View Annual Report

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

TERMS and CONDITIONS Standard Chartered Kuala Lumpur Marathon 2019 (“SCKLM 2019”) Priority Sign up Campaign

TERMS AND CONDITIONS Standard Chartered Kuala Lumpur Marathon 2019 (“SCKLM 2019”) Priority Sign Up Campaign Campaign 1.0 The Standard Chartered Bank Malaysia Berhad and Standard Chartered Saadiq Berhad (“the Bank”) Standard Chartered KL Marathon 2019 Priority Sign-Up Campaign (“Campaign”) will run from 15 January 2019 to 15 February 2019, inclusive of both dates (“Campaign Period”). 2.0 This campaign includes accounts under Standard Chartered Bank Malaysia Berhad (“SCBMB”) and also Standard Chartered Saadiq Berhad (“SCSB”). 3.0 By participating in this Campaign, participants agree to be bound by all the terms and conditions below. This Campaign terms must be read together with the product terms and the relevant banking agreements. If there are any inconsistencies between these terms and the relevant product terms and the banking agreement, these terms shall prevail limited only to the inconsistencies. Eligibility 4.0 This campaign is open to New-to-Bank (“NTB”) clients of the Bank who fulfil the following conditions (“Successful Sign-Up”): 4.1 Successfully establish a new Priority relationship where the NTB needs to maintain a minimum of MYR250,000 in deposits and/or investments as a Primary account holder during the Campaign Period. The Priority banking terms and conditions are available at https://www.sc.com/my/priority/tnc/; 4.2 Individuals over the age of 18 years. A NTB client is defined as an individual who starts a relationship with the Bank during the Campaign Period and does not include an individual who maintains or had maintained a banking relationship with the Bank within the past twelve (12) months from the date of commencement of the Campaign Period. -

The Bull Runner Magazine When She Bagged 2Nd Place for Women in Standard Chartered Do Not Necessarily Represent You Won One Pair of You Featured Inspired Me a Lot

Runner Bull The Runner Bull The [RACES] House, Glorietta 4. www. Call 491-5105 / 413-8083. avonkgbcphilippines.com www.thepinkrun.com SEPTEMBER 3: TAKBO! BREAST 17: THE BLUEWATER Hill, 3/5/10k. Call Nikki FRIENDS, Ultra, 3/5/10k. DAY SPA FUN RUN, SM 421-1213/ 0922-8151942 11: THE FS RUN (The Call 502-4260/ 0917- MOA. Call 703-1736 27: 1ST CEBU ULTRA- Fort Striders Club), 8138149 Bonifacio Global City, 24: ADIDAS KING OF MARATHON, Cebu City. 5/10/16k. Call 896-1954 3: TRAIL CALL RUN, THE Road, Bonifacio [email protected] Timberland, San Mateo, Global City, 5/10/21k. ST 28: MILO MARATHON - 12: 1 FINEX FUN RUN, 3/5/10k. Call 0927- Register at adidas Stores, CDO.Call Rudy Biscocho SM MOA, 3/5/10k. Call 3409023 RUNNR Store, BHS. 811-4052. finex.org.ph 0922-8367992 9: SOUTHRIDGE RUN, 24: MAYON TRAIL RUN, 28: KNOWLEDGE 12: THRILL OF THE West Gate Alabang, Legazpi City, 21k. www. CHANNEL TRAIL, Bohol, 11/22k. 1/5/10k. mayontrailrun.com www.thrillofthetrail.ph KARUNUNGAN 9: 1ST PAU MT. PINATUBO 31: MILO MARATHON 2010, Meralco, Ortigas, 12: MAKILING 50K TRAIL CHALLENGE, - Puerto Princesa. Call 3/5/10/15k. Call 983-5204/ CHALLENGE 9, U.P. Los Sta. Juliana, Capas, Tarlac Rudy Biscocho 0922- 983-2903, 0917-6256517 Baños, 5/10/16k. Call to Mt. Pinatubo Crater. 8367992 0906-4251387 Call 497-6442 [CLINICS] 12: MILO MARATHON 10: RUN FOR PASIG NOVEMBER MON/WED/FRI, 6:00 pm: - Tagbilaran. Call Rudy RIVER, 3/5/10/21k. 3k- Biscocho 0922-8367992 7: ATENEO BLUE RACE, RUNWALKING CLINIC, SM MOA, 5k- Luneta, ADMU, 3/5/7.5k, Call Philsports Complex 19: MILO MARATHON 10k- Bonifacio Global 0922-8330928, (ULTRA). -

