Introduction

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

IBM Software Support

Version 5.0.0 What’s New . Phone Contacts We have eliminated the phone number section from this document and direct you to IBM Planetwide for contact information. I would appreciate your feedback on what you like and what you think should be improved about this document. e-mail me at mcknight@ us.ibm.com Cover design by Rick Nelson, IBM Raleigh 2 June, 2014 Contents What’s New ................................................................................... 2 Overview of IBM Support .............................................................. 4 IBM Commitment......................................................................... 4 Software Support Organization ...................................................... 4 Software Support Portfolio ................................................................. 5 IBM Software Support ...................................................... 5 Support Foundation .......................................................................... 5 Passport Advantage & IBM Software Maintenance ................................ 6 System z (S/390) ......................................................................... 7 Support Line and SoftwareXcel ..................................................... 7 IBM Selected Support Offering ....................................................... 8 Premium Support ............................................................................ 8 Enhanced Technical Support ........................................................ 8 IBM Software Accelerated Value -

Chicago Board Options Exchange Annual Report 2001

01 Chicago Board Options Exchange Annual Report 2001 cv2 CBOE ‘01 01010101010101010 01010101010101010 01010101010101010 01010101010101010 01010101010101010 CBOE is the largest and 01010101010101010most successful options 01010101010101010marketplace in the world. 01010101010101010 01010101010101010 01010101010101010 01010101010101010 01010101010101010 01010101010101010ifc1 CBOE ‘01 ONE HAS OPPORTUNITIES The NUMBER ONE Options Exchange provides customers with a wide selection of products to achieve their unique investment goals. ONE HAS RESPONSIBILITIES The NUMBER ONE Options Exchange is responsible for representing the interests of its members and customers. Whether testifying before Congress, commenting on proposed legislation or working with the Securities and Exchange Commission on finalizing regulations, the CBOE weighs in on behalf of options users everywhere. As an advocate for informed investing, CBOE offers a wide array of educational vehicles, all targeted at educating investors about the use of options as an effective risk management tool. ONE HAS RESOURCES The NUMBER ONE Options Exchange offers a wide variety of resources beginning with a large community of traders who are the most experienced, highly-skilled, well-capitalized liquidity providers in the options arena. In addition, CBOE has a unique, sophisticated hybrid trading floor that facilitates efficient trading. 01 CBOE ‘01 2 CBOE ‘01 “ TO BE THE LEADING MARKETPLACE FOR FINANCIAL DERIVATIVE PRODUCTS, WITH FAIR AND EFFICIENT MARKETS CHARACTERIZED BY DEPTH, LIQUIDITY AND BEST EXECUTION OF PARTICIPANT ORDERS.” CBOE MISSION LETTER FROM THE OFFICE OF THE CHAIRMAN Unprecedented challenges and a need for strategic agility characterized a positive but demanding year in the overall options marketplace. The Chicago Board Options Exchange ® (CBOE®) enjoyed a record-breaking fiscal year, with a 2.2% growth in contracts traded when compared to Fiscal Year 2000, also a record-breaker. -

