ENERGY INVESTMENTS for the FUTURE 2005 Annual Report CONTENTS

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Linguapax Review 2010 Linguapax Review 2010

LINGUAPAX REVIEW 2010 MATERIALS / 6 / MATERIALS Col·lecció Materials, 6 Linguapax Review 2010 Linguapax Review 2010 Col·lecció Materials, 6 Primera edició: febrer de 2011 Editat per: Amb el suport de : Coordinació editorial: Josep Cru i Lachman Khubchandani Traduccions a l’anglès: Kari Friedenson i Victoria Pounce Revisió dels textos originals en anglès: Kari Friedenson Revisió dels textos originals en francès: Alain Hidoine Disseny i maquetació: Monflorit Eddicions i Assessoraments, sl. ISBN: 978-84-15057-12-3 Els continguts d’aquesta publicació estan subjectes a una llicència de Reconeixe- ment-No comercial-Compartir 2.5 de Creative Commons. Se’n permet còpia, dis- tribució i comunicació pública sense ús comercial, sempre que se’n citi l’autoria i la distribució de les possibles obres derivades es faci amb una llicència igual a la que regula l’obra original. La llicència completa es pot consultar a: «http://creativecom- mons.org/licenses/by-nc-sa/2.5/es/deed.ca» LINGUAPAX REVIEW 2010 Centre UNESCO de Catalunya Barcelona, 2011 4 CONTENTS PRESENTATION Miquel Àngel Essomba 6 FOREWORD Josep Cru 8 1. THE HISTORY OF LINGUAPAX 1.1 Materials for a history of Linguapax 11 Fèlix Martí 1.2 The beginnings of Linguapax 14 Miquel Siguan 1.3 Les débuts du projet Linguapax et sa mise en place 17 au siège de l’UNESCO Joseph Poth 1.4 FIPLV and Linguapax: A Quasi-autobiographical 23 Account Denis Cunningham 1.5 Defending linguistic and cultural diversity 36 1.5 La defensa de la diversitat lingüística i cultural Fèlix Martí 2. GLIMPSES INTO THE WORLD’S LANGUAGES TODAY 2.1 Living together in a multilingual world. -

Phillips Petroleum Company 2001 Annual Report

Phillips Petroleum Company 2001 Annual Report NEW EXPECTATIONS PHILLIPS’ MISSION IS TO PROVIDE SUPERIOR RETURNS FOR SHAREHOLDERS THROUGH TOP PERFORMANCE IN ALL OUR BUSINESSES. PHILLIPS PETROLEUM CONTENTS COMPANY IN BRIEF 2 PHILLIPS’WORLDWIDE OPERATIONS Phillips Petroleum Company is a 4 LETTER TO SHAREHOLDERS major integrated U.S. oil and gas CEO Jim Mulva describes Phillips’ journey and explains why the company has company. It is headquartered in new expectations for increased shareholder returns. Bartlesville, Oklahoma. The company 7 THE CHAIRMAN’S PERSPECTIVE was founded in 1917. Phillips’ core Jim Mulva responds to questions about the company as it prepares to enter a new era. activities are: 9 FINANCIAL SUMMARY ■ Petroleum exploration and produc- Phillips remains financially strong despite a challenging economic climate. tion on a worldwide scale. 10 EXPLORATION AND PRODUCTION (E&P) ■ Petroleum refining, marketing and Phillips anticipates increased oil and gas output from existing projects, and is transportation, primarily in the carrying out a balanced and focused exploration program. United States. 18 REFINING, MARKETING AND TRANSPORTATION (RM&T) ■ Chemicals and plastics production Following its acquisition of Tosco, Phillips is capturing synergies and taking advantage and distribution worldwide through of its expanded capabilities as one of the largest U.S. refiners and marketers. a 50 percent interest in Chevron 24 CHEMICALS Phillips Chemical Company Chevron Phillips Chemical Company is weathering a difficult market, holding down (CPChem). costs and carrying out growth projects. ■ Natural gas gathering, processing 26 GAS GATHERING, PROCESSING AND MARKETING and marketing in North America Phillips’ midstream joint venture is making the most of its strengths while through a 30.3 percent interest in pursuing growth opportunities. -

