Audit Manual for Kerala State Audit Department

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Particulars of Some Temples of Kerala Contents Particulars of Some

Particulars of some temples of Kerala Contents Particulars of some temples of Kerala .............................................. 1 Introduction ............................................................................................... 9 Temples of Kerala ................................................................................. 10 Temples of Kerala- an over view .................................................... 16 1. Achan Koil Dharma Sastha ...................................................... 23 2. Alathiyur Perumthiri(Hanuman) koil ................................. 24 3. Randu Moorthi temple of Alathur......................................... 27 4. Ambalappuzha Krishnan temple ........................................... 28 5. Amedha Saptha Mathruka Temple ....................................... 31 6. Ananteswar temple of Manjeswar ........................................ 35 7. Anchumana temple , Padivattam, Edapalli....................... 36 8. Aranmula Parthasarathy Temple ......................................... 38 9. Arathil Bhagawathi temple ..................................................... 41 10. Arpuda Narayana temple, Thirukodithaanam ................. 45 11. Aryankavu Dharma Sastha ...................................................... 47 12. Athingal Bhairavi temple ......................................................... 48 13. Attukkal BHagawathy Kshethram, Trivandrum ............. 50 14. Ayilur Akhileswaran (Shiva) and Sri Krishna temples ........................................................................................................... -

KERALA SOLID WASTE MANAGEMENT PROJECT (KSWMP) with Financial Assistance from the World Bank

KERALA SOLID WASTE MANAGEMENT Public Disclosure Authorized PROJECT (KSWMP) INTRODUCTION AND STRATEGIC ENVIROMENTAL ASSESSMENT OF WASTE Public Disclosure Authorized MANAGEMENT SECTOR IN KERALA VOLUME I JUNE 2020 Public Disclosure Authorized Prepared by SUCHITWA MISSION Public Disclosure Authorized GOVERNMENT OF KERALA Contents 1 This is the STRATEGIC ENVIRONMENTAL ASSESSMENT OF WASTE MANAGEMENT SECTOR IN KERALA AND ENVIRONMENTAL AND SOCIAL MANAGEMENT FRAMEWORK for the KERALA SOLID WASTE MANAGEMENT PROJECT (KSWMP) with financial assistance from the World Bank. This is hereby disclosed for comments/suggestions of the public/stakeholders. Send your comments/suggestions to SUCHITWA MISSION, Swaraj Bhavan, Base Floor (-1), Nanthancodu, Kowdiar, Thiruvananthapuram-695003, Kerala, India or email: [email protected] Contents 2 Table of Contents CHAPTER 1. INTRODUCTION TO THE PROJECT .................................................. 1 1.1 Program Description ................................................................................. 1 1.1.1 Proposed Project Components ..................................................................... 1 1.1.2 Environmental Characteristics of the Project Location............................... 2 1.2 Need for an Environmental Management Framework ........................... 3 1.3 Overview of the Environmental Assessment and Framework ............. 3 1.3.1 Purpose of the SEA and ESMF ...................................................................... 3 1.3.2 The ESMF process ........................................................................................ -

Day Tour to Guruvayur Temple and Elephant Camp

DAY TOUR TO GURUVAYUR TEMPLE AND ELEPHANT CAMP Around 07:30 AM, pick up from respective hotels in Cochin and proceed to Guruvayur (Around 2 ½ hrs drive). Upon arrival visit Punnathur Elephant Court. Punnathurkotta was once the palace of a local ruler, but the palace grounds are now used to house the elephants belonging to the Guruvayoor temple, and has been renamed Anakkotta (meaning "Elephant Fort"). There were 86 elephants housed there, but currently there are about 59 elephants. The elephants are ritual offerings made by the devotees of Lord Guruvayurappa. This facility is also used to train the elephants to serve Lord Krishna as well as to participate in many festivals that occur throughout the year. The oldest elephant is around 82 years of age and is called 'Ramachandran'. Later visit the famous Guruvayur Temple. Guruvayur Sri Krishna Temple is a Hindu temple dedicated to the god Krishna (an avatar of the god Vishnu), located in the town of Guruvayur in Kerala, India. It is one of the most important places of worship for Hindus of Kerala and is often referred to as "Bhuloka Vaikunta" which translates to the "Holy Abode of Vishnu on Earth". Have lunch from Guruvayur and proceed back to conference venue. En route visit Kodungaloor. Once a maritime port of international repute because of its strategic location at the confluence of the Periyar River and the Arabian Sea, Kondugalloor was considered the gateway to ancient India or the Rome of the East, because of its status as a centre for trade. It was also the entry point of three major religions to India - Christianity, Judaism and Islam. -

