CHAPTER 4: Economic Profile and Development

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

LAGUNA LAKE DEVELOPMENT AUTHORITY National Ecology Center, East Avenue, Diliman, Quezon City Phone Nos

LAGUNA LAKE DEVELOPMENT AUTHORITY National Ecology Center, East Avenue, Diliman, Quezon City Phone Nos. (02) 8 376-4039, (02) 8 376-4072, (02) 8 376-4044, (02) 8 332-2353, (02) 8 332-2341, (02) 8 376-5430 Locals 115, 116, 117 and look for Ms. Julie Ann G. Blanquisco or Ms. Marivic A. Dela Torre-Santos E-mail: [email protected] | [email protected] Website: http://llda.gov.ph List of APPROVED DISCHARGE PERMITS as of September 03, 2021 Establishment Address Permit No. Approve Date 11 FTC Enterprises, Inc. 236 P. Dela Cruz San Bartolome Quezon City MM DP-25b-2021-03532 August 18, 2021 189 Realty Corp. (CI Market) Qurino Highway Santa Monica, Novaliches Quezon City MM DP-25b-2021-03744 August 20, 2021 189 Realty Corporation - 2nd (CI Market/Commercial Complex) Quirino Highway, Sta. Monica Novaliches Quezon City MM DP-25b-2021-03743 August 20, 2021 21st Century Mouldings Corporation 18 F. Carlos St. cor. Howmart Road Apolonio Samson Quezon City MM DP-25b-2021-03541 August 23, 2021 24K Property Ventures, Inc. (20 Lansbergh Place Condominium) 170 T. Morato Ave. cor. Sct. Castor Sacred Heart Quezon City MM DP-25b-2021-02819 July 15, 2021 3J Foods Corp. Sta. Ana San Pablo City Laguna DP-16d-2021-03174 August 06, 2021 8 Gilmore Place Condominium 8 Gilmore Ave. cor. 1st St. Valencia New Manila Quezon City MM DP-25b-2021-03829 August 27, 2021 AC Technical Services, Inc. 5 RMT Ind`l. Complex Tunasan Muntinlupa City MM DP-23a-2021-01804 May 12, 2021 Ace Roller Manufacturing, Inc. -

Climate Disasters in the Philippines: a Case Study of the Immediate Causes and Root Drivers From

Zhzh ENVIRONMENT & NATURAL RESOURCES PROGRAM Climate Disasters in the Philippines: A Case Study of Immediate Causes and Root Drivers from Cagayan de Oro, Mindanao and Tropical Storm Sendong/Washi Benjamin Franta Hilly Ann Roa-Quiaoit Dexter Lo Gemma Narisma REPORT NOVEMBER 2016 Environment & Natural Resources Program Belfer Center for Science and International Affairs Harvard Kennedy School 79 JFK Street Cambridge, MA 02138 www.belfercenter.org/ENRP The authors of this report invites use of this information for educational purposes, requiring only that the reproduced material clearly cite the full source: Franta, Benjamin, et al, “Climate disasters in the Philippines: A case study of immediate causes and root drivers from Cagayan de Oro, Mindanao and Tropical Storm Sendong/Washi.” Belfer Center for Science and International Affairs, Cambridge, Mass: Harvard University, November 2016. Statements and views expressed in this report are solely those of the authors and do not imply endorsement by Harvard University, the Harvard Kennedy School, or the Belfer Center for Science and International Affairs. Design & Layout by Andrew Facini Cover photo: A destroyed church in Samar, Philippines, in the months following Typhoon Yolanda/ Haiyan. (Benjamin Franta) Copyright 2016, President and Fellows of Harvard College Printed in the United States of America ENVIRONMENT & NATURAL RESOURCES PROGRAM Climate Disasters in the Philippines: A Case Study of Immediate Causes and Root Drivers from Cagayan de Oro, Mindanao and Tropical Storm Sendong/Washi Benjamin Franta Hilly Ann Roa-Quiaoit Dexter Lo Gemma Narisma REPORT NOVEMBER 2016 The Environment and Natural Resources Program (ENRP) The Environment and Natural Resources Program at the Belfer Center for Science and International Affairs is at the center of the Harvard Kennedy School’s research and outreach on public policy that affects global environment quality and natural resource management. -

