Incentives and Tranche Retention in Securitisation: a Screening Model

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Mortgage-Backed Securities & Collateralized Mortgage Obligations

Mortgage-backed Securities & Collateralized Mortgage Obligations: Prudent CRA INVESTMENT Opportunities by Andrew Kelman,Director, National Business Development M Securities Sales and Trading Group, Freddie Mac Mortgage-backed securities (MBS) have Here is how MBSs work. Lenders because of their stronger guarantees, become a popular vehicle for finan- originate mortgages and provide better liquidity and more favorable cial institutions looking for investment groups of similar mortgage loans to capital treatment. Accordingly, this opportunities in their communities. organizations like Freddie Mac and article will focus on agency MBSs. CRA officers and bank investment of- Fannie Mae, which then securitize The agency MBS issuer or servicer ficers appreciate the return and safety them. Originators use the cash they collects monthly payments from that MBSs provide and they are widely receive to provide additional mort- homeowners and “passes through” the available compared to other qualified gages in their communities. The re- principal and interest to investors. investments. sulting MBSs carry a guarantee of Thus, these pools are known as mort- Mortgage securities play a crucial timely payment of principal and inter- gage pass-throughs or participation role in housing finance in the U.S., est to the investor and are further certificates (PCs). Most MBSs are making financing available to home backed by the mortgaged properties backed by 30-year fixed-rate mort- buyers at lower costs and ensuring that themselves. Ginnie Mae securities are gages, but they can also be backed by funds are available throughout the backed by the full faith and credit of shorter-term fixed-rate mortgages or country. The MBS market is enormous the U.S. -

Hedging Credit Index Tranches Investigating Versions of the Standard Model Christopher C

Hedging credit index tranches Investigating versions of the standard model Christopher C. Finger chris.fi[email protected] Risk Management Subtle company introduction www.riskmetrics.com Risk Management 22 Motivation A standard model for credit index tranches exists. It is commonly acknowledged that the common model is flawed. Most of the focus is on the static flaw: the failure to calibrate to all tranches on a single day with a single model parameter. But these are liquid derivatives. Models are not used for absolute pricing, but for relative value and hedging. We will focus on the dynamic flaws of the model. www.riskmetrics.com Risk Management 32 Outline 1 Standard credit derivative products 2 Standard models, conventions and abuses 3 Data and calibration 4 Testing hedging strategies 5 Conclusions www.riskmetrics.com Risk Management 42 Standard products Single-name credit default swaps Contract written on a set of reference obligations issued by one firm Protection seller compensates for losses (par less recovery) in the event of a default. Protection buyer pays a periodic premium (spread) on the notional amount being protected. Quoting is on fair spread, that is, spread that makes a contract have zero upfront value at inception. www.riskmetrics.com Risk Management 52 Standard products Credit default swap indices (CDX, iTraxx) Contract is essentially a portfolio of (125, for our purposes) equally weighted CDS on a standard basket of firms. Protection seller compensates for losses (par less recovery) in the event of a default. Protection buyer pays a periodic premium (spread) on the remaining notional amount being protected. New contracts (series) are introduced every six months. -

Non-Binding Summary of Terms Series a Preferred Stock Financing

NON-BINDING SUMMARY OF TERMS SERIES A PREFERRED STOCK FINANCING NewCo Biosciences, Inc. March 9, 2013 This Term Sheet summarizes the principal terms of the Series A Preferred Stock Financing of the Company. Issuer: NewCo Biosciences, Inc. (the “Company”). Investors: ABC Venture Partners IV, LP and its Affiliates (“ABC”), XYZ Partners, LP (“XYZ,” and each of ABC and XYZ, a “Co-Lead Investor”), and other investors approved by both Co-Lead Investors and the Company. Collectively, the Co-Lead Investors, the holders of the bridge notes on an as-converted basis (the “Bridge Note Holders”) and other investors and holders of Series A Preferred Stock shall be hereinafter known as Investors. Pursuant to the terms of the bridge notes, all outstanding bridge notes will convert into Series A Preferred Stock at the First Tranche Closing. Amount of Financing: $15,000,000 to $17,000,000 in two tranches (the “First Tranche” Comment [1]: The proposed and the “Second Tranche”, collectively, the “Tranches”) in the investment is a range since there may amounts set forth below (exclusive of debt converting at the First be other investors coming in or the Tranche Closing), with each such Tranche becoming due as set forth valuation may change during due in the “Closings” section below. diligence. § First Tranche: 40% of the total investment amount Comment [2]: To reduce their risk, the investors will allocate money in § Second Tranche:60% of the total investment amount two chunks or tranches, based on The Investors total capital commitments are as follows: milestones. For the company, this guarantees a stock price and valuation § ABC: Up to $5,000,000 for a significant period of time, reducing the amount of negotiations § XYZ: Up to $8,000,000 required for a series B. -

