Annual Report 2000

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

CITY of MELBOURNE CREATIVE STRATEGY 2018–2028 Acknowledgement of Traditional Owners

CITY OF MELBOURNE CREATIVE STRATEGY 2018–2028 Acknowledgement of Traditional Owners The City of Melbourne respectfully acknowledges the Traditional Owners of the land, the Boon Wurrung and Woiwurrung (Wurundjeri) people of the Kulin Nation and pays respect to their Elders, past and present. For the Kulin Nation, Melbourne has always been an important meeting place for events of social, educational, sporting and cultural significance. Today we are proud to say that Melbourne is a significant gathering place for all Aboriginal and Torres Strait Islander peoples. melbourne.vic.gov.au CONTENTS Foreword 04 Context 05 Melbourne, a city that can’t stand still 05 How to thrive in a world of change 05 Our roadmap to a bold, inspirational future 05 Why creativity? Work, wandering and wellbeing 06 Case Studies 07 Düsseldorf Metro, Germany, 2016 09 Te Oro, New Zealand, 2015 11 Neighbour Doorknob Hanger 13 The Strategy 14 Appendices 16 Measuring creativity 17 How Melburnians contributed to this strategy 18 Melbourne’s Creative Strategy on a page 19 September 2018 Cover Image: SIBLING, Over Obelisk, part of Biennial Lab 2016. Photo by Bryony Jackson Image on left: Image: Circle by Naretha Williams performed at YIRRAMBOI Festival 2017. Photo Bryony Jackson Disclaimer This report is provided for information and it does not purport to be complete. While care has been taken to ensure the content in the report is accurate, we cannot guarantee is without flaw of any kind. There may be errors and omissions or it may not be wholly appropriate for your particular purposes. In addition, the publication is a snapshot in time based on historic information which is liable to change. -

City Link's High-Speed Electronic Tolling

CASE PROGRAM 2007-91.1 City Link’s high-speed electronic tolling (A) The tolling systems went live without a glitch at 1 am Monday the 3rd [of January 2000], a national public holiday. Charges now apply at three toll points located at the Tullamarine section, the elevated roadway between Racecourse and Dynon Roads, and the Bolte Bridge… Although fewer motorists were on the road, demand for e-Tags was strong. Since the 23 December announcement [that tolling would begin 3 January] more than 45,000 e-Tags have been ordered, bringing the total sales to date to almost 400,000. The first day of tolling, CityLink’s 132629 hotline fielded more than 20,000 calls. The continued demand throughout the week prompted Transurban to announce the availability of a second hotline for general enquiries… Transurban Managing Director Kim Edwards said the company was pleased with the recent developments and expressed appreciation for the public’s patience during recent delays. “We are thrilled to deliver the completed Western Link to Melbourne’s motorists, who will now get the full benefit of the project’s leading-edge technology and design,” he said. Extract from: fasttrack, Transurban CityLink executive information newsletter, January 2000. In August 2000, Transurban City Link chief executive Kim Edwards announced that his company’s damages claim against the consortium Transfield-Obayashi Joint Venture (TOJV) for delays and difficulties with the 22-km City Link tollway was ________________________________________________________________ This case was prepared from published information by Susan Keyes-Pearce, MBA 1998 and Professor Michael Vitale of the Centre for Management of Information Technology at the University of Melbourne. -

Citylink Groundwater Management

CASE STUDY CityLink Groundwater Management Aquifer About CityLink Groundwater implications for design and construction A layer of soil or rock with relatively higher porosity CityLink is a series of toll-roads that connect major and permeability than freeways radiating outward from the centre of Design of tunnels requires lots of detailed surrounding layers. This Melbourne. It involved the upgrading of significant geological studies to understand the materials that enables usable quantities stretches of existing freeways, the construction of the tunnel will be excavated through and how those of water to be extracted from it. new roads including a bridge over the Yarra River, materials behave. The behavior of the material viaducts and two road tunnels. The latter are and the groundwater within it impacts the design of Fault zone beneath residential areas, the Yarra River, the the tunnel. A challenge for design beneath botanical gardens and sports facilities where surface suburbs and other infrastructure is getting access A area of rock that has construction would be either impossible or to sites to get that information! The initial design of been broken up due to stress, resulting in one unacceptable. the tunnel was based on assumptions of how much block of rock being groundwater would flow into the tunnel, and how displaced from the other. The westbound Domain tunnel is approximately much pressure it would apply on the tunnel walls They are often associated 1.6km long and is shallow. The east-bound Burnley (Figure 2). with higher permeability than the surrounding rock tunnel is 3.4km long part of which is deep beneath the Yarra River. -