Petroleum News 082904

page Bear rule stays: Salazar decides not 5 to revoke Bush-era special ESA rule Vol. 14, No. 20 • www.PetroleumNews.com A weekly oil & gas newspaper based in Anchorage, Alaska Week of May 17, 2009 • $2 Drilling at Point Thomson NATURAL GAS Chugach contract Following nearly five years of looking, Chugach Electric gets a gas supply COURTESY EXXONMOBIL COURTESY By ERIC LIDJI The proposed contract gives Chugach all Petroleum News the gas it needs through 2010, but leaves hugach Electric Association filed a supply the utility with about one-third of its 2011 Ccontract with state regulators on May 12 to needs and half of its 2012 needs buy some 66 billion cubic feet of gas from unaccounted for. The Point Thomson pad in early May, with drilling progressing on ConocoPhillips over the next seven years. the PTU 15 well; ExxonMobil will drill to 5,000 feet, then drill PTU 16 to the same depth. Drilling into hydrocarbon-bearing zones on the The contract is the result of nearly five years of gas needs in 2016. coast is limited to Nov. 1 through April 15; drilling will resume in solicitations and negotiations, and is the first long- Chugach supplies electricity directly to most of December-January. See story page 10. term gas supply agreement filed by the electric Anchorage, and indirectly to homes and business- utility in more than 20 years. es throughout the Railbelt region that runs from Alberta cleans up royalty house; Under the proposed contract, ConocoPhillips Homer to Fairbanks. would provide 100 percent of Chugach’s unmet About 90 percent of the new gas volumes will Alyeska wins operator award; gas needs through April 2011, about half of its be priced using a “Production Area Composite JPO moving; Foothills road unmet gas needs between June 2011 and December 2015, and about 25 percent of its unmet studies this summer see CONTRACT page 19 WHATEVER ALBERTA’S OIL AND GAS PRODUCERS NATURAL GAS think of the province’s new royalty scheme — and the displeas- ure is close to universal — Alberta Auditor-General Fred Dunn isn’t about to give them a break. -

11 January 2002 O Fficial Opening of Dialog's First Projet Station in Kajang, Selangor by Mr. Jim Nokes, the Executive Vice Pr

Annual Report 2002 Laporan Ta h u n a n 65 Calendar of Events ( c o n t i n u e d ) Kalendar Peristiwa ( s a m b u n g a n ) 11 January 2002 O fficial opening of Dialog’s first ProJET station in Kajang, Selangor by Mr. Jim Nokes, the Executive Vice President, Refining, Marketing, Supply and Transportation of CONOCO I n c . 11 Januari 2002 Pembukaan rasmi stesyen minyak ProJET Dialog yang pertama di Kajang, Selangor oleh Encik Jim Nokes, Naib Presiden Eksekutif, Penapisan, Pemasaran, Pembekalan dan Pengangkutan, CONOCO Inc. 12 January 2002 Hari Raya Open House at Kelab Golf Perkhidmatan Awam Malaysia, Bukit Kiara, Kuala L u m p u r. 12 Januari 2002 Rumah Terbuka Hari Raya di Kelab Golf Perkhidmatan Awam Malaysia, Bukit Kiara, Kuala Lumpur. 27 February 2002 Citation from Kertih Terminals Sdn Bhd for the successful completion of Kertih Centralised Tankage Facility Project and 5.53 million manhours without lost time incident by its Chief Executive Off i c e r, Mr. Eric S A r n o l d . 27 Februari 2002 Penerimaan sijil penghargaan dari Kertih Terminals Sdn Bhd (KTSB) di atas kejayaan menyiapkan Projek Kemudahan Tangki Berpusat Kertih dan catatan 5.53 juta jumlah jam kerja tanpa kemalangan. KTSB telah diwakili oleh Ketua Pegawai Eksekutif, Encik Eric S A r n o l d . 9 - 10 March 2002 Sales Carnival at Dialog’s first ProJET station, Kajang, Selangor to celebrate its of f i c i a l o p e n i n g . 9 - 10 Mac 2002 Karnival Jualan di stesyen minyak ProJET Dialog yang pertama di Kajang, Selangor untuk meraikan pembukaan rasminya. -