Abstract Introduction

Global Media Journal – Malaysian Edition Volume 6, Issue 2, 2016 ISSN : 2231-9948 THE NUPTIALS OF SOCIAL AND TRADITIONAL MEDIA – WHY THIS SOPHISTICATED MIXED MARRIAGE IS WORTH MONITORING IN THE LONG-TERM Elliza Abdul Rahim Essence Communications Pusat Dagangan, Phileo Damansara 1, Selangor, Malaysia. [email protected] ABSTRACT For companies in Malaysia who want to stay ahead, monitoring their traditional media is no longer an only option. It is imperative that attention is paid to the implications of the heavy activity on the Internet via portals and social networking sites. Neglect would lead to a handicap of a swift response in real time which is a necessity in this age of nanotechnology. Integrating traditional and social media monitoring elevates management of information to a level that allows organizations to document, analyze and place a numeric value to their public relation efforts. Therefore, the objective of this paper is to highlight the activities reflecting the media monitoring based on a few samples of case studies and at the end emphasizes on the worth of mixed marriage of traditional and social media. Keywords: Mixed marriage; traditional; social media; monitoring and social sites. INTRODUCTION This country has been advocating mixed marriages since Adam. We marry the Malay and English language to make Manglish – much to the dismay of the English Language purist. We marry a plethora of food, customs and traditions to create the unique Malaysians we are today. It should not come as a surprise that there is an important 1 Global Media Journal – Malaysian Edition Volume 6, Issue 2, 2016 ISSN : 2231-9948 public relations marriage quietly being negotiated in the media arena that we need to be aware of. -

2020 Iif Annual Membership Meeting Financing a Sustainable Economy: Crisis Recovery and Drivers of Future Growth

OCTOBER 12-16, 2020 2020 IIF ANNUAL MEMBERSHIP MEETING FINANCING A SUSTAINABLE ECONOMY: CRISIS RECOVERY AND DRIVERS OF FUTURE GROWTH AGENDA * Timings for all sessions are noted in US EDT * DAY 1 MONDAY, OCTOBER 12 Timings for all sessions are noted in US EDT POLICYMAKER SERIES 7:00 am – 7:50 am IN-CONVERSATION The 2020 IIF Annual Membership Meeting (AMM) was the first fully + Haruhiko Kuroda, Governor, Bank of Japan + Tim Adams, President and Chief Executive Officer, IIF (Moderator) livestreamed AMM held from Monday, October 12 to Friday, October 8:00 am – 8:50 am IN-CONVERSATION 16 and focused on some of the most critical issues facing the financial + Ravi Menon, Managing Director, Monetary Authority of Singapore industry as a result of the COVID-19 pandemic. + Tim Adams, President and Chief Executive Officer, IIF (Moderator) 9:00 am – 9:50 am KEYNOTE/IN-CONVERSATION + Ryozo Himino, Commissioner, Financial Services Agency, Japan The 5-day program included the IIF's hallmark Views from the C-Suite + Andrés Portilla, Managing Director, Regulatory Affairs, IIF (Moderator) series and the new Policymaker series along with discussions on 10:00 am – 10:50 am IN-CONVERSATION + Jörg Kukies, State Secretary, Financial Market Policy and European sustainable finance, digital finance and innovation, the global regulatory Policy, Federal Ministry of Finance, Germany + Clay Lowery, Executive Vice President, Research and Policy, IIF outlook, and the economic outlook in developed and emerging (Moderator) markets. Attendees had the opportunity to hear from many influential 11:00 am – 11:50 am IN-CONVERSATION + Luis de Guindos, Vice President, European Central Bank voices, including CEO/Chairs, Policymakers, Innovators and Regulators + Clay Lowery, Executive Vice President, Research and Policy, IIF who offered perspectives on the global economy and the future of the (Moderator) 12:00 pm – 12:50 pm BIG THINK financial services industry in a post-COVID world. -