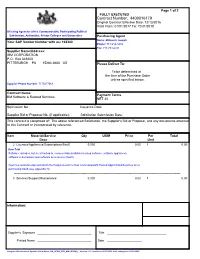

Contract Number: 4400016179

Page 1 of 2 FULLY EXECUTED Contract Number: 4400016179 Original Contract Effective Date: 12/13/2016 Valid From: 01/01/2017 To: 12/31/2018 All using Agencies of the Commonwealth, Participating Political Subdivision, Authorities, Private Colleges and Universities Purchasing Agent Name: Millovich Joseph Your SAP Vendor Number with us: 102380 Phone: 717-214-3434 Fax: 717-783-6241 Supplier Name/Address: IBM CORPORATION P.O. Box 643600 PITTSBURGH PA 15264-3600 US Please Deliver To: To be determined at the time of the Purchase Order unless specified below. Supplier Phone Number: 7175477069 Contract Name: Payment Terms IBM Software & Related Services NET 30 Solicitation No.: Issuance Date: Supplier Bid or Proposal No. (if applicable): Solicitation Submission Date: This contract is comprised of: The above referenced Solicitation, the Supplier's Bid or Proposal, and any documents attached to this Contract or incorporated by reference. Item Material/Service Qty UOM Price Per Total Desc Unit 2 Licenses/Appliances/Subscriptions/SaaS 0.000 0.00 1 0.00 Item Text Software: includes, but is not limited to, commercially available licensed software, software appliances, software subscriptions and software as a service (SaaS). Agencies must develop and attach the Requirements for Non-Commonwealth Hosted Applications/Services when purchasing SaaS (see Appendix H). -------------------------------------------------------------------------------------------------------------------------------------------------------- 3 Services/Support/Maintenance 0.000 0.00 -

Michael Mcgeein, CPA, CA September 2018

IBM Cognos Analytics Data Prep. and Modelling Working with your data Michael McGeein, CPA, CA September 2018 IBM Business Analytics :: IBM Confidential :: © 2016 IBM Corporation Notices and disclaimers Copyright © 2018 by International Business Machines Corporation (IBM). as illustrations of how those customers have used IBM products and No part of this document may be reproduced or transmitted in any form without the results they may have achieved. Actual performance, cost, savings or other written permission from IBM. results in other operating environments may vary. U.S. Government Users Restricted Rights — use, duplication or disclosure References in this document to IBM products, programs, or services does not restricted by GSA ADP Schedule Contract with IBM. imply that IBM intends to make such products, programs or services available in all countries in which IBM operates or does business. Information in these presentations (including information relating to products that have not yet been announced by IBM) has been reviewed for accuracy as Workshops, sessions and associated materials may have been prepared by of the date of initial publication and could include unintentional technical or independent session speakers, and do not necessarily reflect the typographical errors. IBM shall have no responsibility to update this information. views of IBM. All materials and discussions are provided for informational This document is distributed “as is” without any warranty, either express or purposes only, and are neither intended to, nor shall constitute legal or other implied. In no event shall IBM be liable for any damage arising from the use of guidance or advice to any individual participant or their specific situation. -

Java and Z/OS (And Rdz)

® IBM Software Group Java and z/OS (and RDz) Jon Sayles – [email protected] © 2016 IBM Corporation IBM Software Group | Rational software Merrill Class . They’ll have RDz exposure . Terms & Concepts & Vocabulary Remove fear of Java Analogies – Procedural vocabulary 20 – 30 students - mix of young + old (mostly old) dudes . Call COBOL from Java Java doesn’t create an .exe Objects . z/OS Java Standard z/OS environment JCL – pointing to Unix Aware of JVM – can call COBOL http://www.s390java.com/index.htm IBM Software Group | Rational software Trademarks Trademarks The following are trademarks of the International Business Machines Corporation in the United States and/or other countries. For a complete list of IBM Trademarks, see www.ibm.com/legal/copytrade.shtml: AS/400, DBE, e-business logo, ESCO, eServer, FICON, IBM, IBM Logo, iSeries, MVS, OS/390, pSeries, RS/6000, S/30, VM/ESA, VSE/ESA, Websphere, xSeries, z/OS, zSeries, z/VM The following are trademarks or registered trademarks of other companies Lotus, Notes, and Domino are trademarks or registered trademarks of Lotus Development Corporation Java and all Java-related trademarks and logos are trademarks of Sun Microsystems, Inc., in the United States and other countries LINUX is a registered trademark of Linux Torvalds UNIX is a registered trademark of The Open Group in the United States and other countries. Microsoft, Windows and Windows NT are registered trademarks of Microsoft Corporation. SET and Secure Electronic Transaction are trademarks owned by SET Secure Electronic Transaction LLC. Intel is a registered trademark of Intel Corporation * All other products may be trademarks or registered trademarks of their respective companies. -