Modern Money Mechanics

Modern Money Mechanics A Workbook on Bank Reserves and Deposit Expansion Federal Reserve Bank of Chicago Modern Money Mechanics The purpose of this booklet is to desmmbethe basic Money is such a routine part of everyday living that process of money creation in a ~actionalreserve" bank- its existence and acceptance ordinarily are taken for grant- ing system. l7ze approach taken illustrates the changes ed. A user may sense that money must come into being either automatically as a result of economic activity or as in bank balance sheets that occur when deposits in banks an outgrowth of some government operation. But just how change as a result of monetary action by the Federal this happens all too often remains a mystery. Reserve System - the central bank of the United States. What Is Money? The relationships shown are based on simplil5ring If money is viewed simply as a tool used to facilitate assumptions. For the sake of simplicity, the relationships transactions, only those media that are readily accepted in are shown as if they were mechanical, but they are not, exchange for goods, services, and other assets need to be as is described later in the booklet. Thus, they should not considered. Many things -from stones to baseball cards be intwreted to imply a close and predictable relation- -have served this monetary function through the ages. Today, in the United States, money used in transactions is ship between a specific central bank transaction and mainly of three kinds -currency (paper money and coins the quantity of money. in the pockets and purses of the public); demand deposits The introductory pages contain a briefgeneral (non-interest-bearingchecking accounts in banks); and other checkable deposits, such as negotiable order of desm'ption of the characte*ics of money and how the withdrawal (NOW)accounts, at all depository institutions, US. -

How Risky Are Structured Exposures Compared with Corporate Bonds?

How Risky are Structured Exposures Compared with Corporate Bonds? William Perraudina and Astrid Van Landschootb a Imperial College and Bank of England b National Bank of Belgium Abstract This paper compares the risk of structured exposures with that of defaultable corporate bonds with the same agency ratings. Risk is defined in a variety of ways including return volatility, value-at-risk, expected shortfall and betas with credit portfolios. * The views expressed are those of the authors and not of the institutions to which they are affiliated. 1 Introduction Understanding the relative risks involved in investing in different sectors of credit markets will always be important for market participants and regulators alike. However, the debate about capital initiated by the Basel Committee’s recently published proposals on regulatory capital make this issue especially topical (See Basel Committee on Banking Supervision (2004)). In brief, the Committee’s proposals involve requiring each bank to hold capital to cover its banking book credit exposures largely based on the rating of these exposures.1 For bonds and loans, the ratings for most banks will be internally generated based on systems approved by supervisors. For structured products, the ratings will be mostly agency ratings provided by the major international rating agencies. Whether internal or external, the rating for an exposure is based on its expected loss or default probability. These aspects of an exposure are not the same as the exposure’s unexpected loss, which is generally thought to be an appropriate basis for setting capital. But experience suggests that, for reasonably homogeneous categories of assets, one may expect to find a stable relationship between expected loss and default probabilities and hence ratings on the one hand and unexpected loss and hence capital on the other hand. -

Glossary of Bond Terms

Glossary of Bond Terms Accreted value- The current value of your zero-coupon municipal bond, taking into account interest that has been accumulating and automatically reinvested in the bond. Accrual bond- Often the last tranche in a CMO, the accrual bond or Z-tranche receives no cash payments for an extended period of time until the previous tranches are retired. While the other tranches are outstanding, the Z-tranche receives credit for periodic interest payments that increase its face value but are not paid out. When the other tranches are retired, the Z-tranche begins to receive cash payments that include both principal and continuing interest. Accrued interest- (1) The dollar amount of interest accrued on an issue, based on the stated interest rate on that issue, from its date to the date of delivery to the original purchaser. This is usually paid by the original purchaser to the issuer as part of the purchase price of the issue; (2) Interest deemed to be earned on a security but not yet paid to the investor. Active tranche- A CMO tranche that is currently paying principal payments to investors. Adjustable-rate mortgage (ARM)- A mortgage loan on which interest rates are adjusted at regular intervals according to predetermined criteria. An ARM's interest rate is tied to an objective, published interest rate index. Amortization- Liquidation of a debt through installment payments. Arbitrage- In the municipal market, the difference in interest earned on funds borrowed at a lower tax-exempt rate and interest on funds that are invested at a higher-yielding taxable rate. -

