Government of Sikkim

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Official Site, Telegram, Facebook, Instagram, Instamojo

Page 1 Follow us: Official Site, Telegram, Facebook, Instagram, Instamojo All SUPER Current Affairs Product Worth Rs 1200 @ 399/- ( DEAL Of The Year ) Page 2 Follow us: Official Site, Telegram, Facebook, Instagram, Instamojo SUPER Current Affairs MCQ PDF 3rd August 2021 By Dream Big Institution: (SUPER Current Affairs) © Copyright 2021 Q.World Sanskrit Day 2021 was celebrated on ___________. A) 3 August C) 5 August B) 4 August D) 6 August Answer - A Sanskrit Day is celebrated every year on Shraavana Poornima, which is the full moon day in the month of Shraavana in the Hindu calendar. In 2020, Sanskrit Day was celebrated on August 3, while in 2019 it was celebrated on 15 August. Sanskrit language is believed to be originated in India around 3,500 years ago. Q.Nikol Pashinyan has been re-appointed as the Prime Minister of which country? A) Ukraine C) Turkey B) Armenia D) Lebanon Answer - B Nikol Pashinyan has been re-appointed as Armenia’s Prime Minister by President Armen Sarkissian. Pashinyan was first appointed as the prime minister in 2018. About Armenia: Capital: Yerevan Currency: Armenian dram President: Armen Sargsyan Page 3 Follow us: Official Site, Telegram, Facebook, Instagram, Instamojo Q.Min Aung Hlaing has taken charge as the Prime Minister of which country? A) Bangladesh C) Thailand B) Laos D) Myanmar Answer - D The Chief of the Myanmar military, Senior General Min Aung Hlaing has taken over as the interim prime minister of the country on August 01, 2021. About Myanmar Capital: Naypyitaw; Currency: Kyat. NEWLY Elected -

South District of Forest Environment & Wildlife Management Department in Their Respective GPU/Ward with Immediate Effect

GOVERNMENT OF SIKKIM DEPARTMENT OF FOREST ENVIRONMENT & WILDLIFE MANAGEMENT FOREST SECRETARIAT, DEORALI, GANGTOK SIKKIM-737102 No: 606/ADM/FEWMD Dated: 30/01/2019 OFFICE ORDER With the approval of the competent authority, the following employees appointed on temporary ad-hoc basis under “One Family One Job Scheme” are hereby posted under various Divisions South District of Forest Environment & Wildlife Management Department in their respective GPU/Ward with immediate effect:- Sl. POST APPOINTED Reporting NAME CONSTITUENCY GPU/ WARD No. No. FOR Officer Environmental Rangang Lower Togday Ms. Shanti Maya Rai Assistant Yangang Ward DFO (T) 1 South Environmental Nambung Ward DFO (T) 2 Ms. Rekha Subba Temi Namphing Assistant Temi Namphing South Lower Sripatam Environmental Yangyang Mr. Rajesh Dahal Ward, Yangang DFO (T) 3 Assistant Rangang Rangrang South Environmental Rolak Kabey Ward, DFO (T) 4 Mr. Nutan Subba Temi Namphing Assistant Temi Namphing South Ms. Elizabeth Environmental Namchi DFO (T) 5 Rong Ward Gurung Assistant Singhithang South 12 Bermiok Tokal 6 Mr. Bishal Tamang Multi-task Office Staff Temi Namphing GPU Upper Tokal DFO (T) No. 5 South Environmental DFO(WL) 7 Ms. Namrata Nepal Temi Namphing Lower Tarku Assistant South Environmental Salghari Zoom DFO(WL) 8 Mr. Suman Rai Khaling Gaon Ward Assistant (SC) South Lingee Shokpay Environmental Tumin Lingee Mr. Sagar Rai GPU, Maidam DFO(WL) 9 Assistant (BL) Ward South Mr. Devi Charan Environmental Rangang Upper Kolthang DFO(WL) 10 Chettri Assistant Yangang Ward South Environmental Namthang DFO(WL) 11 Mr. Santa Tamang Kolbung Assistant Rateypani South Environmental DFO(WL) 12 Ms. Chabi Maya rai Barfung (BL) Lamten Tingmoo Assistant South Environmental Rangang DFO (E & 13 Ms. -

