Commodity Market Integration, 1500–2000

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Control of the Value of Black Goldminers' Labour-Power in South

Farouk Stemmet Control of the Value of Black Goldminers’ Labour-Power in South Africa in the Early Industrial Period as a Consequence of the Disjuncture between the Rising Value of Gold and its ‘Fixed Price’ Thesis submitted for the Degree of Doctor of Philosophy Faculty of Social Sciences, University of Glasgow October, 1993. © Farouk Stemmet, MCMXCIII ProQuest Number: 13818401 All rights reserved INFORMATION TO ALL USERS The quality of this reproduction is dependent upon the quality of the copy submitted. In the unlikely event that the author did not send a com plete manuscript and there are missing pages, these will be noted. Also, if material had to be removed, a note will indicate the deletion. uest ProQuest 13818401 Published by ProQuest LLC(2018). Copyright of the Dissertation is held by the Author. All rights reserved. This work is protected against unauthorized copying under Title 17, United States C ode Microform Edition © ProQuest LLC. ProQuest LLC. 789 East Eisenhower Parkway P.O. Box 1346 Ann Arbor, Ml 48106- 1346 GLASGOW UNIVFRSIT7 LIBRARY Abstract The title of this thesis,Control of the Value of Black Goldminers' Labour- Power in South Africa in the Early Industrial Period as a Consequence of the Disjuncture between the Rising Value of Gold and'Fixed its Price', presents, in reverse, the sequence of arguments that make up this dissertation. The revolution which took place in the value of gold, the measure of value, in the second half of the nineteenth century, coincided with the need of international trade to hold fast the value-ratio at which the world's various paper currencies represented a definite weight of gold. -

1 ENTER the GHOST Cashless Payments in the Early Modern Low

ENTER THE GHOST Cashless payments in the Early Modern Low Countries, 1500-18001 Oscar Gelderbloma and Joost Jonkera, b Abstract We analyze the evolution of payments in the Low Countries during the period 1500-1800 to argue for the historical importance of money of account or ghost money. Aided by the adoption of new bookkeeping practices such as ledgers with current accounts, this convention spread throughout the entire area from the 14th century onwards. Ghost money eliminated most of the problems associated with paying cash by enabling people to settle transactions in a fictional currency accepted by everyone. As a result two functions of money, standard of value and means of settlement, penetrated easily, leaving the third one, store of wealth, to whatever gold and silver coins available. When merchants used ghost money to record credit granted to counterparts, they in effect created a form of money which in modern terms might count as M1. Since this happened on a very large scale, we should reconsider our notions about the volume of money in circulation during the Early Modern Era. 1 a Utrecht University, b University of Amsterdam. The research for this paper was made possible by generous fellowships at the Netherlands Institute for Advanced Studies (NIAS) in Wassenaar. The Meertens Institute and Hester Dibbits kindly allowed us to use their probate inventory database, which Heidi Deneweth’s incomparable efforts reorganized so we could analyze the data. We thank participants at seminars in Utrecht and at the Federal Reserve Bank of Atlanta, and at the Silver in World History conference, VU Amsterdam, December 2014, for their valuable suggestions. -

Globalization and the European Economy: Medieval Origins to the Industrial Revolution

CORE Metadata, citation and similar papers at core.ac.uk Provided by Columbia University Academic Commons Columbia University Department of Economics Discussion Paper Series Globalization and the European Economy: Medieval Origins to the Industrial Revolution Ronald Findlay Discussion Paper #:0102-28 Department of Economics Columbia University New York, NY 10027 March 2002 1. Introduction Any consideration of “The Europeanization of the Globe and the Globalization of Europe” must confront the problem of how to specify the spatio-temporal coordinates of the concept of Europe. When does “Europe” begin as a meaningful cultural, social and political expression and how far east from the shores of the Atlantic and the North Sea does it extend? In this paper I will begin with Charlemagne, which is to say around 800. It is at about this time that that the designations of Europe and European first begin to be used. Denys Hay (1966:25) cites an eighth-century Spanish chronicler who refers to the forces of Charles Martel, Charlemagne’s grandfather, at the celebrated Battle of Poitiers in 732 as Europeenses or Europeans, rather than as Christians, and their opponents as Arabs, rather than as Muslims, a nice example of ethnic as opposed to religious identification of “ourselves” and “the other.” In terms of space I will go not too much further east than the limits of the Carolingian Empire at its peak, which is conveniently depicted in the map provided by Jacques Boussard (1976:40-41). In this map it is remarkable to see how closely the empire coincides with the area covered by the “Inner Six” of the European Common Market, with the addition of Austria and Hungary. -

