Second Annual Report of the Federal Housing Administration

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Wishful Thinking Or Buying Time? the Logic of British Appeasement in the 1930S

Wishful Thinking or Buying Time? Wishful Thinking or Norrin M. Ripsman and Buying Time? Jack S. Levy The Logic of British Appeasement in the 1930s The “lessons of the 1930s,” based on British and French appeasement of Germany, have pro- foundly inºuenced U.S. security policy for a half century. Presidents have invoked these lessons in decisions for war in Korea, Vietnam, and Iraq in 1990–91 and 2003, and in presidential campaigns.1 Among policymakers and publics, and among many scholars as well, the futility of appeasement has ac- quired the status of a lawlike generalization.2 The implicit assumption is that the Western allies’ primary aim was to secure a lasting peace with Germany through concessions to resolve Adolf Hitler’s grievances. If that was the aim, the policy clearly failed. But, as we shall demonstrate, that was not appease- ment’s primary aim. Scholars need to rethink both the concept of appeasement and the goals of appeasement in the 1930s. The popular image of appeasement was fueled by the scholarship of tra- ditional historians, who condemned British and French appeasement of Germany as politically naïve and morally bankrupt. In their view, the policies Norrin M. Ripsman is Associate Professor in the Department of Political Science at Concordia University. He is the author of Peacemaking by Democracies: The Effect of State Autonomy on the Post–World War Settlements (University Park: Penn State University Press, 2002). Jack S. Levy is Board of Gover- nors’ Professor of Political Science at Rutgers University, Senior Associate at the Arnold A. Saltzman Insti- tute of War and Peace Studies at Columbia University, and past president of both the International Studies Association (2007–08) and the Peace Science Society (2005–06). -

Records of the Immigration and Naturalization Service, 1891-1957, Record Group 85 New Orleans, Louisiana Crew Lists of Vessels Arriving at New Orleans, LA, 1910-1945

Records of the Immigration and Naturalization Service, 1891-1957, Record Group 85 New Orleans, Louisiana Crew Lists of Vessels Arriving at New Orleans, LA, 1910-1945. T939. 311 rolls. (~A complete list of rolls has been added.) Roll Volumes Dates 1 1-3 January-June, 1910 2 4-5 July-October, 1910 3 6-7 November, 1910-February, 1911 4 8-9 March-June, 1911 5 10-11 July-October, 1911 6 12-13 November, 1911-February, 1912 7 14-15 March-June, 1912 8 16-17 July-October, 1912 9 18-19 November, 1912-February, 1913 10 20-21 March-June, 1913 11 22-23 July-October, 1913 12 24-25 November, 1913-February, 1914 13 26 March-April, 1914 14 27 May-June, 1914 15 28-29 July-October, 1914 16 30-31 November, 1914-February, 1915 17 32 March-April, 1915 18 33 May-June, 1915 19 34-35 July-October, 1915 20 36-37 November, 1915-February, 1916 21 38-39 March-June, 1916 22 40-41 July-October, 1916 23 42-43 November, 1916-February, 1917 24 44 March-April, 1917 25 45 May-June, 1917 26 46 July-August, 1917 27 47 September-October, 1917 28 48 November-December, 1917 29 49-50 Jan. 1-Mar. 15, 1918 30 51-53 Mar. 16-Apr. 30, 1918 31 56-59 June 1-Aug. 15, 1918 32 60-64 Aug. 16-0ct. 31, 1918 33 65-69 Nov. 1', 1918-Jan. 15, 1919 34 70-73 Jan. 16-Mar. 31, 1919 35 74-77 April-May, 1919 36 78-79 June-July, 1919 37 80-81 August-September, 1919 38 82-83 October-November, 1919 39 84-85 December, 1919-January, 1920 40 86-87 February-March, 1920 41 88-89 April-May, 1920 42 90 June, 1920 43 91 July, 1920 44 92 August, 1920 45 93 September, 1920 46 94 October, 1920 47 95-96 November, 1920 48 97-98 December, 1920 49 99-100 Jan. -

