The Birr Castle Retreat And

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Killeen Castle and Estate Being Turned Into Major Hotel and Golf Resort Consulting Engineers: Barrett Mahony, Dublin

ACEI_07-p69-110 3/1/07 10:22 AM Page 91 ACEI Killeen Castle and estate being turned into major hotel and golf resort Consulting engineers: Barrett Mahony, Dublin Killeen Castle, an historic residence in Co Meath, long derelict, is being totally restored in a long term project that will see the castle form the basis of a five star luxury hotel, the creation of a top class 18 hole golf course and the building of 179 luxury houses. Already, the resort has been selected as the venue in 2011 of the Solheim Cup, when the best female golfers in Europe will compete against their opposite numbers from the US. It’s a biennial competition that is the female equivalent of the Ryder Cup. For the Killeen Castle project, it’s a huge vote of confidence, before the project is even finished.When this com- petition was held in Sweden in 2003, it attracted over 100,000 spectators, so when the Solheim Cup competition comes to Killeen Castle, it is likely to prove just as popular draw for visitors as the Ryder Cup was at the K Club in September, 2006. The Killeen demesne was the ancestral home of the Plunkett family for close on 600 years; St Oliver Plunkett was a member of this distinguished family. The demesne of Killeen was created in 1181 by explaining why even today, the Killeen estate is much Hugh de Lacy. Sir Christopher Plunkett, deputy Lord larger than its next door neighbour. Lieutenant of Ireland, was created the Baron of Killeen in the early 15th century; he had married the The original Norman keep at Killeen was built in the daughter of Sir Lucas Cusack in 1403, thereby bring- 12th century and subsequently, various extensions ing the demesnes of both Killeen and neighbouring were built before it fell into ruin. -

Copyrighted Material

18_121726-bindex.qxp 4/17/09 2:59 PM Page 486 Index See also Accommodations and Restaurant indexes, below. GENERAL INDEX Ardnagashel Estate, 171 Bank of Ireland The Ards Peninsula, 420 Dublin, 48–49 Abbey (Dublin), 74 Arigna Mining Experience, Galway, 271 Abbeyfield Equestrian and 305–306 Bantry, 227–229 Outdoor Activity Centre Armagh City, 391–394 Bantry House and Garden, 229 (Kildare), 106 Armagh Observatory, 394 Barna Golf Club, 272 Accommodations. See also Armagh Planetarium, 394 Barracka Books & CAZ Worker’s Accommodations Index Armagh’s Public Library, 391 Co-op (Cork City), 209–210 saving money on, 472–476 Ar mBréacha-The House of Beach Bar (Aughris), 333 Achill Archaeological Field Storytelling (Wexford), Beaghmore Stone Circles, 446 School, 323 128–129 The Beara Peninsula, 230–231 Achill Island, 320, 321–323 The arts, 8–9 Beara Way, 230 Adare, 255–256 Ashdoonan Falls, 351 Beech Hedge Maze, 94 Adrigole Arts, 231 Ashford Castle (Cong), 312–313 Belfast, 359–395 Aer Lingus, 15 Ashford House, 97 accommodations, 362–368 Agadhoe, 185 A Store is Born (Dublin), 72 active pursuits, 384 Aillwee Cave, 248 Athlone, 293–299 brief description of, 4 Aircoach, 16 Athlone Castle, 296 gay and lesbian scene, 390 Airfield Trust (Dublin), 62 Athy, 102–104 getting around, 362 Air travel, 461–468 Athy Heritage Centre, 104 history of, 360–361 Albert Memorial Clock Tower Atlantic Coast Holiday Homes layout of, 361 (Belfast), 377 (Westport), 314 nightlife, 386–390 Allihies, 230 Aughnanure Castle (near the other side of, 381–384 All That Glitters (Thomastown), -

