Devaluation in Kazakhstan: History, Causes, Consequences

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Devaluation, Wealth Effects, and Relative Prices Harvey Lapan Iowa State University, [email protected]

Economics Publications Economics 9-1978 Devaluation, Wealth Effects, and Relative Prices Harvey Lapan Iowa State University, [email protected] Walter Enders Iowa State University Follow this and additional works at: http://lib.dr.iastate.edu/econ_las_pubs Part of the Economic Theory Commons, International Economics Commons, and the Other Economics Commons The ompc lete bibliographic information for this item can be found at http://lib.dr.iastate.edu/ econ_las_pubs/152. For information on how to cite this item, please visit http://lib.dr.iastate.edu/ howtocite.html. This Article is brought to you for free and open access by the Economics at Iowa State University Digital Repository. It has been accepted for inclusion in Economics Publications by an authorized administrator of Iowa State University Digital Repository. For more information, please contact [email protected]. Devaluation, Wealth Effects, and Relative Prices Abstract The mee rgence of the portfolio balance approach 1 has led to a reformulation of the causes of balance-of-trade and payments disequilibria. According to this approach, balance-of-trade deficits and surpluses reflect discrepancies between desired and actual wealth holdings; while balance-of payments deficits and surpluses reflect discrepancies between desired and actual money holdings. Thus, balance-of-trade and payments disequilibria are viewed as representing disequilibria within the asset markets. Using this framework several authors2 have examined the self-correcting nature of disequilibria within the balance of-payments accounts and the ability of a devaluation to reduce the magnitude of a disequilibrium. Disciplines Economic Theory | International Economics | Other Economics Comments This is an article from The American Economic Review 68 (1978): 601. -

The Decline of Neoliberalism: a Play in Three Acts* O Declínio Do Neoliberalismo: Uma Peça Em Três Atos

Brazilian Journal of Political Economy, vol. 40, nº 4, pp. 587-603, October-December/2020 The decline of neoliberalism: a play in three acts* O declínio do neoliberalismo: uma peça em três atos FERNANDO RUGITSKY**,*** RESUMO: O objetivo deste artigo é examinar as consequências políticas e econômicas da pandemia causada pelo novo coronavírus, colocando-a no contexto de um interregno gram sciano. Primeiro, o desmonte da articulação triangular do mercado mundial que ca- racterizou a década anterior a 2008 é examinado. Segundo, a onda global de protestos e os deslocamentos eleitorais observados desde 2010 são interpretados como evidências de uma crise da hegemonia neoliberal. Juntas, as crises econômica e hegemônica representam o interregno. Por fim, argumenta-se que o combate à pandemia pode levar à superação do neoliberalismo. PALAVRAS-CHAVE: Crise econômica; hegemonia neoliberal; interregno; pandemia. ABSTRACT: This paper aims to examine the political and economic consequences of the pandemic caused by the new coronavirus, setting it in the context of a Gramscian interregnum. First, the dismantling of the triangular articulation of the world market that characterized the decade before 2008 is examined. Second, the global protest wave and the electoral shifts observed since 2010 are interpreted as evidence of a crisis of neoliberal hegemony. Together, the economic and hegemonic crises represent the interregnum. Last, it is argued that the fight against the pandemic may lead to the overcoming of neoliberalism. KEYWORDS: Economic crisis; neoliberal hegemony; interregnum; pandemic. JEL Classification: B51; E02; O57. * A previous version of this paper was published, in Portuguese, in the 1st edition (2nd series) of Revista Rosa. -

On the Effectiveness of Exchange Rate Interventions in Emerging Markets

On the effectiveness of exchange rate interventions in emerging markets Christian Daude, Eduardo Levy Yeyati and Arne Nagengast CID Working Paper No. 288 September 2014 Copyright 2014 Daude, Christian; Levy Yeyati, Eduardo; Nagengast, Arne; and the President and Fellows of Harvard College Working Papers Center for International Development at Harvard University On the effectiveness of exchange rate interventions in emerging markets Christian Daude Organisation for Economic Co-operation and Development Eduardo Levy Yeyati Universidad Torcuato Di Tella Arne Nagengast Deutsche Bundesbank Abstract We analyze the effectiveness of exchange rate interventions for a panel of 18 emerging market economies during the period 2003-2011. Using an error-correction model approach we find that on average intervention is effective in moving the real exchange rate in the desired direction, controlling for deviations from the equilibrium and short-term changes in fundamentals and global financial variables. Our results are robust to different samples and estimation methods. We find little evidence of asymmetries in the effect of sales and purchases, but some evidence of more effective interventions for large deviations from the equilibrium. We also explore differences across countries according to the possible transmission channels and nature of some global shocks. JEL-classification: F31, F37 Keywords: exchange rate; FX intervention; equilibrium exchange rate 1 1. INTRODUCTION Few macroeconomic policy topics have been as hotly debated as the exchange rate -