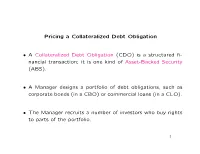

Pricing a Collateralized Debt Obligation • a Collateralized Debt

Pricing a Collateralized Debt Obligation • A Collateralized Debt Obligation (CDO) is a structured fi- nancial transaction; it is one kind of Asset-Backed Security (ABS). • A Manager designs a portfolio of debt obligations, such as corporate bonds (in a CBO) or commercial loans (in a CLO). • The Manager recruits a number of investors who buy rights to parts of the portfolio. 1 • Each investor buys the right to receive certain cash flows derived from the portfolio, divided into tranches. • The senior tranche has first call on the cash flows (interest and principal), up to a set percentage. • The junior tranche has next call, again up to a set percent- age. • Remaining cash flows are passed through to the equity tranche. 2 • Simplified example: suppose that the portfolio consists of two corporate bonds, B1 and B2, and neither pays interest. • The bonds are priced at b1 and b2 at t = 0. • Each bond returns 1 at t = T if its issuer is not in default, and 0 if the issuer has defaulted. • The matrix D is: In default: Neither Issuer 1 Issuer 2 Both Cash erT erT erT erT B1 1 0 1 0 B2 1 1 0 0 3 • D is 3×4, so N = 3 < n = 4, and the market is not complete. • Now 0 1 1 B C S0 = @ b1 A : b2 −rT • If 0 < bi < e ; i = 1; 2, then S0 = D where 0 1 (1 − p1)(1 − p2) B (1 ) C −rT B p1 − p2 C = e B C @ (1 − p1) p2 A p1p2 rT and pi = 1 − e bi; i = 1; 2. -

Incentives and Tranche Retention in Securitisation: a Screening Model

Incentives and Tranche Retention in Securitisation: A Screening Model Ingo Fender (Bank for International Settlements) and Janet Mitchell (National Bank of Belgium and CEPR)y First draft: November, 2008z This draft: May, 2009 Abstract This paper examines the power of di¤erent contractual mechanisms to in‡uence an originator’schoice of costly e¤ort to screen borrowers when the originator plans to securitise its loans. The analysis focuses on three potential mechanisms: the originator holds a “vertical slice”, or share of the portfolio; the originator holds the equity tranche of a structured …nance transaction; the originator holds the mezzanine tranche, rather than the equity tranche. These mechanisms will result in di¤ering levels of screening, and the di¤erences arise from varying sensitivities to a systematic risk factor. Equity tranche retention is not always the most e¤ective mechanism. The equity tranche can be dominated by either a vertical slice or a mezzanine tranche if the probability of a downturn is likely and if the equity tranche is likely to be depleted in a downturn. In addition, a vertical slice is unlikely to dominate both the equity tranche and the mezzanine tranche, unless the vertical slice is very "thick". Monetary and Economic Department, Bank for International Settlements, Central- bahnplatz 2, 4002 Basel, Switzerland, tel: +41 61 280 8415, email: [email protected] yFinancial Stability Department, National Bank of Belgium, Boulevard de Berlaimont 14, B-1000 Brussels, Belgium, tel: +32 2 221 3459, email: [email protected] zThe views expressed in this paper remain those of the authors and do not necessarily re‡ect those of the BIS or the NBB. -

Banknotes Week Ended 28 November 2014

NEWSLETTER FINANCIAL SERVICES Banknotes Week ended 28 November 2014 KPMG China’s weekly banking news summary This publication is a summary of publicly reported information, the accuracy of which has not been verified by KPMG. In the news Bank of China News China Merchants Bank Commerzbank AG signed an agreement with BOC for direct RMB settlement – Commerzbank AG signed an agreement with Bank of China (BOC) to establish a Commerzbank AG RMB clearing centre for direct settlement of RMB payments in Frankfurt, Germany. Industrial Bank Co., Ltd. CMB issues RMB bonds in Hong Kong – China Merchants Bank (CMB) agreed to People’s Bank of China issue two tranches of RMB bonds of 1,000 million each under its medium term note programme. The first tranche will be 3-year bonds with 3.95% coupon due in December 2017 while the second tranche will be 5-year bonds with 4.05% coupon due in December 2019. The net proceeds will be used for working capital and general corporate purposes. Industrial Bank Co., Ltd. granted approval from CSRC for preferred share private placement – Industrial Bank Co., Ltd. has received approval from the China Securities Regulatory Commission (CSRC) to issue a maximum of 260 million preferred shares under a private placement. © 2014 KPMG, a Hong Kong partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity In brief PBOC plans to launch bank deposit insurance system – People’s Bank of China (PBOC) has released details of a draft bank deposit insurance system which will cover mainland bank deposits up to RMB 500,000. -

Optimal Structuring of Collateralized Debt Obligation Contracts: an Optimization Approach