National Institute of Technology Sikkim Ravangla Campus

NATIONAL INSTITUTE OF TECHNOLOGY SIKKIM RAVANGLA CAMPUS Closing Date for submission extended till 30th Nov-2016 Notice inviting applications for Empanelment of Hotel/Guest House Accommodations & Rate Contract Tender No: 100/NITS/HotelEmpanelment/16-17/602/609 Date: 21.11.2016 EXPRESSION OF INTEREST FOR EMPANELMENT OF HOTEL / GUEST HOUSE ACCOMMODATION & RATE CONTRACT IN RAVANGLA AND NAMCHI, SOUTH SIKKIM AND SILIGURI / NJP, W.B.: RATE CONTRACT TO BE VALID TILL 30TH SEPTEMBER 2017. Closing Data for submission 30.11.2016 (5pm) Opening Date & Time 01.12.2016 (3 pm ) Application Fees (Non-refundable) ₹500/- (Rupees Five Hundred only) as DD in favour of The Director, NIT Sikkim Bid to be submitted to Faculty In-charge, Store & Purchase Activities, National Institute of Technology Sikkim, Ravangla Campus, Barfung, South Sikkim, 737139. Place of opening of bid Conference Hall, National Institute of Technology Sikkim, Ravangla Campus, Barfung, South Sikkim, 737139 Background: National Institute of Technology Sikkim is an autonomous body set up by Govt. of India, under Ministry of Human Resource & Development; New Delhi. It is one of the newly setup NIT’s and is an institute of National Importance. NIT Sikkim is looking for hotel/guest house accommodation in around Ravangla, Namchi and also in Siliguri for accommodating visiting guest and official of institute. Applications in prescribed format along with documentary proof are invited from registered hotel/guest houses from Ravangla, Namchi and Siliguri having fully furnished rooms. Eligibility Criteria of Intending Hotel/guest house empanelment: (Proof/supporting documents to be enclosed for the points mentioned below: a. The firm must be registered with the concerned authority, Govt. -

District Election Plan for General Elections 2014

District Election Plan for General Elections 2014 South District, Sikkim 2 Contents 1 DISTRICT PROFILE ........................................................................................................................................... 8 1.1 GEOGRAPHY ........................................................................................................................................................ 8 1.2 DEMOGRAPHY ...................................................................................................................................................... 8 1.3 ADMINISTRATIVE UNIT ............................................................................................................................................... 9 1.4 ASSEMBLY CONSTITUENCIES IN SOUTH SIKKIM .......................................................................................................... 10 1.4.1 9 – BERFUNG ........................................................................................................................................ 11 1.4.2 10-POKLOK-KAMRANG ........................................................................................................................ 11 1.4.3 11-NAMCHI-SINGHITHANG .................................................................................................................. 13 1.4.4 12-MELLI .............................................................................................................................................. 14 1.4.5 13-NAMTHANG-RATEYPANI ............................................................................................................... -