Commodity Price Movements in 1936 by Roy G

March 1937 March 1937 SURVEY OF CURRENT BUSINESS 15 Commodity Price Movements in 1936 By Roy G. Blakey, Chief, Division of Economic Research HANGES in the general level of wholesale prices to 1933 also rose most rapidly during 1936 as they did C during the first 10 months of 1936 were influenced in the preceding 3 years. (See fig. 1.) mostly by the fluctuations of agricultural prices, with The annual index of food prices was 1.9 percent lower nonagricultural prices moving approximately horizon- for 1936 than for 1935, but the index of farm products tally. Agricultural prices, after having risen sharply as was 2.7 percent and the index of prices of all commodi- a result of the 1934 drought, moved lower during the ties other than farm products and foods was 2.2 per- first 4% months of 1936 on prospects for increased INDEX NUMBERS (Monthly average, 1926= lOO) supplies. When the 1936 trans-Mississippi drought 1201 • • began to appear serious, however, agricultural prices turned up sharply and carried the general price average -Finished Products with them. The rapid rise during the summer was suc- / ceeded by a lull in September and October, but imme- 60 diately following the November election there was a -Row Maferia/s sharp upward movement of most agricultural prices at the same time that a marked rise in nonagricultural products was experienced. The net result of these 1929 1930 1952 1934 I9?6 divergent movements was a 1-percent increase in the Figure 1.—Wholesale Prices by Economic Classes, 1929-36 (United 1936 annual average of the Bureau of Labor Statistics States Department of Labor). -

Federal Reserve Bulletin June 1935

FEDERAL RESERVE BULLETIN JUNE 1935 ISSUED BY THE FEDERAL RESERVE BOARD AT WASHINGTON Business and Credit Conditions Industrial Advances by Federal Reserve Banks Annual Report of the Bank for International Settlements UNITED STATES GOVERNMENT PRINTING OFFICE WASHINGTON: 1935 Digitized for FRASER http://fraser.stlouisfed.org/ Federal Reserve Bank of St. Louis FEDERAL RESERVE BOARD Ex-officio members: MARRINER S. ECCLES, Governor. HENRY MORGENTHAU, Jr., J. J. THOMAS, Vice Governor. Secretary of the Treasury, Chairman, CHARLES S. HAMLIN. J. F. T. O'CONNOR, ADOLPH C. MILLER. Comptroller of the Currency. GEORGE R. JAMES. M. S. SZYMCZAK. LAWRENCE CLAYTON, Assistant to the Governor. LAUCHLIN CURRIE, Assistant Director, Division of ELLIOTT L. THURSTON, Special Assistant to the Governor. Research and Statistics. CHESTER MORRILL, Secretary. WOODLIEF THOMAS, Assistant Director, Division of J. C. NOELL, Assistant Secretary. Research and Statistics. LISTON P. BETHEA, Assistant Secretary. E. L. SMEAD, Chief, Division of Bank Operations. S. R. CARPENTER, Assistant Secretary. J. R. VAN FOSSEN, Assistant Chief, Division of Bank WALTER WYATT, General Counsel. Operations. GEORGE B. VEST, Assistant General Counsel. J. E. HORBETT, Assistant Chief, Division of Bank B. MAGRUDER WINGFIELD, Assistant General Counsel. Operations. LEO H. PAULGER, Chief, Division of Examinations. CARL E. PARRY, Chief, Division of Security Loans. R. F. LEONARD, Assistant Chief, Division of Examina- PHILIP E. BRADLEY, Assistant Chief, Division of Security tions. Loans. C. E. CAGLE, Assistant Chief, Division of Examinations. O. E. FOULK, Fiscal Agent. FRANK J. DRINNEN, Federal Reserve Examiner. JOSEPHINE E. LALLY, Deputy Fiscal Agent. E. A. GOLDENWEISER, Director, Division of Research and Statistics. FEDERAL ADVISORY COUNCIL District no. -

Chapter Three: Daily Life in the Public Domain, 1933–1938

125 Chapter Three: Daily Life in the Public Domain, 1933–1938 Nazi Policy toward the Jews The introduction and the implementation of Nazi policy toward the Jews affected them in all aspects of their lives, including the public domain. As the years progressed, their level of insecurity and lack of safety escalated. Whether policy dealt with public or private space, Jewish or non-Jewish space was inconsequential. All policy was engineered toward the demonisation, humiliation and exclusion of Jews from all spheres of life and influence in Germany. Included in this was their constant surveillance as declared ‘enemies of the German people.’ All policy also affected the behaviours and attitudes of non-Jews towards Jews in the public domain, as Jews had been allocated pariah status. In depicting the effect of Nazi policy on the daily lives of Jews in the city from 1933 until the pogrom in November 1938, a similar pattern corresponding to the time-line of economic disenfranchisement emerges. The initial shock and violence of 1933 was followed by a period of adjustment to their new and disturbing status.1 Ongoing boycotts and public defamation, combined with the exclusion from some public places, were the main features until the introduction of the Nuremberg Laws in 1935. After September 1935 Jews no longer possessed any legal status and were racially defined. This led to an open season of accusing Jews of either invented crimes or newly created crimes, such as ‘Rassenschande.’ In Magdeburg this resulted in show trials and the trial by media of a number of community members. -