Journal of Credit Risk Volume 8/Number 4, Winter 2012/13 (133–155) Optimal structuring of collateralized debt obligation contracts: an optimization approach Alexander Veremyev Risk Management and Financial Engineering Lab, Department of Industrial and Systems Engineering, University of Florida, 303 Weil Hall, Gainesville, FL 32611, USA; email: [email protected] Peter Tsyurmasto Risk Management and Financial Engineering Lab, Department of Industrial and Systems Engineering, University of Florida, 303 Weil Hall, Gainesville, FL 32611, USA; email: [email protected] Stan Uryasev Risk Management and Financial Engineering Lab, Department of Industrial and Systems Engineering, University of Florida, 303 Weil Hall, Gainesville, FL 32611, USA; email: [email protected] The objective of this paper is to help a bank originator of a collateralized debt obligation (CDO) to build a maximally profitable CDO. We consider an opti- mization framework for structuring CDOs. The objective is to select attachment/ detachment points and underlying instruments in the CDO pool. In addition to “standard” CDOs we study so-called “step-up” CDOs. In a standard CDO con- tract the attachment/detachment points are constant over the life of a CDO. In a step-up CDO the attachment/detachment points may change over time. We show that step-up CDOs can save about 25–35% of tranche spread payments (ie, prof- itability of CDOs can be boosted by about 25–35%). Several optimization mod- els are developed from the bank originator perspective. We consider a synthetic CDO where the goal is to minimize payments for the credit risk protection (pre- mium leg), while maintaining a specific credit rating (assuring the credit spread) of each tranche and maintaining the total incoming credit default swap spread payments. -

Securitisations: Tranching Concentrates Uncertainty1

Adonis Antoniades Nikola Tarashev [email protected] [email protected] Securitisations: tranching concentrates uncertainty1 Even when securitised assets are simple, transparent and of high quality, risk assessments will be uncertain. This will call for safeguards against potential undercapitalisation. Since the uncertainty concentrates mainly in securitisation tranches of intermediate seniority, the safeguards applied to these tranches should be substantial, proportionately much larger than those for the underlying pool of assets. JEL classification: G24, G32. The past decade has witnessed the spectacular rise of the securitisation market, its dramatic fall and, recently, its timid revival. Much of this evolution reflected the changing fortunes of securitisations that were split into tranches of different seniority. Initially, such securitisations appealed strongly to investors searching for yield, as well as to banks seeking to reduce regulatory capital through the sale of judiciously selected tranches.2 Then, the financial crisis exposed widespread underestimation of tranche riskiness and illustrated that even sound risk assessments were not immune to substantial uncertainty. The crisis sharpened policymakers’ awareness that addressing the uncertainty in risk assessments is a precondition for a sustainable revival of the securitisation market. Admittedly, constructing simple and transparent asset pools would be a step towards reducing some of this uncertainty. That said, substantial uncertainty would remain and would concentrate in particular securitisation tranches. Despite the simplicity and transparency of the underlying assets, these tranches would not be simple. We focus on the uncertainty inherent in estimating the risk parameters of a securitised pool and study how it translates into uncertainty about the distribution of losses across tranches of different seniority. -

Markit Credit Indices Primer

Markit Credit Indices Primer Markit Credit Indices A Primer July 2014 1 Confidential. Copyright © 2013, Markit Group Limited. All rights reserved. www.markit.com Markit Credit Indices Primer Copyright © 2014 Markit Group Limited Any reproduction, in full or in part, in any media without the prior written permission of Markit Group Limited will subject the unauthorized party to civil and criminal penalties. Trademarks Mark-it™, Markit™, CDX™, LCDX™, ABX, CMBX, MCDX, SovX, Markit Loans™, Markit RED™, Markit Connex™, Markit Metrics™ iTraxx®, LevX® and iBoxx® are trademarks of Markit Group Limited. Other brands or product names are trademarks or registered trademarks of their respective holders and should be treated as such. Limited Warranty and Disclaimer Markit specifically disclaims any implied warranty or merchantability or fitness for a particular purpose. Markit does not warrant that the use of this publication shall be uninterrupted or error free. In no event shall Markit be liable for any damages, including without limitation, direct damages, punitive or exemplary damages, damages arising from loss of data, cost of cover, or other special, incidental, consequential or indirect damages of any description arising out of the use or inability to use the Markit system or accompanying documentation, however caused, and on any theory of liability. This guide may be updated or amended from time to time and at any time by Markit in its sole and absolute discretion and without notice thereof. Markit is not responsible for informing any client of, or providing any client with, any such update or amendment. 2 Copyright © 2014, Markit Group Limited. All rights reserved.