November 26 0 20191126.Pdf

SIkKIM HERALD Vol. 63 No. 75 visit us at www.ipr.sikkim.gov.in Gangtok (Tuesday) November 26, 2019 Regd. No.WB/SKM/01/2017-19 th Sikkim Legislative Assembly Secretariat Governor attends 50 Governor’s Sonam Tshering Marg, Gangtok, Sikkim, 737101 No.259/L&PA Dated:20/11/2019 Conference NOTIFICATION the country was concerned In exercise of the power conferred under Rule16 of the Rules of Governor stressed on its up Procedure and Conduct of Business in Sikkim Legislative Assembly, gradation and expediting Shri L.B.Das, Hon’ble Speaker Sikkim Legislative Assembly has been construction of alternate highway pleased to reconvene a sitting of the House in the Assembly Hall, to Sikkim. This is necessary in view Gangtok on 28th November, 2019 at 11:00 a.m. of Sikkim’s developmental needs, The Hon’ble Members are notified accordingly. tourism and above all, the national security, he said. By order Railway Connectivity: Sd/- Expressing concern and Dr.(Gopal Pd. Dahal) SLASS displeasure about the slow pace Secretary of construction of the much awaited Sevoke-Rangpo Rail Link project, Governor drew the attention of Railway Ministry and Sikkim receives India stressed on its early completion for the benefit of the State and the country as a whole. Today 2019 Awards Air Connectivity: Governor while highlighting the issues and bottlenecks which has halted the flight operations at Pakyong President, Mr. Ram Nath Kovind, Governor Mr. Ganga Prasad, Airport from June 1 this year and th respective Governors and Lt. Governors during the 50 Governor’s the obvious sense of Conference at Rashtrapati Bhawan, New Delhi. -

Table of Contents

Plan for Conservation and Sustainable Utilization of Medicinal Plants Sikkim 2003 Table of Contents i. Acknowledgements ii. Executive Summary iii. Abbreviations used iv. Glossary of local terms 1 Introduction ……… 8 - 10 2 Profile of the Area ……… 11 - 21 3 Process or Methodology ……… 22 - 28 4 Statement of Threats pertaining to Medicinal Plants and Local Health Cultures ……… 29 - 32 5 Ongoing Initiatives related to Medicinal Plants and Local Health Cultures ……… 33 - 45 6 Strategy for conservation of Medicinal Plants and Local Health Cultures ……… 46 - 56 7 Action Plan for conservation of Medicinal Plants and Local Health Cultures ……… 57 - 75 8 Tentative Budgetary Requirements ……… 76 9 References and Bibliography ……… 77 10 Appendix ……… 78 - 99 Prepared by the Sikkim State Level Planning Committee 1 Plan for Conservation and Sustainable Utilization of Medicinal Plants Sikkim 2003 Appendix Appendix 1: State Level Planning Committee and Working Group .……… 78 Appendix 2: List of Medicinal Plants of Sikkim .……… 80 Appendix 3: Summary of Consultative Process .……… 83 Appendix 4: Blueprint of Collaboration with other Research Institutes .……… 95 List of Box Items Box Item 1: Life and Vision of a Faith Healer .……… 21 Box Item 2: Microplanning for Conservation .……… 23 Box Item 3: Smuggling of Medicinal Plants by Yak Graziers .……… 31 Box Item 4: Hydel Power Model for Harnessing Herbal Power .……… 47 Box Item 5: Community Policing as a Conservation Tool .……… 53 Box Item 6: Dreams of a Traditional Health Practitioner .……… 59 Box Item 7: Action Plan to Revitalize -

Midweek: Beyond the Headlines

13 - 19 Sept, 2006 111 13 - 19 SEPT, 2006, GANGTOK [email protected] VOLUME 1 NO. 2. Rs. 10 GANGTOK: Given the hype and the COME SEPTEMBER 30 AND historic significance of the historic THE FIRST PHASE OF TRADE trading links with Tibet, expectations were high when Nathula finally opened OVER THE NATHULA WILL for trade on June 6. But three months CLOSE FOR THIS YEAR. THE later trading has not really taken place NATHULA in the scale that was planned. Trading INITIAL EUPHORIA in the first month itself witnessed SURROUNDING THE several impediments. The first hurdle was the Import-Export Code for RESUMPTION OF TRADE required for the traders. When the HAS GIVEN WAY TO A MORE trading began, the traders were then told REALISTIC ASSESSMENT. that they needed the IEC for international trade. And for that, one SARIKAH ATREYA REVIEWS had to furnish his Personal Account THE FIRST THREE MONTHS Number (PAN), which is not issued to the Sikkim residents as there are not OF TRADING AND LOOKS AT Central Direct Taxes extended in the THE LOOPHOLES AND State. With no IEC, trading was stalled. BOTTLENECKS THAT The Sikkim Chamber of Commerce approached both the Sikkim as well as CONTINUE TO DETER Photo: PEMA L. SHANGDERPA the Central Government on the issue of TRADE. IEC clearance and after much persuasion, the Centre decided to temporarily waive the IEC requirement for trade over Nathula, which took CONT’D ON Page 7 HYPE vs REALITY K Y M C DELIMITATION DRAMA PLAYS OUT Opposition harps on non reservation for Limboo-Tamangs by PEMA L. -