Inbound Flights Into Adelaide Sydney to Adelaide

INBOUND FLIGHTS INTO ADELAIDE SYDNEY TO ADELAIDE DATE AIRLINE FLIGHT NUMBER DEPARTURE CITY DEPARTURE TIME ARRIVAL CITY ARRIVAL TIME 11 FEB 2018 JETSTAR JQ762 SYDNEY 0700 ADELAIDE 0835 11 FEB 2018 QANTAS QF1555 SYDNEY 0815 ADELAIDE 0955 11 FEB 2018 VIRGIN VA412 SYDNEY 0840 ADELAIDE 1020 11 FEB 2018 QANTAS QF741 SYDNEY 1045 ADELAIDE 1220 11 FEB 2018 QANTAS QF751 SYDNEY 1235 ADELAIDE 1410 11 FEB 2018 VIRGIN VA418 SYDNEY 1240 ADELAIDE 1420 11 FEB 2018 QANTAS QF759 SYDNEY 1355 ADELAIDE 1530 11 FEB 2018 QANTAS QF761 SYDNEY 1510 ADELAIDE 1645 11 FEB 2018 JETSTAR JQ764 SYDNEY 1530 ADELAIDE 1705 11 FEB 2018 VIRGIN VA428 SYDNEY 1610 ADELAIDE 1750 11 FEB 2018 QANTAS QF765 SYDNEY 1640 ADELAIDE 1815 11 FEB 2018 JETSTAR JQ768 SYDNEY 1725 ADELAIDE 1900 11 FEB 2018 QANTAS QF743 SYDNEY 1815 ADELAIDE 1950 11 FEB 2018 VIRGIN VA436 SYDNEY 1815 ADELAIDE 1955 11 FEB 2018 QANTAS QF783 SYDNEY 1955 ADELAIDE 2130 11 FEB 2018 JETSTAR JQ770 SYDNEY 2015 ADELAIDE 2150 11 FEB 2018 VIRGIN VA444 SYDNEY 2015 ADELAIDE 2155 11 FEB 2018 QANTAS QF785 SYDNEY 2035 ADELAIDE 2210 DATE AIRLINE FLIGHT NUMBER DEPARTURE CITY DEPARTURE TIME ARRIVAL CITY ARRIVAL TIME 12 FEB 2018 VIRGIN VA403 SYDNEY 0645 ADELAIDE 0825 12 FEB 2018 JETSTAR JQ762 SYDNEY 0700 ADELAIDE 0835 12 FEB 2018 QANTAS QF735 SYDNEY 0705 ADELAIDE 0840 12 FEB 2018 QANTAS QF739 SYDNEY 0820 ADELAIDE 0955 12 FEB 2018 VIRGIN VA412 SYDNEY 0840 ADELAIDE 1020 12 FEB 2018 JETSTAR JQ766 SYDNEY 1025 ADELAIDE 1200 12 FEB 2018 QANTAS QF741 SYDNEY 1045 ADELAIDE 1220 12 FEB 2018 QANTAS QF1557 SYDNEY 1130 ADELAIDE 1310 For any queries -

