Project Document

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

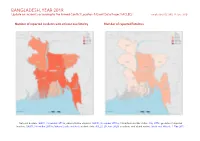

Bangladesh, Year 2019: Update on Incidents According to the Armed Conflict Location & Event Data Project (ACLED)

BANGLADESH, YEAR 2019: Update on incidents according to the Armed Conflict Location & Event Data Project (ACLED) compiled by ACCORD, 29 June 2020 Number of reported incidents with at least one fatality Number of reported fatalities National borders: GADM, November 2015b; administrative divisions: GADM, November 2015a; China/India border status: CIA, 2006; geodata of disputed borders: GADM, November 2015b; Natural Earth, undated; incident data: ACLED, 20 June 2020; coastlines and inland waters: Smith and Wessel, 1 May 2015 BANGLADESH, YEAR 2019: UPDATE ON INCIDENTS ACCORDING TO THE ARMED CONFLICT LOCATION & EVENT DATA PROJECT (ACLED) COMPILED BY ACCORD, 29 JUNE 2020 Contents Conflict incidents by category Number of Number of reported fatalities 1 Number of Number of Category incidents with at incidents fatalities Number of reported incidents with at least one fatality 1 least one fatality Protests 930 1 1 Conflict incidents by category 2 Riots 405 107 122 Development of conflict incidents from 2010 to 2019 2 Violence against civilians 257 184 195 Battles 99 43 63 Methodology 3 Strategic developments 15 0 0 Conflict incidents per province 4 Explosions / Remote 7 2 2 violence Localization of conflict incidents 4 Total 1713 337 383 Disclaimer 6 This table is based on data from ACLED (datasets used: ACLED, 20 June 2020). Development of conflict incidents from 2010 to 2019 This graph is based on data from ACLED (datasets used: ACLED, 20 June 2020). 2 BANGLADESH, YEAR 2019: UPDATE ON INCIDENTS ACCORDING TO THE ARMED CONFLICT LOCATION & EVENT DATA PROJECT (ACLED) COMPILED BY ACCORD, 29 JUNE 2020 Methodology GADM. Incidents that could not be located are ignored. -

Development Coordination

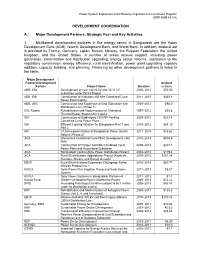

Power System Expansion and Efficiency Improvement Investment Program (RRP BAN 42378) DEVELOPMENT COORDINATION A. Major Development Partners: Strategic Foci and Key Activities 1. Multilateral development partners in the energy sector in Bangladesh are the Asian Development Bank (ADB), Islamic Development Bank, and World Bank. In addition, bilateral aid is provided by France, Germany, Japan, Kuwait, Norway, the Russian Federation, the United Kingdom, and the United States. A number of areas receive support, including power generation, transmission and distribution upgrading, energy sector reforms, assistance to the regulatory commission, energy efficiency, rural electrification, power plant upgrading capacity addition, capacity building, and planning. Financing by other development partners is listed in the table. Major Development PartnersDevelopment Amount Partner Project Name Duration (million) ADB, KfW Development of new 132/33 kV and 33/11 kV 2006–2012 $53.00 substation under DESA Project ADB, IDB Construction of Ashuganj 450 MW Combined Cycle 2011–2015 $365.4 Power Plant (North) ADB, JBIC Construction and Expansion of Grid Substation with 2005–2012 $94.0 Distribution Line (Phase 1) CIS, Russia Rehabilitation and Modernization of Ghorashal 1997–2012 $30.8 Thermal Power Station Unit 1 and 2 IDA Construction of Siddhirganj 335 MW Peaking 2009–2015 $253.4 Combined Cycle Power Plant IDA Efficient Lighting Initiative for Bangladesh Part 1 and 2009–2012 $34.10 Part 2 IDA TA for Implementation of Bangladesh Power Sector 2011–2015 $16.62 Reform -