Activities at the K Club.Pdf

While at The K Club, why not make the most of your stay and enjoy the range of activities we have on offer. From quiet fishing to energetic horse-riding we have a whole host of family friendly activities to suit everyone. www.kclub.ie Welcome €125.00 per adult for 3 hours €15.00 for each additional hour (Max 3 people per Ghillie, inclusive of all required Fishing at The K Club is mostly for Brown Trout and Rainbow Trout with the equipment) occasional Pike or Perch also. Fishing is carried out from the bank of the lakes Seasons Dates for Lakes Fishing and is done with a spinning rod and artificial bait or by Fly Rod and artificial flies. The group are accompanied by a ghillie (Fishing Guide) throughout the Brown Trout March 1st to September 30th session who will advise and demonstrate the art of casting and the placing of Rainbow Trout All year round baits in the correct manner so that a fish may be caught. All fish are returned alive to the water or if the guests wish may be brought to the kitchen and cooked Pike All year round to their requirements if so desired. Fishing €80.00 per adult / €55.00 per child for 2 hours Kayaking is now available on our private mile-long stretch of the beautiful river Liffey. If you have never kayaked before, you are in for a real treat, particularly as the river is so beautiful and peaceful here in the demesne. Our friendly and helpful instructors will provide wetsuits and an introduction to kayaking if needed before you set off for the afternoon. -

Phhwlqjv Lqfhqwlyh W

October 2008 MEET, EAT& SLEEP Why some conference menus are turkeys + How the Sage Gateshead won plaudits and business + Case studies: MSC Cruises, IPE International, Ungerboeck Systems International + EIBTM preview Distinctive locations. Rich rewards. BOOK+EARN BONUS JANUARY – JUNE 2009 Earn 2,500 bonus Starpoints for every event until 30 June, 2009. Now you can earn 2,500 bonus Starpoints® for every 25 room nights you book by 31 December, 2008, at Starwood properties throughout Europe, Africa and the Middle East for events from 1 January until 30 June, 2009. In addition to your bonus Starpoints, you’ll earn one Starpoint for every three US dollars spent on eligible meeting revenue. Visit the Special Offers section and terms & conditions on starwoodmeetings.com or ring +353 21 4539100 for more information. Sheraton Park Tower, London | UK Not a Starwood Preferred Planner? Sign up today and start accumulating thousands of Starpoints for each event that you book, redeemable for Free Night Awards without blackout dates and a host of other redemption options. STARWOOD Preferred Planner SPG, Starpoints, Preferred Guest, Sheraton, Four Points, W, Aloft, The Luxury Collection, Le Méridien, Element, Westin, St. Regis and their respective logos are the trademarks of Starwood Hotels & Resorts Worldwide, Inc., or its affi liates. © 2008 Starwood Hotels & Resorts Worldwide, Inc. All rights reserved. SHWSPP.08039 EAME 8/08 contents MANAGING EDITOR: MARTIN LEWIS 31 PUBLISHER: STEPHEN LEWIS EDITOR: JOHN KEENAN DEPUTY Meet, eat EDITOR: KATHERINE SIMMONS -

The 2019 Gold Medal Awards Finalist Announcement

The 2019 Gold Medal Awards Finalist Announcement The Gold Medal Awards, in association with Hotel & Catering Review magazine, are delighted to announce the Finalists for the 2019 awards. These awards celebrate the outstanding achievements of the hotel and catering sector throughout the country over the past 12 months. They also recognise and reward the high standards of excellence in terms of both the physical product and the level of service that is being delivered in our industry. After 3 months of travelling all corners of the country and visiting every single property that entered the awards, hours of meetings and further discussions, the Gold Medal Awards Judging Panel are proud to announce the Finalists in each category. Book Your Tickets Join us on Tuesday, September 24th in the Lyrath Estate, Co. Kilkenny where the winners of each category will be announced. To book tickets, please visit www.hotelandcateringreview.ie #GMA2019 @HC_Review Table of Contents Hotel Categories Ireland's Five Star Hotel……………………………………………………………………….……………………………………………………………………………….………… 2 Ireland's Four Star Hotel sponsored by Sodexo..……………………………………………………………………………………………………………….. 3 Ireland’s Five Star Resort…………………………………………………………………….…………………………………………………………………………….………… 4 Ireland's Four Star Resort sponsored by Avvio……………………………………...…………………………...……………………………………………………….... 5 Ireland's Three Star Hotel sponsored by Vernon Catering…………………………………………………………………………………………... 6 Ireland's Country House & Guest House………………………………………………………………...…………………...………………………………... -

