2015 Annual Report

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

2002 Chairman's Letter

Note: The following table appears in the printed Annual Report on the facing page of the Chairman's Letter and is referred to in that letter. Berkshire’s Corporate Performance vs. the S&P 500 Annual Percentage Change in Per-Share in S&P 500 Book Value of with Dividends Relative Berkshire Included Results Year (1) (2) (1)-(2) 1965 .................................................. 23.8 10.0 13.8 1966 .................................................. 20.3 (11.7) 32.0 1967 .................................................. 11.0 30.9 (19.9) 1968 .................................................. 19.0 11.0 8.0 1969 .................................................. 16.2 (8.4) 24.6 1970 .................................................. 12.0 3.9 8.1 1971 .................................................. 16.4 14.6 1.8 1972 .................................................. 21.7 18.9 2.8 1973 .................................................. 4.7 (14.8) 19.5 1974 .................................................. 5.5 (26.4) 31.9 1975 .................................................. 21.9 37.2 (15.3) 1976 .................................................. 59.3 23.6 35.7 1977 .................................................. 31.9 (7.4) 39.3 1978 .................................................. 24.0 6.4 17.6 1979 .................................................. 35.7 18.2 17.5 1980 .................................................. 19.3 32.3 (13.0) 1981 .................................................. 31.4 (5.0) 36.4 1982 ................................................. -

2020 Table 9.Xlsx

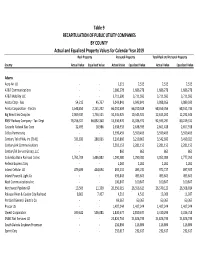

Table 9 RECAPITULATION OF PUBLIC UTILITY COMPANIES BY COUNTY Actual and Equalized Property Values for Calendar Year 2020 Real Property Personal Property Total Real and Personal Property County Actual Value Equalized Value Actual Value Equalized Value Actual Value Equalized Value Adams Aero Air LLC - - 4,647 4,600 4,647 4,600 AT&T Communications - - 1,365,718 1,352,061 1,365,718 1,352,061 AT&T Mobility LLC - - 4,374,524 4,330,779 4,374,524 4,330,779 Avista Corp - Gas 57,107 44,658 2,831,809 2,803,491 2,888,916 2,848,148 Avista Corporation - Electric 2,577,632 2,015,708 66,048,251 65,387,769 68,625,883 67,403,477 Big Bend Elec Coop Inc 2,095,895 1,638,990 10,699,678 10,592,681 12,795,573 12,231,671 BNSF Railway Company - Tax Dept 80,492,277 62,944,961 12,495,871 12,370,912 92,988,148 75,315,872 Cascade Natural Gas Corp 23,845 18,647 5,122,189 5,070,967 5,146,034 5,089,614 Cellco Partnership - - 3,887,710 3,848,833 3,887,710 3,848,833 Century Tel of WA, Inc (T141) 334,132 261,291 2,760,402 2,732,798 3,094,534 2,994,090 CenturyLink Communications - - 2,124,066 2,102,825 2,124,066 2,102,825 Columbia Basin Railroad Co Inc 2,117,474 1,655,865 1,550,963 1,535,454 3,668,437 3,191,318 Federal Express Corp - - 1,260 1,247 1,260 1,247 GATX Corporation - - 17,392,148 17,218,226 17,392,148 17,218,226 Inland Cellular LLC 484,948 379,229 423,122 418,891 908,070 798,120 Inland Power & Light Co - - 412,614 408,487 412,614 408,487 Northwest Pipeline GP 14,159 11,072 31,887,804 31,568,926 31,901,962 31,579,998 Palouse River & Coulee City Railroad 4,516 3,531 -

