2019 PUF Detailed Schedule of Investments

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

KOREA Morning Focus

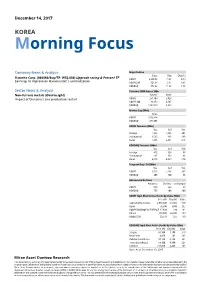

December 14, 2017 KOREA Morning Focus Company News & Analysis Major Indices Close Chg Chg (%) Hanwha Corp. (000880/Buy/TP: W56,000) Upgrade rating & Present TP ' KOSPI 2,480.55 19.55 0.79 Earnings to improve on Hanwha E&C s normalization KOSPI 200 326.18 2.11 0.65 KOSDAQ 772.22 11.82 1.55 Sector News & Analysis Turnover ('000 shares, Wbn) Non-ferrous metals (Overweight) Volume Value Impact of Glencore’s zinc production restart KOSPI 251,104 5,028 KOSPI 200 89,459 4,107 KOSDAQ 1,131,049 5,394 Market Cap (Wbn) Value KOSPI 1,613,324 KOSDAQ 274,605 KOSPI Turnover (Wbn) Buy Sell Net Foreign 1,443 1,648 -205 Institutional 1,585 886 698 Retail 1,945 2,461 -515 KOSDAQ Turnover (Wbn) Buy Sell Net Foreign 412 324 88 Institutional 285 192 93 Retail 4,695 4,869 -174 Program Buy / Sell (Wbn) Buy Sell Net KOSPI 1,513 1,206 307 KOSDAQ 206 120 86 Advances & Declines Advances Declines Unchanged KOSPI 566 244 67 KOSDAQ 733 408 100 KOSPI Top 5 Most Active Stocks by Value (Wbn) Price (W) Chg (W) Value Samsung Electronics 2,566,000 -39,000 570 Hynix 76,800 -1,000 265 KODEX KOSDAQ150 LEVERAGE 17,680 280 191 NCsoft 488,000 22,000 189 KODEX 200 32,670 255 160 KOSDAQ Top 5 Most Active Stocks by Value (Wbn) Price (W) Chg (W) Value SillaJen 89,100 1,100 319 New Pride 4,850 145 263 Celltrion Healthcare 93,100 6,100 231 TissueGene(Reg.S) 54,100 4,300 225 Celltrion 210,000 4,400 205 Note: As of December 13, 2017 Mirae Asset Daewoo Research Hanwha Corp. -

Important Notice the Depository Trust Company

Important Notice The Depository Trust Company B #: 12945-20 Date: February 10, 2020 To: All Participants Category: Dividends | International From: Global Tax Services Attention: Managing Partner/Officer, Cashier, Dividend Mgr., Tax Mgr. BNY Mellon | ADRs | Qualified Dividends for Tax Year 2019 Subject: Bank of New York Mellon Corporation (“BNYM”), as depositary for these issues listed below has reviewed and determined if they met the criteria for reduced U.S. tax rate as “qualified dividends” for tax year 2019. The Depository Trust Company received the attached correspondence containing Tax Information. If applicable, please consult your tax advisor to ensure proper treatment of these events. Non-Confidential DTCC Public (White) 2019 DIVIDEND CERTIFICATION CUSIP DR Name Country Exchange Qualified 000304105 AAC TECHNOLOGIES HLDGS INC CAYMAN ISLANDS OTC N 000380105 ABCAM PLC UNITED KINGDOM OTC Y 001201102 AGL ENERGY LTD AUSTRALIA OTC Y 001317205 AIA GROUP LTD HONG KONG OTC N 002482107 A2A SPA ITALY OTC Y 003381100 ABERTIS INFRAESTRUCTURAS S A SPAIN OTC Y 003725306 ABOITIZ EQUITY VENTURES INC PHILIPPINES OTC Y 003730108 ABOITIZ PWR CORP PHILIPPINES OTC Y 004563102 ACKERMANS & VAN HAAREN BELGIUM OTC Y 004845202 ACOM CO. JAPAN OTC Y 006754204 ADECCO GROUP AG SWITZERLAND OTC Y 007192107 ADMIRAL GROUP UNITED KINGDOM OTC Y 007627102 AEON CO LTD JAPAN OTC Y 008712200 AIDA ENGR LTD JAPAN OTC Y 009126202 AIR LIQUIDE FRANCE OTC Y 009279100 AIRBUS SE NETHERLANDS OTC Y 009707100 AJINOMOTO INC JAPAN OTC Y 015096209 ALEXANDRIA MINERAL - REG. S EGYPT None N 015393101 ALFA LAVAL AB SWEDEN SWEDEN OTC Y 021090204 ALPS ELEC LTD JAPAN OTC Y 021244207 ALSTOM FRANCE OTC Y 022205108 ALUMINA LTD AUSTRALIA OTC Y 022631204 AMADA HLDGS CO LTD JAPAN OTC Y 023511207 AMER GROUP HOLDING - REG. -

