Audit Report on the Accounts of Local Councils/Government Balochistan 2012-2013

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

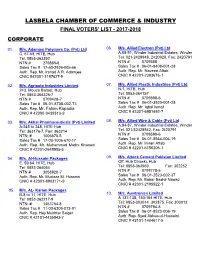

Final Voter List 2017-18

LASBELA CHAMBER OF COMMERCE & INDUSTRY FINAL VOTERS’ LIST - 2017-2018 CORPORATE 01. M/s. Adamjee Polymers Co. (Pvt) Ltd 06. M/s. Allied Electron (Pvt) Ltd C. 67-69, HITE, Hub A.88-91, Winder Industrial Estates, Winder Tel: 0853-363392 Tel: 021-2428948, 2420920, Fax: 2420791 NTN # 279885-6 NTN # 0709588 Sales Tax # 17-50-3926-005-46 Sales Tax # 06-01-8408-001-28 Auth. Rep. Mr. Irshad A.R. Adamjee Auth. Rep. Mr. Naveed Aftab CNIC #42301-3197627-9 CNIC # 42201-2393676-1 02. M/s. Agriauto Industries Limited 07. M/s. Allied Plastic Industries (Pvt) Ltd. 243, Mouza Baroot, Hub N-1, HITE, Hub Tel: 0853-364326-7 Tel: 0853-364157 NTN # 0709428-7 NTN # 0709598-6 Sales Tax # 06-01-8708-002-73 Sales Tax # 06-01-3920-001-28 Auth. Rep. Mr. Fahim Kapadia Auth. Rep. Mr. Iqbal Ismail CNIC # 42000-0439313-9 CNIC # 42301-6951492-7 03. M/s. Akhai Pharmaceuticals (Pvt) Limited 08. M/s. Allied Wire & Cable (Pvt) Ltd A-245 to 248, HITE Hub A.84-87, Winder Industrial Estates, Winder Tel: 363176-7, Fax: 363214 Tel: 021-32428942, Fax: 2420791 NTN: # 1006670-5 NTN # 0709599-6 Sales Tax # 17-00-1006-670-17 Sales Tax # 06-01-8544-004-19 Auth. Rep. Mr. Muhammad Madni Khanani Auth. Rep. Mr. Imran Aftab CNIC # 42201-2649905-5 CNIC # 42201-6156206-1 04. M/s. Al-Hussain Packages 09. M/s. Attock Cement Pakistan Limited E. 59-64, HITE, Hub Off. Hub Chowki, Hub Tel: 0853-364064 Tel: 0853-363569, Fax: 302252 NTN # 3058920-7 NTN # 0709778-5 Auth. -

Buffer Zone, Colonial Enclave, Or Urban Hub?

Working Paper no. 69 - Cities and Fragile States - BUFFER ZONE, COLONIAL ENCLAVE OR URBAN HUB? QUETTA :BETWEEN FOUR REGIONS AND TWO WARS Haris Gazdar, Sobia Ahmad Kaker, Irfan Khan Collective for Social Science Research February 2010 Crisis States Working Papers Series No.2 ISSN 1749-1797 (print) ISSN 1749-1800 (online) Copyright © H. Gazdar, S. Ahmad Kaker, I. Khan, 2010 24 Crisis States Working Paper Buffer Zone, Colonial Enclave or Urban Hub? Quetta: Between Four Regions and Two Wars Haris Gazdar, Sobia Ahmad Kaker and Irfan Khan Collective for Social Science Research, Karachi, Pakistan Quetta is a city with many identities. It is the provincial capital and the main urban centre of Balochistan, the largest but least populous of Pakistan’s four provinces. Since around 2003, Balochistan’s uneasy relationship with the federal state has been manifested in the form of an insurgency in the ethnic Baloch areas of the province. Within Balochistan, Quetta is the main shared space as well as a point of rivalry between the two dominant ethnic groups of the province: the Baloch and the Pashtun.1 Quite separately from the internal politics of Balochistan, Quetta has acquired global significance as an alleged logistic base for both sides in the war in Afghanistan. This paper seeks to examine different facets of Quetta – buffer zone, colonial enclave and urban hub − in order to understand the city’s significance for state building in Pakistan. State-building policy literature defines well functioning states as those that provide security for their citizens, protect property rights and provide public goods. States are also instruments of repression and the state-building process is often wrought with conflict and the violent suppression of rival ethnic and religious identities, and the imposition of extractive economic arrangements (Jones and Chandaran 2008). -

