GOVERNMENT of SIKKIM Report No. 1 of 2013 Report Of

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Official Site, Telegram, Facebook, Instagram, Instamojo

Page 1 Follow us: Official Site, Telegram, Facebook, Instagram, Instamojo All SUPER Current Affairs Product Worth Rs 1200 @ 399/- ( DEAL Of The Year ) Page 2 Follow us: Official Site, Telegram, Facebook, Instagram, Instamojo SUPER Current Affairs MCQ PDF 3rd August 2021 By Dream Big Institution: (SUPER Current Affairs) © Copyright 2021 Q.World Sanskrit Day 2021 was celebrated on ___________. A) 3 August C) 5 August B) 4 August D) 6 August Answer - A Sanskrit Day is celebrated every year on Shraavana Poornima, which is the full moon day in the month of Shraavana in the Hindu calendar. In 2020, Sanskrit Day was celebrated on August 3, while in 2019 it was celebrated on 15 August. Sanskrit language is believed to be originated in India around 3,500 years ago. Q.Nikol Pashinyan has been re-appointed as the Prime Minister of which country? A) Ukraine C) Turkey B) Armenia D) Lebanon Answer - B Nikol Pashinyan has been re-appointed as Armenia’s Prime Minister by President Armen Sarkissian. Pashinyan was first appointed as the prime minister in 2018. About Armenia: Capital: Yerevan Currency: Armenian dram President: Armen Sargsyan Page 3 Follow us: Official Site, Telegram, Facebook, Instagram, Instamojo Q.Min Aung Hlaing has taken charge as the Prime Minister of which country? A) Bangladesh C) Thailand B) Laos D) Myanmar Answer - D The Chief of the Myanmar military, Senior General Min Aung Hlaing has taken over as the interim prime minister of the country on August 01, 2021. About Myanmar Capital: Naypyitaw; Currency: Kyat. NEWLY Elected -

The State Bank of Sikkim (Acquisition of Shares) and Miscellaneous Provisions Act, 1982 Act No

THE STATE BANK OF SIKKIM (ACQUISITION OF SHARES) AND MISCELLANEOUS PROVISIONS ACT, 1982 ACT NO. 62 OF 1982 [6th November, 1982.] An Act to provide, in the public interest, for the acquisition of certain shares of the State Bank of Sikkim for the purpose of better consolidation and extension of banking facilities in the State of Sikkim and for matters connected therewith or incidental thereto. WHEREAS for the purpose of better consolidation and extension of banking facilities in the State of Sikkim, it is expedient to provide for a single apex banking institution in that State, and for that purpose to provide for the acquisition of certain shares of the State Bank of Sikkim and for matters connected therewith or incidental thereto; BE it enacted by Parliament in the Thirty-third Year of the Republic of India as follows:— CHAPTER I PRELIMINARY 1. Short title and commencement.—(1) This Act may be called the State Bank of Sikkim (Acquisition of Shares) and Miscellaneous Provisions Act, 1982. (2) It shall come into force on such date as the Central Government may, by notification in the Official Gazette, appoint. 2. Definitions.—In this Act, unless the context otherwise requires,— (a) “appointed day” means the date on which this Act comes into force; (b) “co-operative bank” means the Sikkim State Co-operative Bank Limited, a society registered under the Sikkim Co-operative Societies Act, 1978 (Sikkim Act No. 12 of 1978); (c) “notification” means a notification published in the Official Gazette; (d) “prescribed” means prescribed by rules made -