Annual Gas Production and Consumption, 2010-2011

Annual Gas Production and Consumption, 2010-2011 October 2011 Hydrocarbon Unit Energy and Mineral Resources Division 1 Table of Content 1. Summary 1 2. Production 3 2.1. National Companies 3 2.1.1. Bangladesh Gas Fields Ltd 3 2.1.1.1. Titas Gas Field 4 2.1.1.2. Habiganj Gas Field 4 2.1.1.3. Bakhrabad Gas Field 4 2.1.1.4. Narshingdi Gas Field 4 2.1.1.5. Meghna Gas Field 4 2.1.1.6. Feni Gas Field 4 2.1.2. Sylhet Gas Field Ltd 4 2.1.2.1. Kailas Tila Gas Field 5 2.1.2.2. Rashidpur Gas Field 5 2.1.2.3. Beani Bazar Gas Field 5 2.1.2.4. Sylhet Gas Field 5 2.1.3. Bangladesh Petroleum Exploration and Production Co. Ltd 5 2.1.3.1. Fenchuganj Gas Field 5 2.1.3.2. Salda Gas Field 6 2.1.3.3. Shahbazpur Gas Field 6 2.1.3.4 Semutang gas Field 6 2.1.3.5 Sundalpur Gas Field 6 2.2. International Oil Companies 6 2.2.1. Chevron Bangladesh 7 2.2.1.1. Bibiyana Gas Field 7 2.2.1.2. Jalalabad Gas Field 7 2.2.1.3. Moulavi Bazar Gas Field 7 2.2.2. Tullow Oil 7 2.2.2.1. Bangura Gas Field 7 2.2.3. Santos (Former Cairn) 8 3. Gas Supply and Consumption 8 4. Figures 1 – 27 9-24 \\HCUCOMMONSERVER\Common Server L\01-039 Strategy Policy Expert\IMP\Annual Report 2010-11\Annual Gas Production and Consumption 2010-11.doc 2 1. -

Ls&Co. Bangladesh Fire Safety and Building Integrity Program

g in progress LEGEND LS&CO. BANGLADESH FIRE SAFETY AND BUILDING INTEGRITY PROGRAM g completed STATUS REPORT MARCH 2018 FIRE SAFETY(1) ELECTRICAL AUDIT BUILDING STABILITY INSPECTION factory factory housing in housing in # of workers Phase I Phase II multi- multi- employed by status of 2013 status of Status of Gravity Loading Status of Detailed POSTAL purpose factory factory (all assessment corrective corrective and Seismic Inspections Engineering Analysis status of corrective FACTORY NAME ADDRESS REGION CODE building building buildings) (annual) action status of audit action (ASCE31)(2) (DEA) action(3) Plot-246-249, Adamjee EPZ, Siddhirganj, Narayanganj Dhaka 1430 No No 2017 Complete 2017- complete complete 2017 - complete 2017 - complete In Progress Ananta Apparels Ltd 2702 Ananta Denim Technology Ltd. Kashpara, Noyabari, Kanchpur, Narayanganj Dhaka 1430 No No 4300 2015 Complete 2015 - complete complete 2015 - complete NA 2015- complete Cosmopolitan Industries Pvt. Ltd Khejur Bagan, Bara Ashulia, Savar Dhaka 1341 No No 4300 2013 Complete 2011 - complete complete 2014 - complete 2014 - complete 2015- complete Cutting Edge Industries Ltd (Washing Plant) 1612, South Salna, Salna Bazar, Gazipur Dhaka 1702 No No 495 2017 Complete 2017-complete complete 2016- complete NA NA Denimach Ltd Kewa Mouja, Ward No. 5, Sreepur, Gazipur Dhaka 1740 No No 6500 2013 Complete 2012 - complete complete 2014 - complete 2014 - complete 2015- complete Dhaka 1340 No No 5295 2017 Complete 2017- complete complete 2017 - complete 2018 - complete In Progress Denitex Ltd 9/1, Karnapara, Savar Karnaphuli Shoes Industries Ltd. (Garments Unit) Korean Export Processing Zone, Anwara, Chittagong. Chittagong 4371 No No 6111 2016 Complete 2016 - complete complete 2016 - complete 2016 - complete 2016 - complete* Kenpark Bangladesh Pvt.Ltd (Unit 1) Sector 8, Plot 31-42, Chittagong Export Processing Zone Chittagong 4223 No No 3400 2013 Complete 2012 - complete complete 2014 - complete 2014 - complete 2015- complete Lalmai Sportswear Inds. -