Defenders of Human Rights in Balochistan in Need of Defence

Defenders of human rights in Balochistan in need of defence Angelika Pathak August 2011 List of contents 1. Attacks on newspapers, electronic media and abuses of individual journalists in Balochistan 1.1 Newspapers and electronic media 1.2 Abuses of individual journalists a. Arbitrary detention of journalists b. Harassment and ill-treatment of journalists c. Journalists subjected to enforced disappearance and extrajudicial execution d. Journalists subjected to enforced disappearance and released, reports of torture e. Journalists subjected to targeted killing f. Journalists inadequately protected while covering violence 2. Human rights abuses inflicted on lawyers in Balochistan 3. Human rights abuses inflicted on human rights activists in Balochistan 4. Recommendations to the Federal Government of Pakistan and the Provincial Government of Balochistan Executive summary Human rights defenders, i.e. persons who uncover human rights violations, bring them to public knowledge and campaign for redress for victims through peaceful and non-violent means, were in December 1998 placed been under the special protection of the international community when the General Assembly adopted the UN Declaration on Human Rights Defenders. It was the first UN instrument that explicitly recognizes the importance and legitimacy of the work of human rights defenders and lays down their right to effective protection. This commitment has not been honoured in Balochistan. Human rights defenders - be they journalists investigating and documenting wrongdoings of state agents, lawyers representing victims of human rights abuses in court or human rights activists campaigning to end human rights violations – have been subjected to a range of human rights violations themselves. They have been harassed, arbitrarily arrested and detained, subjected to enforced disappearance, torture and extrajudicial killings. -

Public Sector Development Programme (Sectorwise) 2014 - 15 Original

Public Sector Development Programme (Sectorwise) 2014 - 15 Original 06-18-2014 1 of 162 Public Sector Development Programme (Sectorwise) 2014 - 15 Original Chapter: AGRICULTURE Sector: Agriculture Subsector: Agricultural Extension Estimated Cost Exp: Upto June 2014 Fin: Allocation 2014-15 Fin: Thr: Fwd: S No Project ID Project Name GOB / Total GOB / Total Achv: Capital/ Revenue Total Target GOB / FPA FPA FPA % FPA % Ongoing 1 Z2004.0083 CONST: OF MARKET SQUARES 187.881 187.881 140.456 140.456 74% 10.000 0.000 10.000 80% 37.425 Provincial AT LORALAI, K. SAIFULLAH, 0.000 0.000 0.000 0.000 Approved PISHIN, LASBELA, PANJGUR & KHUZDAR. 2 Z2008.0015 MIRANI DAM COMMAND AREA 150.000 150.000 105.000 105.000 70% 10.000 0.000 10.000 76% 35.000 Kech DEVELOPMENT PROJECT. 0.000 0.000 0.000 0.000 Approved 3 Z2008.0016 SABAKZAI DAM COMMAND AREA 134.500 134.500 119.519 119.519 88% 14.981 0.000 14.981 100% 0.000 Zhob DEVELOPMENT PROJECT. 0.000 0.000 0.000 0.000 Approved 4 Z2013.0187 AGRICULTURE DEVELOPMENT 19.100 19.100 0.000 0.000 0% 5.000 0.000 5.000 26% 14.100 Pishin SCHEME FOR WATER 0.000 0.000 0.000 0.000 Approved RESOURCE MANAGEMENT IN DIST. PISHIN. 5 Z2013.0195 AGRICULTURE DEVELOPMENT 30.100 30.100 0.000 0.000 0% 10.000 0.000 10.000 33% 20.100 Qilla SCHEME FOR WATER 0.000 0.000 0.000 0.000 Abdullah RESOURCE MANAGEMENT IN Approved DIST. -