Fact Book Fact

FACT BOOK FACT ConocoPhillips Fact Book About the Cover As the world’s need for energy continues to expand, ConocoPhillips is growing to meet that need with a portfolio of new investments. (On the cover, left to right) Announced in 2005, the company will begin a multi-year, domestic refining investment program designed to create an integrated advantage through its existing assets, such as the Borger, Texas, refinery. In the Timor Sea, the Bayu-Undan project was advanced with the connection of a natural gas pipeline from the offshore facilities to the liquefied natural gas facility near Darwin, Australia. The Burlington Resources acquisition, including major producing fields in Canada, has expanded ConocoPhillips’ presence in North America through high-quality, long-life reserves and assets. Through the dedication of the company’s solid work force, these and other projects will provide sustainable shareholder value well into the future. ConocoPhillips Key Assets, Operations and Locations As of March 31, 2006, unless noted otherwise. Third-largest integrated energy company in the United States. Fifth-largest proved reserves holder worldwide.* Fourth-largest refiner worldwide,* second-largest in the United States. About 38,000 employees worldwide.** 1,808 active patents in about 70 countries. *Of nongovernment-controlled companies. **Based on the Annual Reports on Form 10-K of ConocoPhillips and Burlington Resources for the year ended Dec. 31, 2005. Worldwide Locations Branded Marketing 2005 Worldwide Production Algeria Hungary Saudi Arabia -

E L E V a T E Expectations

elevateexpectations 2002 Annual Report Contents ConocoPhillips At A Glance . .2 A review of the company’s global operations. Letter to Shareholders . .5 Chairman Archie Dunham and President and CEO Jim Mulva discuss the company’s strategy for improving returns to shareholders. An Interview with Jim Mulva . .8 President and CEO Jim Mulva answers shareholders’ questions. Operating Review . .10 ConocoPhillips’ operating groups are capturing merger synergies while building on a portfolio of world-class assets. Corporate Review . .30 Corporate staffs are essential to helping ConocoPhillips achieve its objectives while supporting the company’s values and purpose. Financial Review . .36 Directors and Officers . .106 Glossary . .108 Our Theme: Elevate Expectations The PL19-3A wellhead platform rises high above the waters of China’s Bohai Bay, where ConocoPhillips announced first production from the Peng Lai field in late 2002. Like the platform reaching skyward, ConocoPhillips seeks to elevate expectations for performance beyond what was possible before the merger. The company is pursuing a clear strategy to improve returns for its shareholders — by capturing merger-related synergies, selling billions of dollars of non-core assets, growing its Exploration and Production segment, and applying a disciplined approach to cost control, capital spending and debt reduction. Highlights Millions of Dollars Except as Indicated 2002 2001 % Change Financial Total revenues $57,224 25,044 128 Income from continuing operations $ 714 1,611 (56) Net income (loss) -

73247 CVRS E:Layout 1

TransCanada Keystone Pipeline GP Ltd. Keystone XL Pipeline Section 52 Application Section 4: Financing, Appendix 4-9 Page 1 of 60 APPENDIX 4-9 2007 CONOCOPHILLIPS ANNUAL REPORT ConocoPhillips 2007 Annual Report www.conocophillips.com 2007 Annual Report Delivering Energy. Building Value. FinancialFinancial Highlights Highlights . .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. 1. .1 CorporateCorporate Staffs Staffs . .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. 24. .24 WorldwideWorldwide Operations Operations . .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. 2. .2 FinancialFinancial and andOperating Operating Results Results . .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. 28. .28 LetterLetter to Shareholders to Shareholders . .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. 4. .4 DirectorsDirectors and andOfficers Officers . .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. 110. .110 FinancialFinancial Review Review . .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. 8. .8 GlossaryGlossary . .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. 112. .112 Financial Highlights OperatingOperating Review Review . .. .. .. .. .. .. .. . -