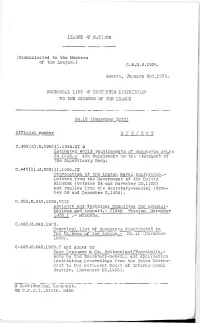

C.6.M.5.1936. Geneva, January 2Nd,1936<, NUMERICAL LIST OF

LEAGUE OF NATIONS (Communicated to the Members of the League.) C.6.M.5.1936. Geneva, January 2nd,1936<, NUMERICAL LIST OF DOCUMENTS DISTRIBUTED TO THE MEMBERS OF THE LEAGUE No.12 (December 1935) Officiel number S U B J E__C T C.462(d).M,198(d).1934.XI ® Estimated world requirements of dangerous drugs in 1955,- 4th Supplement to the statement of the Supervisory Body. C.445(1).M.233(1).1935.IX Convocation of the London Nava 1 Conf e ren c e_, - Letters from the Government of the United Kingdom (October 24 and November 30,1935) and replies from the Secretary-General (Octo ber 30 and December 2,1935). C .458.M.240.1935.VIII Advisory and Technical Comraittee for communi cations and transit.-- (19th bession, November 1935.) . - Records. C.462.M.242.1935. Numerical list of documents distributed_to the Members of the League,- No.il (November 1935). C.463.M.243,1935„V and Annex @3 Case Lo singer & Co. Sw i tz_e r] .and/Yugos lav la. - Nore by the Secretary-General and Application instituting proceedings from the Swiss Govern ment to the Permanent Court of International Justifie. (November 23,1935). @ Confidential document. C.P.J.I.,Distr. 3420 - 2 - Cv464.M.244.1935.Ill and Annex @ In te r-G_) vernmen t al Conference on. _ b i_o1 o^ioal ste.ndardJ. sati on J October 1935).- I-lote by the Secretary-General and report. C.467.M.245,1935.VII Dlsp ute bet ween Et h lopi a. a rid _It aly Tel eg ram from the Ethiopian Government (December 2, 1935), C.469,IVU246» 1935»V and Erratum to numbering, @@ Composition of the_ Çhamb er _ f or Suinma ry_ Pro ce - du rn_ o f the P e rmane nt_ Court of International _ Justice.- Note by the éucretary-Generaï. -

Special Libraries, April 1935

San Jose State University SJSU ScholarWorks Special Libraries, 1935 Special Libraries, 1930s 4-1-1935 Special Libraries, April 1935 Special Libraries Association Follow this and additional works at: https://scholarworks.sjsu.edu/sla_sl_1935 Part of the Cataloging and Metadata Commons, Collection Development and Management Commons, Information Literacy Commons, and the Scholarly Communication Commons Recommended Citation Special Libraries Association, "Special Libraries, April 1935" (1935). Special Libraries, 1935. 4. https://scholarworks.sjsu.edu/sla_sl_1935/4 This Book is brought to you for free and open access by the Special Libraries, 1930s at SJSU ScholarWorks. It has been accepted for inclusion in Special Libraries, 1935 by an authorized administrator of SJSU ScholarWorks. For more information, please contact [email protected]. I I SPECIAL LIBRARIES "Putting Knowledge to Work" - - VOLUME 26 APRIL 9935 NUMBER 4 University Press and the Special Library-Joseph A. Duffy, Jr.. 83 Membership Campaign-Your Share in It-Adeline M. Macrum . 85 To Aid Collectors of Municipal Documents-Josephine 6. Hollingsworth . 86 Reading Notes. .. 87 Special Libraries Directory of United States and Canada . 88 Special Library Survey The Banking LibraryAlta B. Claflin. 90 I Conference News. .. 93 Nominating Committee Report . 95 Snips and Snipes. '. , . , 96 "We Do This". 97 Business Book Review Digest . 98 Whither Special Library Classifications? . 99 New Books Received . 100 Publications of Special Interest. 101 Duplicate Exchange List. , . 104 indexed in industrial Arts index and Public Affairs information Service SPECIAL LIBRARIES published monthly September to April with bi-month1 isrues May to August, by The S ecial Libraries Assodation at 10 Fen streit Concord, N. k. Subscri tion Offices, 10 Fen &met, Concord, N. -