Final Voter List 2016-17

LASBELA CHAMBER OF COMMERCE & INDUSTRY FINAL VOTERS’ LIST-2016-2017 CORPORATE 01. M/s. Adamjee Polymers Co. (Pvt) Ltd 06. M/s. Allied Electron (Pvt) Ltd C. 67-69, HITE, Hub A.88-91, Winder Industrial Estates, Winder Tel: 0853-363392 Tel: 021-2428948, 2420920, Fax: 2420791 NTN # 279885-6 NTN # 0709588 Sales Tax # 17-50-3926-005-46 Sales Tax # 06-01-8408-001-28 Auth. Rep. Mr. Irshad A.R. Adamjee Auth. Rep. Mr. Naveed Aftab CNIC #42301-3197627-9 CNIC # 42201-2393676-1 02. M/s. Agriauto Industries Limited 07. M/s. Allied Plastic Industries (Pvt) Ltd. 243, Mouza Baroot, Hub N-1, HITE, Hub Tel: 0853-364326-7 Tel: 0853-364157 NTN # 0709428-7 NTN # 0709598-6 Sales Tax # 06-01-8708-002-73 Sales Tax # 06-01-3920-001-28 Auth. Rep. Mr. Fahim Kapadia Auth. Rep. Mr. Iqbal Ismail CNIC # 42000-0439313-9 CNIC # 42301-6951492-7 03. M/s. Akhai Pharmaceuticals (Pvt) Limited 08. M/s. Allied Wire & Cable (Pvt) Ltd A-245 to 248, HITE Hub A.84-87, Winder Industrial Estates, Winder Tel: 363176-7, Fax: 363214 Tel: 021-32428942, Fax: 2420791 NTN: # 1006670-5 NTN # 0709599-6 Sales Tax # 17-00-1006-670-17 Sales Tax # 06-01-8544-004-19 Auth. Rep. Mr. Muhammad Madni Khanani Auth. Rep. Mr. Imran Aftab CNIC # 42201-2649905-5 CNIC # 42201-6156206-1 04. M/s. Al-Hussain Packages 09. M/s. Attock Cement Pakistan Limited E. 59-64, HITE, Hub Off. Hub Chowki, Hub Tel: 0853-364064 Tel: 0853-363569, Fax: 302252 NTN # 3058920-7 NTN # 0709778-5 Auth. -

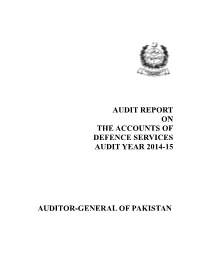

Audit Report on the Accounts of Defence Services Audit Year 2014-15

AUDIT REPORT ON THE ACCOUNTS OF DEFENCE SERVICES AUDIT YEAR 2014-15 AUDITOR-GENERAL OF PAKISTAN TABLE OF CONTENTS Page ABBREVIATIONS AND ACRONYMS iii PREFACE v EXECUTIVE SUMMARY vi AUDIT STATISTICS CHAPTER-1 Ministry of Defence Production 1.1 Introduction 1 1.2 Status of Compliance of PAC Directives 1 AUDIT PARAS 1.3 Recoverable / Overpayments 3 1.4 Loss to State 26 1.5 Un-authorized Expenditure 29 1.6 Mis-procurement of Stores / Mis-management of contract 33 1.7 Non-Production of Records 45 CHAPTER-2 Ministry of Defence 2.1 Introduction48 2.2 Status of Compliance of PAC Directives 48 AUDIT PARAS Pakistan Army 2.3 Recoverable / Overpayments 50 2.4 Loss to State 63 2.5 Un-authorized Expenditure 67 2.6 Mis-procurement of Stores / Mis-management of Contract 84 i 2.7 Non-Production of Auditable Records 95 Military Lands and Cantonments 2.8 Recoverable / Overpayments 100 2.9 Loss to State 135 2.10 Un-authorized Expenditure 152 Pakistan Air Force 2.11 Recoverable / Overpayments 156 2.12 Loss to State 171 2.13 Un-authorized Expenditure 173 2.14 Mis-procurement of Stores / Mis-management of contract 181 Pakistan Navy 2.15 Recoverable / Overpayments 184 2.16 Loss to State 197 2.17 Un-authorized Expenditure 198 2.18 Mis-procurement of Stores / Mis-management of contract 207 Military Accountant General 2.19 Recoverable / Overpayments 215 2.20 Un-authorized Expenditure 219 Inter Services Organization (ISO’s) 2.21 Recoverable / Overpayments 222 Annexure-I MFDAC Paras (DGADS North) Annexure-II MFDAC Paras (DGADS South) ii ABBREVIATIONS AND ACRONYMS -