FTSE Korea 30/18 Capped

2 FTSE Russell Publications 19 August 2021 FTSE Korea 30/18 Capped Indicative Index Weight Data as at Closing on 30 June 2021 Index weight Index weight Index weight Constituent Country Constituent Country Constituent Country (%) (%) (%) Alteogen 0.19 KOREA Hyundai Engineering & Construction 0.35 KOREA NH Investment & Securities 0.14 KOREA AmoreG 0.15 KOREA Hyundai Glovis 0.32 KOREA NHN 0.07 KOREA Amorepacific Corp 0.65 KOREA Hyundai Heavy Industries 0.29 KOREA Nong Shim 0.08 KOREA Amorepacific Pfd. 0.08 KOREA Hyundai Marine & Fire Insurance 0.13 KOREA OCI 0.17 KOREA BGF Retail 0.09 KOREA Hyundai Merchant Marine 1.02 KOREA Orion 0.21 KOREA BNK Financial Group 0.18 KOREA Hyundai Mipo Dockyard 0.15 KOREA Ottogi 0.06 KOREA Celltrion Healthcare 0.68 KOREA Hyundai Mobis 1.53 KOREA Paradise 0.07 KOREA Celltrion Inc 2.29 KOREA Hyundai Motor 2.74 KOREA Posco 1.85 KOREA Celltrion Pharm 0.24 KOREA Hyundai Motor 2nd Pfd. 0.33 KOREA Posco Chemical 0.32 KOREA Cheil Worldwide 0.14 KOREA Hyundai Motor Pfd. 0.21 KOREA Posco International 0.09 KOREA CJ Cheiljedang 0.3 KOREA Hyundai Steel 0.33 KOREA S1 Corporation 0.13 KOREA CJ CheilJedang Pfd. 0.02 KOREA Hyundai Wia 0.13 KOREA Samsung Biologics 0.92 KOREA CJ Corp 0.11 KOREA Industrial Bank of Korea 0.22 KOREA Samsung C&T 0.94 KOREA CJ ENM 0.15 KOREA Kakao 3.65 KOREA Samsung Card 0.08 KOREA CJ Logistics 0.12 KOREA Kangwon Land 0.23 KOREA Samsung Electro-Mechanics 0.81 KOREA Coway 0.36 KOREA KB Financial Group 1.78 KOREA Samsung Electronics 25.36 KOREA Daewoo Engineering & Construction 0.12 KOREA KCC Corp 0.12 KOREA Samsung Electronics Pfd. -

Innovation and Upgrading Pathways in the Chinese Smartphone Production GVC Jiong How Lua National University of Singapore