31227 Stanchart R&A

Group Chief Executive’s Review 2004 has been an excellent year for the Group. We have momentum and scale in our markets and we are delighted with the strategic progress we have made. Over the last three years, we have Looking to the year ahead, our industry Our 2005 priorities pursued a focused agenda. faces a number of challenges: rising sophistication and regionalisation of We set ourselves ambitious performance Expand Consumer Banking local banks; new entrants including goals and have consistently delivered customer segments non-bank financial institutions; margin against them. We have strengthened and products compression in many of our markets; the infrastructure and technology of increasingly demanding regulatory the Bank; we have developed a robust requirements; sophisticated customers Continue Wholesale Banking risk management capability; we are demanding more for less; the risk of a transformation reinvigorating our brand; we have major disruption from an unexpected increased staff engagement and event; and an unrelenting war for talent. deepened our talent pool. Our organic, Integrate Korea First Bank Like all international businesses, retaining broad based growth has given us the and deliver growth and attracting the best people in a highly shareholder support and confidence to competitive industry is always a challenge. make acquisitions and alliances. Accelerate growth in India Companies have to invest heavily in and China I would like to take this opportunity to recruiting and developing the right talent. thank our employees for their tremendous Many of these challenges are not new. efforts over the past three years which Deliver further What is different today is the pace and are turning Standard Chartered into a technology benefits intensity of change. -

Cover Nov 11-01

Volume: 06 | Issue: 04 | April 2015 MTBiz 1 ARTICLE OF THE MONTH An Account of Internaonal Trade of Bangladesh Introducon Industrial raw materials leads the total import volume of the Bangladesh started its internaonal trade since its independence country. From 2007-08 to 2013-14, import of industrial raw and it has been showing improvement in its trade balance materials has been following a posive trend and volume has since then. Though growth was bit flat in its early decades, the been geng bigger and bigger, which is a posive sign in favor improvement excelled since 1990s with the incepon of trade of development of the country. Petrolium and capital machinary liberalizaon. Bangladesh did very well in export, especially in also has been increasing over the years. These three secotrs of RMG, Shrimp & Fish, Leather and Jute & Jute goods sectors. Rise in import are very crucial for economic development and boosng imports of capital machinery and industrial raw materials, instead the export in the long run. of food and consumable items, is a visible trend in Bangladesh now. This arcle is an aempt to sketch the trajectory of Bangladesh in internaonal trade. It depicts the trend of growth in major sectors of export and import. It progresses with a comparave view of foreign trade and elucidates the trade balance of the country. This arcle also depicts the globally leading countries of internaonal trade and their trends. It ends up with a comparave analysis of Bangladesh in global and South Asian contexts. Import data of Bangladesh has been obtained from weekly publicaon of the country’s Central Bank. -

35153 Stanchart R&A 2004 0 Copy

35153 StanChart R&A 2004 C copy 8/3/05 10:01 AM Page 1 Annual Report and Accounts 2004 Standard Chartered Chartered Standard Annual Report and Accounts 2004 ds Leading the way ing ugh in Asia, Africa and – the andard of eye the Middle East rence. ct: ered.com 35153 StanChart R&A 2004 C copy 8/3/05 9:59 AM Page 2 Front Cover: Standard Chartered employs 33,000 people in over Thomas Migwi Kamau breaks the tape 550 locations serving 56 countries and territories to win the 2004 Standard Chartered Hong Kong Marathon across the Asia Pacific region, South Asia, the Middle Mr Kamau, from Kenya, set a personal best time in the 8th annual Standard Chartered Hong Kong East, Africa, the United Kingdom and the Americas. Marathon. The event, which hosted a record 24,000 runners in 2004, is a signature international sporting It is one of the world’s most international banks with event, attracting world-class runners from all corners employees representing 80 nationalities. of the globe. Standard Chartered serves both Consumer and Wholesale Banking customers, is well established in growth markets and aims to be The Right Partner for its customers. The Bank is trusted across its network for its standards of governance and its commitment to making a difference in the communities in which it operates. Leading the Way Leading the Way represents our strategic intent. It is the framework within which we make our strategic and operational decisions. In the context of this framework, each country and business decides its role and determines what actions are required to achieve the Strategic Intent. -