Warren Buffett: Good Morning and Welcome to Berkshire Hathaway

BERKSHIRE HATHAWAY ANNUAL MEETING 2019 Edited Transcript provided by Yahoo Finance: Warren Buffett: Good morning and welcome to Berkshire Hathaway. For those of you who have come from out of state, welcome to Omaha. The city is delighted to have you here at this event. For those of you who came from outside of the country, welcome to the United States. So, we’ve got people here from all over the world. We’ve got some overflow rooms that are taking care of people. We will just have a few preliminaries and then we will move right into the Q&A period. We’ll break about noon for about an hour. We’ll come back and do more Q&A until about 3:30. Then we’ll adjourn for a few minutes, and then we’ll conduct the meeting. I understand that in the room adjacent, that Charlie has been conducting a little insurgency campaign. I don’t know whether you’ve seen these, but these are the buttons that are available for those of you who keep asking questions about succession. And Charlie wants to answer that question by getting your vote today. So this one says, “Maturity, experience, why accept second best? Vote for Charlie.” I, however, have appointed the monitors who collect the votes, so I feel very secure. Charlie is my partner of 60 years, a director and vice chairman, and we make the big decisions jointly. It’s just that we haven’t had any big decisions. So, we’re keeping him available for the next big one. -

For Immediate Release: March 17, 2020 Contact: Henri Gendreau Cell: (206) 619-6704

For Immediate Release: March 17, 2020 Contact: Henri Gendreau Cell: (206) 619-6704 Journalists of The Roanoke Times to form a union ROANOKE, Va. — Journalists and staff at The Roanoke Times on Tuesday announced plans to unionize as the Timesland News Guild. More than 75 percent of the newsroom — reporters, photographers, graphic artists, copy and online editors, designers and support staff — has signed cards authorizing union representation by The NewsGuild, a sector of the Communications Workers of America (CWA). Unionization among news media workers has surged in recent years. Yet the Timesland News Guild is the first to seek to form a union under Lee Enterprises since the company announced in January that it would take over 30 daily papers from Warren Buffett’s Berkshire Hathaway Media Group. The deal closed Monday. Lee had been managing BH Media’s papers since July 2018. Reliable local news is more vital now than ever. As manager, Lee has already shrunk the size of The Roanoke Times print edition and converted full-time copy editing jobs to part-time, depriving employees of benefits and hurting the quality of our journalism. Prior to the sale this week, BH Media reduced sports and crime coverage, and eliminated or reduced beats dedicated to technology, arts and food. Overall, these far-off corporations have slashed our newsroom by about half over the past six years. Corporate decision-making has hamstrung our circulation colleagues, leading to issues with deliveries, canceled subscriptions and declining revenues. The Timesland News Guild is asking Lee to voluntarily recognize the guild and begin bargaining. -

Kennedy Assassination Newspaper Collection : a Finding Aid

University of South Florida Scholar Commons Special Collections and University Archives Finding Aids and Research Guides for Finding Aids: All Items Manuscript and Special Collections 5-1-1994 Kennedy Assassination Newspaper Collection : A Finding Aid Nelson Poynter Memorial Library. Special Collections and University Archives. James Anthony Schnur Hugh W. Cunningham Follow this and additional works at: https://scholarcommons.usf.edu/scua_finding_aid_all Part of the Archival Science Commons Scholar Commons Citation Nelson Poynter Memorial Library. Special Collections and University Archives.; Schnur, James Anthony; and Cunningham, Hugh W., "Kennedy Assassination Newspaper Collection : A Finding Aid" (1994). Special Collections and University Archives Finding Aids: All Items. 19. https://scholarcommons.usf.edu/scua_finding_aid_all/19 This Other is brought to you for free and open access by the Finding Aids and Research Guides for Manuscript and Special Collections at Scholar Commons. It has been accepted for inclusion in Special Collections and University Archives Finding Aids: All Items by an authorized administrator of Scholar Commons. For more information, please contact [email protected]. Kennedy Assassination Newspaper Collection A Finding Aid by Jim Schnur May 1994 Special Collections Nelson Poynter Memorial Library University of South Florida St. Petersburg 1. Introduction and Provenance In December 1993, Dr. Hugh W. Cunningham, a former professor of journalism at the University of Florida, donated two distinct newspaper collections to the Special Collections room of the USF St. Petersburg library. The bulk of the newspapers document events following the November 1963 assassination of John F. Kennedy. A second component of the newspapers examine the reaction to Richard M. Nixon's resignation in August 1974. -