Innovation and Upgrading pathways in the Chinese smartphone production GVC Lua Innovation and Upgrading pathways in the Chinese smartphone production GVC Jiong How Lua National University of Singapore Innovation and Upgrading pathways in the Chinese smartphone production GVC Lua Abstract This paper attends to the recent upgrading developments demonstrated by Chinese smartphone firms. Adopting a comparative approach of tearing down retail-accessible smartphones to their components, this paper traces the upgrading activities across global value chains (GVCs) that Chinese firms partake in during the production process. Upgrading is thus discovered to be diverse and complicated rather than a linear process, carrying significant implications for the production networks and supply chains in Chinese smartphone firms. Innovation and Upgrading pathways in the Chinese smartphone production GVC Lua Introduction China today is not only the world’s largest exporter of labor-intensive goods but also remains as the largest producer of personal electronics devices, surpassing the output of the US (West & Lansang, 2018). Contrary to popular belief, Chinese smartphone producers do not merely mimic their competitors, instead, innovate to “catch-up” with international competitors by upgrading across Global Value Chains (GVCs). Utilizing Liu et al. ’s (2015) illustration as a starting point, I open the dossier for both acknowledgement and critique. Figure 1. Two different expectations, two sources of mobile phone manufacturing Source: Liu et al. (2015, p. 273) This paper primarily take issue with the linear depiction of technological improvements in leading smartphone firms in Figure 1 because upgrading is a complicated process involving different strategies and forms of innovation. Instead, it argues that leading Chinese smartphone firms subscribe to a non-linear upgrading process. -

I, No:40 Sayılı Tebliği'nin 8'Nci Maddesi Gereğince, Hisse Senetleri

Sermaye Piyasas Kurulu’nun Seri :I, No:40 say l Teblii’nin 8’nci maddesi gereince, hisse senetleri Borsada i"lem gören ortakl klar n Kurul kayd nda olan ancak Borsada i"lem görmeyen statüde hisse senetlerinin Borsada sat "a konu edilebilmesi amac yla Merkezi Kay t Kurulu"u’na yap lan ba"vurulara ait bilgiler a"a da yer almaktad r. Hisse Kodu S ra Sat "a Konu Hisse Ünvan Grubu Yat r mc n n Ad -Soyad Nominal Tutar Tsp Sat " No Ünvan (TL)* 5"lemi K s t ** ** ADANA 1 ADANA Ç5MENTO E TANER BUGAY SANAY55 A.;. A GRUBU 2.235,720 ALTIN 2 ALTINYILDIZ MENSUCAT E 5SMA5L AYÇ5N VE KONFEKS5YON 0,066 FABR5KALARI A.;. ARCLK 3 ARÇEL5K A.;. E C5HAT YÜKSEKEL 31,344 ARCLK 4 ARÇEL5K A.;. E ERSAN OYMAN 19,736 ARCLK 5 ARÇEL5K A.;. E FER5DE SEZ5K 0,214 ARCLK 6 ARÇEL5K A.;. E F5L5Z EYÜPOHLU 209,141 ARCLK 7 ARÇEL5K A.;. E HANDE YED5DAL 28,180 ARCLK 8 ARÇEL5K A.;. E HAYRETT5N YAVUZ 0,206 ARCLK 9 ARÇEL5K A.;. E 5HSAN ERSEN 1.259,571 ARCLK 10 ARÇEL5K A.;. E 5RFAN ATALAY 195,262 ARCLK 11 ARÇEL5K A.;. E KEZ5BAN ONBE; 984,120 ARCLK 12 ARÇEL5K A.;. E RAFET SALTIK 23,514 ARCLK 13 ARÇEL5K A.;. E SELEN TUNÇKAYA 29,110 ARCLK 14 ARÇEL5K A.;. E YA;AR EMEK 1,142 ARCLK 15 ARÇEL5K A.;. E ZEYNEP ÖZDE GÖRKEY 2,351 ARCLK 16 ARÇEL5K A.;. E ZEYNEP SEDEF ELDEM 2.090,880 ASELS 17 ASELSAN ELEKTRON5K E ALAETT5N ÖZKÜLAHLI SANAY5 VE T5CARET A.;. -

