Vocus Communications Ltd. (VOC.AX)

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Annual Report

08 Annual Report iinet.net.au iiNet Limited ACN 068 628 937 ABN 48 068 628 937 Contents Financial Calendar and Corporate Information 1 About iiNet 3 iiNet History 17 Financial Highlights 19 Operational Highlights 20 Corporate Highlights 21 Education and Community Outreach 23 Chairman’s Review 25 Managing Director’s Report 29 Directors’ Report 35 Corporate Governance Statement 65 Financial Report 71 Directors’ Declaration 139 Independent Auditor’s Report 141 Shareholder Information 143 Financial Calendar Annual General Meeting The Annual General Meeting of iiNet Limited will be held at the Sheraton Hotel, 297 Adelaide Terrace, Perth, Western Australia, on Monday the 24th of November, 2008 at 10:30am. Other key dates in the 2009 financial year: • Annual report and Notice of Annual General Meeting mailed to shareholders October 2008 • Half-year results February 2009 • Full-year results August 2009 Corporate Information Directors Michael Smith Chairman Michael Malone Managing Director Andrew Milner Director (non-executive) Peter James Director (non-executive) Paul Broad Director (non-executive) Tony Grist Director (non-executive) David Grant Director (non-executive) Company Secretary David Buckingham Principal Place of Business and Registered Office iiNet Limited Durack Centre, Level 6 263 Adelaide Terrace Perth WA 6000 Share Registry Computershare Investor Services Pty Ltd Level 2 Reserve Bank Building 45 St George’s Terrace Perth WA 6000 Telephone: +61 8 9323 2000 Internet: www.computershare.com.au Stock Exchange Listings iiNet Limited’s ordinary shares are quoted on the Australian Stock Exchange Limited (ASX: IIN). Auditors Ernst & Young The Ernst & Young Building 11 Mounts Bay Road Perth WA 6000 1 iiNet Annual Report 2008 Financial Calendar and Corporate Information 2 08 About iiNet We’ve come a long way since our days of working out of a suburban garage in the early 90s. -

TPG Telecom Limited and Its Controlled Entities ABN 46 093 058 069

TPG Telecom Limited and its controlled entities ABN 46 093 058 069 Annual Report Year ended 31 July 2016 2 TPG Telecom Limited and its controlled entities Annual report For the year ended 31 July 2016 Contents Page Chairman’s letter 3 Directors’ report 5 Lead auditor’s independence declaration 34 Consolidated income statement 35 Consolidated statement of comprehensive income 36 Consolidated statement of financial position 37 Consolidated statement of changes in equity 38 Consolidated statement of cash flows 39 Notes to the consolidated financial statements 40 Directors’ declaration 91 Independent auditor’s report 92 ASX additional information 94 3 TPG Telecom Limited and its controlled entities Chairman’s letter For the year ended 31 July 2016 Dear Shareholders On behalf of the Board of Directors, I am pleased to present to you the TPG Telecom Limited Annual Report for the financial year ended 31 July 2016 (“FY16”). Financial Performance FY16 was another successful year for the Group. Continued organic growth and the integration of iiNet into the business have resulted in further increases in revenue, profits and dividends for shareholders. FY16 represents the eighth consecutive year that this has been the case. A detailed review of the Group’s operating and financial performance for the year is provided in the Operating and Financial Review section of the Directors’ Report starting on page 7 of this Annual Report, and set out below are some of the key financial highlights and earnings attributable to shareholders from the year. FY16 FY15 Movement Revenue ($m) 2,387.8 1,270.6 +88% EBITDA ($m) 849.4 484.5 +75% NPAT ($m) 379.6 224.1 +69% EPS (cents/share) 45.3 28.2 +61% Dividends (cents/share) 14.5 11.5 +26% iiNet Acquisition At the beginning of FY16 we completed the acquisition of iiNet and consequently there has been significant focus during the year on integrating the businesses to improve the efficiency of the combined organisation. -