Annual Report 2011

ANNUAL REPORT 2011 TO OUR STOCKHOLDERS: I am pleased to report that KLA-Tencor performed at record levels on several fronts in fi scal year 2011. We achieved company records in our most critical fi nancial metrics, including revenues, net income, earnings per share and profi t margins, and our year-over-year revenue growth signifi cantly exceeded that of our peer group and our industry. At the same time, we generated record free cash fl ow and continued to deliver meaningful returns to our stockholders in the form of dividends and stock repurchases. This performance was the result of our unwavering focus on develop- ing market-leading technology, addressing our customers’ most critical needs and driving operational effi ciency. Though our industry has seen a recent slowdown in demand, we remain very excited about KLA-Tencor’s prospects for the future. The long-term demand drivers for KLA-Tencor and our industry remain intact, and we are well positioned to grow as demand for semiconductor capital equipment recovers. Our record results in fi scal year 2011 demonstrate that our strategies are working. Looking back over our 35-year history, we have established a pattern of achievement and leadership, which has enabled us to create the strong foundation from which we now look ahead to the future. Our accomplishments during fi scal year 2011 in each of our four strategic objectives (Customer Focus, Growth, Operational Excellence and Talent Development) are highlighted below: CUSTOMER FOCUS: MARKET LEADERSHIP Our customer focus strategic objective is measured in customer satisfaction and market share. We maintained our market leadership positions among our foundry and logic customers in fi scal year 2011 and improved our market position in memory, as evidenced by achieving record new order levels across all our end markets during the year. -

IBM Rational Software IBM Rational Software

® IBM Rational Software Development Conference 2008 SDP30: Jazzing Up IT Best Practices from Internal Deployment of IBM Rational Team Concert Doug Weissman – IT Architect, Rational Software [email protected] Cathy Col – Manager, Rational Engineering Services [email protected] © 2007 IBM Corporation IBM Rational Software Development Conference 2008 Agenda Goal of presentation Why did we centralize deployment of Rational Team Concert? A Simple RTC Configuration Considerations for deploying Rational Team Concert Rational Software’s RTC Deployment Benefits, Best Practices, and Lessons Learned SDP30 – Jazzing Up IT 2 IBM Rational Software Development Conference 2008 Goal of Presentation Help you think about how to deploy Rational Team Concert Give you some suggestions as to possible architectures and configurations Discuss some benefits, best practices, pitfalls, and lessons learned SDP30 – Jazzing Up IT 3 IBM Rational Software Development Conference 2008 Agenda Goal of presentation Why did we centralize deployment of Rational Team Concert? A Simple RTC Configuration Considerations for deploying Rational Team Concert Rational Software’s RTC Deployment Benefits, Best Practices, and Lessons Learned SDP30 – Jazzing Up IT 4 s ent rem qui r re rve l se ima Min IBM Rational Software Development Conference 2008 e Grassroot movement to adopt new technology s u e d bl n si “Jazz” adoptiona was rampant ats Rational! ce d y ac e lo ly s p ee a e fr -b d ad ” o lo ne t n g y ow pa s D rt m a o a E p ch p n dly u w frien e s r o , team -

Getting Started with Rational DOORS Release 9.2 Before Using This Information, Be Sure to Read the General Information Under the "Notices" Chapter on Page 27

IBM Rational DOORS Getting Started with Rational DOORS Release 9.2 Before using this information, be sure to read the general information under the "Notices" chapter on page 27. This edition applies to IBM Rational DOORS, VERSION 9.2, and to all subsequent releases and modifications until otherwise indicated in new editions. © Copyright IBM Corporation 1993, 2010 US Government Users Restricted Rights—Use, duplication or disclosure restricted by GSA ADP Schedule Contract with IBM Corp. Table of contents Chapter 1: About this manual 1 Typographical Conventions. 1 Related Documentation . 1 Chapter 2: Introducing Rational DOORS 3 About Rational DOORS . 3 About requirements . 4 About modules. 4 About objects and attributes . 5 Object Heading and Object Text attributes. 6 About traceability . 6 About views . 7 About folders and projects . 7 About tracking changes . 8 About baselines . 9 About edit modes. 9 About the Change Proposal System . 10 About partitions . 11 About user types . 11 About discussions . 12 Chapter 3: Quick tour 13 About this tour. 13 Getting ready to start the tour. 13 Install and run the Example Database . 13 Editing a module . 15 Changing your view . 17 Making a link . 18 Creating an attribute. 20 Sorting and filtering the data . 21 Getting Started with Rational DOORS iii Table of contents Finishing the tour . 21 Chapter 4: Contacting support 23 Contacting IBM Rational Software Support . 23 Prerequisites . 23 Submitting problems. 24 Other information. 26 Chapter 5: Notices 27 Trademarks . 29 Index 31 iv Getting Started with Rational DOORS 1 About this manual Welcome to IBM® Rational® DOORS® 9.2, the world’s leading requirements management application. -