Booklet on Measurement of Digital Payments

BOOKLET ON MEASUREMENT OF DIGITAL PAYMENTS Trends, Issues and Challenges Revised and Updated as on 9thMay 2017 Foreword A Committee on Digital Payments was constituted by the Ministry of Finance, Department of Economic Affairs under my Chairmanship to inter-alia recommend measures of promotion of Digital Payments Ecosystem in the country. The committee submitted its final report to Hon’ble Finance Minister in December 2016. One of the key recommendations of this committee is related to the development of a metric for Digital Payments. As a follow-up to this recommendation I constituted a group of Stakeholders under my chairmanship to prepare a document on the measurement issues of Digital Payments. Based on the inputs received from RBI and Office of CAG, a booklet was prepared by the group on this subject which was presented to Secretary, MeitY and Secretary, Department of Economic Affairs in the review meeting on the aforesaid Committee’s report held on 11th April 2017 at Ministry of Finance. The review meeting was chaired by Secretary, Department of Economic Affairs. This booklet has now been revised and updated with inputs received from RBI and CAG. The revised and updated booklet inter-alia provides valuable information on the trends in Digital Payments in 2016-17. This has captured the impact of demonetization on the growth of Digital Payments across various segments. Shri, B.N. Satpathy, Senior Consultant, NISG, MeitY and Shri. Suneet Mohan, Young Professional, NITI Aayog have played a key role in assisting me in revising and updating this booklet. This updated booklet will provide policy makers with suitable inputs for appropriate intervention for promoting Digital Payments. -

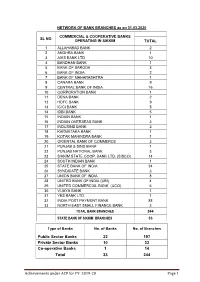

Achievements Under ACP for FY: 2019-20 Page 1 Public Sector Banks 22

NETWORK OF BANK BRANCHES as on 31.03.2020 COMMERCIAL & COOPERATIVE BANKS SL NO. OPERATING IN SIKKIM TOTAL 1 ALLAHABAD BANK 2 2 ANDHRA BANK 1 3 AXIS BANK LTD 10 4 BANDHAN BANK 1 5 BANK OF BARODA 3 6 BANK OF INDIA 2 7 BANK OF MAHARASHTRA 1 8 CANARA BANK 9 9 CENTRAL BANK OF INDIA 16 10 CORPORATION BANK 1 11 DENA BANK 2 12 HDFC BANK 9 13 ICICI BANK 5 14 IDBI BANK 5 15 INDIAN BANK 1 16 INDIAN OVERSEAS BANK 3 17 INDUSIND BANK 2 18 KARNATAKA BANK 1 19 KOTAK MAHINDRA BANK 1 20 ORIENTAL BANK OF COMMERCE 3 21 PUNJAB & SIND BANK 1 22 PUNJAB NATIONAL BANK 3 23 SIKKIM STATE COOP. BANK LTD. (SISCO) 14 24 SOUTH INDIAN BANK 1 25 STATE BANK OF INDIA 34 26 SYNDICATE BANK 3 27 UNION BANK OF INDIA 8 28 UNITED BANK OF INDIA (UBI) 4 29 UNITED COMMERCIAL BANK (UCO) 6 30 VIJAYA BANK 1 31 YES BANK LTD. 1 32 INDIA POST PAYMENT BANK 88 33 NORTH EAST SMALL FINANCE BANK 2 TOTAL BANK BRANCHES 244 STATE BANK OF SIKKIM BRANCHES 53 Type of Banks No. of Banks No. of Branches Public Sector Banks 22 197 Private Sector Banks 10 33 Co-operative Banks 1 14 Total 33 244 Achievements under ACP for FY: 2019-20 Page 1 DISTRICT-WISE BANK BRANCH as on 31.03.2020 NO. OF BRANCHES DISTRICT-WISE BANKS IN SIKKIM NORTH EAST SOUTH WEST TOTAL 1 ALLAHABAD BANK 0 2 0 0 2 2 ANDHRA BANK 0 1 0 0 1 3 AXIS BANK LTD 1 6 1 2 10 4 BANDHAN BANK 0 1 0 0 1 5 BANK OF BARODA 0 3 0 0 3 6 BANK OF INDIA 0 2 0 0 2 7 BANK OF MAHARASHTRA 0 1 0 0 1 8 CANARA BANK 1 5 2 1 9 9 CENTRAL BANK OF INDIA 1 8 1 6 16 10 CORPORATION BANK 0 1 0 0 1 11 DENA BANK 0 1 1 0 2 12 HDFC BANK LTD 0 6 3 0 9 13 ICICI BANK LTD 0 2 2 -