Revaluation of Financial Statement Due To

Academy of Accounting and Financial Studies Journal Volume 25, Special Issue 2, 2021 REVALUATION OF FINANCIAL STATEMENT DUE TO DEVALUATION OF CURRENCY– DOES FINANCIAL STATEMENT SHOW ACCURATE VALUE OF YOUR ORGANIZATION? Muhammad Nabeel Mustafa*, SZABIST University Haroon ur Rashid Khan, SZABIST University Salman Ahmed Shaikh, SZABIST University ABSTRACT Purpose: Debtors are current asset has a time of 120 days at max. During this time, the value of debtors gets changed. This study explores the effect of this time value of money. The objective of this research is to sight see the effect of the time value of money, normal inflation, and purchasing power on the comprehensive debtors/receivable side of the balance sheet, which can be devalued if key macroeconomic factors determine the devaluation percentage of a single currency. Methodology: Concerning these significant questions of the research, we grasped a pragmatic philosophy with an inductive approach. A mono-method of qualitative based on grounded theory was endorsed, which helped to unfold a new model through qualitative data analysis. Results: A new strategy is developed, which utters three components; normal inflation, time value of money, and purchasing power revealing significant contribution in literature. The effect of these constructs was not incorporated in the financial statement, showing vague financial valuation. These constructs have a significant impact on the financial statement of any organization especially with items having time components in the balance sheet, such as receivables and payables. Research Limitations: This research is limited to only one currency i.e., Pakistani Rupee but can be implemented on any currency. Practical Implication: The strategy will help auditors to pass the adjustment entry in the balance sheet to adjust the value of the currency at the year-end. -

Inflation, Interest Rates, and Hyperinflation

INFLATION, INTEREST RATES, AND HYPERINFLATION Demand for goods depends on the real interest rate: Y = A(Y, i-B) Demand for money on the nominal interest rate: M/P = L(Y, i) In the long run, economy tends to natural rate of output Yn. This means that it tends to “natural” real interest rate i-B = rn Recipe for steady inflation: let M grow at a steady rate )M/M = gM Then guess that price level also grows at a steady rate B = gM, and that real interest rate remains at rn. Then )(M/P)/(M/P) = )M/M - )P/P = 0 So M/P constant; Y constant at Yn, i constant at rn + gM End of story But notice that higher B => higher i => lower M/P SEIGNORAGE: THE REVENUE FROM MONEY PRINTING Government gets “revenue” by printing additional money; the real revenue is S = )M/P (change in money supply divided by price level) or rewrite it S = ()M/M)(M/P) = gM(M/P) In steady inflation, however, i = rn+gM - and M/P is a decreasing fn. of i So seignorage does not necessarily increase with rate of money growth; typical shape is “inverted U”: But what if the government “needs” seignorage greater than maximum? Turn the equation around: )M ' S M M/P As people start to expect inflation, M/P falls; this means )M/M rises; means further fall in M/P, etc. Result: Hyperinflation!! FIXED EXCHANGE RATES AND DEVALUATION Aggregate demand in an open economy with a fixed exchange rate: No monetary policy! i = i* So Y = A(Y, i*) + NX(Y, Y*, EP*/P) Higher P means lower output because it makes our goods less competitive on world market Meanwhile, AS curve: P = P-1G(Y, z) Suppose we increase E (a devaluation): A devaluation can produce only a temporary expansion in output. -

