A Healthy Future for Foodservice?

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Differences in Energy and Nutritional Content of Menu Items Served By

RESEARCH ARTICLE Differences in energy and nutritional content of menu items served by popular UK chain restaurants with versus without voluntary menu labelling: A cross-sectional study ☯ ☯ Dolly R. Z. TheisID *, Jean AdamsID Centre for Diet and Activity Research, MRC Epidemiology Unit, University of Cambridge, Cambridge, United a1111111111 Kingdom a1111111111 ☯ These authors contributed equally to this work. a1111111111 * [email protected] a1111111111 a1111111111 Abstract Background OPEN ACCESS Poor diet is a leading driver of obesity and morbidity. One possible contributor is increased Citation: Theis DRZ, Adams J (2019) Differences consumption of foods from out of home establishments, which tend to be high in energy den- in energy and nutritional content of menu items sity and portion size. A number of out of home establishments voluntarily provide consumers served by popular UK chain restaurants with with nutritional information through menu labelling. The aim of this study was to determine versus without voluntary menu labelling: A cross- whether there are differences in the energy and nutritional content of menu items served by sectional study. PLoS ONE 14(10): e0222773. https://doi.org/10.1371/journal.pone.0222773 popular UK restaurants with versus without voluntary menu labelling. Editor: Zhifeng Gao, University of Florida, UNITED STATES Methods and findings Received: February 8, 2019 We identified the 100 most popular UK restaurant chains by sales and searched their web- sites for energy and nutritional information on items served in March-April 2018. We estab- Accepted: September 6, 2019 lished whether or not restaurants provided voluntary menu labelling by telephoning head Published: October 16, 2019 offices, visiting outlets and sourcing up-to-date copies of menus. -

Venue Id Venue Name Address 1 City Postcode Venue Type

Venue_id Venue_name Address_1 City Postcode Venue_type 2012292 Plough 1 Lewis Street Aberaman CF44 6PY Retail - Pub 2011877 Conway Inn 52 Cardiff Street Aberdare CF44 7DG Retail - Pub 2006783 McDonald's - 902 Aberdare Gadlys Link Road ABERDARE CF44 7NT Retail - Fast Food 2009437 Rhoswenallt Inn Werfa Aberdare CF44 0YP Retail - Pub 2011896 Wetherspoons 6 High Street Aberdare CF44 7AA Retail - Pub 2009691 Archibald Simpson 5 Castle Street Aberdeen AB11 5BQ Retail - Pub 2003453 BAA - Aberdeen Aberdeen Airport Aberdeen AB21 7DU Transport - Small Airport 2009128 Britannia Hotel Malcolm Road Aberdeen AB21 9LN Retail - Pub 2014519 First Scot Rail - Aberdeen Guild St Aberdeen AB11 6LX Transport - Local rail station 2009345 Grays Inn Greenfern Road Aberdeen AB16 5PY Retail - Pub 2011456 Liquid Bridge Place Aberdeen AB11 6HZ Retail - Pub 2012139 Lloyds No.1 (Justice Mill) Justice Mill Aberdeen AB11 6DA Retail - Pub 2007205 McDonald's - 1341 Asda Aberdeen Garthdee Road Aberdeen AB10 7BA Retail - Fast Food 2006333 McDonald's - 398 Aberdeen 1 117 Union Street ABERDEEN AB11 6BH Retail - Fast Food 2006524 McDonald's - 618 Bucksburn Inverurie Road ABERDEEN AB21 9LZ Retail - Fast Food 2006561 McDonald's - 663 Bridge Of Don Broadfold Road ABERDEEN AB23 8EE Retail - Fast Food 2010111 Menzies Farburn Terrace Aberdeen AB21 7DW Retail - Pub 2007684 Triplekirks Schoolhill Aberdeen AB12 4RR Retail - Pub 2002538 Swallow Thainstone House Hotel Inverurie Aberdeenshire AB51 5NT Hotels - 4/5 Star Hotel with full coverage 2002546 Swallow Waterside Hotel Fraserburgh -