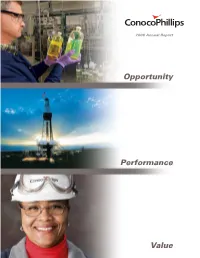

Opportunity Performance Value

2006 Annual Report Opportunity Performance Value Financial Highlights 1 Worldwide Operations 2 Letter to Shareholders 4 Financial Review 8 Operating Review 10 Corporate Staffs 24 Financial and Operating Results 30 Directors and Officers 112 Glossary 114 Our Theme: Who We Are 2006 Annual Report Opportunity — A high-quality ConocoPhillips is an international, integrated energy Opportunity portfolio of existing assets, company. It is the third-largest integrated energy promising major projects under company in the United States, based on market development worldwide, and capitalization, and oil and natural gas proved reserves investment in numerous new and production; and the second-largest refiner in Performance emerging businesses ensures the United States. Worldwide, of non-government- an opportunity-rich future for controlled companies, ConocoPhillips is the sixth- ConocoPhillips. Renewable largest proved reserves holder and the fifth-largest diesel fuel represents one such refiner. Value opportunity. Garry Bush ConocoPhillips is known worldwide for its (featured in the top photo) technological expertise in exploration and production, works with a team at the company’s Bartlesville, Okla., reservoir management and exploitation, 3-D seismic research facility to further the production and marketing technology, high-grade petroleum coke upgrading of renewable fuels in the United States. The company’s and sulfur removal. renewable diesel fuel technology is already in use in Europe. Headquartered in Houston, Texas, ConocoPhillips operates in more than 40 countries. The company Performance — Strong, reliable operating performance, has 38,400 employees worldwide and assets of delivered in a safe and environmentally responsible $165 billion. ConocoPhillips’ stock is listed on the manner, is paramount to ConocoPhillips’ success. -

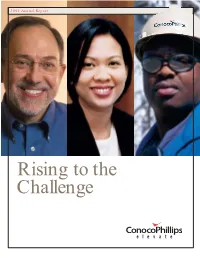

2004 Annual Report 2004 Annual Report

ConocoPhillips 2004 Annual Report 2004 Annual Report Rising to the Challenge www.conocophillips.com Contents Financial Highlights 1 Our purpose is to use our pioneering spirit to responsibly deliver energy to the world. Worldwide Operations 2 Letter to Shareholders 4 Who We Are Operating Review 8 ConocoPhillips is an international, integrated energy Corporate Review 24 company. It is the third-largest integrated energy company in the United States, based on market Financial Review 30 capitalization, and oil and gas proved reserves and Directors and Officers 110 production; and the largest refiner in the United Glossary 112 States. Worldwide, of nongovernment-controlled companies, ConocoPhillips has the eighth-largest total of proved reserves and is the fifth-largest refiner. ConocoPhillips is known worldwide for its technological expertise in exploration and production, reservoir management and exploitation, 3-D seismic technology, high-grade petroleum coke upgrading, and sulfur removal. Headquartered in Houston, Texas, ConocoPhillips operates in more than 40 countries. The company has approximately 35,800 employees worldwide and assets of $93 billion. ConocoPhillips’stock is listed on the New York Stock Exchange under the symbol “COP.” Our Theme: Rising to the Challenge Our Businesses The company has four core activities worldwide: • Petroleum exploration and production. • Petroleum refining, marketing, supply and transportation. • Natural gas gathering, processing and marketing, including a 30.3 percent interest in Duke Energy Each day, employees in ConocoPhillips’ business units around the world make tangible contributions, which Field Services, LLC. elevate the company to new levels of performance. They rise to the challenge of increasing shareholder • Chemicals and plastics production and distribution value by keeping the company’s assets and systems through a 50 percent interest in Chevron Phillips operational, safe, environmentally sound, on the Chemical Company LLC. -

2003 Cp Annual.Qxd

buildingbuilding momentummomentum 2003 Annual Report Our Purpose Use Our Pioneering Spirit to Responsibly Deliver Energy to the World Who We Are Contents ConocoPhillips is an international, integrated energy company. It is the ConocoPhillips’ Worldwide Operations . .2 third-largest integrated energy company in the United States, based on market Letter to Shareholders . .4 capitalization, oil and gas proved Chairman Archie Dunham and President and CEO Jim Mulva reserves and production; and the largest discuss the factors behind the company’s success in 2003. refiner in the United States. Worldwide, of nongovernment-controlled companies, ConocoPhillips has the An Interview with President and CEO Jim Mulva . .8 eighth-largest total of proved reserves and is the fourth largest refiner. Operating Review . .10 ConocoPhillips is known worldwide ConocoPhillips’ operating groups are focused on controlling costs, for its technological expertise in running well and developing projects that will support the exploration and production, reservoir company’s future growth. management and exploitation, liquefied natural gas, 3-D seismic technology, Corporate Review . .28 high-grade petroleum coke upgrading, The corporate staffs played key roles in the company’s strong and sulfur removal. financial and operating performance in 2003. Headquartered in Houston, Texas, ConocoPhillips operates in more than 40 countries. The company has Financial Review . .35 approximately 39,000 employees worldwide and assets of $82.5 billion. Directors and Officers . .110 ConocoPhillips stock is listed on the New York Stock Exchange under the Glossary . .112 symbol “COP.” Our Businesses The company has four core activities worldwide: ■ Petroleum exploration and production. Our Theme: Building Momentum ■ Petroleum refining, marketing, supply A ship steaming through the open ocean and transportation. -