Amaga 2020 Individual.Pdf

Tax invoice Membership category Payment details ABN 83 048 139 955 Membership Form Regular (Loyalty) Concession* (Loyalty) Membership Fee $ (inc of GST) (inc of GST) + Networks $ Individual □ $180 ($162) □ $90 ($81) + Donation* $ Your information Individual (existing Total Payable $ New member ICOM members only) □ $171 ($153) □ $86 ($76.50) □ Australian Museums and Galleries Association AMaGA Membership Card * Donations over $2.00 are tax deductible. □ Renewing member Individual employed by a member - Australian Museums and Galleries Association □ $144 ($144**) Member number (if known) AMaGA □ Membership Card institution Individual employed Payment method AMaGA by a member Please email or post your completed form for payment □ Please send me a new membership card □ $144 ($144**) - Member Number institution (existing New members will automatically get sent a card. Expiry processing. Your receipt and membership card or sticker will be Member Name AMaGA is a partner to ICOM members only) Renewing members will receive a sticker with your Australian AMaGA Museums ICOM Australia. and Galleries If found, please return to Association PO Box 24, Deakin West receipt/invoice to attach to your current card. Member ACT 2600 issued when payment has been processed. * Concession rates available to retired, full-time students, pensioners, unemployed Member Number Expiry Member Name and volunteers Australian AMaGA is a partner to Museums ICOM Australia. and Galleries If found, please return to Association PO Box 24, Deakin West Member ACT 2600 made payable to Australian Museums and Galleries Association ** Discounts are capped at 20% □ Cheque Title □ Mr □ Miss □ Ms □ Mrs □ Dr □ Name Loyalty Discount Members of more than five consecutive years can claim a 10% loyalty Credit Card (Visa or Mastercard only) discount on their membership. -

2021 NBN Plan Awards Methodology Report

Mozo Experts Choice Awards NBN Plans 2021 This is the third year running that we’ve gathered together countless pieces of information and applied our methodology to find the leading NBN broadband plans in Australia. Product providers don’t pay to be in the running with our awards, and we don’t play favourites. Our judges base their decision on hard-nosed calculations of value to the consumer, using Mozo’s extensive product database and research capacity. We identify the most important features of each product, group each product into like-for-like comparisons, and then calculate which are better value than most or offer market-leading features. This report lists the winners and explains the judging methodology for our 2021 NBN awards. 1 NBN Plans - 2021 Winners Fast (NBN 100) This category assessed Premium plans offering the NBN’s top speeds and no data limits. Accord with Officeworks Super Fast Dodo nbn100 Exetel Premium nbn100 iPrimus Premium Kogan Gold Mate Soul Mates Spintel Premium 100 Tangerine Telecom XXL Speed Boost TPG NBN100 Unlimited Standard Plus (NBN 50) For this category, the judges looked at plans for the middle tier NBN speed, with no limit on data usage. Belong Standard Plus Exetel Standard Plus nbn50 iPrimus Standard Plus Kogan Silver Spintel Plus 50 Tangerine Telecom XL Speed Boost 2 Standard (NBN 25) People looking for a more entry level internet service may not need to high speeds of other tiers, and have lower data usage. In this category, plans with a data limit of at least 500GB could qualify, as long as there was a meaningful price benefit. -