Air Quality and Risk Assessment Report

4103 Palladium Way D-6 Compatibility – Air Quality and Risk Assessment Client: Better Life Development Project Name: D-6 Compatibility – Air Quality Assessment – 4103 Palladium Way, Burlington, ON Attention: Sam Badawi 30 Harding Blvd. West, Unit 210 Richmond Hill, ON L4C 9M3 Type of Document: Final Project Number: BRM-00801656-C0 EXP 1595 Clark Boulevard Brampton, ON, L6T 4V1 t: +1.905.793.9800 f: +1.905.793.0641 Date: October 11, 2019 1595 Clark Boulevard | Brampton, ON L6T 4V1 | Canada t: +1.905.793.9800 | f: +1.905.793.0641 | exp.com EXP Services Inc. i D-6 Compatibility – Air Quality Assessment – 4103 Palladium Way, Burlington, ON Project Number: BRM-00801656-C0 October 11, 2019 Version Control Rev. Date Description Submitted by Reviewed by 1.0 June 17, 2019 Initial Draft Scott Grant-Hose Ron Taylor 1.1 October 5, 2019 Draft updated site plan Scott Grant-Hose Ron Taylor 1.2 October 10, 2019 Draft updated site plan Scott Grant-Hose Ron Taylor 1.3 October 11,2019 Draft client comment update Scott Grant-Hose Ron Taylor 1.4 October 11,2019 Final Scott Grant-Hose Ron Taylor EXP Services Inc. ii D-6 Compatibility – Air Quality Assessment – 4103 Palladium Way, Burlington, ON Project Number: BRM-00801656-C0 October 11, 2019 Legal Notification This report was prepared by EXP Services Inc. for the account of Better Life Development Any use which a third party makes of this report, or any reliance on or decisions to be made based on it, are the responsibility of such third parties. EXP Services Inc. -

NEWCASTLE Cushman & Wakefield Global Cities Retail Guide

NEWCASTLE Cushman & Wakefield Global Cities Retail Guide 0 A city once at the heart of the Industrial Revolution, Newcastle has now repositioned itself as a thriving and vibrant capital of the North East. The city offers a blend of culture and heritage, superb shopping, sporting activity and nightlife with the countryside and the coastline at its doorstep. The city is located on the north bank of the River Tyne with an impressive seven bridges along the riverscape. The Gateshead Millennium Bridge is the newest bridge to the city, completed in 2001 - the world’s first and only titling bridge. Newcastle benefits from excellent fast rail links to London with journey times in under three hours. Newcastle Airport is a top ten UK airport and the fastest growing regional airport in the UK, with over 5 million passengers travelling through the airport annually. This is expected to reach 8.5 million by 2030. NEWCASTLE OVERVIEW 1 Cushman & Wakefield | Newcastle | 2019 NEWCASTLE KEY RETAIL STREETS & AREAS NORTHUMBERLAND ST GRAINGER ST & CENTRAL EXCHANGE Newcastle’s traditional prime retail street. Running Grainger Street is located between Newcastle Station and between Haymarket Metro Station to the north and Newcastle’s main retail core. It not only plays host to the Blackett St to the south. It is fully pedestrianised and a key historic Central Exchange Building and Central Arcade footfall route. Home to big brands including H&M, Primark, within, but also Newcastle’s famous Grainger Market. Marks & Spencer, Fenwick among other national multiple Grainger Street is one of Newcastle’s most picturesque retail brands. -

Informed Decisions? Availability of Nutritional Information for a Sample of Out-Of-Home Food Outlets in Scotland

Sept 2017 Informed decisions? Availability of nutritional information for a sample of out-of-home food outlets in Scotland Rachel Ormston, Gareth McAteer and Steven Hope Ipsos MORI Scotland for Food Standards Scotland 16-084454-01 FSS portion sizes | Version 4 | Public | Internal and Client Use Only | This work was carried out in accordance with the requirements of the international quality standard for Market Research, ISO 20252:2012, and with the Ipsos MORI Terms and Conditions which can be found at http://www.ipsos-mori.com/terms. © Ipsos MORI 2016. Ipsos MORI | June 2017 | 16-084454-01 FSS portion sizes report Version 6 | Internal and Client Use Only | © 2017 Ipsos MORI – all rights reserved. 16-084454-01 FSS – portion sizes report | Version 5 | Internal and client Use Only | This work was carried out in accordance with the requirements of the international quality standard for Market Research, ISO 20252:2012, and with the Ipsos MORI Terms and Conditions which can be found at http://www.ipsos-mori.com/terms. © Ipsos MORI 2017. 16-084454-01 FSS portion sizes | Version 4 | Public | Internal and Client Use Only | This work was carried out in accordance with the requirements of the international quality standard for Market Research, ISO 20252:2012, and with the Ipsos MORI Terms and Conditions which can be found at http://www.ipsos-mori.com/terms. © Ipsos MORI 2016. Ipsos MORI | June 2017 | 16-084454-01 FSS portion sizes report Version 6 | Internal and Client Use Only | Contents Summary ......................................................................................................................................... -