Floating Exchange Rates and Their Problems for the Developing Countries

A Service of Leibniz-Informationszentrum econstor Wirtschaft Leibniz Information Centre Make Your Publications Visible. zbw for Economics Erhardt, Barbara Article — Digitized Version Floating exchange rates and their problems for the developing countries Intereconomics Suggested Citation: Erhardt, Barbara (1977) : Floating exchange rates and their problems for the developing countries, Intereconomics, ISSN 0020-5346, Verlag Weltarchiv, Hamburg, Vol. 12, Iss. 1/2, pp. 29-34, http://dx.doi.org/10.1007/BF02929168 This Version is available at: http://hdl.handle.net/10419/139444 Standard-Nutzungsbedingungen: Terms of use: Die Dokumente auf EconStor dürfen zu eigenen wissenschaftlichen Documents in EconStor may be saved and copied for your Zwecken und zum Privatgebrauch gespeichert und kopiert werden. personal and scholarly purposes. Sie dürfen die Dokumente nicht für öffentliche oder kommerzielle You are not to copy documents for public or commercial Zwecke vervielfältigen, öffentlich ausstellen, öffentlich zugänglich purposes, to exhibit the documents publicly, to make them machen, vertreiben oder anderweitig nutzen. publicly available on the internet, or to distribute or otherwise use the documents in public. Sofern die Verfasser die Dokumente unter Open-Content-Lizenzen (insbesondere CC-Lizenzen) zur Verfügung gestellt haben sollten, If the documents have been made available under an Open gelten abweichend von diesen Nutzungsbedingungen die in der dort Content Licence (especially Creative Commons Licences), you genannten Lizenz gewährten -

Currency Devaluation in Developing Countries: a Cross- Sectional Assessment

Yale University EliScholar – A Digital Platform for Scholarly Publishing at Yale Discussion Papers Economic Growth Center 7-1-1969 Currency Devaluation in Developing Countries: A Cross- Sectional Assessment Richard N. Cooper Follow this and additional works at: https://elischolar.library.yale.edu/egcenter-discussion-paper-series Recommended Citation Cooper, Richard N., "Currency Devaluation in Developing Countries: A Cross- Sectional Assessment" (1969). Discussion Papers. 80. https://elischolar.library.yale.edu/egcenter-discussion-paper-series/80 This Discussion Paper is brought to you for free and open access by the Economic Growth Center at EliScholar – A Digital Platform for Scholarly Publishing at Yale. It has been accepted for inclusion in Discussion Papers by an authorized administrator of EliScholar – A Digital Platform for Scholarly Publishing at Yale. For more information, please contact [email protected]. ~ ,J<_ '\ \ ,• ,.,,) r. iJ .I ECONOMIC GROWTH CEUTER YALE rnnVERSITY '\ r. Box 1987, Yale Station ;\,,,') New Haven, Connecticut Cfa'lTER DISCUSSI011 PAPER NO. 72 CURRENCY DEVALUATION Id DEVELOPIHG COUNTRIES: A CROSS-SECTIONAL ASSESSUEaT~: Richard 1~. Cooper July, 1969 ilote: Center Discussion Papers are preliminary materials circulated to stimulate discu~sion and critical comment. References in publi~ations to Discussion Papers should be cleared with the author to protect the tentative character of these papers. Table of Contents Page I. Nominal vs. Effective Devaluation 3 II. Devaluation and the Balance of Payments 8 III. Devaluation and the Terms of Trade 16 IV. Devaluation and Aggregate Demand 19 v. Devaluation and the Wage-Price Spiral 26 VI. Political Effects of Devaluation 36 VII. Conclusions and Recommendat·ions 40 Appendices A. -

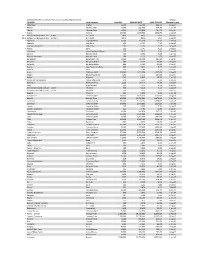

Maximum Monthly Stipend Rates For

MAXIMUM MONTHLY STIPEND RATES FOR FELLOWS AND SCHOLARS Jul 2020 COUNTRY Local Currency Local DSA MAX RES RATE MAX TRV RATE Effective % date * Afghanistan Afghani 12,600 132,300 198,450 1-Aug-07 * Albania Albania Lek(e) 14,000 220,500 330,750 1-Jan-05 Algeria Algerian Dinar 31,600 331,800 497,700 1-Aug-07 * Angola Kwanza 133,000 1,396,500 2,094,750 1-Aug-07 #N/A Antigua and Barbuda (1 Apr. - 30 Nov.) E.C. Dollar #N/A #N/A #N/A 1-Aug-07 #N/A Antigua and Barbuda (1 Dec. - 31 Mar.) E.C. Dollar #N/A #N/A #N/A 1-Aug-07 * Argentina Argentine Peso 18,600 153,450 230,175 1-Jan-05 Australia AUL Dollar 453 4,757 7,135 1-Aug-07 Australia - Academic AUL Dollar 453 1,200 7,135 1-Aug-07 * Austria Euro 261 2,741 4,111 1-Aug-07 * Azerbaijan (new)Azerbaijan Manat 239 1,613 2,420 1-Jan-05 Bahrain Bahraini Dinar 106 2,226 3,180 1-Jan-05 Bahrain - Academic Bahraini Dinar 106 1,113 1,670 1-Aug-07 Bangladesh Bangladesh Taka 12,400 130,200 195,300 1-Aug-07 Barbados Barbados Dollar 880 9,240 13,860 1-Aug-07 Barbados Barbados Dollar 880 9,240 13,860 1-Aug-07 * Belarus New Belarusian Ruble 600 5,850 8,775 1-Jan-06 Belgium Euro 338 3,549 5,324 1-Aug-07 Benin CFA Franc(XOF) 123,000 1,291,500 1,937,250 1-Aug-07 Bhutan Bhutan Ngultrum 7,290 76,545 114,818 1-Aug-07 * Bolivia Boliviano 1,200 10,800 16,200 1-Jan-07 * Bosnia and Herzegovina Convertible Mark 279 3,557 5,336 1-Jan-05 Botswana Botswana Pula 2,220 23,310 34,965 1-Aug-07 Brazil Brazilian Real 530 4,373 6,559 1-Jan-05 British Virgin Islands (16 Apr. -