AIMS CALENDAR January 2010 - March 2011

AIMS CALENDAR January 2010 - March 2011 2010 16 Jan 2010 K inmen Marathon M/H TPE Taroko Gorge Marathon November Woon Kong Lee Post Office Box 47-110 Taipei, Taiwan, R.O.C Tel: 886 2 2585 5659 Fax: 886 2 2599 6716 Email: [email protected] Web: www.sportsnet.org.tw 17 Jan 2010 Standard Chartered MumBai Marathon IND M Hugh Jones Procam International, 14, St. James Court, Marine Drive, Mumbai - 20 Tel: 91 22 2202 02 84 Fax: 91 22 2202 5112 Email: [email protected] Web: www.procamintl.com Part of The Greatest Race on Earth 17 Jan 2010 China Coast Marathon and Half M/H H K G Catherine Leonard AVOHK, P.O. Box 28893, Gloucester Road Post Office, Wanchai Tel: 852 9038 5460 Email: [email protected] Web: www.avohk.org 17 Jan 2010 Maraton Internacional de Culiacan M E X M Juan Antonio Lopez Garibaldi Constitución 175 pte., Colonia Almada C.P. 80200, Culiacán, Sinaloa Tel: 667 712 4710 Fax: 667 713 9116 Email: [email protected] Web: www.maratonculiacan.org.mx 20 Jan 2010 Corrida de Sao Sebastiao 10km BR A R Joao Traven Rua Felix Pacheco 150 BL C-Apt 102 Leblon, Rio - RJ Tel: 55 21 2223 2773 Fax: 55 21 2223 3073 Email: [email protected] Web: www.corridadesaosebastiao.com.br 22 Jan 2010 Standard Chartered Dubai Marathon UAE M Peter Connerton P.O. Box 57176, Dubai Tel: 97 14 367 1062 Fax: 97 14 367 2524 Email: [email protected] Web: www.dubaimarathon.org 24 Jan 2010 K hon K aen Marathon THA M Apsit Rujikeatkamjorm Khon Kaen University Alumni AssociatIon, Khon Kaen University, 123/101 Moo 16, Tumbol Nai Muang, Amphur Muang, Khon Kaen 40002 Tel: 66 43 202 750 / 66 43 202 388 Fax: 66 43 202 750 / 66 43 202 388 Email: [email protected] Web: www.khonkaenmarathon.com 24 Jan 2010 Maui Ocean F ront Marathon & Half USA M Les Wright 2480 S. -

Standard Chartered Bank

Group ORANGE Sunyll Bhima Mohammad Nazir Takeshwarnath Reesaul Geetanjali Seewoosurrun Kaviraj Sukon In 2008 (SCB,2009) Formed in 1969 through a merger of The Standard Bank of British South Africa founded in 1863 & The Chartered Bank of India, Australia and China, founded in 1853. Network of over 1,750 branches and outlets in more than 70 countries across the Asia Pacific Region, South Asia, the Middle East, Africa, Europe and the Americas. 75,000 employees, representing 115 nationalities Listed on London and Hong Kong St ock Exchange in top 25 of FTSE 100 companies SCB in Mauritius: 2002 (SCB,2009) The Board of Directors… John Peace Acting Chairman The committees… Executive Directors Audit & Risk Peter Sands Richard Meddings Steve Bertamini Gareth Bullock Group CE Group FD Group ED Group ED Consumer Banking Africa, Middle East, Europe Board & the Americas Non-Executive Directors Nomination Board Remuneration Jamie Dundas Val Gooding Rudy Markham Ruth Markland NE Director NE Director NE Director NE Director Sustainability & Responsibility Sunil Mittal John Paynter Paul Skinner Oliver Stocken NE Director NE Director NE Director NE Director Business Model Building a sustainable business to deliver value to customers and shareholders whilst helping to address the significant social, economic and environmental issues the world is facing. (SCB,2009) Exhibit 1: The four pillars of SCB Sustainable Business (SCB,2009) Business Model (continued…) Exhibit 2: SCB Business and Strategies (SCB,2009) 1. Creating opportunities for new 4. Strong liquidity position solutions, services and ways to (Resources) grow the business in markets with the greatest social and environmental risks. 5. High A/D Ratio (Ratio of customer loans to 2. -

THE STUDY of VARIOUS FINANCIAL PRODUCTS OFFERED by STANDARD CHARTERED BANK Submitted in Partial Fulfilment for the Award Of

THE STUDY OF VARIOUS FINANCIAL PRODUCTS OFFERED BY STANDARD CHARTERED BANK Submitted in Partial Fulfilment for the Award of the Degree of Bachelor in Business Administration 2010-2012 Under the guidance of: Submitted by: Mr. Manoj Verma (senior scale) Maharaja Agrasen Institute of Management Studies Affiliated to Guru Gobind Singh Indraprastha University, Delhi PSP Area, Plot No.1, Sector-22, Rohini-Delhi 110086 STUDENT DECLARATION This is to certify that I have completed the Summer Project titled ―THE STUDY OF STANDARD CHARTERED BANK‖ under the guidance of ―Mr. Manoj Verma‖ in partial fulfilment of the requirement for the award of Degree of Bachelor of Business Administration at Maharaja Agrasen Institute of Management Studies, Delhi. This is an original piece of work and I have not submitted it earlier elsewhere. Date: 21st October, 2010 Signature: Place: Delhi Name: CERTIFICATE FROM THE INSTITUTE GUIDE This is to certify that the summer project titled ―THE STUDY OF STANDARD CHARTERED BANK‖ is an academic work done by ―‖ submitted in the partial fulfilment of the requirement for the award of the degree of Bachelor of Business Administration at Maharaja Agrasen Institute of Management Studies, Delhi, under my guidance and direction. To the best of my knowledge and belief the data and information presented by her in the project has not been submitted earlier. Signature: Name of the Faculty: Mr. Manoj Verma Designation: Assistant professor (senior scale) ACKNOWLEDGEMENT I gratefully acknowledges the valuable contribution of the following persons in completing my project report. They have been a great help and support in making my project. I am very thankful to them. -