An Earthquake Hits STAMPEX: Quetta 1935

An Earthquake hits STAMPEX: Quetta 1935 Building an Exhibit from a Tragedy Contributed by Neil Donen Neil with his ‘salt of the earth’ philatelic wife Nancy Number 3.2 October 2018 A Rare Opportunity - not to be Missed Sometimes we are presented with an opportunity which just we cannot pass up. It is a foolish man who will turn this down. So when Neil Donen agreed that we could share his Exhibit on the Quetta Earthquake, displayed at the Autumn 2018 STAMPEX with us, it was one of those moments. I was more than delighted to welcome an authoritative and insightful addition to our third set of Occasional Papers Neil’s display fitted the agenda set for our Occasional Publications perfectly: • It tells a story which is compellingly interesting; • It introduces what is for many, a new angle on Indian Philately; • It puts humanity at the centre where we can find examples of bravery, resourcefulness, empathy, organizational capacity, kindness and essential optimism; • It is a self-contained fragment from history; • It is a study which can be limited to just 14 days or be extended into the days and years preceding the earthquake and into the aftermath of its consequences; • It poses many unanswered questions which will require further research and thought to reach a conclusion. Many members of the ISC will already have read some of the research work already undertaken by Neil Donen in India Post 52/2 (2018) No. 207. He makes a compelling case for research in these misty areas to be undertaken on a collaborative basis. -

Inventory Dep.288 BBC Scottish

Inventory Dep.288 BBC Scottish National Library of Scotland Manuscripts Division George IV Bridge Edinburgh EH1 1EW Tel: 0131-466 2812 Fax: 0131-466 2811 E-mail: [email protected] © Trustees of the National Library of Scotland Typescript records of programmes, 1935-54, broadcast by the BBC Scottish Region (later Scottish Home Service). 1. February-March, 1935. 2. May-August, 1935. 3. September-December, 1935. 4. January-April, 1936. 5. May-August, 1936. 6. September-December, 1936. 7. January-February, 1937. 8. March-April, 1937. 9. May-June, 1937. 10. July-August, 1937. 11. September-October, 1937. 12. November-December, 1937. 13. January-February, 1938. 14. March-April, 1938. 15. May-June, 1938. 16. July-August, 1938. 17. September-October, 1938. 18. November-December, 1938. 19. January, 1939. 20. February, 1939. 21. March, 1939. 22. April, 1939. 23. May, 1939. 24. June, 1939. 25. July, 1939. 26. August, 1939. 27. January, 1940. 28. February, 1940. 29. March, 1940. 30. April, 1940. 31. May, 1940. 32. June, 1940. 33. July, 1940. 34. August, 1940. 35. September, 1940. 36. October, 1940. 37. November, 1940. 38. December, 1940. 39. January, 1941. 40. February, 1941. 41. March, 1941. 42. April, 1941. 43. May, 1941. 44. June, 1941. 45. July, 1941. 46. August, 1941. 47. September, 1941. 48. October, 1941. 49. November, 1941. 50. December, 1941. 51. January, 1942. 52. February, 1942. 53. March, 1942. 54. April, 1942. 55. May, 1942. 56. June, 1942. 57. July, 1942. 58. August, 1942. 59. September, 1942. 60. October, 1942. 61. November, 1942. 62. December, 1942. 63. January, 1943. -

1935 Annual Report

ANNUAL REPORT OF THE FEDERAL DEPOSIT INSURANCE CORPORATION FOR THE YEAR ENDING DECEMBER 31, 1935 Digitized for FRASER http://fraser.stlouisfed.org/ Federal Reserve Bank of St. Louis Digitized for FRASER http://fraser.stlouisfed.org/ Federal Reserve Bank of St. Louis LETTER OF TRANSMITTAL Federal Deposit Insurance Corporation, Washington, D. C., September 1, 1936. SIR: Pursuant to the provisions of subsection (r) of section 12B of the Federal Reserve Act, as amended, the Federal Deposit Insurance Corporation has the honor to submit its annual report. Respectfully, Leo T. Crowley, Chairman. T h e P r e s id e n t o f t h e S e n a t e T h e Sp e a k e r o f t h e H o u s e o f R epresentatives Digitized for FRASER http://fraser.stlouisfed.org/ Federal Reserve Bank of St. Louis Digitized for FRASER http://fraser.stlouisfed.org/ Federal Reserve Bank of St. Louis CONTENTS Page Introduction............................................................................................................................. 3 PART ONE OPERATIONS OF THE CORPORATION DURING THE YEAR ENDING DECEMBER 31, 1935 Inauguration of permanent plan of insurance of bank deposits.......................... 7 Organization and staff.......................................................................................................... 8 Financial aspects of the Corporation............................................................................. 9 Payments.to depositors in suspended insured banks............................................... 11 Liquidation of insured -