List of Appellate Authority, S.P.I.O's & A.P.I.O

1 STATEMENT OF TRANSPARENCY OFFICER/APPELLATE AUTHORITY/SPIO/ASPIO RECEIVED FROM DEPARTMENTS/PSUs. Sl.No. Name of Department Appellate Authority SPIO ASPIO Phone No. & Fax No. & website 1. Animal Husbandry LF & 1. Dr. Sangay D.Bhutia, Addl. 1. Dr. P.K. Pradhan, l 1. Dr. N.M.Cintury, Jt. sikkim- VS Department Director (East) 9434127258 Direcor, (E&T) Director (West) ahvs.gov.in 2. Dr. S.K.Subba, Addl. 9434179031 9733047890 Director (North) 2. Dr. Puspa Kala Rai, 2. Dr. D.P.Pradhan, Jt. 9434241634 Director, (VS) Director (East) 3. Dr.Sanjay Pradhan, Jt. 9932706073 9609833698 Director (West) 9733051860 3. Dr. K.T. Bhutia, Jt. 4. Dr. Tilotama Bajgai, Jt. Director (North) Director (South) 9434179407 9434033008 4. Dr.Arthalal Rai, Dy. 5. Dr. N.T.Bhutia, Director Director (South) (VS) 9800815776 (a) Directorate of Fisheries Shri. Sunil Pradhan, Additional Shri C.S Rai, Jt. Director-II (i) Shri. Man Kumar Rai, sikkim- Director U.S/Gangtok/East ahvs.gov.in Mobile No: 9434109803 (ii) Shri Devi Bdr. Rai Jt. Director/East (iii) Shri Chuman Singh Rai, Jt.Director/South Dist. (iv) Shri Nagendra Dhakal , Dy. Director/North Dist. 2 2. Buildings & Housing Shri Kuldip Chettri, C.S 1. Shri M.N Dhakal, Spl. 1. Shri. Sonam Pinsto Bhutia, Department Secretary, (Adm.) DE (South) Gangtok 7319565234 9733017987 2. Shri Bidlat Rai, D.E (N/E) 2. Smt. Yogita Rai, Jt. Gnagtok 9647859299 3. Shri. Saurav T.Lepcha Chief Architect, Gangtok (HQ) - 9434408980 9434110063 4. Shri. Karma Yangtey, DE (Project I) Gangtok 3. Shri S.S Timsina D.E 9474529106 (N/E) 5. -

1. List of Fair Price Shops Under Gangtok Food Godown, East District SL

1. List of Fair Price Shops under Gangtok Food Godown, East District SL. Registartion No Name of FPS Address 1 01/E/GFPS-01 M/s Mingma Lhamu Tathengchen 2 01/E/GFPS-02 M/s M.P.C.S Ltd Upper Tathengchen 3 01/E/GFPS-03 M/s Passangkit Bhutia Upper Tathengchen 4 01/E/GFPS-04 M/s Tshering Doma Lower Tathengchen 5 01/E/GFPS-05 M/s Harish Chandra Gupta Chandmari 6 01/E/GFPS-06 M/s Karma Tenzing Bhutia Chandmari 7 01/E/GFPS-07 M/s Katuk Bhutia Upper Chandmari 8 01/E/GFPS-08 M/s Nima Doma Bhutia Chandmari 9 01/E/GFPS-09 M/s Hira Prasad Chandmari 10 01/E/GFPS-010 M/s Kaushila Lepcha Upper Chandmari 11 01/E/GFPS-011 M/s Om Prakash Mittal Chandmari 12 01/E/GFPS-012 M/s Bhagawati Pradhan Rongek 13 01/E/GFPS-013 M/s C.C.S Ltd. Yalley Bhusuk 14 01/E/GFPS-014 M/s Akkee Bhutia Bhusuk 15 01/E/GFPS-015 M/s Harka Maya Rai Bhusuk 10th Mile 16 01/E/GFPS-016 M/s Chenpa Doma Bhutia Pabik Naitam 17 01/E/GFPS-017 M/s Krishna Kri. Rai Naitam Nandok 18 01/E/GFPS-018 M/s Jasmati Rai Naitam Block 19 01/E/GFPS-019 M/s M.P.C.S Ltd Assam Linzey 20 01/E/GFPS-020 M/s Sudhama Pandit Kazi Road 21 01/E/GFPS-021 M/s Lobsang Choden Kazi Road 22 01/E/GFPS-022 M/s Kessang Bhutia Nam Nang 23 01/E/GFPS-023 M/s T. -

