Mining in Africa's Copperbelt

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

FROM COERCION to COMPENSATION INSTITUTIONAL RESPONSES to LABOUR SCARCITY in the CENTRAL AFRICAN COPPERBELT African Economic

FROM COERCION TO COMPENSATION INSTITUTIONAL RESPONSES TO LABOUR SCARCITY IN THE CENTRAL AFRICAN COPPERBELT African economic history working paper series No. 24/2016 Dacil Juif, Wageningen University [email protected] Ewout Frankema, Wageniningen University [email protected] 1 ISBN 978-91-981477-9-7 AEHN working papers are circulated for discussion and comment purposes. The papers have not been peer reviewed, but published at the discretion of the AEHN committee. The African Economic History Network is funded by Riksbankens Jubileumsfond, Sweden 2 From Coercion to Compensation Institutional responses to labour scarcity in the Central African Copperbelt* Dácil Juif, Wageningen University Ewout Frankema, Wageningen University Abstract There is a tight historical connection between endemic labour scarcity and the rise of coercive labour market institutions in former African colonies. This paper explores how mining companies in the Belgian Congo and Northern Rhodesia secured scarce supplies of African labour, by combining coercive labour recruitment practices with considerable investments in living standard improvements. By reconstructing internationally comparable real wages we show that copper mine workers lived at barebones subsistence in the 1910s-1920s, but experienced rapid welfare gains from the mid-1920s onwards, to become among the best paid manual labourers in Sub-Saharan Africa from the 1940s onwards. We investigate how labour stabilization programs raised welfare conditions of mining worker families (e.g. medical care, education, housing quality) in the Congo, and why these welfare programs were more hesitantly adopted in Northern Rhodesia. By showing how solutions to labour scarcity varied across space and time we stress the need for dynamic conceptualizations of colonial institutions, as a counterweight to their oft supposed persistence in the historical economics literature. -

The Profitable and Untethered March to Global Resource Dominance!

Athens Journal of Business and Economics X Y GlencoreXstrata… The Profitable and Untethered March to Global Resource Dominance! By Nina Aversano Titos Ritsatos† Motivated by the economic causes and effects of their merger in 2013, we study the expansion strategy deployment of Glencore International plc. and Xstrata plc., before and after their merger. While both companies went through a series of international acquisitions during the last decade, their merger is strengthening effective vertical integration in critical resource and commodity markets, following Hymer’s theory of internationalization and Dunning’s theory of Eclectic Paradigm. Private existence of global dominant positioning in vital resource markets, posits economic sustainability and social fairness questions on an international scale. Glencore is alleged to have used unethical business tactics, increasing corruption, tax evasion and money laundering, while attracting the attention of human rights organizations. Since the announcement of their intended merger, the company’s market performance has been lower than its benchmark index. Glencore’s and Xstrata’s economic success came from operating effectively and efficiently in markets that scare off risk-averse companies. The new GlencoreXstrata is not the same company anymore. The Company’s new capital structure is characterized by controlling presence of institutional investors, creating adherence to corporate governance and increased monitoring and transparency. Furthermore, when multinational corporations like GlencoreXstrata increase in size attracting the attention of global regulation, they are forced by institutional monitoring to increase social consciousness. When ensuring full commitment to social consciousness acting with utmost concern with regard to their commitment by upholding rules and regulations of their home or host country, they have but to become “quasi-utilities” for the global industry. -

EIGHTH REPORT for the Fiscal Year Ended 31 December 2015

EIGHTH REPORT For the fiscal year ended 31 December 2015 4 Contents 1. INTRODUCTION .............................................................................................................................7 1.1 Background ........................................................................................................................................................ 7 1.2 Objectives........................................................................................................................................................... 7 1.3 Nature of our work ............................................................................................................................................. 7 2. EXECUTIVE SUMMARY ...................................................................................................................9 2.1 Revenue Generated from the Extractive Sector ............................................................................................... 9 2.2 Analysis of Production and Exports ............................................................................................................... 11 2.3 Scope of the reconciliation .............................................................................................................................. 14 2.4 Completeness and Accuracy of Information ................................................................................................. 15 2.5 Reconciliation of Financial Flows.................................................................................................................. -