Reportable in the Supreme Court of India Civil

Civil Appeal No. 2732 of 2020 (arising out of SLP(C)No.11295 of 2011) etc. Sri Marthanda Varma (D) Thr. LRs. & Anr. vs. State of Kerala and ors. 1 REPORTABLE IN THE SUPREME COURT OF INDIA CIVIL APPELLATE/CIVIL ORIGINAL/INHERENT JURISDICTION CIVIL APPEAL NO.2732 OF 2020 [Arising Out of Special Leave Petition (C) No.11295 of 2011] SRI MARTHANDA VARMA (D) THR. LRs. & ANR. …Appellants VERSUS STATE OF KERALA & ORS. …Respondents WITH CIVIL APPEAL NO. 2733 OF 2020 [Arising Out of Special Leave Petition (C) No.12361 of 2011] AND WRIT PETITION(C) No.518 OF 2011 AND CONMT. PET.(C) No.493 OF 2019 IN SLP(C) No.12361 OF 2011 Civil Appeal No. 2732 of 2020 (arising out of SLP(C)No.11295 of 2011) etc. Sri Marthanda Varma (D) Thr. LRs. & Anr. vs. State of Kerala and ors. 2 J U D G M E N T Uday Umesh Lalit, J. 1. Leave granted in Special Leave Petition (Civil) No.11295 of 2011 and Special Leave Petition (Civil) No.12361 of 2011. 2. Sree Chithira Thirunal Balarama Varma who as Ruler of Covenanting State of Travancore had entered into a Covenant in May 1949 with the Government of India leading to the formation of the United State of Travancore and Cochin, died on 19.07.1991. His younger brother Uthradam Thirunal Marthanda Varma and the Executive Officer of Sri Padmanabhaswamy Temple, Thiruvananthapuram (hereinafter referred to as ‘the Temple’) as appellants 1 and 2 respectively have filed these appeals challenging the judgment and order dated 31.01.2011 passed by the High Court1 in Writ Petition (Civil) No.36487 of 2009 and in Writ Petition (Civil) No.4256 of 2010. -