View Art at the Merrion

Press Information THE ART OF THE MERRION Press Information: Sarah Glavey The Merrion, Dublin Tel: (353) 1 603 0600 Fax: (353) 1 603 0700 Email: [email protected] The spectacular collection of 19 th and 20 th Century Irish art hung throughout The Merrion, Dublin’s most luxurious 5-star hotel, is widely considered to be one of the most important in Ireland. Created from four magnificently restored Listed Georgian townhouses, the grace and elegance of The Merrion’s interior provides the perfect setting for the paintings. The result is a dramatic and successful marriage of classical architecture and contemporary art. True to the spirit of 18 th century arts patronage, Martin Mooney, one of Ireland’s finest young painters, was commissioned to paint a series of works for the elegant neo- classical stairwell in The Merrion’s Front Hall. The Front Hall remains much as it would have been when the house was built in the mid 18 th century. Plain white walls show off the original cornices and plasterwork, leaving Mooney’s murals as the main decorative feature. These, in subtle, warm colours, depict imaginary classical ruins, buildings and architectural details. The pronounced architectural element of Mooney’s style is particularly apt for The Merrion’s Georgian interior. After attending the University of Ulster, Mooney studied at Brighton Polytechnic, followed by a Post Graduate Degree at the Slade School of Fine Art, London. His work has been widely exhibited in both one-man and group exhibitions at galleries including The Solomon Gallery, Dublin; Waterman Fine Art, London; Theo Waddington Fine Art, London; The Royal Academy, London and The Royal Hibernian Academy, Dublin. -

Our 2010 Vacation in Ireland We Arrived in Dublin on Saturday, May 22 and Made the About 2-Hour Drive West to the Inny Bay B&B in Co

Ireland 2010 Our 2010 Vacation in Ireland We arrived in Dublin on Saturday, May 22 and made the about 2-hour drive west to the Inny Bay B&B in Co. Westmeath, north of the town of Athlone in the Irish midlands, on Lough Ree. We learned a bit about using a GPS, because had neither a street address nor coordinates for the B&B. We had to get close and stop at a house to ask directions. The B&B is on private land at the end of a 2 km long private road. We took a three hour nap to adjust for jet lag, and then drove to the nearby town of Ballymahon where we had sea bass, and of course, potatoes for dinner. The Inny Bay B&B is a pretty place amid nice scenery, with pastures, swans, the lough and the Inny River. Sunday’s breakfast, like the others at this B&B was huge, with bacon, kippers, etc. We took a morning walk along the Inny River. Then we visited Locke’s Distillery Museum in Kilbeggan, Co. Westmeath. It’s said to be the world’s oldest licensed pot distillery. The works and museum were interesting and the sample of its whiskey was excellent. We next headed for Clonmacnoise, in Shannonbridge, south of Athlone. It’s an early (6th century) Christian site with an Abby ruin, a church (St. Kiernan’s, Church of Ireland), a tower ruin, and a graveyard noted for its Celtic (or “high”) crosses. On our way there we spotted a castle ruin and found the curator there. -

Birr-Online-Special-2016.Pdf

Irish COUNTRY SPORTS and COUNTRY LIFE Including The NEW IRISH GAME ANGLER magazine SPECIAL GAME FAIRS ISSUE IRISH GAME & COUNTRY FAIR & FINE FOOD FESTIVAL Exciting Jousting from the Knights of the North BIRR CASTLE, CO OFFALY 27th & 28th AUGUST 10.00am – 6.00pm Ireland’s most action packed family event with: • Medieval Jousting • Carriage Driving & • Huge Tented Village with • Living History Village Bygones Area unrivalled shopping • Re-enactments • Dancing Horses opportunities • International Gundogs • Air Rifles & Archery • The Attractions of the • International Clay • Fine Food Pavilion Birr Demesne Shooting • Cookery Demonstrations • Angling Tuition for • International Terriers, • The Dog Guru Children Lurchers & Whippets • Action Packed Main • IFI LICENCE holders get your • Falcons & Ferrets Arena Programme SPECIAL ANGLERS DISCOUNT ADMISSION: Adult €15 Family €35 Parking & Programme Free For Further details see: www.irishgameandcountryfair.com www.countrysportsandcountrylife.com E: [email protected] Tel: 048 44839167/44615416 The Fair is supported by Country Sports and Country Life Editorial Comment iro. Coke. Hoover. And not deter the public who came here in Ireland if you love along in their thousands as usual. Bthe country lifestyle or Now it’s all systems go for the countrysports - Shanes or Birr. Irish Game & Country Fair and What’s the connection? Simple Fine Food Festival at Birr, County really — each of these words is Offaly (its full title) set in the known nationally and glorious Irish midlands internationally as a generic term, countryside, amongst fabled Northern Editor, synonymous with a particular castles and steeped in history. ROI Editor, Paul Pringle class-leading product. Have a look inside and savour Derek Fanning We want a cola — we ask for a coke. -