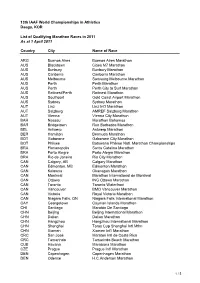

Qualifying Events WCH 2011 in 2010

13th IAAF World Championships in Athletics Daegu, KOR List of Qualifying Marathon Races in 2011 As at 1 April 2011 Country City Name of Race ARG Buenos Aires Buenos Aires Marathon AUS Blacktown Cities M7 Marathon AUS Bunbury Bunbury Marathon AUS Canberra Canberra Marathon AUS Melbourne Samsung Melbourne Marathon AUS Perth Perth Marathon AUS Perth Perth City to Surf Marathon AUS Rottnest/Perth Rottnest Marathon AUS Southport Gold Coast Airport Marathon AUS Sydney Sydney Marathon AUT Linz Linz Int'l Marathon AUT Salzburg AMREF Salzburg Marathon AUT Vienna Vienna City Marathon BAH Nassau Marathon Bahamas BAR Bridgetown Run Barbados Marathon BEL Antwerp Antwerp Marathon BER Hamilton Bermuda Marathon BOT Gaborone Gaborone City Marathon BOT Phikwe Botswana Phikwe Natl. Marathon Championships BRA Florianopolis Santa Catalina Marathon BRA Porto Alegre Porto Alegre Marathon BRA Rio de Janeiro Rio City Marathon CAN Calgary, AB Calgary Marathon CAN Edmonton, MB Edmonton Marathon CAN Kelowna Okanagan Marathon CAN Montreal Marathon International de Montreal CAN Ottawa ING Ottawa Marathon CAN Toronto Toronto Waterfront CAN Vancouver BMO Vancouver Marathon CAN Victoria Royal Victoria Marathon CAN Niagara Falls, ON Niagara Falls International Marathon CAY Georgetown Cayman Islands Marathon CHI Santiago Maratón De Santiago CHN Beijing Beijing International Marathon CHN Dalian Dalian Marathon CHN Hangzhou Hangzhou International Marathon CHN Shanghai Toray Cup Shanghai Intl Mthn CHN Xiamen Xiamen Int'l Marathon CRC San José Maraton Intl de Costa Rica CRC -

2003 Annual Review

30102 StanChart AnRvw Covers 7/5/2004 3:51 pm Page 1 Annual Review 2003 seeing is believing Standard Chartered Chartered Standard Annual Review 2003 Standard Chartered aims to raise funds to restore sight to one million people. © Standard Chartered PLC Our Seeing is Believing global fundraising campaign has already raised March 2004 US$1,400,000, enough to restore the sight of 56,000 people, twice our Registered Office: original target. 1 Aldermanbury Square The money raised will be administered by Sight Savers International and London EC2V 7SB other members of Vision 2020 ‘The Right to Sight’. Telephone +44 (0)20 7280 7500 Leading the way We would like to thank all our employees, customers, suppliers and www.standardchartered.com shareholders for their generous support. Principal Place of Business in Asia, Africa and Now we want to raise enough to restore a million eyesights. in Hong Kong: 32nd Floor, 4-4A Des Voeux Road, If you would like to support Seeing is Believing please contact: Genevieve Kotta, Community Relations Manager the Middle East Central, Hong Kong [email protected] Registered in England Telephone: +44 (0) 20 7280 7657 number: 966425 www.standardchartered.com 30102 StanChart AnRvw Covers 7/5/2004 3:51 pm Page 2 Front Cover: Standard Chartered employs 30,000 people in over The 2004 Standard Chartered Bank 500 locations serving 56 countries and territories Hong Kong Marathon. across the Asia Pacific Region, South Asia, the Standard Chartered has sponsored the Hong Kong Middle East, Africa, the United Kingdom and the Marathon since 1997. This year 24,000 runners took Americas.