Ipswich Borough & Suffolk Coastal District Retail and Commercial

Ipswich Borough & Suffolk Coastal District Retail and Commercial Leisure Town Centre Study October 2017 Volume 1 of 3 – Main Report FINAL DRAFT WYG, 90 Victoria Street, Bristol, BS1 6DP Tel: +44 (0) 117 9254393 Email: [email protected] www. wyg .com www.wyg.com creative minds safe hands Contents 1.0 Introduction ..................................................................................................................................... 1 1.1 Instruction ................................................................................................................................................ 1 1.2 Structure of Study ..................................................................................................................................... 2 2.0 Planning Policy Context ................................................................................................................... 4 2.1 Introduction .............................................................................................................................................. 4 2.2 National Planning Policy Framework (NPPF) ................................................................................................. 4 2.3 Ensuring the Vitality of Town Centres Planning Practice Guidance ................................................................. 6 2.4 Housing and Economic Development Needs Assessment Planning Practice Guidance ..................................... 7 2.5 Local Planning Policy Context .................................................................................................................... -

Taxi School 2021 Section 5 SECTION Z RESTAURANTS TAXI SCHOOL

Taxi School 2021 Section 5 SECTION Z RESTAURANTS TAXI SCHOOL Ad Lib Hope St Bothwell St All Bar One St Vincent St West Nile St Alla Turca Pitt St Buchanan St Amarone Nelson Mandela Pl Buchanan St Amber Regent West Regent St Renfield St Amore Ristorante Ingram St Shuttle St Argyle Suite Govan Stand Ibrox Stadium Arta Albion St Bell St Assmaan Bath St West Nile St Banana Leaf Cambridge St Hill St Barburrito Queen St George Sq Bar Soba (Merchant City) Albion St Bell St Barolo Grill Mitchell St Gordon St Battlefield Rest Battlefield Rd Grange Rd Beechwood Ardmay Cres Millport Ave Bella Pasta St Vincent Place North Court Big Feed Govan Rd Pacific Quay Black Sheep Bistro Clarendon St Maryhill Rd Bombay Blues Hope St Argyle St Bouzy Rouge West Regent St Renfield St Brasserie West Regent St Blythswood St Bread Meats Bread St. Vincent St Renfield St BRGR Royal Exchange Sq Queen St BRGR Great Western Road Hamilton Park Ave Buffet Queen Hope St West Regent St Butchershop Sauchiehall St Radnor St Café Antipasti Pitt St Sauchiehall St Café Andaluz St Vincent St Queen St Café Cossachok King St Parnie St Café Gandolfi Albion St Bell St Café India Albion St Bell St Cantina Del Rey King St Osbourne St Captain’s Table North Stand/Janefield St Celtic Park Casa Gandolfi Ingram St John St Celinos Alexandra Parade Wood St Chaophraya Nelson Mandela Pl Buchanan St page one SECTION Z RESTAURANTS TAXI SCHOOL CONTINUE.... China Buffet King Bath St Renfield St China Sea Renfield St Gordon St China Town New City Rd Shamrock St Church on the Hill Langside Ave Algie -