Holdings-Report.Pdf

The Fund is a closed-end exchange traded management Investment company. This material is presented only to provide information and is not intended for trading purposes. Closed-end funds, unlike open-end funds are not continuously offered. After the initial public offering, shares are sold on the open market through a stock exchange. Changes to investment policies, current management fees, and other matters of interest to investors may be found in each closed-end fund's most recent report to shareholders. Holdings are subject to change daily. PORTFOLIO HOLDINGS FOR THE KOREA FUND as of July 31, 2021 *Note: Cash (including for these purposes cash equivalents) is not included. Security Description Shares/Par Value Base Market Value (USD) Percent of Base Market Value SAMSUNG ELECTRONICS CO 793,950 54,183,938.27 20.99 SK HYNIX INC COMMON 197,500 19,316,452.95 7.48 NAVER CORP COMMON STOCK 37,800 14,245,859.60 5.52 LG CHEM LTD COMMON STOCK 15,450 11,309,628.34 4.38 HANA FINANCIAL GROUP INC 225,900 8,533,236.25 3.31 SK INNOVATION CO LTD 38,200 8,402,173.44 3.26 KIA CORP COMMON STOCK 107,000 7,776,744.19 3.01 HYUNDAI MOBIS CO LTD 26,450 6,128,167.79 2.37 HYUNDAI MOTOR CO 66,700 6,030,688.98 2.34 NCSOFT CORP COMMON STOCK 8,100 5,802,564.66 2.25 SAMSUNG BIOLOGICS CO LTD 7,230 5,594,175.18 2.17 KB FINANCIAL GROUP INC 123,000 5,485,677.03 2.13 KAKAO CORP COMMON STOCK 42,700 5,456,987.61 2.11 HUGEL INC COMMON STOCK 24,900 5,169,415.34 2.00 SAMSUNG 29,900 4,990,915.02 1.93 SK TELECOM CO LTD COMMON 17,500 4,579,439.25 1.77 KOREA INVESTMENT 53,100 4,427,115.84 -

Sasken Technologies Limited

Sasken Technologies Limited January 07, 2019 Summary of rated instruments Previous Rated Amount Current Rated Amount Instrument* Rating Action (Rs. crore) (Rs. crore) Fund-based 50.0 50.0 [ICRA]A1+; Reaffirmed Non-fund based 40.0 40.0 [ICRA]A1+; Reaffirmed Total 90.0 90.0 *Instrument details are provided in Annexure-1 Rationale The reaffirmation of rating factors in the company’s established presence as a Information Technology (IT) service provider in the product engineering and digital transformation space, supported by its longstanding relationships with a reputed customer base spread across various geographies. While the company traditionally derived majority of its revenues from the semiconductor and telecom sectors, it is currently witnessing traction under automotive electronics, industrial automation and consumer segments, which supported YoY growth in revenues of 7.7% and 2.0% in FY2018 and H1FY2019 respectively. ICRA notes that Sasken’s operating margins expanded by 260 bps YoY to 13.8% in FY2018 from 11.2% in FY2017 supported by execution of margin-accretive complex orders, higher contribution from fixed price contracts and cost optimization. The ratings also continue to take comfort from healthy debt metrics of the company supported by nil debt and cash and liquid investments of Rs. 528.5 crore as on Sep 30, 2018. Sasken’s business prospects are further supported by healthy growth prospects in the engineering, research and development (ER&D) industry. Synergies from its legacy in semiconductor industry and strong expertise in communication and multimedia space is expected to support Sasken’s business prospects. That said, the ratings continue to be constrained by Sasken’s moderate scale of operations in a highly competitive industry marked by presence of relatively larger players constraining its pricing flexibility to a certain extent. -