The Monetary Legacy of the Soviet Union / Patrick Conway

ESSAYS IN INTERNATIONAL FINANCE ESSAYS IN INTERNATIONAL FINANCE are published by the International Finance Section of the Department of Economics of Princeton University. The Section sponsors this series of publications, but the opinions expressed are those of the authors. The Section welcomes the submission of manuscripts for publication in this and its other series. Please see the Notice to Contributors at the back of this Essay. The author of this Essay, Patrick Conway, is Professor of Economics at the University of North Carolina at Chapel Hill. He has written extensively on the subject of structural adjustment in developing and transitional economies, beginning with Economic Shocks and Structural Adjustment: Turkey after 1973 (1987) and continuing, most recently, with “An Atheoretic Evaluation of Success in Structural Adjustment” (1994a). Professor Conway has considerable experience with the economies of the former Soviet Union and has made research visits to each of the republics discussed in this Essay. PETER B. KENEN, Director International Finance Section INTERNATIONAL FINANCE SECTION EDITORIAL STAFF Peter B. Kenen, Director Margaret B. Riccardi, Editor Lillian Spais, Editorial Aide Lalitha H. Chandra, Subscriptions and Orders Library of Congress Cataloging-in-Publication Data Conway, Patrick J. Currency proliferation: the monetary legacy of the Soviet Union / Patrick Conway. p. cm. — (Essays in international finance, ISSN 0071-142X ; no. 197) Includes bibliographical references. ISBN 0-88165-104-4 (pbk.) : $8.00 1. Currency question—Former Soviet republics. 2. Monetary policy—Former Soviet republics. 3. Finance—Former Soviet republics. I. Title. II. Series. HG136.P7 no. 197 [HG1075] 332′.042 s—dc20 [332.4′947] 95-18713 CIP Copyright © 1995 by International Finance Section, Department of Economics, Princeton University. -

Countries Codes and Currencies 2020.Xlsx

World Bank Country Code Country Name WHO Region Currency Name Currency Code Income Group (2018) AFG Afghanistan EMR Low Afghanistan Afghani AFN ALB Albania EUR Upper‐middle Albanian Lek ALL DZA Algeria AFR Upper‐middle Algerian Dinar DZD AND Andorra EUR High Euro EUR AGO Angola AFR Lower‐middle Angolan Kwanza AON ATG Antigua and Barbuda AMR High Eastern Caribbean Dollar XCD ARG Argentina AMR Upper‐middle Argentine Peso ARS ARM Armenia EUR Upper‐middle Dram AMD AUS Australia WPR High Australian Dollar AUD AUT Austria EUR High Euro EUR AZE Azerbaijan EUR Upper‐middle Manat AZN BHS Bahamas AMR High Bahamian Dollar BSD BHR Bahrain EMR High Baharaini Dinar BHD BGD Bangladesh SEAR Lower‐middle Taka BDT BRB Barbados AMR High Barbados Dollar BBD BLR Belarus EUR Upper‐middle Belarusian Ruble BYN BEL Belgium EUR High Euro EUR BLZ Belize AMR Upper‐middle Belize Dollar BZD BEN Benin AFR Low CFA Franc XOF BTN Bhutan SEAR Lower‐middle Ngultrum BTN BOL Bolivia Plurinational States of AMR Lower‐middle Boliviano BOB BIH Bosnia and Herzegovina EUR Upper‐middle Convertible Mark BAM BWA Botswana AFR Upper‐middle Botswana Pula BWP BRA Brazil AMR Upper‐middle Brazilian Real BRL BRN Brunei Darussalam WPR High Brunei Dollar BND BGR Bulgaria EUR Upper‐middle Bulgarian Lev BGL BFA Burkina Faso AFR Low CFA Franc XOF BDI Burundi AFR Low Burundi Franc BIF CPV Cabo Verde Republic of AFR Lower‐middle Cape Verde Escudo CVE KHM Cambodia WPR Lower‐middle Riel KHR CMR Cameroon AFR Lower‐middle CFA Franc XAF CAN Canada AMR High Canadian Dollar CAD CAF Central African Republic -

