BANK 2019-BNK16 Table of Contents

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

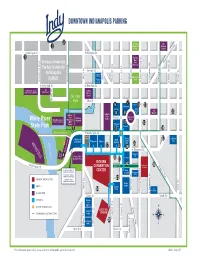

Parking Options in Indianapolis

DOWNTOWN INDIANAPOLIS PARKINGHOTELS & ATTRACTIONS S 2 Veterans Old 1 Memorial National Plaza Centre Blake Michigan St. Michigan St. 3 Indiana World Indiana University War Massachusetts Ave. Purdue University Memorial Vermont St. Indianapolis Courtyard by Marriott University West St. West Meridian St. Pennsylvania St. Delaware St. East St. Senate Ave. Capitol Ave. Illinois St. New Jersey St. Residence Park Alabama St. (IUPUI) Inn by University Blvd. Blackford St. Marriott New York St. New York St. IU Michael A. Carroll IU Indiana Track & Soccer Stadium Natatorium History Military Center Blake St. Park Ohio St. 7 Columbia Club 6 Sheraton 12 13 Hilton Hilton Central Canal Garden City 8 9 Inn Market 15 Indiana Indiana State State Market St. Monument Eiteljorg Capitol Circle White River NCAA Headquarters Museum & Museum & Hall of Champions IMAX 10 Theater Embassy 14 State Park Suites Conrad 5 11 16 Pedestrian Bridge Washington St. ? Parking Garage Circle LaQuinta JW Marriott Hyatt 27 Indianapolis Marriott Westin Centre Inn Indianapolis Zoo & White River Regency White River Gardens ? Mall 26 17 18 19 Maryland St. Visitors Center Hampton Inn The 4 Victory Field Le Méridien Lawn 20 Baseball Park 21 INDIANA 22 Washin Georgia St. Bankers Life 28 Virginia Ave. gton St. CONVENTION Fieldhouse Courtyard by Marriott CENTER Omni Downtown Indianapolis Severin Homewood Fairfield Inn & Suites Suites Downtown Indianapolis Jackson Place CONVENTION FACILITIES SpringHill Suites 23 Downtown Indianapolis Louisiana St. Union HOTELS Crowne Station West St. West The Plaza Meridian St. Delaware St. East St. 24 Pennsylvania St. Alexander ATTRACTIONS South St. South St. SKYWALKS Holiday Inn Express UNDERGROUND N ? VISITOR INFORMATION Madison Ave. -

Circle Tower 55 Monument Circle Indianapolis, in 46204

CIRCLE TOWER 55 MONUMENT CIRCLE INDIANAPOLIS, IN 46204 111,500 SF PROPERTY OVERVIEW Completed in 1930, Circle Tower overlooks downtown Indianapolis’ prestigious Monument Circle and is listed on the National Register of Historic Places. A prime example of Art Deco architecture, this unique building features a ziggurat crown, Art Deco sculptures, and bronze grilles with hieroglyphic images. Retail tenants include the likes of Starbucks, Potbelly, Soupremacy, Giorgios Pizza and Rocket Fizz. 3 | CIRCLE TOWER AVAILABLE SPACE • Second Floor - • Tenth Floor - — Suite 222 - 3,200 SF — Suite 1000 - 2,162 SF • Fourth Floor - — Suite 1014 - 1,997 SF — Suite 429 - 353 RSF — Suite 450 - 3,698 RSF 65 FORT WAYNE AVE. NORTH ST. PARKING OPTIONS NORTH ST. 1. Sheraton Hotel Garage 2. Salesforce Tower Garage MICHIGAN ST. 3. BMO Plaza Garage 4. Express Parking Garage 5. Huntington Parking Garage VERMONT ST. INDIANA AVE. UNIVERSITY BLVD. MASSACHUSETTS AVE. NEW YORK ST. BLACKFORD ST. COLLEGE AVE. OHIO ST. WEST ST. 1 2 3 EAST ST. PENNSYLVANIA ST. ALABAMA ST. ALABAMA CAPITOL AVE. DELAWARE ST. NEW JERSEY ST. MERIDIAN ST. SENATE AVE. SENATE ILLINOIS ST. ILLINOIS MONUMENT MARKET ST. CIRCLE MARKET ST. 4 5 65 WASHINGTON ST. WASHINGTON ST. CIRCLE CENTRE 70 MARYLAND ST. VIRGINIA AVE. WASHINGTON ST. CIRCLE BANKERS LIFE CENTRE FIELDHOUSE INDIANA GEORGIA ST. CONVENTION CENTER SOUTH ST. COLLEGE AVE. 300WEST ST. 200 30 10,300 RESTAURANTSMISSOURI ST. RETAIL OPTIONS HOTELS APARTMENT UNITS MADISON AVE. Sources: Downtown Indy Inc., JobsEQ, Visit Indy, Indy Chamber CIRCLE TOWER | 6 6 | CIRCLE TOWER MCCARTY ST. MCCARTY ST. KENTUCKY AVE. MERIDIAN ST. EAST ST. 70 65 MERIDIAN ST. -