STOXX Asia 100 Last Updated: 03.07.2017

STOXX Asia 100 Last Updated: 03.07.2017 Rank Rank (PREVIOU ISIN Sedol RIC Int.Key Company Name Country Currency Component FF Mcap (BEUR) (FINAL) S) KR7005930003 6771720 005930.KS KR002D Samsung Electronics Co Ltd KR KRW Y 256.2 1 1 JP3633400001 6900643 7203.T 690064 Toyota Motor Corp. JP JPY Y 128.5 2 2 TW0002330008 6889106 2330.TW TW001Q TSMC TW TWD Y 113.6 3 3 JP3902900004 6335171 8306.T 659668 Mitsubishi UFJ Financial Group JP JPY Y 83.5 4 4 HK0000069689 B4TX8S1 1299.HK HK1013 AIA GROUP HK HKD Y 77.2 5 5 JP3436100006 6770620 9984.T 677062 Softbank Group Corp. JP JPY Y 61.7 6 7 JP3735400008 6641373 9432.T 664137 Nippon Telegraph & Telephone C JP JPY Y 58.7 7 8 CNE1000002H1 B0LMTQ3 0939.HK CN0010 CHINA CONSTRUCTION BANK CORP H CN HKD Y 58.2 8 6 TW0002317005 6438564 2317.TW TW002R Hon Hai Precision Industry Co TW TWD Y 52.6 9 12 HK0941009539 6073556 0941.HK 607355 China Mobile Ltd. CN HKD Y 52.0 10 10 JP3890350006 6563024 8316.T 656302 Sumitomo Mitsui Financial Grou JP JPY Y 48.3 11 15 INE040A01026 B5Q3JZ5 HDBK.BO IN00CH HDFC Bank Ltd IN INR Y 45.4 12 13 JP3854600008 6435145 7267.T 643514 Honda Motor Co. Ltd. JP JPY Y 43.3 13 14 JP3435000009 6821506 6758.T 682150 Sony Corp. JP JPY Y 42.3 14 17 JP3496400007 6248990 9433.T 624899 KDDI Corp. JP JPY Y 42.2 15 16 CNE1000003G1 B1G1QD8 1398.HK CN0021 ICBC H CN HKD Y 41.1 16 19 JP3885780001 6591014 8411.T 625024 Mizuho Financial Group Inc. -

Premailer Middle East 2021

Bonds, Loans Shangri-La Bosphorus, Istanbul & Sukuk Turkey 2021 Turkey’s largest capital markets event www.bondsloansturkey.com 93% 50+ 20% 250+ DIRECTOR LEVEL OR ABOVE REGIONAL & INTERNATIONAL SOVEREIGN, CORPORATE & INDUSTRY EXPERT SPEAKERS BANKS ATTENDED FI BORROWERS Bonds, Loans & Sukuk Turkey has become the meeting point of all important players in finance through the correct mix of its participants, and its reliability with continuity of successful organisations in the last consecutive years Selahattin BİLGEN, IGA Airport PLATINUM SPONSOR GOLD SPONSOR BRONZE SPONSORS WELCOME TO THE ANNUAL MEETING PLACE FOR TURKEY’S FINANCE PROFESSIONALS Bonds, Loans & Sukuk Turkey is the country’s largest capital markets event. It is the only event to combine discussions across the Bond, Loans and Sukuk markets, making it a “must attend” event for the country’s leading CEOs, CFOs and Treasurers. With over 65% of the audience representing issuers and borrowers and over 93% being director level or above, it is the place where live deals are discussed and mandates are won each year. As a speaker, I had a dynamic discussion which was a great experience. Overall, the organisation was great and attracted an invaluable list of attendees. Orhan Kaya, ICBC Turkey SAVE YOURSELF SHOWCASE YOUR INCREASE TIME AND MONEY EXPERTISE IN THE REGION AWARENESS get the attendee list 2 weeks by presenting a case study by taking an exhibition space before the event so you can to a room full of potential and demonstrating your pre-arrange meetings. clients. products and services. WIN MORE INCREASE YOUR BUSINESS BRANDS PRESENCE packages include a number through the numerous of staff passes so you can branding opportunities cover more clients. -

Exports: the Heart of Nep

How to Export to 2018 Turkey This report includes all the information related to trade basics and detailed data regarding export from Brazil to Turkey. This report is for information purposes only and Tumer Eng. will not be liable to any direct, indirect, incidental, special, consequential or exemplary damages, including but not limited to, damages for loss of profits, goodwill, use, data, or other intangible losses. Ver:1.0 2018 1 Contents 1 Why Turkey.................................................................................................................................... 12 1.1 General Information .............................................................................................................. 12 1.2 Geography ............................................................................................................................. 13 1.2.1 Distances ....................................................................................................................... 18 1.2.2 Climate of Turkey .......................................................................................................... 19 1.2.2.1 Air temperature changes until now .......................................................................... 20 1.2.2.2 Precipitation changes until now ................................................................................ 21 1.2.2.3 Air temperature changes in the 21st century ........................................................... 21 1.2.2.4 Precipitation changes in the 21st century ................................................................ -