Maximum Monthly Stipend Rates for Fellows And

MAXIMUM MONTHLY STIPEND RATES FOR FELLOWS AND SCHOLARS Sep 2020 COUNTRY Local Currency Local DSA MAX RES RATE MAX TRV RATE Effective % date Afghanistan Afghani 12,500 131,250 196,875 1-Aug-07 * Albania Albania Lek(e) 13,100 206,325 309,488 1-Jan-05 Algeria Algerian Dinar 31,600 331,800 497,700 1-Aug-07 * Angola Kwanza 134,000 1,407,000 2,110,500 1-Aug-07 #N/A Antigua and Barbuda (1 Apr. - 30 Nov.) E.C. Dollar #N/A #N/A #N/A 1-Aug-07 #N/A Antigua and Barbuda (1 Dec. - 31 Mar.) E.C. Dollar #N/A #N/A #N/A 1-Aug-07 * Argentina Argentine Peso 19,700 162,525 243,788 1-Jan-05 Australia AUL Dollar 453 4,757 7,135 1-Aug-07 Australia - Academic AUL Dollar 453 1,200 7,135 1-Aug-07 Austria Euro 261 2,741 4,111 1-Aug-07 Azerbaijan (new)Azerbaijan Manat 239 1,613 2,420 1-Jan-05 Bahrain Bahraini Dinar 106 2,226 3,180 1-Jan-05 Bahrain - Academic Bahraini Dinar 106 1,113 1,670 1-Aug-07 Bangladesh Bangladesh Taka 12,400 130,200 195,300 1-Aug-07 Barbados Barbados Dollar 880 9,240 13,860 1-Aug-07 Barbados Barbados Dollar 880 9,240 13,860 1-Aug-07 * Belarus New Belarusian Ruble 680 6,630 9,945 1-Jan-06 Belgium Euro 338 3,549 5,324 1-Aug-07 Benin CFA Franc(XOF) 123,000 1,291,500 1,937,250 1-Aug-07 Bhutan Bhutan Ngultrum 7,290 76,545 114,818 1-Aug-07 Bolivia Boliviano 1,180 10,620 15,930 1-Jan-07 * Bosnia and Herzegovina Convertible Mark 264 3,366 5,049 1-Jan-05 Botswana Botswana Pula 2,220 23,310 34,965 1-Aug-07 Brazil Brazilian Real 530 4,373 6,559 1-Jan-05 British Virgin Islands (16 Apr. -

Banking Sector and Economy of CEE Countries: Development Features and Correlation

Centre for Research on Settlements and Urbanism Journal of Settlements and Spatial Planning J o u r n a l h o m e p a g e: http://jssp.reviste.ubbcluj.ro Banking Sector and Economy of CEE Countries: Development Features and Correlation Iurii UMANTSIV 1, Olena ISHCHENKO 1 1 Kyiv National University of Trade and Economics, Faculty of Economics, Management and Psychology, Department of Economic Theory and Competition Policy, Kyiv, UKRAINE E-mail: [email protected], [email protected] DOI: 10.24193/JSSP.2017.1.05 https://doi.org/10.24193/JSSP.2017.1.05 K e y w o r d s: economy of CEE country, banking system, financial sector, role of banks, correlation between GDP and bank investments, EU operational programs, CEE countries, banking sector development A B S T R A C T This research focuses on the analysis of current trends in the banking sector of Central and Eastern Europe (CEE), and on its role in the development of the economy. This region is represented by countries situated at different levels of development and types of economic system. The following countries are analyzed: Bulgaria, Poland, Romania, the Republic of Belarus and Ukraine. The article starts with a general description of the economy of each of the five countries listed above, followed by a discussion of main trends of their development and a comparison of these states based on the status of their socioeconomic development. The study will also examine the banking systems of each of these countries looking at the types of banks that are present on the market, capital ownership, and market share, as well as the main indicators of soundness of the banking system.