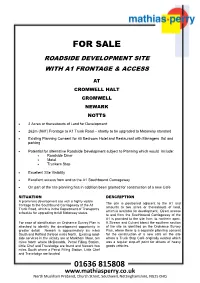

Roadside Development Site with A1 Frontage & Access

FOR SALE ROADSIDE DEVELOPMENT SITE WITH A1 FRONTAGE & ACCESS AT CROMWELL HALT CROMWELL NEWARK NOTTS • 2 Acres or thereabouts of Land for Development • 262m (860’) Frontage to A1 Trunk Road – shortly to be upgraded to Motorway standard • Existing Planning Consent for 40 Bedroom Hotel and Restaurant with Managers flat and parking • Potential for alternative Roadside Development subject to Planning which would include: • Roadside Diner • Motel • Truckers Stop • Excellent Site Visibility • Excellent access from and to the A1 Southbound Carriageway • On part of the site planning has in addition been granted for construction of a new Cafe SITUATION DESCRIPTION A prominent development site with a highly visible The site is positioned adjacent to the A1 and frontage to the Southbound Carriageway of the A1 amounts to two acres or thereabouts of land, Trunk Road, which is in the Department of Transport’s which is available for development. Direct access schedule for upgrading to full Motorway status. to and from the Southbound Carriageway of the A1 is provided to the site from its northern apex. For ease of identification an Ordnance Survey Plan is A Stream and Culvert bisect the southern section attached to identify the development opportunity in of the site as identified on the Ordnance Survey greater detail. Newark is approximately six miles Plan, where there is a separate planning consent South and Retford thirteen miles North. Existing road- for the construction of a new café on the site side services in the vicinity are at Markham Moor, ten where a Truck Stop Café originally existed which miles North where McDonalds, Petrol Filling Station, was a regular stop-off point for drivers of heavy Little Chef and Travelodge are found and Newark two goods vehicles. -

Purple Vouchers Full List of Offers Leeds Book 2017-18

Purple Vouchers full list of offers Leeds book 2017-18 Company Total Offers Total Vouchers Saving Leisure time 4D Golf @ Xplore 1 2 for 1 admission on 4D Golf Up to £5.50 Ashworth Barracks Military 1 2 for 1 on adult admission Up to £7 Museum - Balby Ashworth Barracks Military 1 Half price family ticket Up to £10 Museum - Balby Barley Hall 1 2 for 1 on adult admission Up to £6 Bamburgh Castle 1 2 for 1 on adult admission. Up to £10.85 Bamburgh Castle 1 2 for 1 on child admission Up to £5 Bawtry Paintball Fields 1 5 for 1 on pay as you play Up to £20 Bawtry Paintball Fields 1 3 for 2 on 3 hour laser combat Up to £20 Bawtry Paintball Fields 1 3 for 2 on Tomahawk Axe and Knife throwing Up to £20 Bawtry Paintball Fields 1 3 for 2 on Target Archery Up to £20 Bawtry Paintball Fields 1 Half price rifle shooting Save £80 Bawtry Paintball Fields 1 3 for 2 on a Dead Eyed Dick Shooting Up to £45 Experience Best Western Premier Mount 1 30 Minute Facial Inc. Afternoon Tea For £37.50 Up to £18.50 Pleasant Hotel Best Western Premier Mount 1 1 night stay for 2 people inc. Breakfast for £79 Up to £85 Pleasant Hotel Blackpool Tower Dungeon 1 2 for 1 on admission Up to £16.50 Blackpool Tower Eye 1 2 for 1 on admission Up to £13.50 Blackpool Tower Circus 1 2 for 1 on admission Up to £16.50 Boston Park Farm 1 2 free child tickets with one adult Up to £10 Brit Movie Tours 2 2 for 1 on an Heartbeat tour of filming locations Up to £100 Brit Movie Tours 2 2 for 1 on an Emmerdale Tour of classic Up to £60 locations Cannon Hall Farm 1 £5 off a family ticket Up to -

Dixie Outlet Mall

Dixie Outlet Mall 1250 S Service Rd Property Overview Mississauga, ON L5E 1V4 D'une superficie de 571 000 pieds carrés, le Dixie Outlet Mall est le plus grand centre commercial fermé au Canada dans l'une des régions du Canada qui connaît la croissance la plus rapide. Situé le long de la QEW à Mississauga, le Dixie Outlet Mall abrite plus de 130 magasins d'usine et détaillants à bas prix, notamment Tommy Hilfiger Outlet, Calvin Klein, Guess Factory Store, NIKE Clearance, Levi's Outlet, Famous Footwear, Boathouse Outlet, Winners, Urban. Planet et Laura. Contacts LOCATION Jelena Pukli 416-681-9319 [email protected] LOCATION SPECIALITé Amanda Rakhra 905-278-3494 ext 224 [email protected] GESTIONNAIRE DE Jerry Pollard 905-278-3494 ext 226 [email protected] L'IMMEUBLE DIRECTEUR MARKETING Amanda Rakhra 905-278-3494 ext 224 [email protected] DIRECTEUR DES Eric Puse 905-278-3494 ext 225 [email protected] OPéRATIONS RESPONSABLE DE LA Jordan Hill 905-278-3494 ext 228 [email protected] SéCURITé Dixie Outlet Mall Property Facts TOTAL GLA NUMBER OF FOOD COURT SEATS 426 632 sq ft 448 CRU SQUARE FOOTAGE CRU SALES PER SQ FT 218 840 sq ft $360.00 ANCHORS/MAJORS YEAR BUILT (OVER 20,000 SQ FT) 1956 Laura, Urban Planet, Nike, YEAR LAST RENOVATED Winners 2003 NUMBER OF STORES HOURS OF OPERATION 141 lundi a vendredi 10:00am to 9:00pm samedi 9:30am - 6:00pm dimanche 11:00am - 6:00pm NUMBER OF PARKING SPACES 2500 BUILDING CERTIFICATIONS & AWARDS BOMA Best Silver Dixie Outlet Mall Trade Area Demographics Summary Total Population 5 km: 211,037 10 km: 691,109 15 km: 1,532,695 Average Household Income 5 km: $100,624 10 km: 120,254 15 km: 112,749 Basement Dixie Outlet Mall Dixie Outlet Mall SPRINKLER UP ROOM UP UP MECHANICAL ROOM ELECTRICAL ROOM UP MECHANICAL ROOM UP UP UP UP UP Fantastic Flea Market 50,998 sf B05. -