Maine Alumnus, Volume 16, Number 6, March 1935

The University of Maine DigitalCommons@UMaine University of Maine Alumni Magazines University of Maine Publications 3-1935 Maine Alumnus, Volume 16, Number 6, March 1935 General Alumni Association, University of Maine Follow this and additional works at: https://digitalcommons.library.umaine.edu/alumni_magazines Part of the Higher Education Commons, and the History Commons Recommended Citation General Alumni Association, University of Maine, "Maine Alumnus, Volume 16, Number 6, March 1935" (1935). University of Maine Alumni Magazines. 406. https://digitalcommons.library.umaine.edu/alumni_magazines/406 This publication is brought to you for free and open access by DigitalCommons@UMaine. It has been accepted for inclusion in University of Maine Alumni Magazines by an authorized administrator of DigitalCommons@UMaine. For more information, please contact [email protected]. AN ENGINEERING COURSE AIMS TO DEVELOP 4 • 1. HONESTY AND INTEGRITY 2. SOUND JUDGMENT 3 DESIRE TO SERVE 4 POWER TO VISUALIZE 5 ABILITY TO THINK 6. COOPERATIVE ATTITUDE Wixgaie Hall 7 BROAD KNOWLEDGE OI MEN AND AFFAIRS 8. APPRECIATION OF ART, SCIENCE, AND LI IT RAT URL And Provides Specific Training in CHEMISTRY CHEMICAL ENGINEERING CIVIL ENGINEERING ELECTRICAL ENGINEERING GENERAL ENGINEERING MECHANICAL ENGINEERING PULP AND PAPER TECHNOLOGY COLLEGE of TECHNOLOGY UNIVERSITY of MAINE PAUL CLOKE, ENG.D. Dean, College of Technology Director, Maine Technology Experiment Station ahr lliatur Alumnus Vol. 16, No. 6 March, 1935 Technology Courses Revised To Meet Changing Conditions By Dean Paul Cloke • I HE engineer is an incurable opti soon be used as a basis for graduation. Faculty Is Active in Public Service mist at the same time that he is one In fact the writer hopes that soon these Tof the humblest of God’s creatures. -

1935 Sanctions Against Italy: Would Coal and Crude Oil Have Made a Difference?

1935 SANCTIONS AGAINST ITALY: WOULD COAL AND CRUDE OIL HAVE MADE 1 A DIFFERENCE? CRISTIANO ANDREA RISTUCCIA LINACRE COLLEGE OXFORD OX1 3JA GREAT BRITAIN Telephone 44 1865 721981 [email protected] 1 Thanks to (in alphabetical order): Dr. Leonardo Becchetti, Sergio Cardarelli (and staff of the ASBI), Criana Connal, John Fawcett, Prof. Charles Feinstein, Dr. James Foreman-Peck, Paola Geretto (and staff of the ISTAT library and archive), Gwyneira Isaac, Clare Pettitt, Prof. Maria Teresa Salvemini, Prof. Giuseppe Tattara, Leigh Shaw-Taylor, Prof. Gianni Toniolo, Dr. Marco Trombetta, and two anonymous referees who made useful comments on a previous version of this paper. The responsibility for the contents of the article is, of course, mine alone. ABSTRACT This article assesses the hypothesis that in 1935 - 1936 the implementation of sanctions on the export of coal and oil products to Italy by the League of Nations would have forced Italy to abandon her imperialistic war against Ethiopia. In particular, the article focuses on the claim that Britain and France, the League’s leaders, could have halted the Italian invasion of Ethiopia by means of coal and oil sanctions, and without the help of the United States, or recourse to stronger means such as a military blockade. An analysis of the data on coal consumption in the industrial census of 1937 - 1938 shows that the Italian industry would have survived a League embargo on coal, provided that Germany continued her supply to Italy. The counterfactual proves that the effect of an oil embargo was entirely dependent on the attitude of the United States towards the League’s action.