 June 31/05/2018 25/06/2018 13.63 20.90 A/F Q 818270 100010 July 31/05/2018 25/06/2018 14.02 21.50 A/F TOTAL FILM 818335 100010 June 31/05/2018 25/06/2018 10.11 15.50 A/F WOMAN&HOME 818365 100010 June 31/05/2018 25/06/2018 13.04 20.00 A/F YACHTING WRLD 818380 100010 June 31/05/2018 25/06/2018 14.35 22.00 ALL ABOUT SPACE 105505 100010 NO. -

SYNDICATION Partner with Future OUR PURPOSE

SYNDICATION Partner With Future OUR PURPOSE We change people’s lives through “sharing our knowledge and expertise with others, making it easy and fun for them to do what they want ” CONTENTS ● The Future Advantage ● Syndication ● Our Portfolio ● Company History THE FUTURE ADVANTAGE Syndication Our award-winning specialist content can be used to further enrich the experience of your audience. Whilst at the same time saving money on editorial costs. We have 4 million+ images and 670,000 articles available for reuse. And with the support of our dedicated in-house licensing team, this content can be seamlessly adapted into a range of formats such as newspapers, magazines, websites and apps. The Core Benefits: ● Internationally transferable content for a global audience ● Saving costs on editorial budget so improving profit margin ● Immediate, automated and hassle-free access to content via our dedicated content delivery system – FELIX – or custom XML feeds ● Friendly, dynamic and forward-thinking licensing team available to discuss editorial requirements #1 ● Rich and diverse range of material to choose from ● Access to exclusive content written by in-house expert editorial teams Monthly Bookazines Global monthly Social Media magazines users Fans 78 2000+ 148m 52m Source: Google Search 2018 SYNDICATION ACCESS the entire Future portfolio of market leading brands within one agreement. Our in context licence gives you the ability to publish any number of features, reviews or interviews to boost the coverage and quality of your publications. News Features Interviews License the latest news from all our Our brands speak to the moovers and area’s of interest from a single shakers within every subject we write column to a Double Page spread. -

MUSICRADAR.COM (12/6) Epic-Guitar-Performances-568156

MUSICRADAR.COM (12/6) http://www.musicradar.com/news/guitars/rival-sons-scott-holiday-talks-jimmy-page-riff-writing-and- epic-guitar-performances-568156 Rival Sons' Scott Holiday talks Jimmy Page, riff writing and epic guitar performances If Head Down were Rival Sons' debut album and not their third release, we'd be heralding the unexpected arrival of a bright new talent, and possibly even an important one, a group that manages to take their cues from firmly established blues-rock paradigms while proving there's still rich, untapped pockets to be mined. Oh, hell, let's dispense with the formalities and give it up for this California four-piece (singer Jay Buchanan, guitarist Scott Holiday, bassist Robin Everhart and drummer Mike Miley), who attack well- worn forms – there's also splashes of soul, funk and head-spinning psychedelia, for good measure – with a zeal that borders on audacity. The grooves are deep and the vocals are of the chest-beating variety, but the real star of the show is guitarist Holiday. On the album's 13 exhilarating cuts, he hits with with tectonic force, creating rich tapestries of sound that burst wide open with style, imagination and an infectious, warped charm. We caught up with Holiday the other day to chat about his spunky approach to guitar playing, his many axes and sonic toys, and to find out how he felt rubbing shoulders with a new fan, another six- string slinger who goes by the name Jimmy Page. So Jimmy Page likes your band. That's got to feel good. -

ABC Consumer Magazine Concurrent Release - Dec 2007 This Page Is Intentionally Blank Section 1

December 2007 Industry agreed measurement CONSUMER MAGAZINES CONCURRENT RELEASE This page is intentionally blank Contents Section Contents Page No 01 ABC Top 100 Actively Purchased Magazines (UK/RoI) 05 02 ABC Top 100 Magazines - Total Average Net Circulation/Distribution 09 03 ABC Top 100 Magazines - Total Average Net Circulation/Distribution (UK/RoI) 13 04 ABC Top 100 Magazines - Circulation/Distribution Increases/Decreases (UK/RoI) 17 05 ABC Top 100 Magazines - Actively Purchased Increases/Decreases (UK/RoI) 21 06 ABC Top 100 Magazines - Newstrade and Single Copy Sales (UK/RoI) 25 07 ABC Top 100 Magazines - Single Copy Subscription Sales (UK/RoI) 29 08 ABC Market Sectors - Total Average Net Circulation/Distribution 33 09 ABC Market Sectors - Percentage Change 37 10 ABC Trend Data - Total Average Net Circulation/Distribution by title within Market Sector 41 11 ABC Market Sector Circulation/Distribution Analysis 61 12 ABC Publishers and their Publications 93 13 ABC Alphabetical Title Listing 115 14 ABC Group Certificates Ranked by Total Average Net Circulation/Distribution 131 15 ABC Group Certificates and their Components 133 16 ABC Debut Titles 139 17 ABC Issue Variance Report 143 Notes Magazines Included in this Report Inclusion in this report is optional and includes those magazines which have submitted their circulation/distribution figures by the deadline. Circulation/Distribution In this report no distinction is made between Circulation and Distribution in tables which include a Total Average Net figure. Where the Monitored Free Distribution element of a title’s claimed certified copies is more than 80% of the Total Average Net, a Certificate of Distribution has been issued. -