Mgl-Int-1-2013-Unpaid Shareholders List As on 31

DEMAT ID_FOLIO NAME WARRANT NO MICR DIVIDEND AMOUNT ADDRESS 1 ADDRESS 2 ADDRESS 3 ADDRESS 4 CITY PINCODE JH1 JH2 000404 MOHAMMED SHAFEEQ 27 508 30000.00 PUTHIYAVEETIL HOUSE CHENTHRAPPINNI TRICHUR DIST. KERALA DR. ABDUL HAMEED P.A. 002679 NARAYANAN P S 51 532 12000.00 PANAT HOUSE P O KARAYAVATTOM, VALAPAD THRISSUR KERALA 001431 JITENDRA DATTA MISRA 89 570 36000.00 BHRATI AJAY TENAMENTS 5 VASTRAL RAOD WADODHAV PO AHMEDABAD 382415 IN30066910088862 K PHANISRI 116 597 15900.00 Q NO 197A SECTOR I UKKUNAGARAM VISAKHAPATNAM 530032 IN30047640586716 P C MURALEEDHARAN NAIR 120 601 15000.00 DOOR NO 92 U P STAIRS DEVIKALAYA 8TH MAIN RD 9TH CROSS SARASWATHIPURAM MYSORE 570009 001424 BALARAMAN S N 126 607 60000.00 14 ESOOF LUBBAI ST TRIPLICANE MADRAS 600005 002473 GUNASEKARAN V 128 609 30000.00 NO.5/1324,18TH MAIN ROAD ANNA NAGAR WEST CHENNAI 600040 000697 AMALA S. 143 624 12000.00 36 CAR STREET SOWRIPALAYAM COIMBATORE TAMILNADU 641028 000953 SELVAN P. 150 631 18000.00 18, DHANALAKSHMI NAGAR AVARAMPALAYAM ROAD, COIMBATORE TAMILNADU 641044 001209 PANCHIKKAL NARAYANAN 153 634 60000.00 NANU BHAVAN KACHERIPARA KANNUR KERALA 670009 002985 BABY MATHEW 173 654 12000.00 PUTHRUSSERY HOUSE PULIKKAYAM KODANCHERY CALICUT 673580 001680 RAVI P 182 663 30000.00 SUDARSAN CHEMBAKKASSERY TATTAMANGALAM KERALA 678102 001440 RAJI GOPALAN 198 679 60000.00 ANASWARA KUTTIPURAM THIROOR ROAD KUTTYPURAM KERALA 679571 001756 UNNIKRISHNAN P 222 703 30000.00 'SREE SAILAM' PUDUKULAM ROAD PUTHURKKARA, AYYANTHOLE POST THRISSUR 680003 AMBIKA C P 1201090001296071 REBIN SUNNY 227 708 18750.00 21/14 BEETHEL P O AYYANTHOLE THRISSUR 680003 IN30163741039292 NEENAMMA VINCENT 260 741 18000.00 PLOT NO103 NEHRUNAGAR KURIACHIRA THRISSUR 680006 002191 PRESANNA BABU M V 310 791 30000.00 MURIYANKATTIL HOUSE EDAKULAM IRINJALAKUDA, THRISSUR KERALA 680121 SHAILA BABU 001567 ABUBAKER P B 375 856 15000.00 PUITHIYAVEETIL HOUSE P O KURUMPILAVU THRISSUR KERALA 680564 IN30163741303442 REKHA M P 419 900 20250.00 FLAT NO 571 LUCKY HOME PLAZA NEAR TRIPRAYAR TEMPLE NATTIKA P O THRISSUR 680566 1201090004031286 KUMARAN K K . -

Link to Brochure

GURUVAYURAPPAN TEMPLE OF BRAMPTON A TEMPLE FOR HUMANITY A timeline of the historic facts & landmarks October 2013 The journey Atbutha Saanthi Homam starts here and Khananaadi August 2013 Mid 1990s Third Karishanam Beginning of a dream April 2013 July 1999 Approval of site plan application Corporation registered Bought 10.2 acres of land June-July 2011 June 2002 First Sapthaham Guruvayurappan Temple of Brampton May 2011 GTOB Timeline registered Ownership and land (2 acre) 2006 transferred to GTOB Temporary July 2010 location at Caledon Arrival of Thirumeni Kariannur Mana Second Karishanam Divakaran Namboothiri with family Oct. 2009 2007 Opening of GTOB at its temporary location First Karishanam and Bhoo Parigraham Late 2008 March 2008 Visit by Vezhaparambu Brahmadattan Namboothiri, Application for Vastu and Temple construction rezoning approved expert from Kerala Formation of GTOB chapters – 16 in Canada and 13 in US 2 / 18 GURUVAYURAPPAN TEMPLE OF BRAMPTON PRESIDENT’S MESSAGE A temple of tomorrow I was glad when Mr. Paul Snape, Acting Director, Land Development Services, City of Brampton wrote to us, on 19th April 2013, stating that our “site plan application has been approved!” and City’s Legal Services Department was asked to draft the agreement that Guruvayurappan Temple of Brampton (GTOB) had to execute. GTOB had to deposit an amount equal to the estimated cost of recommended grading, landscaping, parking etc. as a “guarantee” to be refunded once the work is completed to the satisfaction of the city officials. Subsequent changes suggested or made by City and GTOB resulted in further delay by more than one year. We have made modifications to the maximum extent possible, to reduce the cost to affordable levels and to minimize both the debt load and time for construction. -

