Always Driven Contents

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

LAGUNA LAKE DEVELOPMENT AUTHORITY National Ecology Center, East Avenue, Diliman, Quezon City Phone Nos

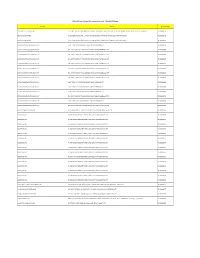

LAGUNA LAKE DEVELOPMENT AUTHORITY National Ecology Center, East Avenue, Diliman, Quezon City Phone Nos. (02) 8 376-4039, (02) 8 376-4072, (02) 8 376-4044, (02) 8 332-2353, (02) 8 332-2341, (02) 8 376-5430 Locals 115, 116, 117 and look for Ms. Julie Ann G. Blanquisco or Ms. Marivic A. Dela Torre-Santos E-mail: [email protected] | [email protected] Website: http://llda.gov.ph List of APPROVED DISCHARGE PERMITS as of September 03, 2021 Establishment Address Permit No. Approve Date 11 FTC Enterprises, Inc. 236 P. Dela Cruz San Bartolome Quezon City MM DP-25b-2021-03532 August 18, 2021 189 Realty Corp. (CI Market) Qurino Highway Santa Monica, Novaliches Quezon City MM DP-25b-2021-03744 August 20, 2021 189 Realty Corporation - 2nd (CI Market/Commercial Complex) Quirino Highway, Sta. Monica Novaliches Quezon City MM DP-25b-2021-03743 August 20, 2021 21st Century Mouldings Corporation 18 F. Carlos St. cor. Howmart Road Apolonio Samson Quezon City MM DP-25b-2021-03541 August 23, 2021 24K Property Ventures, Inc. (20 Lansbergh Place Condominium) 170 T. Morato Ave. cor. Sct. Castor Sacred Heart Quezon City MM DP-25b-2021-02819 July 15, 2021 3J Foods Corp. Sta. Ana San Pablo City Laguna DP-16d-2021-03174 August 06, 2021 8 Gilmore Place Condominium 8 Gilmore Ave. cor. 1st St. Valencia New Manila Quezon City MM DP-25b-2021-03829 August 27, 2021 AC Technical Services, Inc. 5 RMT Ind`l. Complex Tunasan Muntinlupa City MM DP-23a-2021-01804 May 12, 2021 Ace Roller Manufacturing, Inc. -

Familymart Branches

Sheet1 Participating FamilyMart Branches BRANCH ADDRESS CONTACT NUMBER G/F 139 CORPORATE CENTER, VALERO ST. 0917-8129710 139 CORPORATE SALCEDO VILLAGE, MAKATI CITY 978-0109 G/F STALL 21 ELJ COMMUNICATIONS 964-8279 ABS - CBN CENTER, QUEZON CITY 0917-5225533 GF AEON PRIME BUILDING, ALABANG- AEON PRIME ZAPOTE ROAD COR. NORTHGATE 0917-8458988 BRIDGEWAY, MUNTINLUPA CITY G/F UNIT 1-4, AIC GRAND DE TOWER, 0917-846-0651 AIC GRANDE TOWER GARNET ROAD, ORTIGAS CENTER, PASIG 507-6348 CITY G/F ALCO BLDG. 391 SEN. GIL PUYAT ALCO BLDG 954-1585 MAKATI CITY G/F ALPHALAND SOUTHGATE MALL EDSA 0917-5827526 ALPHALAND COR. PASONG TAMO ST. MAKATI CITY 959-0832 LG/F UNIT 7 ANONAS LRT CITY CENTER 978-0131 ANONAS LRT AURORA BLVD. & ANONAS ST. PROJECT 3 0917-8057206 QUEZON CITY AVIDA TOWERS NEW MANILA (TOWER# 5), 0917-8466236 AVIDA NEW MANILA B. SERRANO AVE., BRGY. BAGONG LIPUNAN 964-1352 NG CRAME, QUEZON CITY G/F RETAIL SPACE 2-4, AVIDA TOWERS SAN 0917-8940484 AVIDA SAN LORENZO LORENZO, CHINO ROCES AVE., MAKATI CITY 964-1499 959-1275 AYALA MRT 2/F AYALA MRT STATION 3 MAKATI CITY 09178207217 G/F C1 AYALA TOWER ONE & EXCHANGE AYALA TOWER ONE PLAZA AYALA TRIANGLE AYALA AVE. MAKATI 625 - 0446 CITY AYALA TRIANGLE GARDENS AYALA AVE., AYALA TRIANGLE GARDENS 729-7962 MAKATI CITY 11th AVE COR 30th ST., BONIFACIO GLOBAL 0917-5818190 BGC CORP CITY 978-0138 G/F BLDG K, BLUE BAYWALK MACAPAGAL, 0917-8103789 BLUE BAYWALK EDSA EXT. COR. MACAPAGAL AVE. 218-9335 METROPARK, PASAY CITY G/F SPACE #3 BONIFACIO ONE TECHNOLOGY TOWER RIZAL DRIVE COR. -