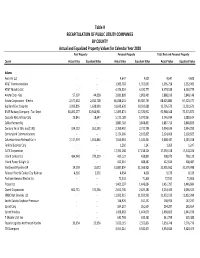

Table 9 RECAPITULATION of PUBLIC UTILITY COMPANIES BY

Table 9 RECAPITULATION OF PUBLIC UTILITY COMPANIES BY COUNTY Actual and Equalized Property Values for Calendar Year 2019 Real Property Personal Property Total Real and Personal Property County Actual Value Equalized Value Actual Value Equalized Value Actual Value Equalized Value Adams Aero Air LLC - - 2,515 2,515 2,515 2,515 AT&T Communications - - 1,686,278 1,686,278 1,686,278 1,686,278 AT&T Mobility LLC - - 3,711,590 3,711,590 3,711,590 3,711,590 Avista Corp - Gas 54,215 45,757 3,043,841 3,043,841 3,098,056 3,089,599 Avista Corporation - Electric 2,548,853 2,151,232 66,010,504 66,010,504 68,559,356 68,161,735 Big Bend Elec Coop Inc 2,069,337 1,746,521 10,545,925 10,545,925 12,615,262 12,292,446 BNSF Railway Company - Tax Dept 79,256,327 66,892,340 13,336,970 13,336,970 92,593,297 80,229,310 Cascade Natural Gas Corp 22,495 18,986 2,638,933 2,638,933 2,661,428 2,657,918 Cellco Partnership - - 3,599,459 3,599,459 3,599,459 3,599,459 Century Tel of WA, Inc (T141) 331,830 280,065 3,210,860 3,210,860 3,542,690 3,490,925 CenturyLink Communications - - 2,281,153 2,281,153 2,281,153 2,281,153 CenturyTel Service Group, LLC - - 860 860 860 860 Columbia Basin Railroad Co Inc 1,761,709 1,486,882 1,290,380 1,290,380 3,052,089 2,777,262 Federal Express Corp - - 1,260 1,260 1,260 1,260 Inland Cellular LLC 479,496 404,694 493,231 493,231 972,727 897,925 Inland Power & Light Co - - 493,843 493,843 493,843 493,843 Noel Communications Inc - - 100,847 100,847 100,847 100,847 Northwest Pipeline GP 13,506 11,399 26,556,615 26,556,615 26,570,120 26,568,014 -

Roanoke School Desegregation and the Politics of Delay

W&M ScholarWorks Dissertations, Theses, and Masters Projects Theses, Dissertations, & Master Projects 2013 Integrating "The Star City of the South": Roanoke School Desegregation and the Politics of Delay Peter Carr Jones College of William & Mary - Arts & Sciences Follow this and additional works at: https://scholarworks.wm.edu/etd Part of the Other Education Commons, and the United States History Commons Recommended Citation Jones, Peter Carr, "Integrating "The Star City of the South": Roanoke School Desegregation and the Politics of Delay" (2013). Dissertations, Theses, and Masters Projects. Paper 1539626722. https://dx.doi.org/doi:10.21220/s2-sa7m-en67 This Thesis is brought to you for free and open access by the Theses, Dissertations, & Master Projects at W&M ScholarWorks. It has been accepted for inclusion in Dissertations, Theses, and Masters Projects by an authorized administrator of W&M ScholarWorks. For more information, please contact [email protected]. Integrating “the Star City of the South”: Roanoke School Desegregation and the Politics of Delay Peter Carr Jones Clearwater, Florida Bachelor of Arts, Washington and Lee University, 2006 A Thesis presented to the Graduate Faculty of the College of William and Mary in Candidacy for the Degree of Master of Arts Lyon Gardiner Tyler Department of History The College of William and Mary May 2013 Integrating “the Star City of the South”: Roanoke School Desegregation and the Politics of Delay Peter Carr Jones Clearwater, Florida Bachelor of Arts, Washington and Lee University, 2006 A Thesis presented to the Graduate Faculty of the College of William and Mary in Candidacy for the Degree of Master of Arts Lyon Gardiner Tyler Department of History The College of William and Mary May 2013 APPROVAL PAGE This Thesis is submitted in partial fulfillment of the requirements for the degree of Master of Arts ^ 1 / F^eter Carr Jones Approved by the Committee, January 2013 ___________ Committee Chair Scott Reynolds Nelson, Legum Professpr of History College of William and Ma M Davison Douglas Dean and Arthur B. -