Club Health Assessment MBR0087

Club Health Assessment for District 318 A through April 2021 Status Membership Reports Finance LCIF Current YTD YTD YTD YTD Member Avg. length Months Yrs. Since Months Donations Member Members Members Net Net Count 12 of service Since Last President Vice Since Last for current Club Club Charter Count Added Dropped Growth Growth% Months for dropped Last Officer Rotation President Activity Account Fiscal Number Name Date Ago members MMR *** Report Reported Report *** Balance Year **** Number of times If below If net loss If no When Number Notes the If no report on status quo 15 is greater report in 3 more than of officers thatin 12 months within last members than 20% months one year repeat do not haveappears in two years appears appears appears in appears in terms an active red Clubs less than two years old 144130 Akkulam 12/22/2020 Active 23 23 0 23 100.00% 0 4 N N/R 139423 Chadayamangalam Jatayu 08/26/2019 Active 27 6 0 6 28.57% 20 1 2 R 1 $954.37 Exc Award (06/30/2020) M,MC,SC 139657 Chavara South 09/05/2019 Active(1) 20 23 20 3 17.65% 20 1 1 2 R 12 Exc Award (06/30/2020) 139408 Kadakkal 09/24/2019 Active 32 11 0 11 52.38% 21 4 2 N 6 90+ Days $51.41 T,M,MC 138461 Kandalloor 06/10/2019 Active(1) 17 0 14 -14 -45.16% 31 1 1 3 N 16 Exc Award (06/30/2020) 144197 Karunagappally Central 12/21/2020 Active 20 20 0 20 100.00% 0 4 T,M,VP,MC,SC N/R 145929 Kovalam Raymond 04/26/2021 Newly 22 22 0 22 100.00% 0 0 N N/R Chartered 144126 Kundara Royals 12/18/2020 Active 26 28 2 26 100.00% 0 0 0 N 1 VP 140297 Pothencode 12/02/2019 Active 42 0 1 -1 -2.33% -

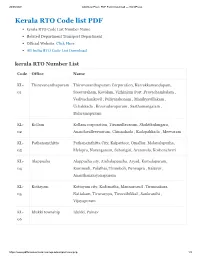

Kerala RTO Code List PDF Kerala RTO Code List Number Name Related Department Transport Department Official Website Click Here All India RTO Code List Download

20/05/2021 Add New Post ‹ PDF Form Download — WordPress Kerala RTO Code list PDF kerala RTO Code List Number Name Related Department Transport Department Official Website Click Here All India RTO Code List Download kerala RTO Number List Code Office Name KL- Thiruvananthapuram Thiruvananthapuram Corporation, Karrakkamandapam, 01 Sreevaraham, Kovalam, Vizhinjam Port ,Pravachambalam , Vedivachankovil , Puliyarakonam , Manikyavillakam , Uchakkada , Kesavadasapuram , Sasthamangalam , Balaramapuram KL- Kollam Kollam corporation, Tirumullavaram, Shaktikulangara, 02 Anandavalleeswaram, Chinnakada , Kadapakkada , Meevaram KL- Pathanamthitta Pathanamthitta City, Kaipattoor, Omallur, Malayalapuzha, 03 Mylapra, Naranganam, Sabarigiri, Aranmula, Kozhencherri KL- Alappuzha Alappuzha city, Ambalappuzha, Aryad, Komalapuram, 04 Kommadi, Polathai, Thumboli, Punnapra , Kalavur , Ananthanarayanapuram KL- Kottayam Kottayam city, Kodimatha, Mannarcaud , Tirunnakara, 05 Nattakam, Tiruvarppu, Tiruvathikkal , Sankranthi , Vijayapuram KL- Idukki township Idukki, Painav 06 https://www.pdfformdownload.com/wp-admin/post-new.php 1/9 20/05/2021 Add New Post ‹ PDF Form Download — WordPress Code Office Name KL- Kochi Kochi Corporation Area, Kalamaserry, Kakkanad, Kochi SEZ, 07 Thrikkakara, Info Park, Smart City , Tiruvankulam , Brahmapuram KL- Thrissur Thrissur corporation, Ollur, Kuriachira, Ammaddam, 08 Ramavarmapuram, Parvattani, Kuttanellur KL- Palakkad Palakkad city, Kallepully, Kannadi, Mundur, Kanjikode, 09 Pathirippala. KL- Malappuram (Part of Malappuram, Manjeri, -