SAN JOSE KOOP CONTENTS SAN JOSE DEL MONTE SAVINGS and COOPERATIVE 1 - Chairperson’S Corner

SAN JOSE KOOP CONTENTS SAN JOSE DEL MONTE SAVINGS AND COOPERATIVE 1 - Chairperson’s Corner 2-11 - Regular Activities ● Grand Opening Minuyan Satellite Office ManaGEMENT BoaRD CHAIRPERSON ● 4th Business Forum CHAIR. ROMEO A. DE JESUS ● Cake Decorating Seminar / Feeding Program CHIEF EXECUTIVE OFFICER CEO CAROLINE D. DAVE & Rice Donation for Home for the Elderly LEGAL COUNSEL ● Officers Retreat ATTY. RODELIO B. PUNZALAN ● 2019 Gawad Parangal / 2nd Laboratory Test EDITORIAL BoaRD ● Senior Citizen’s Day EDITOR-IN-CHIEF MS. MARISSA C. PANTALEON ● Multi Cab Donation ASSOCIATE EDITORS ● Sister Society “Rachael Reilling visits” MR. MORRIS DANIEL BRODITH ● Basic Baking Seminar CONTRIBUTOR DIR. JOVITA V. MATEO DIR. JOHN PAUL VILLAR ● ACCESS Renewal MS. NANCY MAGNO MS. MICHELLE CRUZ VILLANUEVA 12-13 - Main Event MS. CAROLINE D. DAVE MR. RUDOLF Z. GADO ● SSS Moa Signing MS. MARY GRACE B. ALE MS. GLENDA M. LORENZO 14 –Skylab Corner MR. EUGENE D. CABUHAT MS. MARY ANN ANGEL DOMINGO MS. RASEL STA. MARIA 15 - Member’s Corner MR. MIA GRACE V. EVANGELISTA 16 - GAD Corner’s EDITORIAL OFFICE 17-24 - For Your Information OFFICE MANAGER ● Financial Highlight as of September 2019 MS. NYRALYN N. DELA TORRE ● Policy Updates GRAPHIC ARTIST MR. MORRIS DANIEL BRODITH ● Featured Products ● San Jose Koop Partners MASIKAP o MAgasing SInasalamin ang KAPatiran ng mga MAmamayang SImbolo ng KAunlaran at Pag-asa is the ● Abuluyan Program 3rd Quarter 2019 official gazette of the San Jose Del Monte Savings and Credit Cooperative published quarterly with the editorial office at ADMIN ● Loyalty Program Office 2nd Floor SJDMSCC Building, San Pedro St. Poblacion 1, City of San Jose del Monte, Bulacan 3023, Philippines. -

No. Company Star

Fair Trade Enforcement Bureau-DTI Business Licensing and Accreditation Division LIST OF ACCREDITED SERVICE AND REPAIR SHOPS As of November 30, 2019 No. Star- Expiry Company Classific Address City Contact Person Tel. No. E-mail Category Date ation 1 (FMEI) Fernando Medical Enterprises 1460-1462 E. Rodriguez Sr. Avenue, Quezon City Maria Victoria F. Gutierrez - Managing (02)727 1521; marivicgutierrez@f Medical/Dental 31-Dec-19 Inc. Immculate Concepcion, Quezon City Director (02)727 1532 ernandomedical.co m 2 08 Auto Services 1 Star 4 B. Serrano cor. William Shaw Street, Caloocan City Edson B. Cachuela - Proprietor (02)330 6907 Automotive (Excluding 31-Dec-19 Caloocan City Aircon Servicing) 3 1 Stop Battery Shop, Inc. 1 Star 214 Gen. Luis St., Novaliches, Quezon Quezon City Herminio DC. Castillo - President and (02)9360 2262 419 onestopbattery201 Automotive (Excluding 31-Dec-19 City General Manager 2859 [email protected] Aircon Servicing) 4 1-29 Car Aircon Service Center 1 Star B1 L1 Sheryll Mirra Street, Multinational Parañaque City Ma. Luz M. Reyes - Proprietress (02)821 1202 macuzreyes129@ Automotive (Including 31-Dec-19 Village, Parañaque City gmail.com Aircon Servicing) 5 1st Corinthean's Appliance Services 1 Star 515-B Quintas Street, CAA BF Int'l. Las Piñas City Felvicenso L. Arguelles - Owner (02)463 0229 vinzarguelles@yah Ref and Airconditioning 31-Dec-19 Village, Las Piñas City oo.com (Type A) 6 2539 Cycle Parts Enterprises 1 Star 2539 M-Roxas Street, Sta. Ana, Manila Manila Robert C. Quides - Owner (02)954 4704 iluvurobert@gmail. Automotive 31-Dec-19 com (Motorcycle/Small Engine Servicing) 7 3BMA Refrigeration & Airconditioning 1 Star 2 Don Pepe St., Sto. -