Kabwe, Zambia

Mortimer Hays-Brandeis Traveling Fellowship Final Report, Hrvoje Slovene House Secrets: Industrial Tales in one of the World's Most Contaminated Cities: Kabwe, Zambia For the past five years, my primary focus in photography has been to document abandoned, nineteenth-century factories and industrial spaces, as well as to show the irreparable damage modem industrialism has had on the global environment and its population. By photographing the devastating effects on local neighborhoods wrought by factories and industry, my intention has been to show how seemingly isolated problems have contributed to the global environmental crisis we are witnessing today. To date this project has taken me to Manchester, England-the birthplace of the industrial revolution; to Cleveland, Ohio; and Zagreb, Croatia. With the generous help of the Mortimer Hays- Brandeis Traveling Fellowship, I expanded this project to include Kabwe, Zambia. The mining of lead there by a Chinese-based company continues to put the population of hundreds of thousands at serious risk. Through my photographs, I showed the impact of modem industrialism on the real, day-to-day experiences of people and their industrialized habitats. Although my original intention was to visit and document the effects oflead pollution in Kabwe, Zambia; Linfen, China; and Dzerzhinsk, Russia, I found a plethora of material in Zambia, and spent the majority of my time there. I first visited Kabwe in June 2007 and stayed there for three months. During that time I got in touch with local NGOs and familiarized myself with their work on the field. During that time I also became aware of the scale of the lead pollution problem on the location. -

Zambia Mining and Public Health Mtg Rep April2018.Pdf

MINING AND PUBLIC HEALTH IN ZAMBIA MEETING REPORT C Mwansa 2018 Ministry of Health, Zambia in collaboration with the Regional Network for Equity in Health in East and Southern Africa (EQUINET) SBH Centre, Lusaka, Zambia April 10 2018 Contents 1. Background and objectives ....................................................................... 2 2. Opening session ....................................................................................... 3 3. Presentations from Zambia ....................................................................... 4 3.1 Mining and public health in Zambia ............................................................ 4 3.2 Survey findings on mining, TB and health in Zambia.................................. 5 3.3 Lead poisoning in Kabwe ........................................................................... 6 4. Mining and health: A regional perspective ................................................ 7 5. Discussions............................................................................................... 9 5.1 Discussion on public health and mining in Zambia ..................................... 9 5.2 Discussion on regional standards and co-operation ................................. 10 6. Recommendations .................................................................................. 11 7. Closing .................................................................................................... 12 Appendix 1: Programme ............................................................................... -

Fifty Years of the Kasempa District, Zambia 1964 – 2014 Change and Continuity

FIFTY YEARS OF THE KASEMPA DISTRICT, ZAMBIA 1964 – 2014 CHANGE AND CONTINUITY. A case study of the ups and downs within a remote rural Zambian region during the fifty years since Independence. A descriptive analysis of its demography, geography, infrastructure, agricultural practice and present and traditional cultural aspects, including an account on the traditional ceremony of the installation of regional Headmen and the role and functions of the Kaonde clan structure. Dick Jaeger, 2015 [email protected] TABLE OF CONTENTS LIST OF MAPS AND FIGURES...........................................................................................................3 PART I 4 PREFACE – A WORD OF THANKS.....................................................................................................4 INTRODUCTION AND SUMMARY......................................................................................................6 CHAPTER 1. DEMOGRAPHIC CHANGES.......................................................................................10 ZAMBIA.............................................................................................................................10 KASEMPA DISTRICT........................................................................................................10 CHAPTER 2. AGRICULTURE............................................................................................................12 INTRODUCTION...............................................................................................................12 -

Research Report

Research Report Large-scale land acquisitions in Zambia: Evidence to inform policy Jessica Chu and Dimuna Phiri PLAAS Institute for Poverty, Land and Agrarian Studies School of Government • EMS Faculty Research Report Research Report Large-scale land acquisitions in Zambia: Evidence to inform policy Jessica Chu and Dimuna Phiri June 2015 PLAAS Institute for Poverty, Land and Agrarian Studies School of Government • EMS Faculty iii Research Report 50 Large-Scale Land Acquisitions in Zambia: Evidence to inform policy Published by the Institute of Poverty, Land and Agrarian Studies, Faculty of Economic and Management Sciences, University of the Western Cape, Private Bag X17, Bellville 7535, Cape Town, South Africa Tel: +27 21 959 3733 Fax: +27 21 959 3732 Email: [email protected] Institute for Poverty, Land and Agrarian Studies Research Report no. 50 June 2015 All rights reserved. No part of this publication may be reproduced or transmitted in any form or by any means without prior permission from the publisher or the authors. Copy Editor: Glynne Newlands Proof reader: Jennifer Leak Series Editor: Rebecca Pointer Photographs: Darlene Miller Design & Layout: Design for development Typeset in Frutiger Thanks to the Austrian Development Cooperation for supporting this project. Research Report Contents Acronyms v Executive summary 1 1 Introduction 7 2 Methodology 9 3 Background 10 4 Case studies 12 5 Findings and discussion 19 6 Lessons learned 27 7 Conclusion 35 8 Bibliography and sources 37 Large-Scale Land Acquisitions in Zambia: Evidence to -