SEMESTER at SEA COURSE SYLLABUS University of Virginia, Academic Sponsor

SEMESTER AT SEA COURSE SYLLABUS University of Virginia, Academic Sponsor Voyage: Spring 2016 Discipline: Religious Studies RELG 1005-101: World Religions Division: Lower Faculty Name: Patrick T. McCormick Credit Hours: 3; Contact Hours: 38 Pre-requisites: None COURSE DESCRIPTION This course is an introduction to the world’s major religions, particularly the influential religious traditions in the countries we will visit in Asia and Africa. To live and work in a global village where we interact with people and communities from different religious traditions we need to understand and appreciate these neighbors’ religious worldviews. In this course we will examine and compare the beliefs, texts, figures, rituals, and shrines of the world’s most practiced religions and explore how these traditions answer life’s “big questions” (the meaning of existence, what happens after death, how life ought to be lived, etc.) and how they help their members to negotiate life’s crises and passages, and how they have functioned internally, and in relation to those outside them, as means for unity, division, solace and/or exploitation. COURSE OBJECTIVES Upon completion of this course, students will be able to: • Demonstrate familiarity with the basic beliefs, practices, texts, and rituals of the major religious traditions, especially the dominant traditions in the Asian and African nations we visit. • Compare and contrast the basic beliefs, practices, texts, and rituals of the major religious traditions we study in this course. • Analyze the basic principles of interfaith dialogue, instances of religious conflict, and processes and consequences of religion’s being imposed or adopted • Demonstrate understanding of how religion has been viewed and critiqued as a resource for building more peaceful and just societies. -

Birth Vs Merit. Kerala Temple Priests and the Courts Gilles Tarabout

Birth vs Merit. Kerala Temple Priests and the Courts Gilles Tarabout To cite this version: Gilles Tarabout. Birth vs Merit. Kerala Temple Priests and the Courts. Daniela Berti; Gilles Tarabout; Raphaël Voix. Filing Religion. State, Hinduism, and Courts of Law, Oxford University Press, pp.3-33, 2016, 978-0199463794. hal-01341078 HAL Id: hal-01341078 https://hal.archives-ouvertes.fr/hal-01341078 Submitted on 4 Jul 2016 HAL is a multi-disciplinary open access L’archive ouverte pluridisciplinaire HAL, est archive for the deposit and dissemination of sci- destinée au dépôt et à la diffusion de documents entific research documents, whether they are pub- scientifiques de niveau recherche, publiés ou non, lished or not. The documents may come from émanant des établissements d’enseignement et de teaching and research institutions in France or recherche français ou étrangers, des laboratoires abroad, or from public or private research centers. publics ou privés. [Published in Daniela Berti, Gilles Tarabout, and Raphaël Voix (eds), Filing Religion. State, Hinduism, and Courts of Law. New-Delhi, Oxford University Press: 3-33] /p.3/ [Chapter 1] Birth vs Merit. Kerala Temple Priests and the Courts Gilles Tarabout [National Center for Scientific Research (CNRS), Center for Ethnology and Comparative Sociology (LESC)]* In recent years, men born into various non-Brahmanical castes, including former ‘untouchables’, have been appointed as priests at Brahmanical public temples in Kerala. The constitutionality of such appointments has been challenged and was eventually upheld by the Supreme Court in 2002. This decision, I suggest, has to be seen as the outcome of developments by which the courts came to define priesthood in terms of technical procedures performed by expert, but ‘secular’ persons, i.e. -