The State Bank of Sikkim (Acquisition of Shares) and Miscellaneous Provisions Act, 1982 Act No

THE STATE BANK OF SIKKIM (ACQUISITION OF SHARES) AND MISCELLANEOUS PROVISIONS ACT, 1982 ACT NO. 62 OF 1982 [6th November, 1982.] An Act to provide, in the public interest, for the acquisition of certain shares of the State Bank of Sikkim for the purpose of better consolidation and extension of banking facilities in the State of Sikkim and for matters connected therewith or incidental thereto. WHEREAS for the purpose of better consolidation and extension of banking facilities in the State of Sikkim, it is expedient to provide for a single apex banking institution in that State, and for that purpose to provide for the acquisition of certain shares of the State Bank of Sikkim and for matters connected therewith or incidental thereto; BE it enacted by Parliament in the Thirty-third Year of the Republic of India as follows:— CHAPTER I PRELIMINARY 1. Short title and commencement.—(1) This Act may be called the State Bank of Sikkim (Acquisition of Shares) and Miscellaneous Provisions Act, 1982. (2) It shall come into force on such date as the Central Government may, by notification in the Official Gazette, appoint. 2. Definitions.—In this Act, unless the context otherwise requires,— (a) “appointed day” means the date on which this Act comes into force; (b) “co-operative bank” means the Sikkim State Co-operative Bank Limited, a society registered under the Sikkim Co-operative Societies Act, 1978 (Sikkim Act No. 12 of 1978); (c) “notification” means a notification published in the Official Gazette; (d) “prescribed” means prescribed by rules made -

Booklet on Measurement of Digital Payments

BOOKLET ON MEASUREMENT OF DIGITAL PAYMENTS Trends, Issues and Challenges Revised and Updated as on 9thMay 2017 Foreword A Committee on Digital Payments was constituted by the Ministry of Finance, Department of Economic Affairs under my Chairmanship to inter-alia recommend measures of promotion of Digital Payments Ecosystem in the country. The committee submitted its final report to Hon’ble Finance Minister in December 2016. One of the key recommendations of this committee is related to the development of a metric for Digital Payments. As a follow-up to this recommendation I constituted a group of Stakeholders under my chairmanship to prepare a document on the measurement issues of Digital Payments. Based on the inputs received from RBI and Office of CAG, a booklet was prepared by the group on this subject which was presented to Secretary, MeitY and Secretary, Department of Economic Affairs in the review meeting on the aforesaid Committee’s report held on 11th April 2017 at Ministry of Finance. The review meeting was chaired by Secretary, Department of Economic Affairs. This booklet has now been revised and updated with inputs received from RBI and CAG. The revised and updated booklet inter-alia provides valuable information on the trends in Digital Payments in 2016-17. This has captured the impact of demonetization on the growth of Digital Payments across various segments. Shri, B.N. Satpathy, Senior Consultant, NISG, MeitY and Shri. Suneet Mohan, Young Professional, NITI Aayog have played a key role in assisting me in revising and updating this booklet. This updated booklet will provide policy makers with suitable inputs for appropriate intervention for promoting Digital Payments. -