1623400766-2020-Sec17a.Pdf

COVER SHEET 2 0 5 7 3 SEC Registration Number M E T R O P O L I T A N B A N K & T R U S T C O M P A N Y (Company’s Full Name) M e t r o b a n k P l a z a , S e n . G i l P u y a t A v e n u e , U r d a n e t a V i l l a g e , M a k a t i C i t y , M e t r o M a n i l a (Business Address: No. Street City/Town/Province) RENATO K. DE BORJA, JR. 8898-8805 (Contact Person) (Company Telephone Number) 1 2 3 1 1 7 - A 0 4 2 8 Month Day (Form Type) Month Day (Fiscal Year) (Annual Meeting) NONE (Secondary License Type, If Applicable) Corporation Finance Department Dept. Requiring this Doc. Amended Articles Number/Section Total Amount of Borrowings 2,999 as of 12-31-2020 Total No. of Stockholders Domestic Foreign To be accomplished by SEC Personnel concerned File Number LCU Document ID Cashier S T A M P S Remarks: Please use BLACK ink for scanning purposes. 2 SEC Number 20573 File Number______ METROPOLITAN BANK & TRUST COMPANY (Company’s Full Name) Metrobank Plaza, Sen. Gil Puyat Avenue, Urdaneta Village, Makati City, Metro Manila (Company’s Address) 8898-8805 (Telephone Number) December 31 (Fiscal year ending) FORM 17-A (ANNUAL REPORT) (Form Type) (Amendment Designation, if applicable) December 31, 2020 (Period Ended Date) None (Secondary License Type and File Number) 3 SECURITIES AND EXCHANGE COMMISSION SEC FORM 17-A ANNUAL REPORT PURSUANT TO SECTION 17 OF THE SECURITIES REGULATION CODE AND SECTION 141 OF CORPORATION CODE OF THE PHILIPPINES 1. -

JEEP Bus Time Schedule & Line Route

JEEP bus time schedule & line map JEEP Kamuning - Vito Cruz via E. Rodriguez, Mabini View In Website Mode The JEEP bus line (Kamuning - Vito Cruz via E. Rodriguez, Mabini) has 2 routes. For regular weekdays, their operation hours are: (1) Hp Village Square, Pablo Ocampo Sr., Manila →Kamuning Rd / Scout Rallos Extension Intersection, Quezon City, Manila: 12:00 AM - 11:00 PM (2) Kamuning Rd / Scout Rallos Extension Intersection, Quezon City, Manila →Hp Village Square, Pablo Ocampo Sr., Manila: 12:00 AM - 11:00 PM Use the Moovit App to ƒnd the closest JEEP bus station near you and ƒnd out when is the next JEEP bus arriving. Direction: Hp Village Square, Pablo Ocampo Sr., JEEP bus Time Schedule Manila →Kamuning Rd / Scout Rallos Extension Hp Village Square, Pablo Ocampo Sr., Intersection, Quezon City, Manila Manila →Kamuning Rd / Scout Rallos Extension Intersection, Quezon City, Manila Route Timetable: 43 stops VIEW LINE SCHEDULE Sunday 12:00 AM - 10:00 PM Monday 12:00 AM - 11:00 PM Hp Village Square, Pablo Ocampo Sr., Manila Tuesday 12:00 AM - 11:00 PM Hospital, A.Mabini, Manila Wednesday 12:00 AM - 11:00 PM A.Mabini, Manila Thursday 12:00 AM - 11:00 PM A.Mabini, Manila Friday 12:00 AM - 11:00 PM 1770 Apolinario Mabini, Philippines Saturday 12:00 AM - 10:00 PM A.Mabini, Manila 1588 Pedro Gil, Philippines Sta. Monica / A.Mabini Intersection, Manila Santa Monica, Philippines JEEP bus Info Direction: Hp Village Square, Pablo Ocampo Sr., Mayfair Tower, United Nations Ave, Manila Manila →Kamuning Rd / Scout Rallos Extension United Nations Avenue, Philippines Intersection, Quezon City, Manila Stops: 43 T.M. -