IBM Services ISMS / PIMS Products / Pids in Scope

1H 2021 Certified Product List IBM services ISMS/PIMS Product/Service Offerings/PIDs in scope The following is a list of products associated with the offering bundles in scope of the IBM services information security management system (ISMS). The Cloud services ISMS has been certified on: ISO/IEC 27001:2013 ISO/IEC 27017:2015 ISO/IEC 27018:2019 ISO/IEC 27701:2019 As well as the IBM Cloud Services STAR Self-Assessment found here: This listing is current as of 07/20/2021 IBM Cloud Services STAR Self-Assessment Cloud Controls Matrix v3.0.1 https://cloudsecurityalliance.org/registry/ibm-cloud/ To find out more about IBM Cloud compliance go to: https://www.ibm.com/cloud/compliance/global type groupNameproductName pids ISO Group AccessHub-at-IBM Offering AccessHub-at-IBM N/A ISO Group AI Applications - Maximo and TRIRIGA Offering IBM Enterprise Asset Management Anywhere on Cloud (Maximo) 5725-Z55 Offering IBM Enterprise Asset Management Anywhere on Cloud (Maximo) Add-On 5725-Z55 Offering IBM Enterprise Asset Management on Cloud (Maximo) Asset Configuration Manager Add-On 5725-P73 Offering IBM Enterprise Asset Management on Cloud (Maximo) Aviation Add-On 5725-P73 Offering IBM Enterprise Asset Management on Cloud (Maximo) Calibration Add-On 5725-P73 Offering IBM Enterprise Asset Management on Cloud (Maximo) for Managed Service Provider Add-On 5725-P73 Offering IBM Enterprise Asset Management on Cloud (Maximo) Health, Safety and Environment Manager Add-On 5725-P73 Offering IBM Enterprise Asset Management on Cloud (Maximo) Life Sciences Add-On -

A Model Driven Approach for Service Based System Design Using Interaction Templates

Toni Reichelt A Model Driven Approach for Service Based System Design Using Interaction Templates Wissenschaftliche Schriftenreihe EINGEBETTETE, SELBSTORGANISIERENDE SYSTEME Band 10 Prof. Dr. Wolfram Hardt (Hrsg.) Toni Reichelt A Model Driven Approach for Service Based System Design Using Interaction Templates Chemnitz University Press 2012 Impressum Bibliografische Information der Deutschen Nationalbibliothek Die Deutsche Nationalbibliothek verzeichnet diese Publikation in der Deutschen Nationalbibliografie; detaillierte bibliografische Angaben sind im Internet über http://dnb.d-nb.de abrufbar. Zugl.: Chemnitz, Techn. Univ., Diss., 2012 Technische Universität Chemnitz/Universitätsbibliothek Universitätsverlag Chemnitz 09107 Chemnitz http://www.bibliothek.tu-chemnitz.de/UniVerlag/ Herstellung und Auslieferung Verlagshaus Monsenstein und Vannerdat OHG Am Hawerkamp 31 48155 Münster http://www.mv-verlag.de ISBN 978-3-941003-60-6 URL: http://nbn-resolving.de/urn:nbn:de:bsz:ch1-qucosa-85986 Preface to the scientific series “Eingebettete, selbstorganisierende Systeme” The tenth volume of the scientific series Eingebettete, selbstorganisierende Systeme (Em- bedded, self-organised systems) devotes itself to the model driven design of service-oriented systems. Fields of application for such systems, amongst others, range from large scale, distributed enterprise solutions down to modularised embedded systems. The presented work was moti- vated by the complex design process of avionics for unmanned systems, where the increased demand for enhanced system autonomy implies high levels of system collaboration and infor- mation exchange. For such system designs a clear separation between the application logic implemented by system components, the means of interaction between them and finally the realisation of such communication on target platforms is essential. In particular, this sep- aration leads to simplification of the complex design processes and increases the individual components’ re-use potential. -