Free Tram Zone

Melbourne’s Free Tram Zone Look for the signage at tram stops to identify the boundaries of the zone. Stop 0 Stop 8 For more information visit ptv.vic.gov.au Peel Street VICTORIA ST Victoria Street & Victoria Street & Peel Street Carlton Gardens Stop 7 Melbourne Star Observation Wheel Queen Victoria The District Queen Victoria Market ST ELIZABETH Melbourne Museum Market & IMAX Cinema t S n o s WILLIAM ST WILLIAM l o DOCKLANDS DR h ic Stop 8 N Melbourne Flagstaff QUEEN ST Gardens Central Station Royal Exhibition Building St Vincent’s LA TROBE ST LA TROBE ST VIC. PDE Hospital SPENCER ST KING ST WILLIAM ST ELIZABETH ST ST SWANSTON RUSSELL ST EXHIBITION ST HARBOUR ESP HARBOUR Flagstaff Melbourne Stop 0 Station Central State Library Station VICTORIA HARBOUR WURUNDJERI WAY of Victoria Nicholson Street & Victoria Parade LONSDALE ST LONSDALE ST Stop 0 Parliament Station Parliament Station VICTORIA HARBOUR PROMENADE Nicholson Street Marvel Stadium Library at the Dock SPRING ST Parliament BOURKE ST BOURKE ST BOURKE ST House YARRA RIVER COLLINS ST Old Treasury Southern Building Cross Station KING ST WILLIAM ST ST MARKET QUEEN ST ELIZABETH ST ST SWANSTON RUSSELL ST EXHIBITION ST COLLINS ST SPENCER ST COLLINS ST COLLINS ST Stop 8 St Paul’s Cathedral Spring Street & Collins Street Fitzroy Gardens Immigration Treasury Museum Gardens WURUNDJERI WAY FLINDERS ST FLINDERS ST Stop 8 Spring Street SEA LIFE Melbourne & Flinders Street Aquarium YARRA RIVER Flinders Street Station Federation Square Stop 24 Stop Stop 3 Stop 6 Don’t touch on or off if Batman Park Flinders Street Federation Russell Street Eureka & Queensbridge Tower Square & Flinders Street you’re just travelling in the SkyDeck Street Arts Centre city’s Free Tram Zone. -

Melbourne Retail Guide

MELBOURNE Cushman & Wakefield Global Cities Retail Guide Cushman & Wakefield | Melbourne | 2018 0 Melbourne is Victoria's capital city and the business, administrative, cultural and recreational hub of the state. With a combination of world-class dining, art galleries, homegrown fashion and a packed sports calendar, Melbourne is regarded as one of the world’s most liveable city. Melbourne’s retail and hospitality sectors are booming, creating jobs, economic growth and a buzzing international city. Melbourne’s CBD is home to more than 19,000 businesses and caters for 854,000 people on a typical weekday. Melbourne is the centre of the Australian retail industry – an exciting mix of international designer brands, flagship stores, local fashion retailers and world class department stores including Australia’s first Debenhams department store. The city has a reputation for style and elegance while at the same time being fashion forward. Melbourne offers a range of retail locations to suit a variety of stores – with flourishing inner city shopping strips and larger suburban shopping complexes, accounting for 16% of all major shopping centres in Australia. Melbourne's CBD has evolved as the pre- eminent shopping area in Australia and a destination for global brands. The city centre has a wide variety of modern retail complexes housing local and international retailers, historic arcades, bustling laneways, a luxury MELBOURNE precinct and heritage-listed markets. The City of Melbourne municipality covers 37.7 sqkm. It is OVERVIEW made up of the city centre and a number of inner suburbs, each with its own distinctive character and with different businesses, dwellings and communities living and working there. -