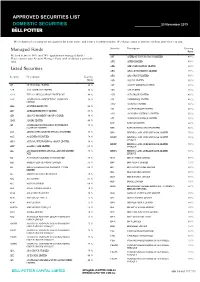

Approved Securities List

APPROVED SECURITIES LIST DOMESTIC SECURITIES 23 November 2019 The inclusion of a security on our approval list is not advice and is not a recommendation. We change ratios at any time without prior notice to you. Security Description Gearing Managed Funds Ratio We lend between 50% and 70% against most managed funds. APT AFTERPAY TOUCH GROUP LIMITED 40 % Please contact your Account Manager if you wish to discuss a particular fund. APX APPEN LIMITED 40 % Listed Securities ARB ARB CORPORATION LIMITED. 60 % ARG ARGO INVESTMENTS LIMITED 75 % Security Description Gearing ARQ ARQ GROUP LIMITED 50 % Ratio ASB AUSTAL LIMITED 50 % 3PL 3P LEARNING LIMITED.. 40 % AST AUSNET SERVICES LIMITED 65 % A2B A2B AUSTRALIA LIMITED 50 % ASX ASX LIMITED 70 % A2M THE A2 MILK COMPANY LIMITED NZ 40 % AUB AUB GROUP LIMITED 40 % AAC AUSTRALIAN AGRICULTURAL COMPANY 50 % AVJ AVJENNINGS LIMITED 40 % LIMITED. AWC ALUMINA LIMITED 70 % ABA AUSWIDE BANK LTD 40 % AX1 ACCENT GROUP LIMITED 50 % ABC ADELAIDE BRIGHTON LIMITED 65 % AYS AMAYSIM AUSTRALIA LIMITED 50 % ABP ABACUS PROPERTY GROUP STAPLED 50 % AZJ AURIZON HOLDINGS LIMITED 70 % ADH ADAIRS LIMITED 40 % BAP BAPCOR LIMITED 60 % AFI AUSTRALIAN FOUNDATION INVESTMENT 75 % COMPANY LIMITED BBN BABY BUNTING GROUP LIMITED 50 % AGI AINSWORTH GAME TECHNOLOGY LIMITED 55 % BEN BENDIGO AND ADELAIDE BANK LIMITED 70 % AGL AGL ENERGY LIMITED. 70 % BENPE BENDIGO AND ADELAIDE BANK LIMITED 70 % LPYR6UT AHG AUTOMOTIVE HOLDINGS GROUP LIMITED. 50 % BENPF BENDIGO AND ADELAIDE BANK LIMITED 70 % AHY ASALEO CARE LIMITED 65 % LPYR6UT AIA AUCKLAND INTERNATIONAL AIRPORT LIMITED 70 % BENPG BENDIGO AND ADELAIDE BANK LIMITED 70 % NZX LPYR3UT ALF AUSTRALIAN LEADERS FUND LIMITED 50 % BGA BEGA CHEESE LIMITED 60 % ALG ARDENT LEISURE GROUP LIMITED 55 % BHP BHP GROUP LIMITED 75 % ALI ARGO GLOBAL LISTED INFRASTRUCTURE 60 % BIN BINGO INDUSTRIES LIMITED 50 % LIMITED BKL BLACKMORES LIMITED 60 % ALL ARISTOCRAT LEISURE LIMITED 70 % BKW BRICKWORKS LIMITED 60 % ALQ ALS LIMITED 65 % BLD BORAL LIMITED. -

Quarterly Investment Update Antares High Growth Shares Fund – June 2021

Quarterly Investment Update Antares High Growth Shares Fund – June 2021 For adviser use only Highlights for the quarter Performance: The Fund returned 9.6% (net of fees) for the June quarter, outperforming its benchmark by 1.3%. Contributors to performance: Positive contributors – Aristocrat Leisure, Telix Pharmaceuticals, Megaport, Boral, Woodside (not owned); Negative contributors – Incitec Pivot, Qantas, ANZ, Resmed (not owned) and Altium (not owned). Stock activity: Buys/additions – Ansell, Downer and TPG Telecom ; Sells/reductions – BlueScope Steel, Boral, Endeavour Group and Worley Fund snapshot Inception date 7 December 1999 Benchmark S&P/ASX 200 Total Return Index To outperform the benchmark (after fees) over rolling Investment objective 5-year periods Investment returns as at 30 June 20211 Period 3 months 1 year 3 years pa 5 years pa 10 years pa Since inception pa Net return2 % 9.6 39.9 9.2 12.6 10.0 11.0 Gross return3 % 9.9 41.9 10.5 13.9 11.2 12.5 Benchmark return % 8.3 27.8 9.6 11.2 9.3 8.5 Net excess return % 1.3 12.1 -0.4 1.4 0.7 2.5 Gross excess return % 1.6 14.1 0.9 2.7 1.9 4.0 1 Past performance is not a reliable indicator of future performance. Returns are not guaranteed and actual returns may vary from any target returns described in this document. 2 Investment returns are based on exit prices, and are net of management fees and assume reinvestment of all distributions. Contributors to performance Pleasingly the Fund enjoyed another strong quarter, returning 9.6% (net of fees) vs the benchmark return of 8.3%. -