Money, States and Empire: Financial Integration Cycles and Institutional Change in Central Europe, 1400-1520

Working Papers No. 132/09 Money, States and Empire: Financial Integration Cycles and Institutional Change in Central Europe, 1400-1520 . David Chilosi and Oliver Volckart © David Chilosi, LSE Oliver Volckart, LSE December 2009 Department of Economic History London School of Economics Houghton Street London, WC2A 2AE Tel: +44 (0) 20 7955 7860 Fax: +44 (0) 20 7955 7730 Money, States and Empire: Financial Integration Cycles and Institutional Change in Central Europe, 1400-1520* David Chilosi and Oliver Volckart Abstract By analysing a newly compiled database of exchange rates, this paper finds that Central European financial integration advanced in a cyclical fashion over the fifteenth century. The cycles were associated with changes in the money supply. Long-distance financial integration progressed in connection with the rise of the territorial state, facilitated by the synergy between princes and emperor. 1. Introduction Traditionally, research paints a gloomy picture of trade in the late Middle Ages. Pirenne (1936/61: 192) saw medieval economic expansion coming to an end early in the fifteenth century. Lopez and Miskimin (1962) coined the ‘economic depression of the Renaissance’. Mainly drawing on English export and import data, Postan (1952/87: 240 ff.) called the second half of the fourteenth and the first of the fifteenth century ‘a period of arrested development’. Analysing customs records from Genoa, Marseilles and Dieppe, Miskimin (1969: 129) arrived at a similar conclusion: According to him, trade experienced a downward trend throughout the greater part of the fifteenth century. As recently as the 1990s, Nightingale (1990; 1997) claimed that in the middle decades of the fifteenth century English commerce ran into serious difficulties, with London merchants suffering a liquidity crisis. -

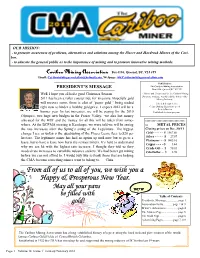

Cariboo Mining Association Box 4184, Quesnel, BC, V2J 6T9 Email: [email protected] Webpage: Ww.Cariboominingassociation.Com

OUR MISSIO: - to promote awareness of problems, alternatives and solutions among the Placer and Hardrock Miners of the Cari- boo. - to educate the general public as to the importance of mining and to promote innovative mining methods. Cariboo Mining Association Box 4184, Quesnel, BC, V2J 6T9 Email: [email protected] Webpage: ww.Cariboominingassociation.com Published by: PRESIDET’S MESSAGE The Cariboo Mining Association Box 4184, Quesnel,BC, V2J 3J3 Well, I hope you all had a good Christmas Season. “ Miners and Prospectors in the Cariboo Mining Division working together for the Future of the 2011 has been a roller coaster ride for investors. Hopefully gold Mining Industry” will recover some, there is allot of “paper gold “ being traded Edited & designed by: right now to hinder a healthy gold price. I expect 2012 will be a Celine Duhamel, Edith Spence & Brenda Dunbar banner year for tax increases, we will be paying for the 2010 Published six times per year. Olympics, two huge new bridges in the Fraser Valley, we also lost money allocated for the HST and the money for all this will be taken from some- $$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$ where. At the BCPMA meeting in Kamloops, we were told we will be seeing $$ METAL PRICES the rate increases after this Spring’s sitting of the Legislature. The biggest Closing prices on Dec. 30/11 change I see as unfair is the quadrupling of the Placer Lease fees to $20 per Gold - - - - - - $ 1567.80 hectare. The legitimate miner has had no option up until now but to go to a Silver - - - - - $ 27.87 lease, but to have a lease now hurts the serious miners. -