Issue Id: 2011/B/56 Annual Returns Received Between 25-Nov-2011 and 01-Dec-2011 Index of Submission Types

ISSUE ID: 2011/B/56 ANNUAL RETURNS RECEIVED BETWEEN 25-NOV-2011 AND 01-DEC-2011 INDEX OF SUBMISSION TYPES B1B - REPLACEMENT ANNUAL RETURN B1C - ANNUAL RETURN - GENERAL B1AU - B1 WITH AUDITORS REPORT B1 - ANNUAL RETURN - NO ACCOUNTS CRO GAZETTE, FRIDAY, 02nd December 2011 3 ANNUAL RETURNS RECEIVED BETWEEN 25-NOV-2011 AND 01-DEC-2011 Company Company Documen Date Of Company Company Documen Date Of Number Name t Receipt Number Name t Receipt 2152 CLEVELAND INVESTMENTS B1AU 28/10/2011 19862 STRAND COURT LIMITED B1C 28/10/2011 2863 HENRY LYONS & COMPANY, LIMITED B1C 25/11/2011 20144 CROWE ENGINEERING LIMITED B1C 01/12/2011 3394 CARRIGMAY LIMERICK, B1AU 28/10/2011 20474 AUTOMATION TRANSPORT LIMITED B1C 28/10/2011 3577 UNITED ARTS CLUB, DUBLIN, LIMITED B1C 28/10/2011 20667 WEXFORD CREAMERY LIMITED B1C 24/11/2011 7246 VALERO ENERGY (IRELAND) LIMITED B1C 21/10/2011 20769 CHERRYFIELD COURTS LIMITED B1C 28/10/2011 7379 RICHARD DUGGAN AND SONS, LIMITED B1C 26/10/2011 20992 PARK DEVELOPMENTS (IRELAND) B1C 28/10/2011 7480 BEWLEY'S CAFÉ GRAFTON STREET B1C 27/10/2011 LIMITED LIMITED 21070 WESTFIELD INVESTMENTS B1AU 28/10/2011 7606 ST. VINCENT'S PRIVATE HOSPITAL B1C 28/11/2011 21126 COMMERCIAL INVESTMENTS LIMITED B1C 24/10/2011 LIMITED 21199 PARK DEVELOPMENTS (1975) LIMITED B1C 28/10/2011 7662 THOMAS BURGESS & SONS LIMITED B1C 18/11/2011 21351 BARRAVALLY LIMITED B1C 28/10/2011 7857 J. H. DONNELLY (HOLDINGS) LIMITED B1C 28/10/2011 22070 CABOUL LIMITED B1C 28/10/2011 8644 CARRIGMAY B1C 28/10/2011 22242 ARKLOW HOLIDAYS LIMITED B1C 28/10/2011 9215 AER LINGUS LIMITED B1C 27/10/2011 22248 OGILVY & MATHER GROUP LIMITED B1C 28/10/2011 9937 D. -