History of Quezon City Public Library

HISTORY OF QUEZON CITY PUBLIC LIBRARY The Quezon City Public Library started as a small unit, a joint venture of the National Library and Quezon City government during the incumbency of the late Mayor Ponciano Bernardo and the first City Superintendent of Libraries, Atty. Felicidad Peralta by virtue of Public Law No. 1935 which provided for the “consolidation of all libraries belonging to any branch of the Philippine Government for the creation of the Philippine Library”, and for the maintenance of the same. Mayor Ponciano Bernardo 1946-1949 June 19, 1949, Republic Act No. 411 otherwise known as the Municipal Libraries Law, authored by then Senator Geronimo T. Pecson, which is an act to “provide for the establishment, operation and Maintenance of Municipal Libraries throughout the Philippines” was approved. Mrs. Felicidad A. Peralta 1948-1978 First City Librarian Side by side with the physical and economic development of Quezon City officials particularly the late Mayor Bernardo envisioned the needs of the people. Realizing that the achievements of the goals of a democratic society depends greatly on enlightened and educated citizenry, the Quezon City Public Library, was formally organized and was inaugurated on August 16, 1948, with Aurora Quezon, as a guest of Honor and who cut the ceremonial ribbon. The Library started with 4, 000 volumes of books donated by the National Library, with only four employees to serve the public. The library was housed next to the Post Office in a one-storey building near of the old City Hall in Edsa. Even at the start, this unit depended on the civic spirited members of the community who donated books, bookshelves and other reading material. -

Title <Book Reviews>Lisandro E. Claudio. Taming People's Power: the EDSA Revolutions and Their Contradictions. Quezon City

View metadata, citation and similar papers at core.ac.uk brought to you by CORE provided by Kyoto University Research Information Repository <Book Reviews>Lisandro E. Claudio. Taming People's Power: Title The EDSA Revolutions and Their Contradictions. Quezon City: Ateneo de Manila University Press, 2013, 240p. Author(s) Thompson, Mark R. Citation Southeast Asian Studies (2015), 4(3): 611-613 Issue Date 2015-12 URL http://hdl.handle.net/2433/203088 Right ©Center for Southeast Asian Studies, Kyoto University Type Journal Article Textversion publisher Kyoto University Book Reviews 611 correct, and was to prove the undoing of the Yingluck government. Nick Nostitz’s chapter on the redshirt movement provides a useful summary of his views, though there are few surprises for those who follow his regular online commentary pieces on these issues. Andrew Walker’s article “Is Peasant Politics in Thailand Civil?” answers its own question in his second sentence: “No.” He goes on to provide a helpful sketch of the arguments he has made at greater length in his important 2012 book Thailand’s Political Peasants. The book concludes with two chapters ostensibly focused on crises of legitimacy. In his discussion of the bloody Southern border conflict, Marc Askew fails to engage with the arguments of those who see the decade-long violence as a legitimacy crisis for the Thai state, and omits to state his own position on this central debate. He rightly concludes that “the South is still an inse- cure place” (p. 246), but neglects to explain exactly why. Pavin Chachavalpongpun offers a final chapter on Thai-Cambodia relations, but does not add a great deal to his brilliant earlier essay on Preah Vihear as “Temple of Doom,” which remains the seminal account of that tragi-comic inter- state conflict. -