Putrajaya Ou Une Utopie Malaisienne. Projet Urbain Et Défi Politique Putrajaya Or a Malaysian Utopia

Bulletin de l’association de géographes français Géographies 91-4 | 2014 Dynamiques urbaines en Asie du Sud-Est Putrajaya ou une utopie malaisienne. Projet urbain et défi politique Putrajaya or a Malaysian utopia. Urban project and political challenge Frédéric Bouchon Édition électronique URL : http://journals.openedition.org/bagf/1543 DOI : 10.4000/bagf.1543 ISSN : 2275-5195 Éditeur Association AGF Édition imprimée Date de publication : 15 décembre 2014 Pagination : 500-522 ISSN : 0004-5322 Référence électronique Frédéric Bouchon, « Putrajaya ou une utopie malaisienne. Projet urbain et défi politique », Bulletin de l’association de géographes français [En ligne], 91-4 | 2014, mis en ligne le 22 janvier 2018, consulté le 20 avril 2019. URL : http://journals.openedition.org/bagf/1543 ; DOI : 10.4000/bagf.1543 Bulletin de l’association de géographes français Putrajaya ou une utopie malaisienne. Projet urbain et défi politique (PUTRAJAYA OR A MALYSIAN UTOPIA. URBAN PROJECT AND POLITICAL CHALLENGE) Frédéric BOUCHON * RÉSUMÉ – La construction d’une nouvelle capitale s’annonce comme un élément majeur, voire fondateur d’une nation. Le projet de Putrajaya en Malaisie s’est inspiré de modèles postcoloniaux comme Brasilia ou Chandigarh, afin d’exprimer dans l’espace la vision du futur de la société malaisienne. Elle s’annonce ostensiblement en rupture avec la morphologie chaotique et l’essence multiple de Kuala Lumpur. Elle en est le satellite, mais c’est un projet urbain et de transformation technologique ambitieux. La capitale fédérale présente une morphologie au parti-pris moderniste monumental et à l’esthétique d’inspiration islamo-malaise. Vingt ans après le choix du site, entre Kuala Lumpur et son aéroport, la ville compte aujourd'hui plus de cent mille habitants. -

In the Matter of a Trade Mark Application No. 15413/97 by Cocon Food Industries Sdn Bhd

In The Matter Of A Trade Mark Application No. 15413/97 By Cocon Food Industries Sdn Bhd And Objection Thereto By Conoco, Inc. Before Principal Assistant Registrar P Arul Selvamalar 30 April 2003 Trade Mark Application– Opposition – whether Opponents had international reputation - whether reputation extends to Singapore – whether the marks were confusingly similar - Trade Marks Act (Cap. 332, 1992 Ed) section 12 and 15 Procedure - Opponents required to state all grounds in Notice of Opposition - Opponents required to state details of mark in Notice of Opposition - Trade Mark Rules 1998, rule 30 Facts The Applicants are Cocon Food Industries Sdn Bhd, who applied for registration of a trade mark, which comprised the word “COCON” in a capsule device, for the goods “Desserts, milky desserts, snack foods, jellies and fruit jellies” in class 29. Their application was accepted for registration and advertised. The Opponents are Conoco Inc., a major energy producer for 125 years. The Opponents have been using a mark which comprises the word “CONOCO” in a capsule device, and had registrations in classes 4, 37 and 42. In 2002, after the Applicants made a statement in their Statutory Declaration that the Opponents were not interested in food products, the Opponents filed an application for food products in class 30. The Opponents’ petrol stations in Europe and Thailand used the mark “JET” and their petrol stations in Malaysia used the mark “ProJET”. The mark CONOCO appeared on the billboards outside the petrol stations below the marks JET and ProJET. The mark CONOCO is used in the United States of America on food products sold from their petrol station convenience stores and/or petrol stations.