Newspapers Round a Bend

Reprinted from the November/December 2013 issue of The Financial Manager magazine Newspapers Round a Bend Big bets by Jeffrey Bezos and John Henry, along with recent moves by Warren Buffett, suggest that new views are developing about print media’s worth. The second in a series of four articles on media valuations. By JOHN S. SANDERS ew aNalysts were sur- mature segment: newspapers. Over the past broken in 2013 with a number of large-mar- prised by the surge in merger 12 months the newspaper sector has become ket acquisitions. The activity reflects a new and acquisition activity that is even more vibrant and has turned some type of buyer and likely offers a window into taking place in sectors like tele- important corners. Purchase-price cash flow the future of the newspaper industry. vision and telecommunications multiples have strengthened; newspapers are A number of questions beg to be asked. this year. The combination of a being acquired in larger markets again, and Why does the pace of small-to-medium Fstrengthening economy, record-low lending some of the best minds in the business world market newspaper acquisitions continue rates and improved financial markets sup- are diversifying into daily newspapers. unabated? Why have we seen an increase in ported landmark transactions like Gannett A year ago, the prevailing logic was that large-market acquisitions, as exemplified by Co.’s $2.2 billion acquisition of Belo Corp.’s large-market papers were permanently dis- Jeff Bezos’ acquisition of the The Washington television stations and Verizon’s recently tressed and offered diminishing economic Post and John Henry’s acquisition of the The announced purchase of Vodafone’s stake in potential, primarily because the markets they Boston Globe? And yet in the midst of this Verizon Wireless for $130 billion. -

WLURG36 01 0885.Pdf

• s~ o::. ' This letter also sent to: Mr .. FhiJI.ipf-L. Scruggs, Editor V.rr. Fred N. Naff The Daily Advance ~tor, Editorial Page Lynchburg, Va. Newport News Daily Press Newport Nevre, Va. Mr. William Atkinson, ¥mg. Ed. The Roanoke Times J).fr. William 1'1. Harrison, Editor Roanoke, Va. The Times Herald · Newport News, Va. Mr. W. G. Stouffer, Mng. Ed. The World-Ne~Js 1'4r. Howard E. Lee. Mgn. Ed. Hoanoke, Va. The Daily Press Newport News, Va. Mr. r-1. Carl Andrews, Editor The World-News l{r. Lenoir Chambers, Editor Roanoke, Va. The Virginian Pilot Norfolk, Va. ¥.tr; E. Lewis Knowles, Editor The Evening Leader ¥.a-. li. Marion Saunders, Editor Staunton, Va. The Danville Register Danville, Va. l4r. A. D. Davidson, Editor The Northern Virginia Daily Mr. C. E. Lindsay, Publisher Strasburg, Va. The Progress qharlottesville, Va. !vir. W. J. Missett, Editor The News-Herald ¥r. R. F. Beirne III 1 Mgn. Ed. Suffolk, Va. The CovW:i.ngton Virginian Covington, Va. Mr. c. R. Babcock, Mng. E~. The Progress Mr, Joseph Leslie, Editor Charlottesville, Va. The Ledger-Dispatch Norfolk, Va. Mr. G. Tetley, Editor The Danville Bee Mr. Edw. A. 11fyatt, Editor Danville, Va. The Progress-Index Petersburg, Va. ~fr. A. Robbins, Jr.* Editor The Hopewell News Mr. Thomas A. ptrl!llips, ir•, Ed. Hopewell, Va. The Southwest Times Pulaski 1 Va. Mr. Robert c. Glass,=Editor The Lynchburg Nev1s :ffr. Dan J • Rooker, Editor Lynchburg, Va. The News J ourna.l -~-.__.-: Radford, Va. :tvr..r. K, L. Thompson, Editor The Bulletin, ¥tr. -