The British Numismatic Journal 2011

THE BRITISH NUMISMATIC JOURNAL 2011 INCLUDING THE Proceedings of the British Numismatic Society for the year 2010 EDITED BY E.M. SCREEN AND M.R. ALLEN VOLUME 81 2011 THE BRITISH NUMISMATIC JOURNAL 2011 ISSN 0143-8956 Typeset by New Leaf Design, Scarborough, North Yorkshire Printed in Malta by Gutenberg Press Ltd, Tarxien, Malta © Royal Mint © Royal DEDICATED TO GRAHAM DYER OBE FSA PRESIDENT OF THE SOCIETY 1994–1998 TO MARK THE 50TH ANNIVERSARY OF HIS APPOINTMENT TO THE ROYAL MINT 8 AUGUST 1961 CONTENTS Roman coins of London from the Falmouth hoard, by Lord STEWARTBY 1 The Pacx type of Edward the Confessor, by Hugh PAGAN 9 The exchanges, silver purchases and trade in the reign of Henry III, by Richard CASSIDY 107 Checking the current coins 1344–1422, by Norman BIGGS 119 Was there a ‘Crisis of Credit’ in fi fteenth-century England? The Howard Linecar Lecture 2009, by James L. BOLTON 144 Presidential Address. The illustration of coins: an historical survey. Part II, by R.J. EAGLEN 165 A study of the ‘Weyl’ pattern pennies, halfpennies and farthings dated 1860 and 1887, by R.J. PEARCE 181 Completing the change: the New Zealand coin reverses of 1940 by Mark STOCKER 203 SHORT ARTICLES AND NOTES Roman quadrantes found in Britain, in light of recent discoveries recorded with the Portable Antiquities Scheme, by Frances MCINTOSH and Sam MOORHEAD 223 The earliest known type of Edward the Confessor from the Bury St Edmunds mint, by David PALMER 230 Stephen BMC type I from Bury St Edmunds with left-facing bust, by R.J. -

Good Or Bad Money? Debasement, Society and the State in the Late Middle Ages

CORE Metadata, citation and similar papers at core.ac.uk Provided by LSE Research Online Working Papers No. 140/10 Good or Bad Money? Debasement, Society and the State in the Late Middle Ages . David Chilosi and Oliver Volckart © David Chilosi, and Oliver Volckart May 2010 Department of Economic History London School of Economics Houghton Street London, WC2A 2AE Tel: +44 (0) 20 7955 7860 Fax: +44 (0) 20 7955 7730 Good or Bad Money? Debasement, Society and the State in the Late Middle Ages David Chilosi and Oliver Volckart Abstract This paper revisits the question of debasement by analysing a newly compiled dataset with a novel approach, as well as employing conventional methods. It finds that mercantile influence on monetary policies favoured relative stability, and wage-payers did not typically gain from silver debasement. Excess demand for bullion was not a major cause of debasement. Yet monetary issues were important. Warfare made the debasement of silver but not of gold more likely. Regime types had an importance comparable to that of warfare: Princes debased silver more often than monetary unions and especially city-states. It is likely that fiscal debasements were more frequent in principalities, not least because princes debased for fiscal reasons also in the absence exceptional needs. The conclusion discusses the implications of the findings. 1. Introduction As a corollary to the revival of interest in medieval trade, scholars have increasingly stressed that ‘medieval money matters’ (Wood, 2004). Under the conditions of a commodity money system with an inelastic supply of bullion, the level of monetisation and therefore commercialisation is assumed to have crucially depended on the supply of hard money as determined by mining output and the balance of trade (cf. -