Zila Report : Narayanganj

POPULATION & HOUSING CENSUS 2011 ZILA REPORT : NARAYANGANJ Bangladesh Bureau of Statistics Statistics and Informatics Division Ministry of Planning BANGLADESH POPULATION AND HOUSING CENSUS 2011 Zila Report: NARAYANGANJ October 2015 BANGLADESH BUREAU OF STATISTICS (BBS) STATISTICS AND INFORMATICS DIVISION (SID) MINISTRY OF PLANNING GOVERNMENT OF THE PEOPLE’S REPUBLIC OF BANGLADESH ISBN-978-984-33-8615-1 COMPLIMENTARY Published by Bangladesh Bureau of Statistics (BBS) Statistics and Informatics Division (SID) Ministry of Planning Website: www.bbs.gov.bd This book or any portion thereof cannot be copied, microfilmed or reproduced for any commercial purpose. Data therein can, however, be used and published with acknowledgement of their sources. Contents Page Message of Honorable Minister, Ministry of Planning …………………………………………….. vii Message of Honorable State Minister, Ministry of Finance and Ministry of Planning …………. ix Foreword ……………………………………………………………………………………………….. xi Preface …………………………………………………………………………………………………. xiii Zila at a Glance ………………………………………………………………………………………... xv Physical Features ……………………………………………………………………………………... xix Zila Map ………………………………………………………………………………………………… xxi Geo-code ………………………………………………………………………………………………. xxii Chapter-1: Introductory Notes on Census ………………………………………………………….. 1 1.1 Introduction ………………………………………………………………………………… 1 1.2 Census and its periodicity ………………………………………………………………... 1 1.3 Objectives ………………………………………………………………………………….. 1 1.4 Census Phases …………………………………………………………………………… 2 1.5 Census Planning …………………………………………………………………………. -

NO PLACE for CRITICISM Bangladesh Crackdown on Social Media Commentary WATCH

HUMAN RIGHTS NO PLACE FOR CRITICISM Bangladesh Crackdown on Social Media Commentary WATCH No Place for Criticism Bangladesh Crackdown on Social Media Commentary Copyright © 2018 Human Rights Watch All rights reserved. Printed in the United States of America ISBN: 978-1-6231-36017 Cover design by Rafael Jimenez Human Rights Watch defends the rights of people worldwide. We scrupulously investigate abuses, expose the facts widely, and pressure those with power to respect rights and secure justice. Human Rights Watch is an independent, international organization that works as part of a vibrant movement to uphold human dignity and advance the cause of human rights for all. Human Rights Watch is an international organization with staff in more than 40 countries, and offices in Amsterdam, Beirut, Berlin, Brussels, Chicago, Geneva, Goma, Johannesburg, London, Los Angeles, Moscow, Nairobi, New York, Paris, San Francisco, Sydney, Tokyo, Toronto, Tunis, Washington DC, and Zurich. For more information, please visit our website: http://www.hrw.org MAY 2018 ISBN: 978-1-6231-36017 No Place for Criticism Bangladesh Crackdown on Social Media Commentary Summary ........................................................................................................................... 1 Information and Communication Act ......................................................................................... 3 Punishing Government Critics ...................................................................................................4 Protecting Religious -

ENVIRONMENTAL ASSESSMENT of WORLD BANK Public Disclosure Authorized FINANCED 2 X 150 MW GAS TURBINE POWER PLANT at SIDDHIRGANJ

POWER CELL, POWER DIVISION MINISTRY OF POWER, ENERGY AND MINERAL RESOURCES GOVERNMENT OF BANGLADESH ENVIRONMENTAL ASSESSMENT OF WORLD BANK Public Disclosure Authorized FINANCED 2 x 150 MW GAS TURBINE POWER PLANT AT SIDDHIRGANJ VOL. I REVISED Public Disclosure Authorized Public Disclosure Authorized FINAL REPORT VOLUME 1: MAIN REPORT Public Disclosure Authorized Bureau of Research, Testing and Consultation (BRTC) Bangladesh University of Engineering & Technology (BUET), Dhaka Dec -2fJO7 POWER CELL, POWER DIVISION MINISTRY OF POWER, ENERGY AND MINERAL RESOURCES GOVERNMENT OF BANGLADESH ENVIRONMENTAL ASSESSMENT OF WORLD BANK FINANCED 2 x 150 MW GAS TURBINE POWER PLANT AT SIDDHIRGANJ FINAL REPORT (Revised December 2007) VOLUME 1: MAIN REPORT Bureau of Research, Testing and Consultation (BRTC) Bangladesh University of Engineering & Technology (BUET), Dhaka December 2007 Executive Summary INTRODUCTION In order to increase the capacity of electricity production, the Ministry of Power, Energy and Mineral Resources, GOB has planned to establish a 2x1 50 MW Gas Turbine Peaking Power Plant at Siddhirga~ljwith the financial assistance of the World Bank. According to the Bangladesh Environment Conservation Rules 1997 (GOB, 1997), construction of a power plant project falls under the RED category. Initial Environmental Examination (IEE) followed by Environmental Impact Assessment (EIA) including Environmental Management Plan are required for these types of projects for getting environmental clearance from the Department of Environment (DOE). According to the World Bank (1999) operational policy OP 4.01, this project is classified as an Environmental Category A project, requiring an Environmental Assessment for the construction and operation of the project with recommendations for appropriate mitigation and management measures. Since a detailed environmental assessment of the proposed project is being carried out, the DOE has exempted the IEE of the project in response to the request by the Electricity Generation Company of Bangladesh Limited (EGCB). -