Development Profile District Quetta

District Development Q Development u e P R O F I L E t t 2 0 1 1 a - D i s t Quetta r i c t D e v e l o p m e n t P r o f i l e 2 0 1 1 Planning & Development Department United Nations Children’s Fund Government of Balochistan, Quetta Provincial Office Balochistan, Quetta Planning & Development Department, Government of Balochistan in Collaboration with UNICEF District Development P R O F I L E 2 0 1 1 Q u e t t a Prepared by Planning & Development Department, Government of Balochistan, Quetta in Collaboration with United Nations Children’s Fund Provincial Office Balochistan, Quetta July 18, 2011 Message Foreword In this age of knowledge economy, reliance on every possible tool The Balochistan District Development Profile 2010 is a landmark exercise of Planning and available for decision making is crucial for improving public resource Development Department, Government of Balochistan, to update the district profile data management, brining parity in resource distribution and maximizing that was first compiled in 1998. The profiles have been updated to provide a concise impact of development interventions. These District Development landmark intended for development planning, monitoring and management purposes. Profiles are vivid views of Balochistan in key development areas. The These districts profiles would be serving as a tool for experts, development practitioners Planning and Development Department, Government of Balochistan and decision-makers/specialists by giving them vast information wrapping more than 18 is highly thankful to UNICEF Balochistan for the technical and dimensions from Balochistan’s advancement extent. -

Lasbela District 2003/4: Drinking and Irrigation Water Key Findings

Project Report PR-PK-lsb1-04 Pakistan Lasbela district 2003/4: Drinking and irrigation water key findings Anne Cockcroft, Khalid Omer, Noor Ansari, Manzoor Baloch and Neil Andersson Social audit of governance and delivery of public services Lasbela district 2003/4 Drinking and irrigation water Key findings CIETcanada and Lasbela District Government December 2004 A Cockcroft, K Omer, N Ansari, M Baloch, N Andersson Contents Contents...................................................................................................i List of tables....................................................................................i List of figures .................................................................................ii List of boxes...................................................................................ii Acknowledgments.........................................................................iii Summary ...............................................................................................vi Introduction............................................................................................ 1 Methods.................................................................................................. 3 Selection of Lasbela as the focus district........................................ 3 Institutional arrangements for the Lasbela social audit .................. 3 Priority setting................................................................................ 3 Design of instruments and sample................................................. -

Download File

Evaluation of CDWA Balochistan Component P&DD/UNICEF Joint Evaluation 1 Evaluation of CDWA Balochistan Component P&DD/UNICEF Joint Evaluation Photo Credits: Survey team Disclaimer: The views and opinion expressed in this report are those of the consultants and do not necessarily reflect the views or policies of UNICEF and/or other organizations involved in the programme. 2 Evaluation of CDWA Balochistan Component P&DD/UNICEF Joint Evaluation TABLE OF CONTENTS Title Page no. ACKNOWLEDGEMENTS 6 EXECUTIVE SUMMARY 7 CHAPTER 1: CONTEXT AND BACKGROUND OF THE EVALUATION 15 1.1 Background to Clean Drinking Water in Balochistan 15 1.2 Object of the Evaluation: Clean Drinking Water for All Project 18 CHAPTER 2: EVALUATION PURPOSE, OBJECTIVES AND METHODOLOGY 23 2.1 Purpose and Objectives 23 2.2 Theory of Change 23 2.3 Evaluation Scope 25 2.4 Users of the Evaluation and Associated Dissemination 26 2.5 Evaluation Criteria 27 2.6 Evaluation Framework and Key Questions 27 2.7 Methodology overview 28 2.8 Challenges and Risks 35 CHAPTER 3: FINDINGS 38 3.1 Overview of Findings against the Hypothesis and Key Evaluation 38 Questions 3.2 Relevance 41 3.3 Effectiveness 45 3.4 Efficiency 51 3.5 Outcomes 56 3.6 Sustainability 57 3.7 HRBA, Equity and Gender 58 CHAPTER 4: CONCLUSIONS AND RECOMMENDATIONS 60 4.1 Conclusion 60 4.2 Lessons learnt 61 4.3 Recommendations 61 ANNEXURES Appendix 1:ToR Evaluation of the Clean Drinking for All (CDWA) Project in 65 Balochistan Appendix 2:Evaluation ToR Annex-1: List of 409 CDWA Water Filtration 77 Plants Appendix 3: Evaluation -