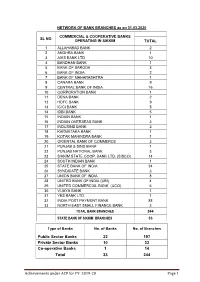

Achievements Under ACP for FY: 2019-20 Page 1 Public Sector Banks 22

NETWORK OF BANK BRANCHES as on 31.03.2020 COMMERCIAL & COOPERATIVE BANKS SL NO. OPERATING IN SIKKIM TOTAL 1 ALLAHABAD BANK 2 2 ANDHRA BANK 1 3 AXIS BANK LTD 10 4 BANDHAN BANK 1 5 BANK OF BARODA 3 6 BANK OF INDIA 2 7 BANK OF MAHARASHTRA 1 8 CANARA BANK 9 9 CENTRAL BANK OF INDIA 16 10 CORPORATION BANK 1 11 DENA BANK 2 12 HDFC BANK 9 13 ICICI BANK 5 14 IDBI BANK 5 15 INDIAN BANK 1 16 INDIAN OVERSEAS BANK 3 17 INDUSIND BANK 2 18 KARNATAKA BANK 1 19 KOTAK MAHINDRA BANK 1 20 ORIENTAL BANK OF COMMERCE 3 21 PUNJAB & SIND BANK 1 22 PUNJAB NATIONAL BANK 3 23 SIKKIM STATE COOP. BANK LTD. (SISCO) 14 24 SOUTH INDIAN BANK 1 25 STATE BANK OF INDIA 34 26 SYNDICATE BANK 3 27 UNION BANK OF INDIA 8 28 UNITED BANK OF INDIA (UBI) 4 29 UNITED COMMERCIAL BANK (UCO) 6 30 VIJAYA BANK 1 31 YES BANK LTD. 1 32 INDIA POST PAYMENT BANK 88 33 NORTH EAST SMALL FINANCE BANK 2 TOTAL BANK BRANCHES 244 STATE BANK OF SIKKIM BRANCHES 53 Type of Banks No. of Banks No. of Branches Public Sector Banks 22 197 Private Sector Banks 10 33 Co-operative Banks 1 14 Total 33 244 Achievements under ACP for FY: 2019-20 Page 1 DISTRICT-WISE BANK BRANCH as on 31.03.2020 NO. OF BRANCHES DISTRICT-WISE BANKS IN SIKKIM NORTH EAST SOUTH WEST TOTAL 1 ALLAHABAD BANK 0 2 0 0 2 2 ANDHRA BANK 0 1 0 0 1 3 AXIS BANK LTD 1 6 1 2 10 4 BANDHAN BANK 0 1 0 0 1 5 BANK OF BARODA 0 3 0 0 3 6 BANK OF INDIA 0 2 0 0 2 7 BANK OF MAHARASHTRA 0 1 0 0 1 8 CANARA BANK 1 5 2 1 9 9 CENTRAL BANK OF INDIA 1 8 1 6 16 10 CORPORATION BANK 0 1 0 0 1 11 DENA BANK 0 1 1 0 2 12 HDFC BANK LTD 0 6 3 0 9 13 ICICI BANK LTD 0 2 2 -