Factors Influencing Bike Share Membership

Transportation Research Part A 71 (2015) 17–30 Contents lists available at ScienceDirect Transportation Research Part A journal homepage: www.elsevier.com/locate/tra Factors influencing bike share membership: An analysis of Melbourne and Brisbane ⇑ Elliot Fishman a, , Simon Washington b,1, Narelle Haworth c,2, Angela Watson c,3 a Department Human Geography and Spatial Planning, Faculty of Geosciences, Utrecht University, Heidelberglaan 2, 3584 CS Utrecht, Netherlands b School of Urban Development, Faculty of Built Environment and Engineering and Centre for Accident Research and Road Safety (CARRS-Q), Faculty of Health Queensland University of Technology, 2 George St., GPO Box 2434, Brisbane, Qld 4001, Australia c Centre for Accident Research and Road Safety – Queensland, K Block, Queensland University of Technology, 130 Victoria Park Road, Kelvin Grove, QLD 4059, Australia article info abstract Article history: The number of bike share programs has increased rapidly in recent years and there are cur- Received 17 May 2013 rently over 700 programs in operation globally. Australia’s two bike share programs have Received in revised form 21 August 2014 been in operation since 2010 and have significantly lower usage rates compared to Europe, Accepted 29 October 2014 North America and China. This study sets out to understand and quantify the factors influ- encing bike share membership in Australia’s two bike share programs located in Mel- bourne and Brisbane. An online survey was administered to members of both programs Keywords: as well as a group with no known association with bike share. A logistic regression model Bicycle revealed several significant predictors of membership including reactions to mandatory CityCycle Bike share helmet legislation, riding activity over the previous month, and the degree to which conve- Melbourne Bike Share nience motivated private bike riding. -

View Walk D'albora Marinas Departure Points Ground Registry of Boathouse Drive Shed 2 Cumberland St No

Melbourne City Map Accessible toilet ARDEN ST BBQ Bike path offroad/onroad Cinema Parking Places of interest City circle tram route with QUEENSBERRY ST DRYBURGH ST stops Places of worship BAILLIE ST Educational facility Melbourne city tourist Playground ABBOTSFORDPROVOST ST ST ARDEN SIDING RAILWAY shuttle bus stop MUNSTER TCE Hospital Post Office STAWELL ST LAURENS ST Tram route with platform Marina Taxi rank stops WRECKYNARTS HOUSE ST VICTORIA ST MARKETMEAT Police Theatre LOTHIAN STTrain station ELM ST Train Toilet MILLER ST BLACKWOOD ST COURTNEY ST To Sydney Road under construction/ ANDERSON ST NORTH via MELBOURNE Sydney Rd RAILWAY PL future development site TOWN HALL & LIBRARY MELBOURNE GOODS RAILWAY CURZON ST PELHAMBERKELEY ST ST Visitor information centre BEDFORD ST BARRY ST QUEENSBERRY ST ELIZABETH ST SPENCER ST ERROL ST No TO ZOO DRYBURGH ST r KING ST M t To LEVESON ST e h BERKELEY ST Melb. Uni., lbo Melb. Cemetery u STBARRY & Dental NORTH MELBOURNE RAILWAY PL EADES rn IRELAND ST e Hosp. GRATTAN ST ADDERLEY ST ABBOTSFORD ST To Airport, PELHAM ST CARLTON ST Bendigo, COSTCO O'CONNELL ST Daylesford via HAWKE ST COBDEN ST PEEL ST Calder Fwy PIAZZA ITALIA CHETWYND ST WILLIAM ST FOOTSCRAY RD VICTORIA ST WESTERN LINK (CITYLINK) RODEN ST HOWARD ST PELHAM ST ICEHOUSE CAPEL ST MOOR ST PEEL ST MILTON ST MILTON PEARL RIVER RD WATERFRONTWAY STANLEY ST Carl LEICESTER ST to KING WILLIAM ST WALSH ST QUEEN n WATERFRONT ROSSLYN ST 8 VICTORIA IMAX k MARKET BOUVERIE ST e CITY W re QUEENSBERRY ST ST DAVID ST C e M To Eastern s s THERRY ST d LITTLE -