Insurance Journal Magazine

MARCH 5, 2012 | VOL. 90, NO. 5 WEST REGION WEST N8 On The Cover Special Report: Auto and Home Inside This Issue Sharing Economy Calls for Insurance Innovation March 5, 2012 • Vol. 90, No. 5 • West Region 10 16 N12 N18 NATIONAL COVERAGE WEST COVERAGE IDEA EXCHANGE N8 Special Report: Auto and Home 8 Smartphone Proof of 28 You Can’t Put a Price on Sharing Economy Calls for Insurance Insurance Bill for California Benefits of Involvement Innovation 8 Nevada Approves Regulations N1 Minding Your Business: Oak N12 Closer Look: The Risks of for Self-Driving Cars and Schoeffler Cloud Computing 10 There’s an App for That: N6 Social Media and Employee N14 Closer Look: What to Know Mobile Phone Quoting Recruiting About Cyber Liability Exposures 16 California Earthquake N36 Closing Quote: Ladner Authority Kicks Off Second N16 P/C Insurers Face Obstacles on Marketing Program for Road to Hard Market Agents N18 Spotlight: 5 Things to Know 20 Alaska’s Hall Saying Farewell About Classic Car Insurance to Director Post N19 Spotlight: Group Personal 26 Insurance Highlights from Excess Liability Gives Added Buffett’s 2011 Letter to Protection Berkshire Shareholders DEPARTMENTS N21 2012 Hospitality Risks Directory 6 Opening Note 9 Declarations 9 Figures 12 People 14 Business Moves N2 MyNewMarkets 4 | INSURANCE JOURNAL-WEST REGION March 5, 2012 www.insurancejournal.com Do we cover landlords? Heck, we cover overlords. Umbrellas for 30 residential and up to 30 commercial units. Rentals and owner-occupied exposures. LLCs, DBAs, estates or trusts are A-OK, but legions of doom are excluded. -

2013-05-06 Warren Buffett Squawk Box Transcript

This is an unofficial transcript of Warren Buffett and Bill Gate appearing live on CNBC’s Squawk Box on Monday, May 6, 2013 from 6 am ET to 9 am ET. ANNOUNCER: The Oracle of Omaha. WARREN BUFFETT: Well, if you have any left over, yeah, mark 'em down, I'll buy one. (LAUGH) ANNOUNCER: Warren Buffett gathering with his faithful. BUFFETT: Let Charlie try and do this. (LAUGHTER) ANNOUNCER: Now he sits down with Squawk Box for a three hour long conversation, the economy, the markets, the business of Berkshire Hathaway. A special presentation begins right now. (MUSIC) BECKY QUICK: Good morning, everybody. Welcome to Squawk Box here on CNBC. I'm Becky Quick, reporting live from Omaha this morning. Joe Kernen and Andrew Ross Sorkin are back at headquarters on the East Coast. We have the man of the morning with us, Warren Buffett. Obviously we have a lot to talk about with him, including stock records runs, the Fed, bonds, the dollar and his deal for Heinz. But first, before we get to all of that, Joe and Andrew will have a short round up of the morning's top headlines. And guys, I'll send it over to you. JOE KERNEN: Okay. Hello. Good morning. Hello, hello— BECKY: Hello. Good morning. JOE: How are you? Hi— Warren. BUFFETT: Well, yeah I— you— JOE: I keep hearing you talk about me, Warren. No one knows what the heck you said, so— I— I don't know. It's like who— (LAUGH) it's like one of the answers you get— BECKY: No, I— (OVERTALK) CNBC SQUAWK BOX TRANSCRIPT: Monday, May 6, 2013 PAGE 1 OF 70 JOE: —to a lot of questions. -

Berkshire's Corporate Performance Vs. the S&P 500 2

Berkshire’s Corporate Performance vs. the S&P 500 Annual Percentage Change in Per-Share in S&P 500 Book Value of with Dividends Relative Berkshire Included Results Year (1) (2) (1)-(2) 1965 ................................................... 23.8 10.0 13.8 1966 ................................................... 20.3 (11.7) 32.0 1967 ................................................... 11.0 30.9 (19.9) 1968 ................................................... 19.0 11.0 8.0 1969 ................................................... 16.2 (8.4) 24.6 1970 ................................................... 12.0 3.9 8.1 1971 ................................................... 16.4 14.6 1.8 1972 ................................................... 21.7 18.9 2.8 1973 ................................................... 4.7 (14.8) 19.5 1974 ................................................... 5.5 (26.4) 31.9 1975 ................................................... 21.9 37.2 (15.3) 1976 ................................................... 59.3 23.6 35.7 1977 ................................................... 31.9 (7.4) 39.3 1978 ................................................... 24.0 6.4 17.6 1979 ................................................... 35.7 18.2 17.5 1980 ................................................... 19.3 32.3 (13.0) 1981 ................................................... 31.4 (5.0) 36.4 1982 ................................................... 40.0 21.4 18.6 1983 ................................................... 32.3 22.4 9.9 1984