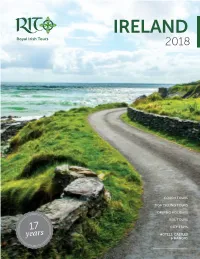

2018 CELEBRATING 17 Years

2018 CELEBRATING 17 years Canadian The authentic Irish roots One name, Company, Irish experience, run deep four spectacular Irish Heritage created with care. at RIT. destinations. Welcome to our We can recommend Though Canada is As we open tours 17th year of making our tours to you home for the Duffy to new regions memories in Ireland because we’ve family, Ireland is of the British Isles with you. experienced in our blood. This and beyond, our It’s been our genuine them ourselves. patriotic love is the priority is that we pleasure to invite you We’ve explored the driving force behind don’t forget where to experience Ireland magnificent basalt everything we do. we came from. up close and personal, columns at the We pride ourselves For this reason, and we’re proud Giant’s Causeway and on the unparalleled, we’ve rolled all of the part we’ve breathed the coastal personal experiences of our tours in played in helping to air at the mighty that we make possible under the name create thousands of Cliffs of Moher. through our strong of RIT. Under this exceptional vacations. We’ve experienced familiarity with the banner, we are As our business has the warm, inviting land and its locals. proud to present grown during this atmosphere of a The care we have for you with your 2018 time, the fundamental Dublin pub and Ireland will be evident vacation options. purpose of RIT has immersed ourselves throughout every Happy travels! remained the same: to in the rich mythology detail of your tour. -

Hide and Seek with Windows Shuttered and Corridors Empty for the First Six Months of the Year, Many Hotels Have Taken the Time to Re-Evaluate, Refresh and Rejuvenate

TRAVEL THE CLIFF AT LYONS Hide and Seek With windows shuttered and corridors empty for the first six months of the year, many hotels have taken the time to re-evaluate, refresh and rejuvenate. Jessie Collins picks just some of the most exciting new experiences to indulge in this summer. THE CLIFF AT LYONS What’s new Insider Tip Aimsir is upping its focus on its own garden produce, Cliff at Lyons guest rooms are all individually designed Best-loved for which is also to be used in the kitchens under the eye of and spread out between a selection of historic buildings Its laid-back luxurious feel and the fastest ever UK and former Aimsir chef de partie and now gardener, Tom that give you that taste of country life while maintaining Ireland two-star ranked Michelin restaurant, Aimsir. Downes, and his partner Stina. Over the summer, a new all the benefits of a luxury hotel. But there is also a There are award-winning spa treatments to be had at orchard will be introduced, along with a wild meadow selection of pet-friendly rooms if you fancy taking your The Well in the Garden, and with its gorgeous outdoor and additional vegetable beds which will be supplying pooch with you. Also don’t forget the Paddle and Picnic spaces, local history, canal walks, bike rides and paddle- the Cliff at Lyons restaurants. Chicken coops, pigs and package which gives you a one-night B&B stay plus SUP boarding there’s plenty to do. Sean Smith’s fresh take even beehives are also to be added, with the aim of session, and a picnic from their pantry, from €245 for two on classic Irish cuisine in The Mill has been a great bringing the Cliff at Lyons closer to self-sustainability. -

At Hayfield Manor 5 Star Hotel Cork, We

Press Pack At Hayfield Manor Video - Our Family, Your Home 5 Star Hotel Cork, we believe that a visit is an experience in itself. Whether you are joining us for leisure or business, it is our pleasure to care for every detail for you. Click Here to Watch the Video Online Conference Facilities Accommodation Hayfield Manor is the number of delegates (up to) ideal venue for weekend Kane Kirby 120 including 3 Grand Suites breaks, golfing holidays, William Kirby 60 88 1 Master Suite corporate meetings & Robert Kane 60 Bedrooms events, as well as intimate Boole Suite 50 wedding celebrations. Cork’s premier 5 Star hotel, Location Hayfield Manor continues To make an enquiry or Dining & Entertaining to extend the same warm to book please contact us 9km from Cork International Airport welcome to guests that it has (Approx 20mins car journey) done for the last 20+ years. + 353 21 484 5900 [email protected] 1.5km from Cork City Centre hayfieldmanor.ie (Approx 10mins walk) Perrott Avenue, College Road, 3.5km from Kent Train Station Cork, T12 HT97, Ireland. Key Team Members (Approx 10mins car journey) twitter.com/hayfieldmanor facebook.com/hayfieldmanor Hayfield Manor is located a short General Manager google.com/+hayfieldmanor/ journey from many of Cork’s most TJ Mulcahy pinterest.com/hayfieldmanor/ popular tourist attractions such as instagram.com/hayfieldmanor/ Blarney Castle, Kinsale, Cobh and Executive Head Chef Jameson Distillery Mark Staples Health & Beauty Events Manager Erin McCluskey Treatment Rooms Central Reservations Manager Nail Bar, Fitness Studio, Sauna, Barbara Culloty Steam Room, 17 Metre Indoor Pool & Outdoor Jacuzzi The Hayfield Manor Method We know that we have something special at Hayfield Manor.