Chronological List of Central Acts ------Page: 1

CHRONOLOGICAL LIST OF CENTRAL ACTS -------- PAGE: 1 Name of the Act Year Act No -------------------------------------------------- ---------- -------------------------------------------------------------------- Bengal Indigo Contracts Act 1836 10 Bengal Districts Act 1836 21 Madras Public Property Malversation Act 1837 36 Bengal Bonded Warehouse Association Act 1838 5 Coasting Vessels Act 1838 19 Madras Rent and Revenue Sales Act 1839 7 Bengal Land Revenue Sales Act 1841 12 Revenue, Bombay 1842 13 Revenue Commissioners, Bombay 1842 17 Sales of Land for Revenue Arrears 1845 1 Boundary-marks, Bombay 1846 3 Boundaries 1847 1 Bengal Alluvion and Diluvion Act 1847 9 Bengal Land Holders' Attendance Act 1848 20 Madras Revenue Commissioner Act 1849 10 Judicial Officers Protection Act 1850 18 Calcutta Land-revenue Act 1850 23 Forfeited Deposits Act 1850 25 Improvements in Towns 1850 26 Indian Tolls Act 1851 8 Madras City Land Revenue Act 1851 12 Bombay Rent-free Estates Act 1852 11 Rent Recovery Act 1853 6 Shore Nuisances (Bombay and Kolaba) Act 1853 11 Bengal Bonded Warehouse Association Act 1854 5 Police, Agra 1854 16 Legal Representatives' Suits Act 1855 12 Fatal Accidents Act 1855 13 Usury Laws Repeal Act 1855 28 Bengal Embankment Act 1855 32 Sonthal Parganas Act 1855 37 Indian Bills of Lading Act 1856 9 Calcutta Land-revenue Act 1856 18 Bengal Chaukidari Act 1856 20 Tobacco Duty (Town of Bombay) Act 1857 4 Oriental Gas Company 1857 5 Madras Compulsory Labour Act 1858 1 Bengal Ghatwali Lands Act 1859 5 Bengal Rent Act 1859 10 Bengal Land Revenue -

Sikkim Government Gazette

SIKKIM GOVERNMENT GAZETTE EXTRAORDINARY PUBLISHED BY AUTHORITY Gangtok Friday 24th May, 2019 No. 243 ELECTION DEPARTMENT, GANGTOK No. 24/2019/Elec Dated: 24th May 2019 Notification No. 308/SKM-LA/2019 dated 24th May, 2019 of the Election Commission of India, Nirvachan Sadan, New Delhi is hereby re-published for general information. ELECTION COMMISSION OF INDIA Nirvachan Sadan, Ashoka Road, New Delhi – 110001 Dated 24th May, 2019 3 Jyaistha, 1941, (Saka). NOTIFICATION No. 308/SKM-LA/2019: - Whereas, in pursuance of the Notification No. 32/Home/2019 issued by the Governor of Sikkim on 18th March, 2019 under sub-section (2) of Section 15 of the Representation of the People Act, 1951 (43 of 1951), a General Election has been held for the purpose of constituting a new Legislative Assembly for the State of Sikkim; and Whereas, the results of the elections in all the Assembly Constituencies of Sikkim, in the said General Election have been declared by the Returning Officers concerned Now, therefore, in pursuance of Section 73 of the Representation of the People Act, 1951 (43 of 1951), the Election Commission of India hereby notifies the names of the Members elected for those Assembly Constituencies, along with their party affiliation, if any, in the SCHEDULE to this Notification. By Order, ARVIND ANAND SECRETARY, ELECTION COMMISSION OF INDIA. R. TELANG, IAS CHIEF ELECTORAL OFFICER/SIKKIM - 1 - S.G.P.G. - 243/ Com. 2/Gazette /100 Nos./ Dt:- 24. 05. 2019. SCHEDULE TO NOTIFICATION No. 308/SKM-LA/2019, DATED 24th MAY, 2019 OF ELECTION COMMISSION OF INDIA NAME OF THE STATE: SIKKIM S. -