Lasbela District Education Plan (2016-17 to 2021-22)

Lasbela District Education Plan (2016-17 to 2021-22) Table of Contents LIST OF ACRONYMS 1 LIST OF FIGURES 3 LIST OF TABLES 4 1 INTRODUCTION 5 2 METHODOLOGY & PROCESS 7 2.1 METHODOLOGY 7 2.1.1 DESK RESEARCH 7 2.1.2 CONSULTATIONS 7 2.1.3 STAKEHOLDERS INVOLVEMENT 7 2.2 PROCESS FOR DEPS DEVELOPMENT: 8 2.2.1 SECTOR ANALYSIS: 8 2.2.2 IDENTIFICATION AND PRIORITIZATION OF STRATEGIES: 9 2.2.3 FINALIZATION OF DISTRICT PLANS: 9 3 LASBELA DISTRICT PROFILE 10 3.1 POPULATION 11 3.2 ECONOMIC ENDOWMENTS 11 3.3 POVERTY & CHILD LABOR: 12 3.4 STATE OF EDUCATION 12 4 ACCESS & EQUITY 14 4.1 EQUITY AND INCLUSIVENESS 19 4.2 IMPORTANT FACTORS 19 4.2.1 SCHOOL AVAILABILITY AND UTILIZATION 19 4.2.2 MISSING FACILITIES AND SCHOOL ENVIRONMENT 21 4.2.3 POVERTY 21 4.2.4 PARENT’S ILLITERACY 21 4.2.5 ALTERNATE LEARNING PATHWAYS 22 4.3 OBJECTIVES AND STRATEGIES 23 5 DISASTER RISK REDUCTION 27 5.1 OBJECTIVES AND STRATEGIES 28 6 QUALITY AND RELEVANCE OF EDUCATION 29 6.1 SITUATION 29 6.2 DISTRICT LIMITATIONS AND STRENGTHS 30 6.3 OVERARCHING FACTORS FOR POOR EDUCATION 32 6.4 DISTRICT RELATED FACTORS OF POOR QUALITY 33 6.4.1 OWNERSHIP OF QUALITY IN EDUCATION 33 6.4.2 CAPACITY OF FIELD TEAMS 33 6.4.3 ACCOUNTABILITY MODEL OF HEAD TEACHERS 33 6.4.4 NO DATA COMPILATION AND FEEDBACK 33 6.4.5 CURRICULUM IMPLEMENTATION AND FEEDBACK 34 6.4.6 TEXTBOOKS DISTRIBUTION AND FEEDBACK 34 6.4.7 PROFESSIONAL DEVELOPMENT 34 6.4.8 TEACHERS AVAILABILITY 35 6.4.9 ASSESSMENTS 35 6.4.10 EARLY CHILDHOOD EDUCATION (ECE) 35 6.4.11 AVAILABILITY AND USE OF LIBRARIES & LABORATORIES 36 6.4.12 SCHOOL ENVIRONMENT -