Malolos-Clark Railway Project – Tranche 1 Volume I

Environmental Monitoring Report Semi-annual Environmental Monitoring Report No. 1 March 2020 PHI: Malolos-Clark Railway Project – Tranche 1 Volume I September 2019 – March 2020 Prepared by the Project Management Office (PMO) of the Department of Transportation (DOTr) for the Government of the Republic of the Philippines and the Asian Development Bank. CURRENCY EQUIVALENTS (as of 30 March 2020) Currency unit – Philippine Peso (PHP) PHP1.00 = $0.02 $1.00 = PHP50.96 ABBREVIATIONS ADB – Asian Development Bank BMB – Biodiversity Management Bureau Brgy – Barangay CCA – Climate Change Adaptation CCC – Climate Change Commission CDC – Clark Development Corporation CEMP – Contractor’s Environmental Management Plan CENRO – City/Community Environment and Natural Resources Office CIA – Clark International Airport CIAC – Clark International Airport Corporation CLLEx – Central Luzon Link Expressway CLUP – Comprehensive Land Use Plan CMR – Compliance Monitoring Report CMVR – Compliance Monitoring and Validation Report CNO – Certificate of No Objection CPDO – City Planning and Development Office DAO – DENR Administrative Order DD / DED – Detailed Design Stage / Detailed Engineering Design Stage DENR – Department of Environment and Natural Resources DepEd – Department of Education DIA – Direct Impact Area DILG – Department of Interior and Local Government DOH – Department of Health DOST – Department of Science and Technology DOTr – Department of Transportation DPWH – Department of Public Works and Highways DSWD – Department of Social Welfare and Development -

Population by Barangay National Capital Region

CITATION : Philippine Statistics Authority, 2015 Census of Population Report No. 1 – A NATIONAL CAPITAL REGION (NCR) Population by Province, City, Municipality, and Barangay August 2016 ISSN 0117-1453 ISSN 0117-1453 REPORT NO. 1 – A 2015 Census of Population Population by Province, City, Municipality, and Barangay NATIONAL CAPITAL REGION Republic of the Philippines Philippine Statistics Authority Quezon City REPUBLIC OF THE PHILIPPINES HIS EXCELLENCY PRESIDENT RODRIGO R. DUTERTE PHILIPPINE STATISTICS AUTHORITY BOARD Honorable Ernesto M. Pernia Chairperson PHILIPPINE STATISTICS AUTHORITY Lisa Grace S. Bersales, Ph.D. National Statistician Josie B. Perez Deputy National Statistician Censuses and Technical Coordination Office Minerva Eloisa P. Esquivias Assistant National Statistician National Censuses Service ISSN 0117-1453 Presidential Proclamation No. 1269 Philippine Statistics Authority TABLE OF CONTENTS Foreword v Presidential Proclamation No. 1269 vii List of Abbreviations and Acronyms xi Explanatory Text xiii Map of the National Capital Region (NCR) xxi Highlights of the Philippine Population xxiii Highlights of the Population : National Capital Region (NCR) xxvii Summary Tables Table A. Population and Annual Population Growth Rates for the Philippines and Its Regions, Provinces, and Highly Urbanized Cities: 2000, 2010, and 2015 xxxi Table B. Population and Annual Population Growth Rates by Province, City, and Municipality in National Capital Region (NCR): 2000, 2010, and 2015 xxxiv Table C. Total Population, Household Population, -