Government of Sikkim

GOVERNMENT OF SIKKIM MEMORANDUM TO THE FOURTEENTH FINANCE COMMISSION VOLUME – III SUBSIDIARY POINTS (NOTES ON TOPICS-STATE) FINANCE, REVENUE & EXPENDITURE DEPARTMENT Contents I. BASE AND RATES OF STATE TAXES, DUTIES ETC .............................................. 1 1. Land Revenue ............................................................................................................ 1 (a) Base and existing rates of land ............................................................................... 1 (b) In some States in addition to irrigation,. .................................................................. 1 (c) The size of holdings – un-irrigated and irrigated ...................................................... 2 (d) Any cess on land revenue whether land revenue .................................................... 2 2. Agricultural Income Tax .............................................................................................. 2 (a) Base and existing rates. .......................................................................................... 2 (b) Changes made in the base/rates during each of the last three years ...................... 2 3. Tax on Urban Land ..................................................................................................... 2 (a) Base and prevailing rates of tax from 2010-11 onward (year-wise). ........................ 2 (b) Rate of premium for conversion of agricultural land to non-agricultural uses. .......... 2 (c) The base and tax rate of (a) & (b) above in 2010-11. -

Shortlisted Candidate for the Post of Office Superintendent

1 SHORTLISTED CANDIDATE FOR THE POST OF OFFICE SUPERINTENDENT SL. Name and Address of the Applicant NO. (Contact & Email Id) 1. Mr. Amit Gazmer S/o of Mr. Shri Bhakta Badr. Gazmer High Court of Sikkim, Gangtok 9593883774 2. Mr. Abhay Kumar, S/o Mr. Harendra Prasad Yadav At-2M/97 B H Colony Bhoothnath,Road Kankarbagh, Patna 9708726701 7011287320 3. Ms. Alina Rai, D/O Ganga Prasad rai Singithang, South Sikkim 9432092096, 78728, 93846 [email protected] 4. Ms. Aruna Chhetri, D/o Mr Kamal Das Chjhetri R.o. Upper Syari, Gangtok, East Sikkim 78729-69762 [email protected] 5. Ms. Alenla Bhutia, D/o Mr. Tashi Tobden Bhutia 51/2, Upper Gumpa Ghurpisey, Namchi,South Sikkim 737126 8597643493 [email protected] 6. Ms. Arati Chettri D/o Mr.Prahlad Chettri Kartak Busty, Namchaybung Pakyong, East Sikkim 7076052811 [email protected] 7. Mr. Allen Subba D/o. Mr. Budhi Man Subba Chota Singtam, Ranipool, East Sikkim 7872970355 8. Mr. Abinash Pradhan, S/o Mr. Purna Bdr. Pradhan Aritar Mareydara, East Sikkim. 8016772039 9. - Ms. Anu Chettri D/o Mr. bal Brd Chettri - Tallo Syari PW Syari, Tadong, East Sikkim. 10. - Mr. Abishek Tamang S/o Mr. Karma Tamang - Rongneck, Maneydara, East Sikkim. - 8637810455 11. - Mr. Amit Manger, S/o Mr. Damber Singh Manger - Sumbuk, Kamarey, South Sikkim. - 9593380984, 7908595546 12. - Mr. Abhishek Chettri, S/o Mr. Purna Bdr Chettri - Dikchu, East Sikkim. - 9609703318, 9832655515 13. Mr. Ajay Chettri, S/o Late Sitaram Chettri Mengwa Forest, Teesta Bazar, W.B. 9475659679 2 14. Mr. Attendra Raj Bagdas, S/o Shri Anil Kr Bagdas Development Area, Gangtok. -

Minutes of the 60Th SLBC Meeting, Sikkim Held on 19Th March 2019 at the Conference Hall of Tashiling, Secretariat, Gangtok