5,849 SF of Restaurant Space Available in Downtown Indianapolis

5,849 SF of Restaurant Space Available in Downtown Indianapolis 6351 Crawfordsville Rd, Indianapo- 14 E Washington St, Indianapolis, IN 46204 Property Highlights: • Turn-Key Restaurant: Equipped with full bar, hoods, walk-in • 5,849 sq. ft. of restaurant space available coolers, two ADA restrooms, grease interceptor • Located in the heart of Indianapolis’ Central Business District • Exposed brick, high ceilings, original hard wood floors • Patio capabilities fronting the Cultural Trail FOR MORE INFORMATION Andrew Demaree John Holloway PLEASE CONTACT: T: 317-472-1800 T: 317-472-1800 E: [email protected] E: [email protected] 5,849 SF of Restaurant Space Available in Downtown Indianapolis 14 E Washington St, Indianapolis, IN 46204 14 E Washington St, Indianapolis, IN 46204 Main Level: Front Dining Area Main Level: Full Bar + Kitchen Lower Level: Temp-Controlled Wine Display Lower Level: Seating, Restrooms, & Private Dining FOR MORE INFORMATION Andrew Demaree John Holloway PLEASE CONTACT: T: 317-472-1800 T: 317-472-1800 E: [email protected] E: [email protected] 5,849 SF of Restaurant Space Available in Downtown Indianapolis 5,849 SF of Restaurant Space Available in Downtown Indianapolis 14 E Washington St, Indianapolis, IN 46204 6 Cultural trail - Mass Ave to (one way south) 28,710 Students Broad Ripple 2,800 Faculty (one way south) )ts a e y a w e n o( (one way south) 10 12 15 4 9 SITE 14 5 3 (one way west) (one way north) 2 1 1 9 6 7 )ts a e y a w e n o( (one way north) 3 13 2 • 276 Conventions Per Year • 2,058,701 Attendees Per Year 10 8 • $3.6B Spent by Convention Visitors 8 4 Former GM Plant Mixed Use Redevelopment Top Existing Hotels New Development Hotels Cultural trail - 1. -

Centre Offering Memorandum

Symphony Centre Confidential offering memorandum 32 East Washington Street, Indianapolis, Indiana Unique opportunity to acquire a historic building in the heart of downtown Indianapolis. 1 | Symphony Centre | 32 E. Washington St. Contents Investment summary 05 Property overview 06 Location overview 13 Market overview 21 Transaction guidelines 25 2 | Symphony Centre | 32 E. Washington St. JLL | 3 Investment summary Symphony Centre | 32 E. Washington St. The Offering JLL is pleased to offer for sale Symphony Centre (the “Property”), a 73,017 square foot building, located in the heart of a thriving downtown Indianapolis. The historic, 17-story building is situated along East Washington Street less than one block from Monument Circle and within walking distance of exceptional NORTH MERIDIAN STREET area amenities. With a timeless brick exterior, an exceptional window line and efficient floorplates, the Property boasts historic character with an eclectic feel that appeals to the modern tenant. INVESTMENT HIGHLIGHTS • Flexible zoning opportunity. CBD-1 zoning allows for flexible opportunities including retail, outdoor cafe or redevelopment opportunities. • Significant upside potential. With a recent remeasurement to BOMA square footage and expiring rents at approximately $3.00 below market, there is a significant upside potential by rolling expiring PENNSYLVANIA AVENUE leases to rental rates reflective of current market rates. • Appeal to today’s tenants. With a footprint reflective of the highest velocity of tenant demand, Symphony Centre offers everything today’s modern tenants want. The unique finishes, panoramic views and value-add potential for a rooftop patio add to the appeal. WASHINGTON STREET DELAWARE STREET • Healthy submarket and office market strength. Leasing activity in the CBD continues its uphill climb and represents 43% of the completed leases in Indianapolis MSA year to date. -