Ebook Download the Energy Crisis 1St Edition Ebook, Epub

THE ENERGY CRISIS 1ST EDITION PDF, EPUB, EBOOK David Hawdon | 9781351396301 | | | | | The Energy Crisis 1st edition PDF Book An early response from stakeholders is the call for reports, investigations and commissions into the price of fuels. Help Learn to edit Community portal Recent changes Upload file. Hidden categories: Webarchive template wayback links CS1 errors: missing periodical Webarchive template archiveis links Articles with short description Short description matches Wikidata All articles with unsourced statements Articles with unsourced statements from October Articles with unsourced statements from February Commons category link is on Wikidata. Send MSN Feedback. February Richard M. A crisis could possibly emerge after infrastructure damage from severe weather. Three Mile Island is the site of a nuclear power plant in south central Pennsylvania. Chinese energy policy includes specific targets within their 5-year plans. Live TV. Economics portal Energy portal Renewable energy portal. The utility said the blackouts would generally last about an hour, and as many as , could be affected. Gas station owners placed signs like this one on the back bumpers of cars, designating the last car to be served. The risk of stagflation increases. Though the Yom Kippur War ended in late October, the embargo and limitations on oil production continued, sparking an international energy crisis. It is the responsibility of utilities to keep on upgrading the infrastructure and set a high standard of performance. If an energy shortage is prolonged a crisis management phase is enforced by authorities. Amsterdam banking crisis of Bengal bubble crash — Crisis of Dutch Republic financial collapse c. An emergency may emerge during very cold winters due to increased consumption of energy. -

Money and the Economy

Chapter 9 Money and the Economy Nick Mayhew Historians have often underestimated the role of money in the medieval econo- my. There have been a number of different reasons for this. In the first place, the recognition of coin as money has long been overshadowed by an awareness of its role within a network of socio- political relationships, at least partially expressed by the giving and receiving of gifts. Although such gifts were by no means restrict- ed to offerings in coin, some scholars have felt that early medieval coins of the 6th to 8th centuries were more typically used as gifts rather than as an economic means of exchange. 1 From the 9th to the 13th centuries, the role of coin as money also seemed for some to be overshadowed by payments in kind and labour rents, which loomed large in the documentary evidence. The manuscript sources that mention coin are often somewhat ambiguous, speaking of silver or gold, but even explicit mention of specific sums of £- s- d is sometimes explained away as really meaning goods to that value, rather than actual coins.2 However, many scholars have been ready to accept references to the use of coin as money at face value. M.M. Postan, writing as early as 1944, cham- pioned an interpretation of coins as money, dismissing the notion that coins mentioned in the documents might not be real.3 It should be recognized that England, the principal focus of this chapter, is unusually rich in medieval doc- umentation. Yet those arguing for the reality of coin use there before the Nor- man conquest of 1066 have still encountered much resistance. -

Download Free at ISBN 978‑1‑909646‑73‑5 (PDF Edition) ISBN 978 1 905165 16 2 (Hardback Edition) Contents

Professor James L. Bolton (Photo: Tom Bolton, 2015) Medieval merchants and money Essays in honour of James L. Bolton Medieval merchants and money Essays in honour of James L. Bolton Edited by Martin Allen and Matthew Davies LONDON INSTITUTE OF HISTORICAL RESEARCH Published by UNIVERSITY OF LONDON SCHOOL OF ADVANCED STUDY INSTITUTE OF HISTORICAL RESEARCH Senate House, Malet Street, London WC1E 7HU First published in print in 2016. This book is published under a Creative Commons Attribution- NonCommercial-NoDerivatives 4.0 International (CC BY-NC-ND 4.0) license. More information regarding CC licenses is available at https://creativecommons.org/licenses/ Available to download free at http://www.humanities-digital-library.org ISBN 978-1-909646-73-5 (PDF edition) ISBN 978 1 905165 16 2 (hardback edition) Contents Preface ix List of contributors xiii List of figures and tables xvii List of abbreviations xix I. London merchants: companies, identities and culture 1. Negotiating merchant identities: the Stockfishmongers and London’s companies merging and dividing, c.1450–1550 3 Justin Colson 2. ‘Writying, making and engrocyng’: clerks, guilds and identity in late medieval London 21 Matthew Davies 3. What did medieval London merchants read? 43 Caroline M. Barron 4. ‘For quicke and deade memorie masses’: merchant piety in late medieval London 71 Christian Steer II. Warfare, trade and mobility 5. Fighting merchants 93 Sam Gibbs and Adrian R. Bell 6. London and its merchants in the Italian archives, 1380–1530 113 F. Guidi-Bruscoli 7. Settled or fleeting? London’s medieval immigrant community revisited 137 Jessica Lutkin III. Merchants and the English crown 8. -