List of Bridges in Sikkim Under Roads & Bridges Department

LIST OF BRIDGES IN SIKKIM UNDER ROADS & BRIDGES DEPARTMENT Sl. Total Length of District Division Road Name Bridge Type No. Bridge (m) 1 East Singtam Approach road to Goshkan Dara 120.00 Cable Suspension 2 East Sub - Div -IV Gangtok-Bhusuk-Assam lingz 65.00 Cable Suspension 3 East Sub - Div -IV Gangtok-Bhusuk-Assam lingz 92.50 Major 4 East Pakyong Ranipool-Lallurning-Pakyong 33.00 Medium Span RC 5 East Pakyong Ranipool-Lallurning-Pakyong 19.00 Medium Span RC 6 East Pakyong Ranipool-Lallurning-Pakyong 26.00 Medium Span RC 7 East Pakyong Rongli-Delepchand 17.00 Medium Span RC 8 East Sub - Div -IV Gangtok-Bhusuk-Assam lingz 17.00 Medium Span RC 9 East Sub - Div -IV Penlong-tintek 16.00 Medium Span RC 10 East Sub - Div -IV Gangtok-Rumtek Sang 39.00 Medium Span RC 11 East Pakyong Ranipool-Lallurning-Pakyong 38.00 Medium Span STL 12 East Pakyong Assam Pakyong 32.00 Medium Span STL 13 East Pakyong Pakyong-Machung Rolep 24.00 Medium Span STL 14 East Pakyong Pakyong-Machung Rolep 32.00 Medium Span STL 15 East Pakyong Pakyong-Machung Rolep 31.50 Medium Span STL 16 East Pakyong Pakyong-Mamring-Tareythan 40.00 Medium Span STL 17 East Pakyong Rongli-Delepchand 9.00 Medium Span STL 18 East Singtam Duga-Pacheykhani 40.00 Medium Span STL 19 East Singtam Sangkhola-Sumin 42.00 Medium Span STL 20 East Sub - Div -IV Gangtok-Bhusuk-Assam lingz 29.00 Medium Span STL 21 East Sub - Div -IV Penlong-tintek 12.00 Medium Span STL 22 East Sub - Div -IV Penlong-tintek 18.00 Medium Span STL 23 East Sub - Div -IV Penlong-tintek 19.00 Medium Span STL 24 East Sub - Div -IV Penlong-tintek 25.00 Medium Span STL 25 East Sub - Div -IV Tintek-Dikchu 12.00 Medium Span STL 26 East Sub - Div -IV Tintek-Dikchu 19.00 Medium Span STL 27 East Sub - Div -IV Tintek-Dikchu 28.00 Medium Span STL 28 East Sub - Div -IV Gangtok-Rumtek Sang 25.00 Medium Span STL 29 East Sub - Div -IV Rumtek-Rey-Ranka 53.00 Medium Span STL Sl. -

Principal Secy (H&Fw) & Mission Director (Nhm)*

PRINCIPAL SECY (H&FW) & MISSION DIRECTOR (NHM)* Principal Secy Mission Directors Sl.No Name State/UT Name Contact Details of Pr.Secy Name Ph: Off, Mobile, Res, Email High- Focus Non-NE (10) Shri Anil kumar singhal Tele off : 0863-2445030 Shri Bhaskar Katamneni Tele Off : 0866-2410968,2410978 Principal Secretary (Medical H&FW) Mob : 8800923456 Commissioner (H&FW) & Mob : 9676697575 Department of (H&FW) E-Mail : [email protected], Mission Director (NHM) E-Mail : [email protected], Government of Andhra Pradesh Department of (H&FW) [email protected], 1 Andhra Pradesh Ground floor Building -5, Government of Andhra Pradesh AP secretariat , Velgapudi Guntur 5th Floor, APIIC Building, District, Andhra Pradesh-522238 Mangalagiri Guntur Distt., Andhra Pradesh-522002 Shri P. Parthiban Tele Off : 0360-2213329 Shri C. R. Khampa Tele Off : 0360-2350129 Secretary (H&FW) Mob : 8667318189 Mission Director (NHM) Fax No : 0360-2213329 Department of (H&FW) Email : [email protected], Department of (H&FW) Mob : 09436051148 1st Floor,Block 3, C- Sector , Naharlagun, Email : [email protected], 2 Arunachal Pradesh Civil Secretariat Itanagar, P/O Naharlagun, Itanagar Capital Region, Arunachal Pradesh - 791110 Arunachal Pradesh - 791111 Shri Anurag Goel Tele Off : 0361- 2237491 Dr. Lakshmanan. S Tele Off : 0361-2340239,2340236 Principal Secretary (H&FW) Moblie : 09435540400 Mission Director (NHM) Fax No : 0361-2349921,2340238 Department of (H&FW) Email : Office of Mission Director, Mob : 09435137819 Govt. of Assam, [email protected] (NHM) Saikia Commercial complex, Email : [email protected], 3 Assam C.M Block 3rd Floor m, Srinagar Path, christianbasti, Assam Secretariat, Dispur, [email protected], G.S.