CENTRAL INDIANA CENTRAL INDIANA Montcalm Muskegon NORTH CENTRAL INDIANA

th annual 24COMMERCIAL REAL ESTATE MARKET STUDY 2016-2017 CENTRAL INDIANA CENTRAL INDIANA Montcalm Muskegon NORTH CENTRAL INDIANA Kent Ionia NORTHEAST INDIANA Ottawa NORTHWEST INDIANA Allegan Barry Eaton WEST MICHIGAN Van Buren Calhoun Kalamazoo Lake Michigan Cass St. Joseph Branch Berrien LaGrange Steuben St. Joseph Elkhart LaPorte Porter Noble DeKalb Lake Marshall Starke Kosciusko Whitley Allen Pulaski Fulton Newton Jasper Huntington Wabash White Cass Adams Wells Benton Miami Carroll Grant Blackford Howard Jay Warren Tippecanoe Clinton Tipton Delaware Madison Randolph Hamilton Fountain Montgomery Boone n Henry Wayne Marion Hancock Vermillio Parke Hendricks Putnam Rush Union Fayette Shelby Morgan Johnson Vigo Clay Franklin Owen Decatur Bartholomew Brown Monroe /company/bradley-company @bradley_company /bradleycompanyCRE @bradleycompany TABLE OF CONTENTS PRESIDENT’S LETTER RETAIL 02 13 INDUSTRIAL MULTI-HOUSING 05 17 OFFICE SERVICES & PROFESSIONALS 09 20 RESEARCH | ANALYSIS LAYOUT | DESIGN STEVEN HEATHERLY MICHELLE MOREY [email protected] [email protected] GAGE HUDAK JONATHAN KITCHENS [email protected] [email protected] LUCAS DEMEL KYLIE CURTIS [email protected] [email protected] PRESIDENT’S LETTER s a regional leader of commercial real estate services in the Midwest, we understand that critical market knowledge is foundational to the value we provide to our clients. AThis 24th Edition of our Market Study reflects the collective insights and experience of the growing team of skilled Bradley Company professionals. We first thank our sponsors, who are recognized in the back of this report, for helping deliver this 24th Edition that again provides in-depth analyses on the regions we serve throughout Indiana and Michigan. Within this report you will find market activity from several aspects of our business, which reflect the local, regional, and national economic landscape. -

Largest Indianapolis-Area Commercial Property Management

Largest Indianapolis-Area Commercial Property Management Firms (Ranked by gross leasable area managed locally (1)) LOCAL FTE: BROKERS / PERCENT: LOCAL PROPERTIES AGENTS PROPERTY RANK FIRM GLA MANAGED:(1) OFFICE MANAGED HEAD(S) OF LOCAL EMPLOYEES: OWNERSHIP: ESTAB. 2013 ADDRESS LOCALLY RETAIL LARGEST INDIANAPOLIS-AREA % OF SPACE OPERATIONS, TITLE(S) PROPERTY MGT. % INDIANA LOCALLY rank TELEPHONE / FAX / WEBSITE NATIONALLY INDUSTRIAL PROPERTIES MANAGED OWNED BY FIRM LOCAL DIRECTOR(S) TOTAL % OTHER HQ CITY Cassidy Turley 32.9 million 30 Keystone at the Crossing, 308 Jeffrey L. Henry, 29 24 1918 One American Square, Suite 1300, 46282 400.0 million 4 The Precedent Office Park, 0 regional managing principal 145 76 Washington, 1 (317) 634-6363 / fax (317) 639-0504 / cassidyturley.com 66 OneAmerica Tower Timothy J. Michel 209 D.C. 1 Duke Realty Corp. 27.5 million 22 AllPoints Midwest Bldg. 1, 164 Keith Konkoli, Charlie Podell, 9 94 1972 600 E. 96th St., Suite 100, 46240 15.3 million 0 AllPoints Midwest Bldg. 3, 91 SVPs; Jeff Stone, VP 18 6 Indianapolis 2 (317) 808-6000 / fax (317) 808-6650 / dukerealty.com 78 AllPoints at Anson Bldg. 1 Chris Yeakey, Ryan Rothacker 360 2 Cushman & Wakefield/Summit Realty Group (2) 10.2 million 20 BMO PLaza, 58 Matt Langfeldt, Brian Zurawski, DND DND 1993 241 N. Pennsylvania St, Suite 300, 46204 DND 1 ISTA Center, DND managing partners 23 DND Indianapolis 3 (317) 713-2100 / fax (317) 713-2103 / summitrealtygroup.com 79 One and Two Penn Mark Kenneth M. Petruska DND 3 Simon Property Group Inc. 7.0 million 1 Castleton Square, 13 David E. -