IBM Cloud Nurture Milestones

The Rise of the Built-For- Purpose Marketing Stack Magith Noohukhan Customer Engagement Evangelist Braze Introductions Magith Noohukhan Neetika Bhargava Customer Engagement Evangelist Consumer Marketing Manager Braze IBM I I Your Brand iI Your Brand iI Forge human connections between consumers and the brands they love through relevant and memorable experiences. The bar is getting higher. Today’s consumer expects relevant experiences from the brands they engage with. Headspace Uses Beautiful, Branded Emails to Guide Customers Through Key Milestones Acquire Engage Convert Retain Welcome Email First-Session Prompt Subscription Confirmation Personalized Newsletter Burger King Promotes Their BK Cafe Subscription by Sending a Weather-Based Push Notification Content: Nurture Streams Looks like you just upgraded your IBM Cloud account, [First Name]. Nice. Aspera First things first, take a few minutes to get familiar IBM Cloud Nurture with your account: Getting started with Aspera is ALMOST as fast Step 1: Log in as our file transfers. Step 2: Take a spin through the documention Onboarding Step 3: Check out the IBM service catalog Step 4: Pat yourself on the back The onboarding lifecycle is a series of welcome emails (this step is strongly suggested. sent to new users regardless of their current engagement, Finally, just in case you need a hand, have a question, or just want Hello there, [First Name]! in an effort to set them with the resources for success. to say hi, talk to us! Visit our Support page to chat with a team member anytime. It’s been a few days since you became an Aspera on Cloud admin. -

27Th Large Installation System Administration Conference (LISA '13)

conference proceedings Proceedings of the 27th Large Installation System Administration Conference 27th Large Installation System Administration Conference (LISA ’13) Washington, D.C., USA November 3–8, 2013 Washington, D.C., USA November 3–8, 2013 Sponsored by In cooperation with LOPSA Thanks to Our LISA ’13 Sponsors Thanks to Our USENIX and LISA SIG Supporters Gold Sponsors USENIX Patrons Google InfoSys Microsoft Research NetApp VMware USENIX Benefactors Akamai EMC Hewlett-Packard Linux Journal Linux Pro Magazine Puppet Labs Silver Sponsors USENIX and LISA SIG Partners Cambridge Computer Google USENIX Partners Bronze Sponsors Meraki Nutanix Media Sponsors and Industry Partners ACM Queue IEEE Security & Privacy LXer ADMIN IEEE Software No Starch Press CiSE InfoSec News O’Reilly Media Computer IT/Dev Connections Open Source Data Center Conference Distributed Management Task Force IT Professional (OSDC) (DMTF) Linux Foundation Server Fault Free Software Magazine Linux Journal The Data Center Journal HPCwire Linux Pro Magazine Userfriendly.org IEEE Pervasive © 2013 by The USENIX Association All Rights Reserved This volume is published as a collective work. Rights to individual papers remain with the author or the author’s employer. Permission is granted for the noncommercial reproduction of the complete work for educational or research purposes. Permission is granted to print, primarily for one person’s exclusive use, a single copy of these Proceedings. USENIX acknowledges all trademarks herein. ISBN 978-1-931971-05-8 USENIX Association Proceedings of the 27th Large Installation System Administration Conference November 3–8, 2013 Washington, D.C. Conference Organizers Program Co-Chairs David Nalley, Apache Cloudstack Narayan Desai, Argonne National Laboratory Adele Shakal, Metacloud, Inc.