Bangladesh Investigation (IR)BG-6 BG-6

BG-6 UNITED STATES DEPARTMENT OF THE INTERIOR GEOLOGICAL SURVEY PROJECT REPORT Bangladesh Investigation (IR)BG-6 GEOLOGIC ASSESSMENT OF THE FOSSIL ENERGY POTENTIAL OF BANGLADESH By Mahlon Ball Edwin R. Landis Philip R. Woodside U.S. Geological Survey U.S. Geological Survey Open-File Report 83- ^ 0O Report prepared in cooperation with the Agency for International Developme U.S. Department of State. This report is preliminary and has not been reviewed for conformity with U.S. Geological Survey editorial standards. CONTENTS INTPDDUCTION...................................................... 1 REGIONAL GEOLOGY AND STRUCTURAL FRAMEWORK......................... 3 Bengal Basin................................................. 11 Bogra Slope.................................................. 12 Offshore..................................................... 16 ENERGY RESOURCE IDENTIFICATION............................."....... 16 Petroleum.................................................... 16 History of exploration.................................. 17 Reserves and production................................. 28 Natural gas........................................ 30 Recent developments................................ 34 Coal......................................................... 35 Exploration and Character................................ 37 Jamalganj area..................................... 38 Lamakata-^hangarghat area.......................... 40 Other areas........................................ 41 Resources and reserves.................................. -

Development Coordination

SASEC Bangladesh India Electrical Grid Interconnection Project – Additional Financing (RRP BAN 44192) DEVELOPMENT COORDINATION A. Major Development Partners: Strategic Foci and Key Activities 1. Multilateral development partners in the energy sector in Bangladesh are the Asian Development Bank (ADB), Islamic Development Bank, and the World Bank. In addition, bilateral aid comes from France, Germany, Japan, Kuwait, Norway, the Russian Federation, the United Kingdom, and the United States. Subsectors receiving support include power generation, transmission and distribution upgrading, energy sector reforms and sector planning, energy efficiency, rural electrification, generation plant upgrades, and capacity building. Financing by other development partners is listed in the table. Major Development Partners Development Project Name Duration Amount Partner (million) ADB, KfW Development of New 132/33 kV and 33/11 kV Substation under 2006–2012 $53.00 DESA Project ADB, IDB Construction of Ashuganj 450 MW Combined-Cycle Power Plant 2011–2015 $365.40 (North) ADB, JBIC Construction and Expansion of Grid Substation with Distribution 2005–2012 $94.00 Line (Phase 1) CIS, Russian Rehabilitation and Modernization of Ghorashal Thermal Power 1997–2012 $30.80 Federation Station Unit 1 and 2 DFID Increasing Palli Bidyut Samiti’s customers by 1 million under its 2006–2013 $42.41 distribution system KfW Rehabilitation and Modernization of Ashuganj Power Station Unit 2000–2011 $125.00 3, 4, and 5 (revised) EDCF Bibiana-Kaliakoir 400 kV and Fenchuganj–Bibiana -