ASX/Media Release

ASX/Media Release 29 March 2017 Sale of Investment in Macquarie Telecom Group Vocus Group Limited (ASX: VOC, ‘Vocus’) today announces that it has disposed of 3,358,511 shares representing ~16% relevant interest in the ordinary shares of Macquarie Telecom Group Limited (ASX: MAQ). The shares were held via a total return swap as described in the FY16 Vocus financial statements. Attached is the Form 605 Notice of ceasing to be a substantial holder. ENDS For further information please contact: Kelly Hibbins Investor Relations Debra Mansfield Corporate Communications P: +61 2 8316 9856 P: +61 3 9674 6569 M: +61 414 609 192 E: [email protected] E: [email protected] About Vocus: Vocus Group (ASX: VOC) is a vertically integrated telecommunications provider, operating in the Australian and New Zealand markets. The Company owns an extensive national infrastructure network of metro and back haul fibre connecting all capital cities and most regional centres across Australia and New Zealand. Vocus infrastructure now connects directly to more than 5,500 buildings. Vocus owns a portfolio of brands catering to corporate, small business, government and residential customers across Australia and New Zealand. Vocus also operates in the wholesale market providing high performance, high availability and highly scalable communications solutions which allow service providers to quickly and easily deploy new services for their own customer base. For more information please go to our website www.vocusgroup.com.au. VOCUSGROUP.COM.AU 605 page 1/2 15 July 2001 Form 605 Corporations Act 2001 Section 671B Notice of ceasing to be a substantial holder To Company Name/Scheme ACN/ARSN 1. -

Communication Infrastructure Study for Precise Positioning Services in Regional Queensland

View metadata, citation and similar papers at core.ac.uk brought to you by CORE provided by Queensland University of Technology ePrints Archive QUT Digital Repository: http://eprints.qut.edu.au/ Wang, Charles and Feng, Yanming and Higgins, Matthew and Looi, Mark (2009) Communication infrastructure study for precise positioning services in regional Queensland. In: Proceedings of International Global Navigation Satellite Systems Society Symposium, 1-3 December 2009, Holiday Inn Hotel, Gold Coast, Queensland. © Copyright 2009 [please consult the authors] International Global Navigation Satellite Systems Society IGNSS Symposium 2009 Holiday Inn Surfers Paradise, Qld, Australia 1 – 3 December, 2009 Communication Infrastructure Study for Precise Positioning Services in Regional Queensland Charles Wang Queensland University of Technology, Australia +61 7 3138 1963, [email protected] Yanming Feng Queensland University of Technology, Australia +61 7 3138 1926, [email protected] Matt Higgins Department of Environment and Resource Management +61 7 3896 3754, [email protected] Mark Looi Queensland University of Technology, Australia +61 7 3138 5114, [email protected] ABSTRACT Providing precise positioning services in regional areas to support agriculture, mining, and construction sectors depends on the availability of ground continuously operating GNSS reference stations and communications linking these stations to central computers and users. With the support of CRC for Spatial Information, a more comprehensive review has been completed recently to examine various wired and wireless communication links available for precise positioning services, in particular in the Queensland regional areas. The study covers a wide range of communication technologies that are currently available, including fixed, mobile wireless, and Geo-stationary and or low earth orbiting satellites. -

Interim Report: Senate Select Committee on the National

APPENDIX 4 Witnesses Who Appeared Before the Committee Sydney, Tuesday 7 October 2008 BREALEY, Mr Michael, Manager, Public Policy Vodafone Australia BUDDE, Mr Paul, Managing Director Paul Budde Communication Pty Ltd CHAPMAN, Mr Alexander, Executive Officer, Policy and Strategy Coordinator Australian Federation of Deaf Societies CORBIN, Ms Teresa, Chief Executive Officer Consumers Telecommunications Network HICKS, Mr Gregory, Chairman Adam Internet Pty Ltd POOLMAN, Mr Clive, General Manager Strategy AAPT SCHUBERT, Ms Georgia Kate, General Manager, Public Policy Vodafone Australia WALTERS, Ms Sheena, Manager, Interpreting and Advocacy Deaf Society of New South Wales WEIR, Ms Deanne, Group Director, Corporate Development and Legal Affairs AUSTAR United Communications Ltd Canberra, Wednesday 8 October 2008 COBCROFT, Mr Simon, Acting Assistant Secretary, Broadband Infrastructure Branch Department of Broadband, Communications and the Digital Economy COSGRAVE, Mr Michael, Group General Manager, Communications Group Australian Competition and Consumer Commission DIMASI, Mr Joe, Executive General Manager, Regulatory Affairs Division Australian Competition and Consumer Commission 126 EGAN, Hon. Michael Rueben, Chairman Terria Pty Ltd FORMAN, Mr David, Executive Director Competitive Carriers Coalition HEALY, Mr Matthew, Chair Competitive Carriers Coalition KING, Ms Marianne, Assistant Secretary, National Broadband Network Taskforce Department of Broadband, Communications and the Digital Economy LYON, Mr Brendan Curtis, Executive Director Infrastructure -