2Nd Generation Restaurant Opportunities in CBD Downtown Indy 6, 10 & 24 W

2nd Generation Restaurant Opportunities in CBD Downtown Indy 6, 10 & 24 W. Washington Street, Indianapolis, IN 46204 Overview Employee Aerial Hotel Aerial Parking Map Micro Aerial Columbia Club Market St apartmentsapartments 10,126 SF w/ 4,571 SF Finished 2,858 SF 2,177 SF Basement Delaware St Delaware FutureFuture 11 N.N. Future St Delaware Illinois St Illinois St Meridian Hotel Pacers Bike Share IndianapolisIndianapolis CulturalCultural TrailTrail IndianapolisIndianapolis CulturalCultural TrailTrail Pacers Bike Share Washington St 11,727 ADT IndianapolisIndianapolis CulturalCultural TrailTrail StationStation Meridian St 6,345 ADT Circle Centre Mall Meridian St 6,345 ADT Future Pennsylvania St Pennsylvania Pennsylvania St Pennsylvania Maryland St 11,926 ADT Property Highlights: • Three 2nd generation restaurant spaces available in CBD Downtown Indianapolis o 6 W. Washington Street = 2,177 SF former restaurant (no hood) 2020 DEMOGRAPHICS 1 miles 2 miles 3 miles o 10 W. Washington Street = 10,126 SF former restaurant with 4,571 SF finished basement o 24 W. Washington Street = 2,858.5 SF former restaurant Population 15,966 49,496 104,016 • Surrounded by hotels with new hotel projects under-construction or planned nearby, restaurants, Avg. HHI $88,453 $66,033 $54,305 and retail. Located across from Circle Centre mall Employees 99,956 164,981 191,072 • Located in the heart of downtown Indianapolis’ Central Business District with 99,956 employees within 1 mile. Floors 2-7 of the building above the retail opportunities are leased by Indiana Department of Health Median Age 31.9 33.1 29.9 with 650+ employees • Located one block south of Indianapolis’ Monument Circle which is a host to local, state and national events and gatherings • Excellent parking with 10 parking garage within two blocks of the site and metered street parking surrounding the site • Patio opportunities along Indianapolis Cultural Trail which is a large walking, running, biking trail that connects all of downtown from 10th Street to Fountain Square • Busiest Pacers Bike Share Station on Cultral Trail. -

DOWNTOWN Indianapolisworld HOTELS Indiana University War Massachusetts Ave

Schedule of Events JANUARY 9-11, 2020 Indiana Convention Center- Indianapolis, IN ATA Show Hours Exhibitor Set-Up 1.9.20 Thursday 8:30am-6:00pm *Buyer Day Exhibit Halls A-I 1.10.20 Friday 8:30am-6:00pm 1.7.20 Tuesday 8am-8pm 1.11.20 Saturday 8:30am-4:00pm 1.8.20 Wednesday 8am-8pm 1.9.20 Thursday 6:30am-8:30am Registration Hours Hoosier & Crossroads Lobby 1.10.20 Friday 6:30am-8:30am 1.7.20 Tuesday 7am-7pm 1.11.20 Saturday 6:30am-8:30am 1.8.20 Wednesday 7am-8pm Exhibitor Move Out 1.9.20 Thursday 7am-6pm Exhibit Halls A-I 1.11.20 Saturday 4pm-11pm 1.10.20 Friday 7am-6pm 1.12.20 Sunday 8am-4pm 1.11.20 Saturday 7am-1pm * Only those with a Retailer/Buyer Badge or Exhibitor Badge will have access to the Exhibit Hall on January 9. 1.7.20 TUESDAY 3:00pm-6:00pm A.R.R.O. Hot Show Exhibit Hall J 6:00pm-8:30pm A.R.R.O. Dealer Reception Rooms 233-235 1.8.20 WEDNESDAY 8:00am-8:00pm Featured Products Exhibitor Product Drop-Off Exhibit Hall F 8:00am-8:00pm Innovation Zone Exhibitor Setup Exhibit Hall H 9:00am-2:00pm A.R.R.O. Hot Show Exhibit Hall J 1:00pm-5:00pm NABA Super Show Wabash Ballroom 2:00pm-4:00pm A.R.R.O. Annual Member Meeting Exhibit Hall J 5:30pm-6:30pm International Welcome Reception Rooms 109-110 6:30pm Outtech Innovations XXII Sagamore Ballroom 1.9.20 THURSDAY 7:30am-6:00pm Press Room Open Room 141 8:30am-6:00pm ATA Show Hours *Buyer Day Exhibit Halls A-I 5:00pm-5:15pm $5,000 ATA and $1,000 Scentlok Cash Giveaway Drawing MyATA Exhibit Hall F 6:00pm-8:00pm Connections: An ATA Happy Hour Exhibit Hall J 1.10.20 FRIDAY 6:30am-8:30am Target -