A History of Mining in Broken Hill (Kabwe): 1902-1929 Buzandi Mufinda

A HISTORY OF MINING IN BROKEN HILL (KABWE): 1902-1929 BY BUZANDI MUFINDA THIS THESIS HAS BEEN SUBMITTED IN ACCORDANCE WITH THE REQUIREMENTS FOR THE DEGREE OF MASTER OF ARTS IN THE FACULTY OF THE HUMANITIES, FOR THE CENTRE FOR AFRICA STUDIES AT THE UNIVERSITY OF THE FREE STATE. FEBRUARY 2015 SUPERVISOR: PROF. I.R. PHIMISTER CO-SUPERVISOR: DR L. KOORTS DECLARATION I declare that the dissertation hereby submitted by me for the Master of Arts degree at the University of the Free State is my own independent work and has not previously been submitted by me at another university/faculty. I furthermore cede copyright of the dissertation in favour of the University of the Free State. Buzandi Mufinda i DEDICATION I dedicate this work to the memory of my late parents, Edward Mufinda, and Rosemary Mufinda, and to my niece Chipego Munene and hope one day she might follow in the footsteps of academia. ii ACKNOWLEDGEMENTS Glory is to the enabling power of the Almighty God whose hand has worked through many ways to make it possible for me to accomplish this study. I would like to express my sincere appreciation to my supervisor, Professor Ian Phimister, for the patient guidance, encouragement and advice he has provided throughout my time as his student. I have been extremely lucky to have a supervisor who cared so much about my work, and who responded to my questions and queries so promptly. To Doctor Lindie Koorts, your expertise in structuring and editing of this work continually amazed me. Thank you also for your moral support. -

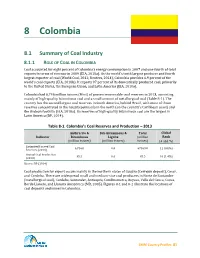

Chapter 8: Colombia

8 Colombia 8.1 Summary of Coal Industry 8.1.1 ROLE OF COAL IN COLOMBIA Coal accounted for eight percent of Colombia’s energy consumption in 2007 and one-fourth of total exports in terms of revenue in 2009 (EIA, 2010a). As the world’s tenth largest producer and fourth largest exporter of coal (World Coal, 2012; Reuters, 2014), Colombia provides 6.9 percent of the world’s coal exports (EIA, 2010b). It exports 97 percent of its domestically produced coal, primarily to the United States, the European Union, and Latin America (EIA, 2010a). Colombia had 6,746 million tonnes (Mmt) of proven recoverable coal reserves in 2013, consisting mainly of high-quality bituminous coal and a small amount of metallurgical coal (Table 8-1). The country has the second largest coal reserves in South America, behind Brazil, with most of those reserves concentrated in the Guajira peninsula in the north (on the country’s Caribbean coast) and the Andean foothills (EIA, 2010a). Its reserves of high-quality bituminous coal are the largest in Latin America (BP, 2014). Table 8-1. Colombia’s Coal Reserves and Production – 2013 Anthracite & Sub-bituminous & Total Global Indicator Bituminous Lignite (million Rank (million tonnes) (million tonnes) tonnes) (# and %) Estimated Proved Coal 6,746.0 0.0 67469.0 11 (0.8%) Reserves (2013) Annual Coal Production 85.5 0.0 85.5 10 (1.4%) (2013) Source: BP (2014) Coal production for export occurs mainly in the northern states of Guajira (Cerrejón deposit), Cesar, and Cordoba. There are widespread small and medium-size coal producers in Norte de Santander (metallurgical coal), Cordoba, Santander, Antioquia, Cundinamarca, Boyaca, Valle del Cauca, Cauca, Borde Llanero, and Llanura Amazónica (MB, 2005). -