Bangladesh Gas Fields Company Limited for the Asian Development Bank

Initial Environmental Examination Document Stage: Update Project Number: P45203 (BAN) September 2016 People’s Republic of Bangladesh: Natural Gas Infrastructure and Efficiency Improvement Project (Component 1 - Installation of Wellhead Gas Compressors at Location “A” of Titas Gas Field) Prepared by Bangladesh Gas Fields Company Limited for the Asian Development Bank. This is an updated version of the draft originally posted in August 2016 available on https://www.adb.org/sites/default/files/project-document/190161/45203-006-iee-01.pdf. CURRENCY EQUIVALENTS (as of 3 August 2016) Currency unit – Taka (Tk) Tk 1.00 = $0.012755 $1.00 = Tk78.40 ABBREVIATIONS ADB - Asian Development Bank AIIB - Asian Infrastructure Investment Bank BGFCL - Bangladesh Gas Fields Company Limited CITES - Convention on International Trade in Endangered Species of Wild Fauna and Flora DOE - Department of Environment EA - Executing Agency ECA - Environment Conservation Act ECC - Environmental Clearance Certificate ECR - Environment Conservation Rules EIA - Environmental Impact Assessment EMP - Environmental Management Plan EMRD - Energy and Mineral Resources Division ESMS - Environment and Safety Management System GoB - Government of Bangladesh GRC - Grievance Redress Committee IEE - Initial Environmental Examination LCC - Locational Clearance Certificate MOEF - Ministry of Environment and Forests MPEMR - Ministry of Power, Energy and Mineral Resources NOC - No Objection Certificate PIU - Project Implementation Unit ROW - Right of Way SPS - Safeguard Policy Statement WEIGHTS AND MEASURES oC - degree Celsius dB(A) - A-weighted decibel ha - hectare Hp - horsepower lahk - 100,000 ppb - parts per billion ppm - parts per million µg/m3 - microgram per cubic meter m2 - square meter NOTE In this report, "$" refers to US dollars. This initial environmental examination is a document of the borrower. -

Preparatory Survey on the Natural Gas Efficiency Project in the People's Republic of Bangladesh FINAL REPORT

Ministry of Power, Energy and Mineral Resources The People’s Republic of Bangladesh Preparatory Survey on The Natural Gas Efficiency Project in The People’s Republic of Bangladesh FINAL REPORT March 2014 JAPAN INTERNATIONAL COOPERATION AGENCY ORIENTAL CONSULTANTS CO., LTD. IL JR 14-069 Ministry of Power, Energy and Mineral Resources The People’s Republic of Bangladesh Preparatory Survey on The Natural Gas Efficiency Project in The People’s Republic of Bangladesh FINAL REPORT March 2014 JAPAN INTERNATIONAL COOPERATION AGENCY ORIENTAL CONSULTANTS CO., LTD. Survey Area Table of Contents Survey Area List of Figures List of Tables Abbreviations Executive Summary Page Chapter 1 Introduction ........................................................................................................... 1-1 1.1 Background of the Survey ........................................................................................... 1-1 1.2 Objective of the Survey ............................................................................................... 1-2 1.3 Objective of the Project ............................................................................................... 1-2 1.4 Survey Team ................................................................................................................ 1-3 1.5 Survey Schedule........................................................................................................... 1-4 1.5.1 Entire Schedule ..................................................................................................... -

Data Collection Survey on Bangladesh Natural Gas Sector FINAL REPORT

Ministry of Power, Energy and Mineral Resources The People’s Republic of Bangladesh Data Collection Survey on Bangladesh Natural Gas Sector FINAL REPORT January 2012 JAPAN INTERNATIONAL COOPERATION AGENCY ORIENTAL CONSULTANTS CO., LTD. SAD JR 12-005 Ministry of Power, Energy and Mineral Resources The People’s Republic of Bangladesh Data Collection Survey on Bangladesh Natural Gas Sector FINAL REPORT January 2012 JAPAN INTERNATIONAL COOPERATION AGENCY ORIENTAL CONSULTANTS CO., LTD. Source: Petrobangla Annual Report 2010 Abbreviations ADB Asian Development Bank BAPEX Bangladesh Petroleum Exploration & Production Company Limited BCF Billion Cubic Feet BCMCL Barapukuria Coal Mine Company Limited BEPZA Bangladesh Export Processing Zones Authority BERC Bangladesh Energy Regulatory Commission BEZA Bangladesh Economic Zone Authority BGFCL Bangladesh Gas Fields Company Limited BGSL Bakhrabad Gas Systems Limited BOI Board of Investment BPC Bangladesh Petroleum Corporation BPDB Bangladesh Power Development Board CNG Compressed Natural Gas DWMB Deficit Wellhead Margin for BAPEX ELBL Eastern Lubricants Blenders Limited EMRD Energy and Mineral Resources Division ERD Economic Related Division ERL Eastern Refinery Limited GDP Gross Domestic Product GEDBPC General Economic Division, Bangladesh Planning Commission GIZ Gesellschaft für Internationale Zusammenarbeit GOB Government of Bangladesh GTCL Gas Transmission Company Limited GTZ Deutsche Gesellschaft fur Technische Zusammenarbeit GSMP Gas Sector Master Plan GSRR Gas Sector Reform Roadmap HCU Hydrocarbon