Dining Guide for Reservations Or Directions Quick 7 Minute Walk

Local Favorites The Loft Bar and Bistro – American (9) 90 South Second St. – 408-291-0677 Drinks and dancing are the draw for this nightlife hotspot in downtown, but it is also known for its Contemporary American Cuisine. From grilled filet mignon with cabernet sauce to a healthy crab cake salad to a wonderful baked halibut, you will have many things for lunch and dinner to choose from. Fuji Sushi – Japanese (10) 56 W. Santa Clara St. – 408-298-3854 Billed as a moderate Japanese restaurant, Fuji Sushi has some of the best sushi in downtown San Jose. Unforgettable favorites such as dragon and spider rolls to Bento boxes and tempura are all within a Dining Guide For reservations or directions quick 7 minute walk. please dial “55” for Concierge Gordon Biersch – American (11) 33 E. San Fernando St. – 408-294-6785 Micro Brews and Garlic Fries! Gordon Biersch has a wonderful pub-type atmosphere combined with a hearty sit-down restaurant that features hearty steak, fish and pasta entrees with salads and great burgers. Original Joe’s – Italian/American (12) 301 South First St. – 408-292-7030 Original Joes is a fine, old-school, authentic- Italian/American restaurant with a rustic Chicago- type atmosphere that has been a San Jose favorite for over 40 years. Huge portions! San Pedro Square (13) Santa Clara St. and San PedroSt. San Pedro Square has a wonderful collection of local The Fairmont San Jose restaurants located within two blocks of each other. 170 S. Market St. San Jose, CA 95113 You can choose from a number of non-chain cuisines such as Mexican, Chinese, Italian, Cuban, Phone: (408) 998-1900 Fax: (408) 287-1648 ( 3). -

Pub Catering - UK - May 2019

Pub Catering - UK - May 2019 The above prices are correct at the time of publication, but are subject to Report Price: £1995.00 | $2693.85 | €2245.17 change due to currency fluctuations. “A shift to eating locally sourced ingredients will lead to demand for more seasonal varieties of meat, fish and vegetables as well as British-made products on pub menus. However, pubs/bars risk missing vital sales opportunities if they fail to cater to under-45s who choose to stay dry, and still enjoy the experience of consuming high-quality alcohol-free drinks.” – Trish Caddy, Senior Foodservice Analyst This report looks at the following areas: BUY THIS • Families just want to have fun REPORT NOW • Baby Boomers' ethical values • 18-24 year olds crave new experiences VISIT: While consumers are still most likely to head to a pub or bar for dinner, visitation continues to spread store.mintel.com across other mealtimes as pubs/bars strengthen their position as a breakfast/brunch and lunch destination. CALL: As consumers become more health-oriented (particularly around consumption of alcohol) and more EMEA value-conscious, food-led pubs have managed to maintain growth by welcoming diners throughout the +44 (0) 20 7606 4533 day, rather than in the evening alone. Whilst growth in the pub catering sector has moderated, Mintel expects the value of the market to grow Brazil by 5% between 2019 and 2023, to reach £8.1 billion. 0800 095 9094 Americas +1 (312) 943 5250 China +86 (21) 6032 7300 APAC +61 (0) 2 8284 8100 EMAIL: [email protected] This report is part of a series of reports, produced to provide you with a DID YOU KNOW? more holistic view of this market reports.mintel.com © 2019 Mintel Group Ltd.