Jon Fauer ASC Issue 99 Feb 2020

Jon Fauer ASC www.fdtimes.com Feb 2020 Issue 99 Technique and Technology, Art and Food in Motion Picture Production Worldwide Photo of Claire Mathon AFC by Ariane Damain Vergallo www.fdtimes.com Art, Technique and Technology On Paper, Online, and now on iPad Film and Digital Times is the guide to technique and technology, tools and how-tos for Cinematographers, Photographers, Directors, Producers, Studio Executives, Camera Assistants, Camera Operators, Grips, Gaffers, Crews, Rental Houses, and Manufacturers. Subscribe It’s written, edited, and published by Jon Fauer, ASC, an award-winning Cinematographer and Director. He is the author of 14 bestselling books—over 120,000 in print—famous for their user-friendly way Online: of explaining things. With inside-the-industry “secrets-of the-pros” www.fdtimes.com/subscribe information, Film and Digital Times is delivered to you by subscription or invitation, online or on paper. We don’t take ads and are supported by readers and sponsors. Call, Mail or Fax: © 2020 Film and Digital Times, Inc. by Jon Fauer Direct Phone: 1-570-567-1224 Toll-Free (USA): 1-800-796-7431 subscribe Fax: 1-724-510-0172 Film and Digital Times Subscriptions www.fdtimes.com PO Box 922 Subscribe online, call, mail or fax: Williamsport, PA 17703 Direct Phone: 1-570-567-1224 USA Toll-Free (USA): 1-800-796-7431 1 Year Print and Digital, USA 6 issues $ 49.95 1 Year Print and Digital, Canada 6 issues $ 59.95 Fax: 1-724-510-0172 1 Year Print and Digital, Worldwide 6 issues $ 69.95 1 Year Digital (PDF) $ 29.95 1 year iPad/iPhone App upgrade + $ 9.99 Film and Digital Times (normally 29.99) Get FDTimes on Apple Newsstand with iPad App when you order On Paper, Online, and On iPad a Print or Digital Subscription (above) Total $ __________ Print + Digital Subscriptions Film and Digital Times Print + Digital subscriptions continue to Payment Method (please check one): include digital (PDF) access to current and all back issues online. -

Building a Video Game Collection: Resources to Help You Get Started Philip Hallman Ambassador Books and Media, [email protected]

Against the Grain Volume 20 | Issue 5 Article 33 November 2008 Media Minder -- Building a Video Game Collection: Resources to Help you Get Started Philip Hallman Ambassador Books and Media, [email protected] Follow this and additional works at: https://docs.lib.purdue.edu/atg Part of the Library and Information Science Commons Recommended Citation Hallman, Philip (2008) "Media Minder -- Building a Video Game Collection: Resources to Help you Get Started," Against the Grain: Vol. 20: Iss. 5, Article 33. DOI: https://doi.org/10.7771/2380-176X.5211 This document has been made available through Purdue e-Pubs, a service of the Purdue University Libraries. Please contact [email protected] for additional information. As I See It! from page 78 Media Minder — Building a Video So what do we potential customers do? We Game Collection: Resources to default to Google, and Google Scholar. Google is a starting point for much serious Help you Get Started research. It is free of charge. And it is good enough for most initial searches, given that we Column Editor: Philip Hallman (Ambassador are otherwise priced out of the market. We may Books and Media) <[email protected]> also visit a nearby university library on occasions where a generalist search engine is simply not y interest in video games began, Re- good enough. There, we might simply use Web and subsequently ended, with the sponding of Science or Scopus. Mrelease of Pong. It was Christmas, to the frenzy, Speaking personally, my search engine of 1975, and my eldest brother bought a system colleges and universities have joined the choice is Google/Google Scholar. -

Complete Digital Magazine List Over 3,200 Titles

Complete Digital Magazine List Over 3,200 Titles $10 DINNERS (OR LESS!) (inside) interior design review .net CSS Design Essentials ¡Hola! Cocina ¡Hola! Especial Decoración ¡Hola! Especial Viajes ¡HOLA! FASHION ¡Hola! Fashion: Especial Alta Costura ¡Hola! Los Reyes Felipe VI y Letizia ¡Hola! Mexico ¡Hola! Prêt-À-Porter 0024 Horloges 01net 10 Minute Pilates 10 Minute Yoga Calm Highland Public Library Digital Magazine List - Last Updated 1.26.21 Page: 2 10 Week Fat Burn: Lose a Stone 100 All-Time Greatest Comics 100 Greatest Comedy Movies by Radio Times 100 greatest moments from 100 years of the Tour De France 100 Greatest Sci-Fi Characters 100 Greatest Thriller Movies by Radio Times 101 Home Sewing Ideas 101 Quick & Easy Crochet Makes 11 Freunde 1116 Design Tips 15 Minute Fitness: Busy Girls Guide 150 Thrifty Knits 200 Scrapbooking Ideas 220 Triathlon 220 Triathlon presents the Beginner's Guide to Triathlon 24H Brasil 25 Beautiful Homes 25 Years of the Hubble Space Telescope - from BBC Sky at Night Magazine 273 Papercraft & Card Ideas Highland Public Library Digital Magazine List - Last Updated 1.26.21 Page: 3 2nd セカンド 3D Art & Design Tips, Tricks & Fixes 3D Make And Print 3D World 400 Calories or Less: Easy Italian 45 Years on the MR&T 47 Creative Photography & Photoshop Projects 4x4 magazine 4x4 Magazine Australia 50 Baby Knits 50 Dream Rooms 50 Great British Locomotives 50 Greatest Mysteries in the Universe 50 Photo Projects Vol 2 50 Things No Man Should Be Without 50+ Decorating Ideas 500 Calorie Diet Complete Meal Planner 52 Bracelets