Domestic Transmission Capacity Service

Domestic Transmission Capacity Service An ACCC Draft Report on the review of the declaration for the Domestic Transmission Capacity Service December 2018 1 2 List of abbreviations ACCC Australian Competition and Consumer Commission AVC Access virtual circuit CAN Customer access network CBD Central business district CCA Competition and Consumer Act 2010 CSA Connectivity serving area CSP Carriage service provider CVC Connectivity virtual circuit DCS Data Carriage Service DSL Digital subscriber line DSLAM Digital subscriber line access multiplexer DTCS Domestic transmission capacity service ESA Exchange service area FAD Final access determination FSA Fibre serving area FTTB Fibre to the building FTTC Fibre to the curb FTTN Fibre to the node FTTP Fibre to the premises HFC Hybrid fibre coaxial Infrastructure RKR Audit of Telecommunications Infrastructure Assets – Record Keeping Rules IP Internet protocol LTIE Long-term interests of end-users Mbps Megabits per second MLL Managed leased line MNO Mobile network operator NBN National Broadband Network NBN Co NBN Co Limited 3 NNI Link product Virtual network-to-network interface link product currently being developed by NBN Co POI Point of interconnection POP Point of presence RKR Record keeping rules RSP Retail service provider SAM Service area module SAOs Standard access obligations SIOs Services in operation SSU Structural separation undertaking TC-1 NBN Co’s highest priority traffic class. It is suitable for applications such as voice. TC-2 An NBN traffic class that provides support for business type applications that require a committed information rate. TC-3 An NBN traffic class designed to give priority to transactional data such as business applications. -

Annual Report 2011

Telecommunications Industry Ombudsman TELECOMMUNICATIONS INDUSTRY OMBUDSMAN 2011 ANNUAL REPORT A year of change CONTENTS ABOUT US 1 How the TIO works 1 Board and Council 2 THE YEAR AT A GLANCE 5 Ombudsman’s overview 5 A year of change 6 Highlights 7 Top trends 2010-11 8 PERFORMANCE 11 Resolving complaints 11 Our organisation 18 Contributing to the co-regulatory environment 22 Creating awareness 23 The Road Ahead 26 TIO IN NUMBERS 27 Complaint statistics 2010–11 27 Top 10 members 32 Complaints by member 37 Timeliness 49 Industry Codes 50 FiNANCiaL REPORT FOR THE YEAR ENDED 30 JUNE 2011 55 Financial report 56 APPENDICES 88 Appendix 1 Systemic issues 1 July 2010- 30 June 2011 88 Appendix 2 List of public submissions made by the TIO 91 Appendix 3 Calendar of outreach activities 93 Appendix 4 Issues by Category 94 Appendix 5 Explanation of TIO data terms 108 1 ABOUT US How the TIO works The Telecommunications Industry Ombudsman is a fast, free and fair dispute resolution service for small business and residential consumers who have a complaint about their telephone or internet service in Australia. We are independent and do not take sides. Our goal is to settle disputes quickly in an objective and non-bureaucratic way. We are able to investigate complaints about telephone and internet services, including by collecting all documentation and information relevant to the complaint. We have the authority to make binding decisions (decisions a telecommunications company is legally obliged to implement) up to the value of $30,000, and recommendations up to the value of $85,000. -

ICT Services Contractor Profiles: Category 3 1 February 2016 to 31 March 2021

Contract No: ICTS2015 Last Updated: 20 May 2020 Document number: 01791286 ICT Services Contractor Profiles: Category 3 1 February 2016 to 31 March 2021 CONTRACT MANAGER Email: [email protected] Tel: 08 6551 1375 Government Procurement Department of Finance Optima Centre 16 Parkland Road OSBORNE PARK WA 6017 Contents 4Logic ......................................................................................................................................................... 5 Agile Computing Pty Ltd ............................................................................................................................. 6 agility IT Consulting .................................................................................................................................... 7 Amristar Solutions ...................................................................................................................................... 8 ASG Group Limited .................................................................................................................................... 9 Asterisk Information Security .................................................................................................................... 10 Aurora Consulting Pty Ltd ......................................................................................................................... 11 Avantgarde Technologies ......................................................................................................................... 12