Registered Pawnshops & Msbs

LIST OF MONEY SERVICE BUSINESSES REGISTERED WITH THE AMLC AS OF SEPTEMBER 2020 INST CODE NAME OF MONEY SERVICE BUSINESSES 1 060000176 'ASMA MONEY CHANGER 2 060000233 0209 ROYAL STONES, INC. 3 060000234 101 FASTPAY, INC. 4 060000132 19TH MONEY CHANGER 5 060000587 5 SISTERS FOREIGN CURRENCY EXCHANGE CORP. 6 060000758 88 ARKADE INCORPORATED 7 060000743 8A8 MONEY CHANGER 8 060000825 A & V REMITTANCE CENTER 9 060000213 A STAR MONEY REMITTANCE 10 060000056 A.L. MONEY CHANGER 11 060000137 A.R.T. MONEY CHANGER 12 060000204 A.X. CURRENCY EXCHANGE 13 060000123 AAA MONEY CHANGER, REMITTANCE AND BILLS PAYMENT 14 060000777 ABA GLOBAL PHILIPPINES INC. 15 060000019 ABBA CURRENCY EXCHANGE, INC. 16 060000091 ABELEN'S MUSIC STORE AND GENERAL MERCHANDES 17 060000284 ABIGENCOUR CORP. 18 060000100 ACCE EASY REMIT & SERVICES 19 060000396 ACHIEVERS MONEY CHANGER 20 060000805 ACTION.ABLE INC. 21 060000515 ACURREX ENTERPRISE 22 060000429 ACYAO AND ACGALVEZ CURRENCY EXCHANGE INC. 23 060000386 ADA SINGAPORE 1 GIFTSHOP AND MONEYCHANGER ADVENTURE INTERNATIONAL TOURS, INC. DOING BUSINESS UNDER THE NAME AND 24 060000662 STYLE OF AMERICAN EXPRESS TRANSNATIONAL 25 060000659 AG & G MONEY EXCHANGE 26 060000784 AGOO MONEY CHANGER 27 060000620 AGPC MONEY CHANGER 28 060000510 AGUINALDO NETWORK INTERNATIONAL INC. 29 060000071 AIAH FOREIGN EXCHANGE DEALER 30 060000746 AIDA MONEY CHANGER 31 530013 AIRPAY TECHNOLOGIES PHILIPPINES INC Page 1 of 24 LIST OF MONEY SERVICE BUSINESSES REGISTERED WITH THE AMLC AS OF SEPTEMBER 2020 INST CODE NAME OF MONEY SERVICE BUSINESSES 32 060000329 AIRPORTVILLE CURRENCY TRADING 33 060000129 AKONG MONEY CHANGER 34 060000054 ALAINA JEM TRAVEL SERVICES 35 060000377 ALCHOR FOREX-MONEY CHANGER 36 060000796 ALCO AND LEE FOREIGN EXCHANGE, INC. -

Company Name: Ayala Land Malls Inc. Corporate Address: 5Th Floor, Glorietta 4, Ayala Center Makati City

Company Name: Ayala Land Malls Inc. Corporate Address: 5th Floor, Glorietta 4, Ayala Center Makati City Mall List Luzon Mall Name Mall Location Harbor Point Subic Bay Freeport Zone, Zambales MarQuee Mall Angeles City, Pamapanga Ayala Malls Cloverleaf A Bonifacio Ave Brgy Balingasa, Quezon City TriNoma Edsa Corner North Avenue, Quezon City Ayala Malls Vertis North North Avenue Brgy Bagong Pag-asa, Quezon City Fairview Terraces Quirino Highway cor Maligaya Drive Novaliches, Quezon City U.P. Town Center Katipunan Avenue Diliman, Quezon City Ayala Malls Feliz Amang Rodriguez Cor J.P. Rizal Brgy Dela Paz, Pasig City Ayala Malls Marikina Liwasag Kalayaan Brgy Marikina Heights, Marikina City Ayala Malls The 30th Meralco Ave. Brgy Ugong, Pasig City Market! Market! Bonifacio Global City, Taguig One Ayala Ave Ayala Avenue, Makati City Glorietta Ayala Center, Makati City Greenbelt Legazpi Street, Makati City Ayala Malls Circuit Circuit Makati, Hippodromo, Carmona, Makati City Ayala Malls Manila Bay Macapagal Blvd cor. Aseana Avenue, Paranaque City Alabang Town Center Alabang Town Center, Muntinlupa City The District Dasma Molina Road, Dasmarinas, Cavite The District Imus Aguinaldo Highway cor. Daang Hari Road Anabu II-D, Imus, Cavite Vermosa Daang Hari Road cor. Vermosa Blvd., Imus, Cavite Ayala Malls Solenad Nuvali, Brgy. Sto. Domingo, City of Santa Rosa, Laguna Ayala Malls Serin Gen. Emilio Aguinaldo Highway Tagaytay City, Cavite Ayala Malls Legazpi Rizal Street corner Quezon Ave., Barangay Capantawan, Legazpi City, Albay Mall List VisMin Mall Name Mall Location Abreeza J.P. Laurel Ave., Davao City Ayala Center Cebu Cebu Business Park, Cebu City Central Bloc I. Villa Street Cebu IT Park, Cebu City Centrio Mall CM Recto-Corrales Ave, Cagayan de Oro Ayala Malls Capitol Central Gatuslao Street, Bacolod City . -