1 Construction of 2BHK Housing Complex for GCDA at West

ONGOING PROJECTS (PMC & NON PMC) Sl No Name of Project Client Contract Amount/Agreement Construction of 2BHK Housing complex for GCDA at 1 West Rameshwaram, Fort Kochi, Eranakulam District GCDA 146,169,100.00 under LIFE Mission, Kerala Kerala Agro Industries 2 Establishment of Banana & Honey Park at Thrissur 119,208,792.00 Corporation Limited Construction of Karunagappally Municipal Tower in 3 Karunagappally Municipality 57,960,000.00 Division No.15 of Karunagappally Municipality 4 Construction of New Block at Fort Kochi Taluk Hospital KMRL/CSML 48,243,975.00 Construction of New Block Mattanchery Women & 5 KMRL/CSML 46,718,818.00 Children Hospittal 6 Construction of She Lodge at Kozhikkode Kozhikode corporation 41,679,244.00 Setting up of foundation work for 44 HP,20 HP 7 Defibering Units and Electrical Panel Board works - All KSCMMC- COIR BOARD 31,603,969.20 Kerala Construction of Training Center for Vegetable and Fruit 8 VFPCK 20,000,000.00 Promotion Council Keralam DMC, Kudumbashree, 9 Construction of houses for ST in Alappuzha Constituency 21,995,297.00 Alappuzha 10 Construction of Auditorium at Aliyavur Siva Temple DTPC 20,000,000.00 Repair and Maintenance work of Existing Auditorium of 11 KILA 10,000,000.00 KILA Construction of New water tank at KILA 12 KILA 9,000,000.00 ,Mulamkunnathukavu Construction of Auditorium at Kalampally Sri Durga 13 DTPC 8,000,000.00 Temple 14 Extension of Canteen Building at KILA KILA 5,000,000.00 Completion of commercial Institute Building in Marutha 15 District Panchayath ,Palakkad 5,000,000.00 Road -

Report on the Audit of Accounts of Cochin Devaswom Board for the Year 2016-17 (Dbar /2018)

1 REPORT ON THE AUDIT OF ACCOUNTS OF COCHIN DEVASWOM BOARD FOR THE YEAR 2016-17 (DBAR /2018) NO.KSA(CDB) C- 571/2018 Dated:14/09/2018 Audited by DEPUTY DIRECTOR OF KERALA STATE AUDIT, COCHIN DEVASWOM AUDIT THRISSUR 2 No.KSA (CDB) C-571 /2018 Office of the Deputy Director of Kerala State Audit, Cochin Devaswom Audit,Thrissur. Dated : 14.09.2018 Phone No.-0487 2322609 Email:[email protected] From The Deputy Director. To The Registrar, Honourable High Court of Kerala, Ernakulam. Sir, Sub: Cochin Devaswom Board –Audit Report for 2016-17 (DBAR - /2018) – Forwarded. The Report on the audit of accounts of Cochin Devaswom Board for the year 2016 - 17 in quadruplicate under section 102 to 104 of the Travancore Cochin Hindu Religious Institutions Act 1950 is forwarded herewith for favour of necessary action. A copy of the Report has been forwarded to the Secretary Cochin Devaswom Board also. It is requested that a copy of the proceedings issued on the consideration of the Audit Report by the Honourable High Court may kindly be forwarded to me for reference and guidance in future audit. Yours Faithfully, DEPUTY DIRECTOR. Encl: As above Copy to: 1) The Secretary, Cochin Devaswom Board, Thrissur. 2) The Director of Kerala State Audit Department, Thiruvananthapuram. (With C/L) 3) Spare. No. of Corrections: 3 CONTENTS PREFACE 4 OVERVIEW 5-7 CHAPTER 1 GENERAL 8-11 CHAPTER 2 FINANCE OF COCHIN 12-36 DEVASWOM BOARD CHAPTER 3 AUDIT OF RECEIPT 37-133 ACCOUNTS CHAPTER 4 AUDIT OF TRANSACTIONS 134-163 REVIEW OF AUDIT 164-165 APPENDICES 166-253 No.