Regions Tower

Regions Tower REGIONS TOWER PRIME DINING LOCATION A SOPHISTICATED DINING EXPERIENCE • 11,772 SF available on premier intersection of downtown Indianapolis • Upscale outdoor seating with enviable setback from street— along 2 sides of Regions Tower corner protected under elevated colonnade structure • Location offers 2 potential adjacent valet parking areas • Impressive upgrades to Regions Tower lobby • Great proximity to various downtown venues + experiences SCALE: NOT TO SCALE PROJECT MGR: EH DATE: 09.18.18 MARQUEE SPOT ANCHORED in the center of downtown activity FLOOR PLAN GROUND FLOOR • 11,772 SF available on premier intersection of downtown Indianapolis • Situated among cluster of Indy’s top-tier Class A office towers • Frontage along 2 primary pathways — N PENNSYLVANIA ST Pennsylvania + Ohio Streets — offering exceptional visibility OUTDOOR SEATING • Location provides great proximity to city’s GARAGE | VALET PARKING nearby entertainment experiences OUTDOOR SEATING E OHIO ST SCALE: NOT TO SCALE PROJECT MGR: EH DATE: 09.18.18 Salesforce Tower 4,712 2,841 300 N Meridian employees OneAmerica Tower 1,516 3,312 Monument City Ctr 313 Capital Center INDYGO RED LINE 2,429 101 W Ohio St 1,253 Market Tower Market Square Ctr 2,161 BMO Plaza 1,234 1,693 City-County Bldg 3,656 Cummins HQ PENNSYLVANIA ST 30 South PNC Center 1,407 2,626 Simon Property HQ 1,575 ACCESSIBILITY PRIME DEVELOPMENT ZONE with 24/7 exposure to downtown professionals and residents FLOOR PLAN IDEAL LOCATION GROUND FLOOR TOP TIER PROJECTS NEARBY 1 N PENNSYLVANIA HOTEL INDY PULLIAM -

Downtown Indianapolis Hotels & Attractions

DOWNTOWNDOWNTOWN INDIANAPOLISINDIANAPOLIS PARKINGHOTELS & ATTRACTIONS Veterans Old 2 Memorial National 1 Plaza Centre Blake Michigan St. Michigan St. Indiana 3 World Indiana University War Massachusetts Ave. Purdue University Memorial Vermont St. Indianapolis Courtyard by Marriott University West St. West Meridian St. Pennsylvania St. Delaware St. Senate Ave. Capitol Ave. Illinois St. East St. Alabama St. Residence Park New Jersey St. (IUPUI) Inn by University Blvd. Blackford St. Marriott New York St. New York St. IU Michael A. Carroll IU Indiana Track & Soccer Stadium Natatorium History Military Center Blake St. Park Ohio St. 7 Columbia Club 6 Sheraton 12 13 Hilton Hilton Central Canal Garden City 9 Inn Market 15 Indiana Indiana 8 State State Market St. Monument Eiteljorg Capitol Circle White River NCAA Headquarters Museum & Museum & Hall of Champions IMAX 10 Theater Embassy 14 State Park Suites 5 11 Conrad 16 Pedestrian Bridge Washington St. ? Indianapolis Zoo & Circle LaQuinta White River Gardens Hyatt 27 Marriott Place Marriott Westin Centre Inn White River ? Indianapolis Regency Mall 26 17 18 19 Maryland St. Visitors Center Hampton 4 Inn The Victory Field 20 Lawn Canterbury Baseball Park INDIANA 21 W CONVENTION 22 28 ashingt Georgia St. Bankers Life Virginia on St. CENTER Fieldhouse JW Marriott Downtown Omni Indianapolis Severin Homewood Suites A Courtyard by Marriott ve. Downtown Indianapolis 23 Jackson Place Fairfield Inn & Suites CONVENTION FACILITIES Downtown Indianapolis Louisiana St. SpringHill Suites Union Downtown Indianapolis Crowne Station West St. West 24 The Plaza Meridian St. Delaware St. East St. HOTELS Pennsylvania St. Alexander South St. South St. ATTRACTIONS Holiday Inn SKYWALKS Express N Madison Ave. -