Naval Reserve Command

NAVAL RESERVE OFFICER TRAINING CORPS Military Science –1 (MS-1) COURSE ORIENTATION Training Regulation A. Introduction: The conduct of this training program is embodied under the provisions of RA 9163 and RA 7077 and the following regulations shall be implemented to all students enrolled in the Military Science Training to produce quality enlisted and officer reservists for the AFP Reserve Force. B. Attendance: 1. A minimum attendance of nine (9) training days or eighty percent (80%) of the total number of ROTC training days per semester shall be required to pass the course. 2. Absence from instructions maybe excuse for sickness, injury or other exceptional circumstances. 3. A cadet/ cadette (basic/advance) who incurs an unexcused absence of more than three (3) training days or twenty percent (20%) of the total number of training during the semester shall no longer be made to continue the course during the school year. 4. Three (3) consecutive absences will automatically drop the student from the course. C. Grading: 1. The school year which is divided into two (2) semesters must conform to the school calendar as practicable. 2. Cadets/ cadettes shall be given a final grade for every semester, such grade to be computed based on the following weights: a. Attendance - - - - - - - - - - 30 points b. Military Aptitude - - - - - 30 points c. Subject Proficiency - - - - 40 points 3. Subject proficiency is forty percent (40%) apportioned to the different subjects of a course depending on the relative importance of the subject and the number of hours devoted to it. It is the sum of the weighted grades of all subjects. -

1 Introduction

Formulation of an Integrated River Basin Management and Development Master Plan for Marikina River Basin VOLUME 1: EXECUTIVE SUMMARY 1 INTRODUCTION The Philippines, through RBCO-DENR had defined 20 major river basins spread all over the country. These basins are defined as major because of their importance, serving as lifeblood and driver of the economy of communities inside and outside the basins. One of these river basins is the Marikina River Basin (Figure 1). Figure 1 Marikina River Basin Map 1 | P a g e Formulation of an Integrated River Basin Management and Development Master Plan for Marikina River Basin VOLUME 1: EXECUTIVE SUMMARY Marikina River Basin is currently not in its best of condition. Just like other river basins of the Philippines, MRB is faced with problems. These include: a) rapid urban development and rapid increase in population and the consequent excessive and indiscriminate discharge of pollutants and wastes which are; b) Improper land use management and increase in conflicts over land uses and allocation; c) Rapidly depleting water resources and consequent conflicts over water use and allocation; and e) lack of capacity and resources of stakeholders and responsible organizations to pursue appropriate developmental solutions. The consequence of the confluence of the above problems is the decline in the ability of the river basin to provide the goods and services it should ideally provide if it were in desirable state or condition. This is further specifically manifested in its lack of ability to provide the service of preventing or reducing floods in the lower catchments of the basin. There is rising trend in occurrence of floods, water pollution and water induced disasters within and in the lower catchments of the basin. -