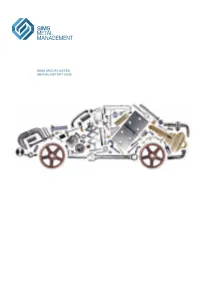

SIMS GROUP LIMITED Annual REPORT 2008 SIM S G R O U P L IM IT E D a N N U a L RE P O R T 2 0

SIMS GROUP LIMITED GROUP SIMS ANN U a L REPORT2008 L ThE average motor vEhIcle SIMS GROUP LIMITED Lasts 13.5 yEars anD comprises annUaL report 2008 approximately 15,000 IndividuaL Parts, Of whIch 80% are potentially recOverable. Approximately 68% Of a vEhIcle’S Parts by weighT aRE steel, followed by plastic (9%) anD nOn ferrous metals (8%), with ThE remaInder rubber, glass anD other materials. www.simsMM.cOM finanCiaL Summary Corporate DireCtory For the year ended 30 June 2008 SeCuritieS exChange LiSting Shareholder enquirieS The Company’s ordinary shares are quoted Enquiries from investors regarding their $7.67 b 38% $433m 81% 306¢ 60% 130¢ 8% on the Australian Securities Exchange under share holdings should be directed to: the ASX Code ‘SGM’. Computershare Investor Services Pty Limited TotaL REvEnue Profit after Tax EaRnIngs per ShaRE DIvidends per Share The Company’s American Depositary Shares Level 3 (ADSs) are quoted on the New York Stock 60 Carrington Street Exchange under the symbol ‘SMS’. The Company Sydney NSW 2000 has a Level II ADS program, and the Depositary Postal Address: is the Bank of New York Mellon Corporation. GPO Box 7045 ADSs trade under cusip number 829160100 Sydney NSW 2001 with each ADS representing one (1) ordinary Telephone: 1300 855 080 share. Further information and investor Facsimile: (02) 8235 8150 enquiries on ADSs may be directed to: Company SeCretarieS $181m 42% 14.6% 22% 10.9% 43% $8.02 72% The Bank of New York Mellon Corporation Frank Moratti Depositary Receipts Division Scott Miller Net caSh flowS Return -

Victoria Harbour Docklands Conservation Management

VICTORIA HARBOUR DOCKLANDS CONSERVATION MANAGEMENT PLAN VICTORIA HARBOUR DOCKLANDS Conservation Management Plan Prepared for Places Victoria & City of Melbourne June 2012 TABLE OF CONTENTS LIST OF FIGURES v ACKNOWLEDGEMENTS xi PROJECT TEAM xii 1.0 INTRODUCTION 1 1.1 Background and brief 1 1.2 Melbourne Docklands 1 1.3 Master planning & development 2 1.4 Heritage status 2 1.5 Location 2 1.6 Methodology 2 1.7 Report content 4 1.7.1 Management and development 4 1.7.2 Background and contextual history 4 1.7.3 Physical survey and analysis 4 1.7.4 Heritage significance 4 1.7.5 Conservation policy and strategy 5 1.8 Sources 5 1.9 Historic images and documents 5 2.0 MANAGEMENT 7 2.1 Introduction 7 2.2 Management responsibilities 7 2.2.1 Management history 7 2.2.2 Current management arrangements 7 2.3 Heritage controls 10 2.3.1 Victorian Heritage Register 10 2.3.2 Victorian Heritage Inventory 10 2.3.3 Melbourne Planning Scheme 12 2.3.4 National Trust of Australia (Victoria) 12 2.4 Heritage approvals & statutory obligations 12 2.4.1 Where permits are required 12 2.4.2 Permit exemptions and minor works 12 2.4.3 Heritage Victoria permit process and requirements 13 2.4.4 Heritage impacts 14 2.4.5 Project planning and timing 14 2.4.6 Appeals 15 LOVELL CHEN i 3.0 HISTORY 17 3.1 Introduction 17 3.2 Pre-contact history 17 3.3 Early European occupation 17 3.4 Early Melbourne shipping and port activity 18 3.5 Railways development and expansion 20 3.6 Victoria Dock 21 3.6.1 Planning the dock 21 3.6.2 Constructing the dock 22 3.6.3 West Melbourne Dock opens -

Southbank Community Plan Involved Extensive Consultation with City of Melbourne 2