Minutes of the 60th SLBC Meeting, Sikkim held on 19th March 2019 At The Conference Hall of Tashiling, Secretariat, Gangtok The 60th Meeting of State Level Bankers’ Committee (SLBC) for the State of Sikkim was held at The Conference Hall of Tashiling, Secretariat, Gangtok on 19th March 2019. The meeting was chaired by Shri A.K. Srivastava, IAS, Chief Secretary, Govt. of Sikkim Shri Thomas Chandy, IFS, Principal Secretary, Commerce and Industries Dept, Govt. of Sikkim, Shri C S Rao, IFS, Principal Secretary, Rural Management and Development Department, Govt. of Sikkim, Dr. P Senthil Kumar, IAS, Commissioner, Rural Management and Development Department, Govt. of Sikkim, Shri Naresh Yadav, GM, State Bank of India, LHO, Kolkata, Shri Olden Nongpluh , GM, RBI, Gangtok, Smt R Tshering, GM, NABARD Gangtok & Shri Satish Rao, DGM, State Bank of India, Zonal Office, Siliguri, were the other dignitaries on the dais. Shri Surender Singh, Deputy Secretary, Department of Financial Services, Govt of India was also present in the meeting. State Bank of Sikkim and India Post Payment Bank were the special invitees in the meeting, represented by Shri. P Wangdi Bhutia, Chief General Manager State Bank of Sikkim and Shri Mridul Das, Senior Manager, India Post Payment Banks,respectively. Representatives from member Banks and Government Departments also attended the meeting. Shri Aftab Ahmad Mallick, Regional Manager, State Bank of India and SLBC Convenor , welcomed the dignitaries on the dais as well as all the stakeholders present in the meeting. He also introduced and welcomed to the house, Shri P Wangdi Bhutia, Chief General Manager, State Bank of Sikkim as a special guest . -

Scanned by Camscanner ANNEXURE I

Scanned by CamScanner ANNEXURE I (1) EAST DISTRICT (A) BLOCK RATES UNDER GANGTOK SUB-DIVISION PROPOSED MARKET RATE SL NO. REVENUE CIRCLE REVENUE BLOCK PER SQ. FT (IN RS) ARITHANG (GANGTOK STATION) 1617 GNATHANG 20 1 GANGTOK CHANDMARI 243 BURTUK 409 GANGTOK (PIONEER RESERVE) 1617 UPPER TADONG 1039 2 TADONG SAMDUR 619 TADONG 660 SYARI 166 UPPER TATHANGCHEN 178 3 SICHEY TATHANGCHEN 336 SICHEY 523 RONGYEK 184 NANDOK 183 NAITAM 67 ASSAM 100 4 NAITAM BHUSUK 67 LINGZEY 67 NAMONG 67 CHOTA SINGTAM 325 RALEY KHESE 59 TINTEK 67 5 SAMDONG KAMBAL 38 RAKDONG 47 SAMDONG 177 NAVEY 51 SHOTAK 141 6 LINGDOK PENLONG 310 NAMPHONG 146 LINGDOK 83 MARTAM 229 NAZITAM 42 TIRKUTAM 42 SIRWANI 178 SAKYONG 104 7 SANG CHISOPANI 525 NAMGEYTHANG 55 PHENGYONG 42 RAPDANG 42 BYANGSANG 30 TSHALUMTHANG 110 1 KHAMDONG 37 DUNG - DUNG 114 SINGBEL 313 8 KHAMDONG ARITAR 38 BENG 38 BUDANG THANGSING 37 TUMIN 42 SIMIK 48 9 TUMIN CHADEY 42 PATUK 48 LINGZEY 42 SANGTONG 163 RANKA 190 BARBING 151 LINGDUM 104 10 RANKA LUING 133 REY MINDU 20 REY 20 PARBING 138 CHINZEY 85 RAWTEY RUMTEK 290 SAJONG - RUMTEK 139 CHUBA 158 11 RUMTEK NAMIN 36 NAMLI 353 TUMLABUNG 63 MARCHAK 503 (B) BLOCK RATES UNDER RONGLI SUB-DIVISION. PROPOSED MARKET RATE SL NO. REVENUE CIRCLE REVENUE BLOCK PER SQ. FT (IN RS) ROLEP 18 LAMATEN 18 1 RONGLI CHUJACHEN 20 CHANGEYLAKHA 20 RONGLI BAZAR 378 DALAPCHAND 43 SOUTH REGU 20 SUBANEYDARA 22 NORTH REGU 20 2 SUBANEYDARA PHADAMCHEN 20 PREMLAKHA 20 LINGTAM 20 SINGANEYBAS 20 RHENOCK BAZAR 262 RHENOCK 34 TARPIN 31 3 RHENOCK MULUKEY 43 ARITAR 52 SUDUNGLAKHA 43 2 (C) BLOCK RATES UNDER PAKYONG SUB-DIVISION.