PHILIPPINES Manila GLT Site Profile

PHILIPPINES Manila GLT Site Profile AZUSA PACIFIC UNIVERSITY GLOBAL LEARNING TERM 626.857.2753 | www.apu.edu/glt 1 TABLE OF CONTENTS INTRODUCTION TO MANILA ................................................... 3 GENERAL INFORMATION ........................................................ 5 CLIMATE AND GEOGRAPHY .................................................... 5 DIET ............................................................................................ 5 MONEY ........................................................................................ 6 TRANSPORTATION ................................................................... 7 GETTING THERE ....................................................................... 7 VISA ............................................................................................. 8 IMMUNIZATIONS ...................................................................... 9 LANGUAGE LEARNING ............................................................. 9 HOST FAMILY .......................................................................... 10 EXCURSIONS ............................................................................ 10 VISITORS .................................................................................. 10 ACCOMODATIONS ................................................................... 11 SITE FACILITATOR- GLT PHILIPPINES ................................ 11 RESOURCES ............................................................................... 13 NOTE: Information is subject to -

COVID-19 Government Hotlines

COVID-19 Advisory COVID-19-Related Government Hotlines Department of Health (DOH) 02-894-COVID (02-894-26843); 1555 (PLDT, Smart, Sun, and TNT Subscribers) Philippine Red Cross Hotline 1158 Metro Manila Emergency COVID-19 Hotlines Caloocan City 5310-6972 / 0947-883-4430 Manila 8527-5174 / 0961-062-7013 Malabon City 0917-986-3823 Makati City 168 / 8870-1959-59 Navotas City 8281-1111 Mandaluyong City 0916-255-8130 / 0961-571-6959 Valenzuela City 8352-5000 / 8292-1405 San Juan City 8655-8683 / 7949-8359 Pasig City 8643-0000 Muntinlupa City 0977-240-5218 / 0977-240-5217 Municipality of Pateros 8642-5159 Paranaque City 8820-7783 Marikina City 161 / 0945-517-6926 Las Pinas City 8994-5782 / 0977-672-6211 Taguig City 0966-419-4510 / 8628-3449 Pasay City 0956-7786253 / 0908-9937024 Quezon City 122 Research Institute for Tropical Medicine (RITM) (+632) 8807-2631 Department of the Interior and Local (+632) 8876-3444 local 8806 ; Government (DILG) Emergency 8810 to monitor the implementation of directives and Operations Center Hotline measures against COVID-19 in LGUs Department of Trade and Industry 0926-612-6728 (Text/Viber) DTI Officer of the Day COVID Rapid Response Team deployed in NDRRMC Camp Aguinaldo Other Government Hotlines Bangko Sentral ng Pilipinas (BSP) (+632) 8708.77.01 Email: [email protected] Credit Information Corporation (CIC) Email: [email protected] Social Security System (SSS) Trunkline: (+632) 8920-6401 Call Center: (+632) 8920-6446 to 55 IVRS: (+632) 7917-7777 Toll Free: 1-800-10-2255777 Email: [email protected] -