Introduction - the Trident Project

Introduction - The Trident Project January 2014 www.first-quantum.com TSX: FM LSE: FQM LuSE: FQMZ TRIDENT PROJECT LOCATION January 2014 2 ABOUT THE TRIDENT PROJECT Trident Project: . Located in the Solwezi District of Northwestern Province, Zambia . Approximately 150km from Solwezi on the T5 main road to Mwinilunga . Comprises five prospecting large scale licences . A number of attractive base metal prospects including the Sentinel deposit and the Enterprise deposit . 5 x large-scale mining licences awarded 20 April 2011 for 25 years tenure . Land use agreement signed 14 July 2011 . EIA approved 8 July 2011 and Addendum 12 August 2013 . Resettlement Action Plan approved 15 October 2013 January 2014 3 TRIDENT PROJECT LAYOUT January 2014 4 SENTINEL MINE IN CONSTRUCTION – COMMISSIONING MID 2014 Updated resource published May 2012: . 514 boreholes for 172,692m defined an NI43-101 resource of: . Total measured & indicated : 1,027Mt @ 0.51% Cu . Inferred : 165Mt @ 0.42% Cu . Cut-off : 0.2% Cu . Mineral Reserve: 774 Mt @ 0.50% Cu . Proved : 476 Mt @ 0.52% Cu . Probable : 298 Mt @ 0.47%Cu. Strip ratio 2.2 : 1 Mine planning: . Grade of 0.5% Cu requires a high throughput of 55 Mtpa to achieve production target of 280 – 300,000t Cu per annum. Sentinel will put Zambia at the forefront of global mining technology January 2014 5 ENTERPRISE MINE IN APPROVAL – EARLY WORKS UNDERWAY Maiden resource published December 2012: . 359 boreholes for 116,000m defined an NI43-101 resource of: . Total measured indicated : 40.1Mt @ 1.07% Ni . Inferred : 7.1Mt @ 0.70% Ni . Cutoff : 0.15% Ni . -

Profiles of Active Civil Society Organisations in North-Western, Copperbelt and Southern Provinces of Zambia

Profiles of Active Civil Society Organisations in North-Western, Copperbelt and Southern Provinces of Zambia On behalf of Implemented by Published by: Deutsche Gesellschaft für Internationale Zusammenarbeit (GIZ) GmbH Registered offices Bonn and Eschborn, Germany Address Civil Society Participation Programme (CSPP) Mpile Office Park, 3rd floor 74 Independence Avenue Lusaka, Zambia P +260 211 250 894 E [email protected] I www.giz.de/en Programme: Civil society participation in governance reform and poverty reduction Author: Isaac Ngoma, GFA Consulting Group GmbH Editor: Markus Zwenke, GFA Consulting Group GmbH, Eulenkrugstraße 82, 22359 Hamburg, Germany Design/layout: GFA Consulting Group GmbH and IE Zhdanovich Photo credits/sources: GFA Consulting Group GmbH On behalf of German Federal Ministry for Economic Cooperation and Development (BMZ) As of June, 2021 TABLE OF CONTENT ACTIVE CIVIL SOCIETY ORGANISATIONS IN NORTH-WESTERN PROVINCE � � � � � �7 Dream Achievers Academy �������������������������������������������������������������������������������������������������������������������������� 8 Anti-voter Apathy Project ���������������������������������������������������������������������������������������������������������������������������� 9 Mentra Youth Zambia . 10 The Africa Youth Initiative Network �������������������������������������������������������������������������������������������������������� 11 Radio Kabangabanga ���������������������������������������������������������������������������������������������������������������������������������� -

Copper for Development Report 2021

2021 COPPER FOR DEVELOPMENT REPORT 2 COPPER FOR DEVELOPMENT REPORT Contents List of tables ii List of figures ii Acknowledgements iii List of Abbreviations iv Executive Summary v 1 Introduction 1 1.1 Study Objectives 1 1.2 Overview of Methodology 1 2 Zambia’s Macroeconomic Context 2 2.1 Mining Economic Contribution 2 2.1.1 Contribution to GDP 3 2.1.2 Contribution to International Trade 3 2.1.3 Contribution to Domestic Revenues 5 2.1.4 Contribution to Employment 5 3 Legal and Institutional Framework 5 3.1 The Significance of a Legal and Institutional Framework in the Extractive Sector 5 4 Expenditure in the Priority Sectors (Health, Education and Agriculture) 8 5 Copper Revenue Management at Subnational Level in Zambia 10 5.1 The Transfer of Mining Revenues at Local Government Level 10 5.1.1 Findings from Key Informant interviews with Local Authorities 13 5.2 The role of Chiefs in Mineral Revenue Management 15 5.2.1 Key Informant Interviews with Chiefs 15 5.3 Analysis of Subnational Transfers 17 5.4 Rationale for mineral revenue sharing mechanism 18 6 Case Studies of Mineral Revenue Sharing Mechanisms in Selected African countries 20 6.1 Mineral Revenue Sharing Mechanism in Ghana 20 6.1.1 Challenges of Mineral Revenue Sharing in Ghana 20 6.2 Mineral Revenue Sharing Mechanism in Botswana 6.2.1 The Role of Mineral Revenue in Botswana 21 6.2.2 Lessons from Botswana’s Mineral Revenue Management “Mechanism” 22 7 Conclusion and Recommendations 22 7.1 Main Findings 22 7.1.1 Mining Sector Specific Findings 22 7.1.2.