DOLE-NCR for Release AEP Transactions As of 7-16-2020 12.05Pm

DOLE-NCR For Release AEP Transactions as of 7-16-2020 12.05pm Company Address Transaction No. 3M SERVICE CENTER APAC, INC. 17TH, 18TH, 19TH FLOORS, BONIFACIO STOPOVER CORPORATE CENTER, 31ST STREET COR., 2ND AVENUE, BONIFACIO GLOBAL CITY, TAGUIG CITY TNCR20000756 3O BPO INCORPORATED 2/F LCS BLDG SOUTH SUPER HIGHWAY, SAN ANDRES COR DIAMANTE ST, 087 BGY 803, SANTA ANA, MANILA TNCR20000178 3O BPO INCORPORATED 2/F LCS BLDG SOUTH SUPER HIGHWAY, SAN ANDRES COR DIAMANTE ST, 087 BGY 803, SANTA ANA, MANILA TNCR20000283 8 STONE BUSINESS OUTSOURCING OPC 5-10/F TOWER 1, PITX KENNEDY ROAD, TAMBO, PARAÑAQUE CITY TNCR20000536 8 STONE BUSINESS OUTSOURCING OPC 5TH-10TH/F TOWER 3, PITX #1, KENNEDY ROAD, TAMBO, PARAÑAQUE CITY TNCR20000554 8 STONE BUSINESS OUTSOURCING OPC 5TH-10TH/F TOWER 3, PITX #1, KENNEDY ROAD, TAMBO, PARAÑAQUE CITY TNCR20000569 8 STONE BUSINESS OUTSOURCING OPC 5TH-10TH/F TOWER 3, PITX #1, KENNEDY ROAD, TAMBO, PARAÑAQUE CITY TNCR20000607 8 STONE BUSINESS OUTSOURCING OPC 5TH-10TH/F TOWER 3, PITX #1, KENNEDY ROAD, TAMBO, PARAÑAQUE CITY TNCR20000617 8 STONE BUSINESS OUTSOURCING OPC 5TH-10TH/F TOWER 3, PITX #1, KENNEDY ROAD, TAMBO, PARAÑAQUE CITY TNCR20000632 8 STONE BUSINESS OUTSOURCING OPC 5TH-10TH/F TOWER 3, PITX #1, KENNEDY ROAD, TAMBO, PARAÑAQUE CITY TNCR20000633 8 STONE BUSINESS OUTSOURCING OPC 5TH-10TH/F TOWER 3, PITX #1, KENNEDY ROAD, TAMBO, PARAÑAQUE CITY TNCR20000638 8 STONE BUSINESS OUTSOURCING OPC 5-10/F TOWER 1, PITX KENNEDY ROAD, TAMBO, PARAÑAQUE CITY TNCR20000680 8 STONE BUSINESS OUTSOURCING OPC 5-10/F TOWER 1, PITX KENNEDY -

Marikina City Disaster Coordinating Council Preparedness Program

MARIKINA CITY DISASTER COORDINATING COUNCIL PREPAREDNESS PROGRAM A BRIEF HISTORY OF THE MARIKINA DISASTER COORDINATING COUNCIL Marikina Valley is located in the Eastern part of Metro Manila, on the Western part of the city, you can find the Marikina River. alongside of it is the Valley Fault Line. No place in the Philippines can you find two disaster prone areas in one place. We have no choice but TO BE PREPARED. 1 In 1992 upon the assumption to office of Mayor Bayani F. Fernando, he reactivated the Marikina Disaster Coordinating Council. Although in the previous administrations such body was already in existence but when disaster strikes or damage occurs only then will this council operates or activates or what we call reactive response. Under the present administration all disaster scenarios are addressed to 3 levels namely the pre-disaster, disaster and post-disaster periods with more emphasis on the preparedness aspect of the plan which makes the big difference in dealing with these man-made, natural disaster or calamity. The Marikina City Disaster Preparedness Plan was already tested and proven to be very effective not once but many times when our city faces disasters, not only in our locality but also when we are asked to extend help and assistance to our neighboring cities like the Cherry Hills landslide in Antipolo City and the recent Payatas tragedy in Quezon City. 2 Our mission in this program is to prepare our community and most especially, the entire government machinery to anticipate the onset of and respond to any disaster thus bringing the number of casualties or damages at a minimum level and to provide an integrated direction and control of manpower, material, monetary and other necessary resources that can be made available and responsive to the disasters and calamities which may occur in the City of Marikina. -