The Southbank Community Plan BOATHOUSE DRIVE ALEXANDRA GARDENS SOUTHGATE HENLEY RESERVE ST KILDA RD RIVERSIDE ALEXANDRA AV QUAY CITY RD QUEEN VICTORIA ST GARDENS AGH CROWN CASINO IDGE ST VAN KAVANAGHKA ST KINGS ENTERTAINMENTCOMPLEX POWER ST SOUTHBANK SIDNEY MYER BR DOMAIN LINLITHGOW CLARENDON BOULEVARD MUSIC BOWL YARRA RIVER KINGS DOM (BURNLEY TUNNEL) QUEENS KINGS FERRARS ST ST (DOMAIN TUNNEL) AV WAY AIN LORIMER ST VICTORIAN MELBOURNE COLLEGE OF THE ARTS EXHIBITION KINGS ST ANAGH ST CT CENTRE BY DOMAIN A KAVANAGHKAV ST GOVERNMENT D Z MORAY ST WADEY ST HOUSE DRIVE A ALEXANDRA AV NORMAN CLARKE AV MONTAGUE ST MAZDAM CT MUNRO ST DEPARTMENT CITY RD DEFENCE OF ANZAC AV GOVERNMENT DODDS ST HAIG ST ST WELLS ST VICTORIA HOUSE BARRACKS KINGS WAY BIRDWOOD ALEXANDRA AV Y ST.KILDA RD EWA FRE T GATE WES MILES ST COVENTRY ST STURT ST ROYAL BOTANIC AV GARDENS CLOWES ST WELLS ST DRIVE ST DORCAS ST KINGS WAY SHRINE OF REMEMBRANCE RESERVE BROOKS KINGS ANDERSON DOMAIN WALSH ST DALLAS SOUTH DOMAIN RD MELBOURNE GRAMMAR SCHOOL BROMBY ST RD ST ST S ARNOLD ST HOPE ST ADAM MILLSWYN What happens now? PARK ST DOMAIN ST MARNE ST WALSH ST PUNT RD An implementation plan and specific timelines are being TOORAK RD developed. Some items are expected to be completed by August 2004. QUEENS ST.KILDA RD RO Implementation timelines FAWKNER PARK AD Details of short and long term actions are provided CORDNER in the full implementation plan. The implementation OVAL ST.KILDA plan is available by contacting the Council Hotline after July 15, 2004. -

Toll Roads - National Cover Australian Toll Roads

Toll Roads - National Cover Australian Toll Roads Roam Express offers a visitor e-pass which is valid for up Please be aware that toll fees apply on some roads in to 30 days on all Australian toll roads. Australia. A visitor E-Pass can be set up before or within 48 hours of You will likely encounter toll roads if you are driving through your first trip to cover travel on all Australian toll roads. Metropolitan New South Wales, Queensland and Victoria. When driving a thl rental vehicle in Australia you are responsible for paying toll fees, so it is important to be aware of these roads before you travel. As most toll roads in Australia Roam Contact Details are electronically tolled, you will not be able to stop and pay Ph: 13 76 26 cash. www.roamexpress.com.au Please refer to this brochure which provides an overview of all International Callers: +61 2 9086 6400 Australian toll roads as well as information on how to pay for toll travel. Bitte beachten Sie, dass einige Strassen Zahlungspflichtig 17 16 15 Castle Hill 14 sind in Australien. 13 Die Mautstrassen befinden sich in New South Wales, Queensland 18 10 12 M2 und Victoria. 11 9 Manly Wenn Sie ein Wohnmobil von thl gemietet haben in Australien 19 sind Sie verantwortlich die Gebuehren zu zahlen, deshalb ist es 44 20 Paramatta 8 wichtig dass Sie sich ueber diese Strassen informieren. Die moisten 21 7 Mautstrassen sind elektronisch und Sie koennen nicht Bar bezahlen 22 Harbour 6 oder anhalten. Eastern Bridge 5 Sydney 4 Bitte beachten Sie die Broschure die Sie in Ihren Unterlagen Creek M7 CBD 2 3 bekommen wo diese Strassen sind und wie Sie bezahlen koennen.