Bonchon Store List

Bonchon Store List RCBC Bankard-JCB Spend Anywhere Store Name Store Address SM MEGAMALL Unit 159-A, Bldg. A, Upper Ground Floor, SM Megamall, Mandaluyong City ROBINSONS GALLERIA Ground Floor, Food Court, Robinsons Galleria, Ortigas, Pasig City GREENHILLS PROMENADE Unit FC 4, Lower Level, Greenhills Promenade, GSC, Ortigas Avenue, San Juan City KATIPUNAN 2F Regis Center, 327 Katipunan Avenue, Quezon City SHANGRI-LA PLAZA Unit 48 Lower Ground Floor Level, Shangrila Plaza Mall, Edsa Shaw Boulevard, Mandaluyong City UNIVERSITY MALL TAFT Ground Floor University Mall, 2507 Taft Avenue, Malate, Manila TOMAS MORATO 2nd Floor Il Terrazo, Tomas Morato corner Scout Madrinan, Quezon City TRINOMA Level 1 Trinoma, Quezon City SM MALL OF ASIA G/F Space 100-101, SM Mall of Asia, Diokno Boulevard, Pasay City ALABANG TOWN CENTER Space 1011 Lower Ground Floor, New Wing, The Garden, Alabang Town Center, Alabang, Muntinlupa City GREENBELT Ground Floor, Greenbelt 1, Ayala Center, Paseo de Roxas, Brgy. San Lorenzo, Makati City AYALA TRIANGLE GARDEN Ground Floor Space 4, Ayala Triangle Gardens, Paseo de Roxas corner Makati Avenue, Makati Cty LUCKY CHINATOWN 3rd Floor Lucky Chinatown Mall, Reina Regente corner Dela Reina Sts., Brgy. 293, Zone 28, Binondo, Manila SM TAYTAY GF Building A, SM City Taytay, Manila East Road, Brgy. Dolores, Taytay, Rizal SM NORTH EDSA ANNEX 3/F SM North Edsa, The Annex, Quezon City HIGH STREET THE FORT Ground Level, 7th Avenue corner 28th St., One Parkade Building, Bonifacio High Street, Taguig City SM FAIRVIEW 2/F Main Building, Quirino Avenue corner Regalado St., Greater Lagro, Quezon City SM MANILA 4/F Unit 418, SM Manila, Concepcion corner Arroceros and San Marcelino Streets, Manila ROBINSONS MANILA 4/F Center Atrium, Robinsons Place Ermita, Manila EASTWOOD Unit H2A, Eastwood City Walk 1, Eastwood City, Libis, Quezon City SM DAVAO G/F The Annex, SM City Davao, Quimpo Blvd., Tulip Drive, Ecoland Subdivision Matina, Davao City UP TECHNOHUB 2/F Space No. -

REAL.ESTATE Cpdprogram.Pdf

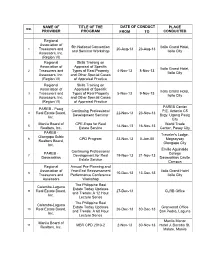

NAME OF TITLE OF THE DATE OF CONDUCT PLACE NO. PROVIDER PROGRAM FROM TO CONDUCTED Regional Association of 5th National Convention Iloilo Grand Hotel, 1 Treasurers and 20-Aug-13 23-Aug-13 and Seminar Workshop Iloilo City Assessors, Inc. (Region VI) Regional Skills Training on Association of Appraisal of Specific Iloilo Grand Hotel, 2 Treasurers and Types of Real Property 4-Nov-13 8-Nov-13 Iloilo City Assessors, Inc. and Other Special Cases (Region VI) of Appraisal Practice Regional Skills Training on Association of Appraisal of Specific Iloilo Grand Hotel, 3 Treasurers and Types of Real Property 5-Nov-13 9-Nov-13 Iloilo City Assessors, Inc. and Other Special Cases (Region VI) of Appraisal Practice PAREB Center PAREB - Pasig Continuing Professional P.E. Antonio C5 4 Real Estate Board, 22-Nov-13 23-Nov-13 Development Seminar Brgy. Ugong Pasig Inc. City Manila Board of CPE-Expo for Real World Trade 5 14-Nov-13 16-Nov-13 Realtors, Inc. Estate Service Center, Pasay City PAREB - Traveler's Lodge, Olongapo Subic 6 CPD Program 23-Nov-13 0-Jan-00 Magsaysay Realtors Board, Olongapo City Inc. Emilio Aguinaldo Continuing Professional PAREB - College 7 Development for Real 19-Nov-13 21-Nov-13 Dasmariñas Dasmariñas Cavite Estate Service Campus Regional Annual Pre-Planning and Association of Year-End Reassessment Iloilo Grand Hotel 8 10-Dec-13 13-Dec-13 Treasurers and Performance Conference Iloilo City Assessors Workshop The Philippine Real Calamba-Laguna Estate Today Updates 9 Real Estate Board, 27-Dec-13 CLRB Office and Trends: A 12 Hour Inc.