THE LOCKERBIE MARKETPLACE 333 North Alabama Street @ New York Street & Historic Mass Ave Cultural District

THE LOCKERBIE MARKETPLACE 333 North Alabama Street @ New York Street & Historic Mass Ave Cultural District INDIANAPOLIS, INDIANA >>> PRIME CORNER RETAIL SPACE | 42,000 SF Available GERSHMAN Gershman Partners | 350 Massachusetts Avenue, Suite 400, Indianapolis, IN 46204 | 317.599.4800 | Eric Gershman | [email protected] LOCKERBIE MARKETPLACE >>> FACTS 333 North Alabama Street @ New York Street & Historic Mass Ave. District SIZE ::: 42,000 sf available TRAFFIC COUNT ::: PARKING ::: 477 paved spaces BUILDING ::: 180,000 sf | mixed-use | 3 stories POPULATION ::: 22,000 within vacinity NEIGHBORHOOD ::: Historic Mass Ave | est. 1929 LOCATION ::: tri-intersection of Alabama Street @ E New Jersey Street & Massachusetts Avenue <<< Current Marketplace Tenants GERSHMAN Gershman Partners | 350 Massachusetts Avenue, Suite 400, Indianapolis, IN 46204 | 317.599.4800 | Eric Gershman | [email protected] Historic Mass Ave Cultural District 333 North Alabama Street @ New York Street & Historic Mass>>> Ave. District DOWNTOWN INDIANAPOLIS Salesforce Tower INDIANAPOLIS, INDIANA >>> 3900 employees Regions Tower >>> 82% occupied >>> 2106 employees >>> 72% occupied OneAmerica Tower >>> 2661 employees BMO Plaza >>> 85% occupied >>> 1436 employees Market Tower Market Square Center >>> 74% occupied >>> 1621 employees >>> 1009 employees >>> 72% occupied >>> 57% occupied 35,000 Students 300 North Meridian >>> 1302 employees >>> 86% occupied Bazbeaux The Tap Ball & Biscuit MacNiven’s The Eagle Bakersfield Marott Center GardenTable 40,000 sq.ft. of office Coming Soon: 2017 The Marietta Hedge Row Old Point Tavern 30,000 sq.ft. of office Lockerbie Marketplace Bru Burger Bar >>> 180,000 sq.ft. of Office & Retail Space | 42,000 corner storefront available Chatterbox Jazz GERSHMAN Gershman Partners | 350 Massachusetts Avenue, Suite 400, Indianapolis, IN 46204 | 317.599.4800 | Eric Gershman | [email protected] Class-A Multi-Family Developments 333 North Alabama Street @ New York Street & Historic Mass>>> Ave. -

Exhibitor Important Dates

EXHIBITOR IMPORTANT DATES September 1 Final booth payments and insurance liability certificate due to ATA September 1 Signed shooting lane contracts due to ATA for exhibitors who have reserved shooting lanes November 1 Deadline to reserve space in the Goodie Bags and Big Buck Tag Coupon Book November 10 Deadline to reserve advertising space in the Official ATA Trade Show Pocket Guide November 17 Ad materials due to Zebra Publishing for the Official ATA Trade Show Pocket Guide November 21 Deadline to update your company information for the Official Show Guide & Membership Directory November 30 Deadline to submit special booth events registration form for inclusion in the Official Show Guide & Membership Directory December 1 Goodie Bag materials/inserts due to ATA December 5 Deadline to reserve advertising space in Official Show Guide & Membership Directory December 11 Ad materials due to Zebra Publishing for the Official Show Guide & Membership Directory December 11 Deadline to order lead retrieval services from QMS at the Advanced Rate December 14 First day show freight can arrive at advance warehouse without a surcharge December 13 Deadline to preregister for Featured Products Showcase to guarantee space December 15 Premium Sponsorship Material (banners, wraps, clings, etc) due to advance warehouse December 21 Deadline to order decorating services from Shepard at the discounted Advance Order Rate December 22 Deadline to order audio visual and computer equipment at Advanced Rate December 26 Deadline to make hotel reservations through