Top 100 Stockholders As of June 30, 2011

BPI STOCK TRANSFER OFFICE MANCHESTER INTERNATIONAL HOLDINGS UNLIMITED CORP. TOP 100 STOCKHOLDERS AS OF JUNE 30, 2011 RANK STOCKHOLDER NUMBER STOCKHOLDER NAME NATIONALITY CERTIFICATE CLASS OUTSTANDING SHARES PERCENTAGE TOTAL 1 09002935 INTERPHARMA HOLDINGS & MANAGEMENT CORPORATION FIL A 255,264,483 61.9476% 255,264,483 C/O INTERPHIL LABORATORIES INC KM. 21 SOUTH SUPERHIGHWAY 1702 SUKAT, MUNTINLUPA, M. M. 2 1600000001 PHARMA INDUSTRIES HOLDINGS LIMITED BRT B 128,208,993 31.1138% 128,208,993 C/O ZUELLIG BUILDING, SEN. GIL J. PUYAT AVENUE, MAKATI CITY 3 16015506 PCD NOMINEE CORPORATION (FILIPINO) FIL A 10,969,921 G/F MKSE. BLDG, 6767 AYALA AVE MAKATI CITY B 8,258,342 4.6663% 19,228,263 4 16009811 PAULINO G. PE FIL A 181,250 29 NORTH AVENUE, DILIMAN, QUEZON CITY B 575,000 0.1835% 756,250 5 10002652 KASIGOD V. JAMIAS FIL A 464,517 109 APITONG ST., AYALA ALABANG MUNTINLUPA, METRO MANILA B 106,344 0.1385% 570,861 6 16011629 PCD NOMINEE CORPORATION (NON-FILIPINO) NOF B 393,750 0.0955% 393,750 G/F MKSE BUILDING 6767 AYALA AVENUE MAKATI CITY 7 16010090 PUA YOK BING FIL A 375,000 0.0910% 375,000 509 SEN. GIL PUYAT AVE. EXT. NORTH FORBES PARK MAKATI CITY 8 16009868 PAULINO G. PE FIL B 240,000 0.0582% 240,000 29 NORTH AVENUE, DILIMAN, QUEZON CITY 9 03030057 ROBERT S. CHUA FIL A 228,750 0.0555% 228,750 C/O BEN LINE, G/F VELCO CENTER R.S. OCA ST. COR. A.C. DELGADO PORT AREA, MANILA 10 03015970 JOSE CUISIA FIL A 187,500 0.0455% 187,500 C/O PHILAMLIFE INSURANCE CO. -

Ccn Tin Importer Im0006021794 430968150000 Daesang Ricor Corporation Im0002959372 003873536000 Westpoint Industrial Sales Co

CCN TIN IMPORTER IM0006021794 430968150000 DAESANG RICOR CORPORATION IM0002959372 003873536000 WESTPOINT INDUSTRIAL SALES CO. INC. IM0002992817 000695510000 ASIAN CARMAKERS CORPORATION IM0002963779 232347770000 STRONG LINK DEVELOPMENT CORPORATION IM0003299511 002624091000 TABAQUERIA DE FILIPINAS INC. IM0003063011 217711150000 ASIAWIDE REFRESHMENTS CORPORATION IM0002963639 001007787000 GX INTERNATIONAL INC. IM0006830714 456650820000 MOBIATRIX INC IM0003014592 002765139000 INNOVISTA TECHNOLOGIES INC. IM0003214699 005393872000 MONTEORO CHEMICAL CORPORATION IM0004340299 000126640000 LINKWORTH INTERNATIONAL INC. IM0006804179 417272052000 EATON INDUSTRIES PHILIPPINES LLC PH IM0002957590 000419293000 ALLEGRO MICROSYSTEMS PHILS. INC. IM0004143132 001030408000 PUENTESPINA ORCHIDS AND TROPICAL IM0003131297 004558769000 ARCHITECKS METAL SYSTEMS INC. IM0003025799 103873913000 MCMASTER INTERNATIONAL SALES IM0002973979 000296020000 CARE PRODUCTS INC IM0003014231 001026198000 INFRATEX PHILIPPINES INC. IM0002962691 000288655000 EURO-MED LABORATORIES PHILS. INC. IM0003031438 006818264000 NORTHFIELDS ENTERPRISES INT'L. INC. IM0003170217 002925850000 KENRICH INT'L . DISTRIBUTOR INC. IM0003259994 000365522000 KAMPILAN MANUFACTURING CORPORATION IM0003132498 103901522000 PEONY MERCHANDISING IM0002959496 204366533000 GLOBEWIDE TRADING IM0002966514 000070213000 NORKIS TRADING CO INC. IM0003232492 000117630000 ENERGIZER PHILIPPINES INC. IM0003131513 000319974000 HI-Q COMMERCIAL.INC IM0003035816 000237662000 PHILIPPINE INTERNATIONAL DEV'T INC. IM0003090795 113041122000