The Future Looks Bright for Android for Work

The Future Looks Bright for Android for Work The Future Looks Bright for Android for Work Whitepaper 1 The Future Looks Bright for Android for Work Abstract Since its inception, Android grew fast and by mid-2014, it had covered 80 percent of mobile phones in the market. Thereafter, its steady growth slowed due to the need for low-cost phones and the towering market share of Apple and Windows phones. Google addressed the former by launching $100 phones with AndroidOne. This move egged Android’s growth to 88 percent. In order to increase its market share by garnering more users, Google has had to attract brand loyalists of its competitors with phones that have smarter features but are available at lower costs. Authors: Krishna Kishore, Senior Architect & Vidya Krithivasan, Manager, Portfolio and Pre-Sales, Product Engineering Services 2 The Future Looks Bright for Android for Work Table of Content Introduction ............................................... 04 About The Authors .................................... 08 About Sasken ............................................ 09 Authors: Krishna Kishore, Senior Architect & Vidya Krithivasan, Manager, Portfolio and Pre-Sales, Product Engineering Services 3 The Future Looks Bright for Android for Work Introduction With more than a billion Android smartphones Traditionally, enterprise users veered towards • Restricting users to side load applications in the world today, one of the major using Blackberry and Apple devices due in enterprise profile challenges organizations face is the lack to their advanced enterprise platforms • Restricting users copying data from of control over how much official data supporting features such as: enterprise profile to personal profile might be stored and used in the employees’ • Keeping personal data separate from personal devices. -

SCHEDULE of INVESTMENTS MID-CAP 1.5X STRATEGY FUND

SCHEDULE OF INVESTMENTS December 31, 2020 MID-CAP 1.5x STRATEGY FUND SHARES VALUE SHARES VALUE COMMON STOCKS† - 39.5% United Bankshares, Inc. 118 $ 3,823 Kinsale Capital Group, Inc. 19 3,802 FINANCIAL - 9.3% Highwoods Properties, Inc. REIT 95 3,765 Medical Properties Trust, Inc. REIT 489 $ 10,655 RLI Corp. 36 3,749 Brown & Brown, Inc. 215 10,193 Park Hotels & Resorts, Inc. REIT 215 3,687 Camden Property Trust REIT 89 8,893 Selective Insurance Group, Inc. 55 3,684 CyrusOne, Inc. REIT 110 8,047 Rayonier, Inc. REIT 125 3,673 Alleghany Corp. 13 7,848 Healthcare Realty Trust, Inc. REIT 124 3,670 RenaissanceRe Holdings Ltd. 46 7,628 Valley National Bancorp 369 3,598 Omega Healthcare Investors, Inc. REIT 207 7,518 Webster Financial Corp. 82 3,456 STORE Capital Corp. REIT 216 7,340 Bank OZK 110 3,440 Reinsurance Group of Physicians Realty Trust REIT 190 3,382 America, Inc. — Class A 62 7,186 PROG Holdings, Inc. 62 3,340 Eaton Vance Corp. 104 7,065 Hudson Pacific Properties, Inc. REIT 139 3,339 Jones Lang LaSalle, Inc.* 47 6,973 Sabra Health Care REIT, Inc. 189 3,283 Signature Bank 49 6,629 Alliance Data Systems Corp. 44 3,260 Lamar Advertising Co. — Class A REIT 79 6,574 Wintrust Financial Corp. 53 3,238 East West Bancorp, Inc. 129 6,541 CIT Group, Inc. 90 3,231 National Retail Properties, Inc. REIT 159 6,506 JBG SMITH Properties REIT 102 3,190 First Horizon National Corp. 507 6,469 Sterling Bancorp 177 3,183 SEI Investments Co.