Audit Report on the Accounts of Defence Services Audit Year 2016-17

AUDIT REPORT ON THE ACCOUNTS OF DEFENCE SERVICES AUDIT YEAR 2016-17 AUDITOR-GENERAL OF PAKISTAN TABLE OF CONTENTS Page ABBREVIATIONS AND ACRONYMS iii PREFACE vi EXECUTIVE SUMMARY vii AUDIT STATISTICS I. Audit Work Statistics xi II. Audit Observations Classified by Categories xi III. Outcome Statistics xii IV. Irregularities Pointed Out xiii V. Cost-Benefit Analysis xiii CHAPTER-1 Ministry of Defence 1.1 Introduction 01 1.2 Status of Compliance of PAC Directives 01 AUDIT PARAS Pakistan Army 1.3 Recoverables / Overpayments 03 1.4 Irregular / Un-authorized Expenditure 18 1.5 Mis-procurement of stores 31 1.6 Non-production of Record 38 Military Lands and Cantonments 1.7 Recoverables / Overpayments 41 1.8 Loss to State 72 1.9 Mis-procurement of stores 75 i Pakistan Air Force 1.10 Recoverables / Overpayments 76 1.11 Loss to State 83 1.12 Irregular / Unauthorized Expenditure 83 1.13 Mis-procurement of stores 86 Pakistan Navy 1.14 Recoverables / Overpayments 91 1.15 Loss to State 94 1.16 Irregular / Unauthorized Expenditure 95 1.17 Mis-procurement of stores 98 Military Accountant General 1.18 Recoverables / Overpayments 108 1.19 Irregular / Unauthorized Expenditure 109 1.20 Mis-procurement of stores 110 CHAPTER-2 Ministry of Defence Production 2.1 Introduction 112 2.2 Status of Compliance of PAC Directives 112 AUDIT PARAS 2.3 Recoverables / Overpayments 114 2.4 Loss to State 116 2.5 Irregular / Unauthorized Expenditure 118 2.6 Mis-procurement of stores 121 Annexure-I MFDAC Paras (DGADS North) 122 Annexure-II MFDAC Paras (DGADS South) 134 ii ABBREVIATIONS -

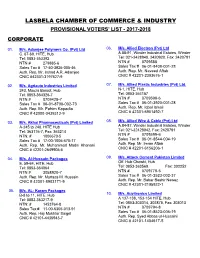

Provisional Voter List 2017-18

LASBELA CHAMBER OF COMMERCE & INDUSTRY PROVISIONAL VOTERS’ LIST - 2017-2018 CORPORATE 01. M/s. Adamjee Polymers Co. (Pvt) Ltd 06. M/s. Allied Electron (Pvt) Ltd C. 67-69, HITE, Hub A.88-91, Winder Industrial Estates, Winder Tel: 0853-363392 Tel: 021-2428948, 2420920, Fax: 2420791 NTN # 279885-6 NTN # 0709588 Sales Tax # 17-50-3926-005-46 Sales Tax # 06-01-8408-001-28 Auth. Rep. Mr. Irshad A.R. Adamjee Auth. Rep. Mr. Naveed Aftab CNIC #42301-3197627-9 CNIC # 42201-2393676-1 02. M/s. Agriauto Industries Limited 07. M/s. Allied Plastic Industries (Pvt) Ltd. 243, Mouza Baroot, Hub N-1, HITE, Hub Tel: 0853-364326-7 Tel: 0853-364157 NTN # 0709428-7 NTN # 0709598-6 Sales Tax # 06-01-8708-002-73 Sales Tax # 06-01-3920-001-28 Auth. Rep. Mr. Fahim Kapadia Auth. Rep. Mr. Iqbal Ismail CNIC # 42000-0439313-9 CNIC # 42301-6951492-7 03. M/s. Akhai Pharmaceuticals (Pvt) Limited 08. M/s. Allied Wire & Cable (Pvt) Ltd A-245 to 248, HITE Hub A.84-87, Winder Industrial Estates, Winder Tel: 363176-7, Fax: 363214 Tel: 021-32428942, Fax: 2420791 NTN: # 1006670-5 NTN # 0709599-6 Sales Tax # 17-00-1006-670-17 Sales Tax # 06-01-8544-004-19 Auth. Rep. Mr. Muhammad Madni Khanani Auth. Rep. Mr. Imran Aftab CNIC # 42201-2649905-5 CNIC # 42201-6156206-1 04. M/s. Al-Hussain Packages 09. M/s. Attock Cement Pakistan Limited E. 59-64, HITE, Hub Off. Hub Chowki, Hub Tel: 0853-364064 Tel: 0853-363569, Fax: 302252 NTN # 3058920-7 NTN # 0709778-5 Auth.