The Quantity Theory of Money in Historical Perspective

A Service of Leibniz-Informationszentrum econstor Wirtschaft Leibniz Information Centre Make Your Publications Visible. zbw for Economics Graff, Michael Working Paper The quantity theory of money in historical perspective KOF Working Papers, No. 196 Provided in Cooperation with: KOF Swiss Economic Institute, ETH Zurich Suggested Citation: Graff, Michael (2008) : The quantity theory of money in historical perspective, KOF Working Papers, No. 196, ETH Zurich, KOF Swiss Economic Institute, Zurich, http://dx.doi.org/10.3929/ethz-a-005582276 This Version is available at: http://hdl.handle.net/10419/50322 Standard-Nutzungsbedingungen: Terms of use: Die Dokumente auf EconStor dürfen zu eigenen wissenschaftlichen Documents in EconStor may be saved and copied for your Zwecken und zum Privatgebrauch gespeichert und kopiert werden. personal and scholarly purposes. Sie dürfen die Dokumente nicht für öffentliche oder kommerzielle You are not to copy documents for public or commercial Zwecke vervielfältigen, öffentlich ausstellen, öffentlich zugänglich purposes, to exhibit the documents publicly, to make them machen, vertreiben oder anderweitig nutzen. publicly available on the internet, or to distribute or otherwise use the documents in public. Sofern die Verfasser die Dokumente unter Open-Content-Lizenzen (insbesondere CC-Lizenzen) zur Verfügung gestellt haben sollten, If the documents have been made available under an Open gelten abweichend von diesen Nutzungsbedingungen die in der dort Content Licence (especially Creative Commons Licences), you -

A Crisis of Credit in the Fifteenth Century, Or of Historical Interpretation?

A CRISIS OF CREDIT IN THE FIFTEENTH CENTURY, OR OF HISTORICAL INTERPRETATION? PAMELA NIGHTINGALE Introduction IN his Howard Linecar Lecture for 2009, published in this journal, and in his recent book, Money in the Medieval English Economy: 973–1489, Professor J.L. Bolton has raised questions about the money supply of fifteenth-century England which have led him to dispute that the century experienced either a shortage of money or a crisis of credit. He believes that although lack of silver coin might have caused temporary difficulties, English society found its way round the problem by creating viable forms of ‘paper money’, and consequently it ‘was not in the main a society held back by an inadequate money supply’.1 This is a surprising conclusion considering that even at its highest in the early fourteenth century, the medieval English cur- rency was scarcely adequate for the size of the economy, while in the course of the next century it plunged critically. At its nadir in the 1440s the mint’s combined output of gold and silver coin was only about five per cent of that struck in the 1420s, and according to Martin Allen’s esti- mates, the silver coin, which was the currency in everyday use, fell from c.56 pence per head in 1351, to c.13 pence in 1422, and by 1470 had risen only to c.33.6 pence.2 If the money supply was adequate for the needs of the economy one has to ask why the government should pass twenty-seven measures between 1390 and 1465 to conserve and increase the supply of bullion, and why falling prices, wages and rents were so widespread from the 1440s to the 1460s that John Hatcher has described the period as ‘the great slump’.3 Bolton allows that ‘shortages of coin due to bullion famines should be factored into any models of the fifteenth-century economy, to a much greater extent than they have been so far’, and he also concedes that ‘at times credit may have been squeezed by the bullion famines’.4 Nonetheless, he asserts that any crisis of credit ‘has been much exaggerated’, on the grounds, for which he claims M.M.