Download Report

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

List of Village Panchayats in Tamil Nadu District Code District Name

List of Village Panchayats in Tamil Nadu District Code District Name Block Code Block Name Village Code Village Panchayat Name 1 Kanchipuram 1 Kanchipuram 1 Angambakkam 2 Ariaperumbakkam 3 Arpakkam 4 Asoor 5 Avalur 6 Ayyengarkulam 7 Damal 8 Elayanarvelur 9 Kalakattoor 10 Kalur 11 Kambarajapuram 12 Karuppadithattadai 13 Kavanthandalam 14 Keelambi 15 Kilar 16 Keelkadirpur 17 Keelperamanallur 18 Kolivakkam 19 Konerikuppam 20 Kuram 21 Magaral 22 Melkadirpur 23 Melottivakkam 24 Musaravakkam 25 Muthavedu 26 Muttavakkam 27 Narapakkam 28 Nathapettai 29 Olakkolapattu 30 Orikkai 31 Perumbakkam 32 Punjarasanthangal 33 Putheri 34 Sirukaveripakkam 35 Sirunaiperugal 36 Thammanur 37 Thenambakkam 38 Thimmasamudram 39 Thilruparuthikundram 40 Thirupukuzhi List of Village Panchayats in Tamil Nadu District Code District Name Block Code Block Name Village Code Village Panchayat Name 41 Valathottam 42 Vippedu 43 Vishar 2 Walajabad 1 Agaram 2 Alapakkam 3 Ariyambakkam 4 Athivakkam 5 Attuputhur 6 Aymicheri 7 Ayyampettai 8 Devariyambakkam 9 Ekanampettai 10 Enadur 11 Govindavadi 12 Illuppapattu 13 Injambakkam 14 Kaliyanoor 15 Karai 16 Karur 17 Kattavakkam 18 Keelottivakkam 19 Kithiripettai 20 Kottavakkam 21 Kunnavakkam 22 Kuthirambakkam 23 Marutham 24 Muthyalpettai 25 Nathanallur 26 Nayakkenpettai 27 Nayakkenkuppam 28 Olaiyur 29 Paduneli 30 Palaiyaseevaram 31 Paranthur 32 Podavur 33 Poosivakkam 34 Pullalur 35 Puliyambakkam 36 Purisai List of Village Panchayats in Tamil Nadu District Code District Name Block Code Block Name Village Code Village Panchayat Name 37 -

Thiruvallur District

DISTRICT DISASTER MANAGEMENT PLAN FOR 2017 TIRUVALLUR DISTRICT tmt.E.sundaravalli, I.A.S., DISTRICT COLLECTOR TIRUVALLUR DISTRICT TAMIL NADU 2 COLLECTORATE, TIRUVALLUR 3 tiruvallur district 4 DISTRICT DISASTER MANAGEMENT PLAN TIRUVALLUR DISTRICT - 2017 INDEX Sl. DETAILS No PAGE NO. 1 List of abbreviations present in the plan 5-6 2 Introduction 7-13 3 District Profile 14-21 4 Disaster Management Goals (2017-2030) 22-28 Hazard, Risk and Vulnerability analysis with sample maps & link to 5 29-68 all vulnerable maps 6 Institutional Machanism 69-74 7 Preparedness 75-78 Prevention & Mitigation Plan (2015-2030) 8 (What Major & Minor Disaster will be addressed through mitigation 79-108 measures) Response Plan - Including Incident Response System (Covering 9 109-112 Rescue, Evacuation and Relief) 10 Recovery and Reconstruction Plan 113-124 11 Mainstreaming of Disaster Management in Developmental Plans 125-147 12 Community & other Stakeholder participation 148-156 Linkages / Co-oridnation with other agencies for Disaster 13 157-165 Management 14 Budget and Other Financial allocation - Outlays of major schemes 166-169 15 Monitoring and Evaluation 170-198 Risk Communications Strategies (Telecommunication /VHF/ Media 16 199 / CDRRP etc.,) Important contact Numbers and provision for link to detailed 17 200-267 information 18 Dos and Don’ts during all possible Hazards including Heat Wave 268-278 19 Important G.Os 279-320 20 Linkages with IDRN 321 21 Specific issues on various Vulnerable Groups have been addressed 322-324 22 Mock Drill Schedules 325-336 -

S.No. Shop Address 1 Anna Nagar Shanthi Colony

S.No. Shop Address Anna Nagar Shanthi Colony Aa-144, 2nd Floor, 3rd Avenue, (Next To Waves) Anna Nagar, Ch-600040. 1 Anna Nagar West No 670,Sarovar Building, School Road, Anna Nagar West, Chennai - 600101. 2 Mogappair East 4/491, Pari Salai, Mogappair East, (Near Tnsc Bank) Ch-600037 3 Mogappair West 1 Plot No.4, 1st Floor, Phase I, Nolambur,(Near Reliance Fresh) Mogappair 4 West, Ch-600037. Annanagar West Extn Plot No: R48, Door No - 157, Tvs Avenue Main Road,Anna Nagar West 5 Extension,Chennai - 600 101. Opp To Indian Overseas Bank. Red Hills 1/172a, Gnt Road, 2nd Floor, Redhills-Chennai:52. Above Lic, Next To Iyappan 6 Temple K.K.Nagar 2 No.455, R.K.Shanuganathan Road, K K Nagar, Land Mark:Near By K M 7 Hospital, Chennai - 600 078 Tiruthani No. 9, Chittoor Road, Thirutani - 631 209 8 Anna Nagar (Lounge) C Block, No. 70, Tvk Colony, Annanagar East, Chennai - 102. 9 K.K.Nagar 1 Plot No 1068, 1st Floor, Munuswami Salai, (Opp To Nilgiri Super Market) 10 K.K.Nagar West, Ch-600078. Alapakkam No. 21, 1st Floor, Srinivasa Nagar,Alapakkam Main 11 Road,Maduravoyal,Chennai 600095 Mogappair West 2 No-113, Vellalar Street, Mogappair West, Chennai -600 037. 12 Poonamalle # 35, Trunk Road, Opp To Grt Poonamalle Chennai-600056. 13 Karayanchavadi N0. 70, Trunk Road, Karayanchavadi, Poonamallee, Chennai - 56 14 Annanagar 6th Avenue 6th Avenue,Anna Nagar,Chennai 15 Chetpet Opp To Palimarhotel,73,Casamajorroad,Egmore,Ch-600008 16 Egmore Lounge 74/26,Fagunmansion,Groundfloor,Nearethirajcollege,Egmore,Chennai-600008 17 Nungambakkam W A-6, Gems Court, New.25 (Old No14), Khader Nawaz Khan Road, (Opp Wills 18 Life Style) Nungambakkam, Ch-600034. -

Family Gender by Club MBR0018

Summary of Membership Types and Gender by Club as of December, 2014 Club Fam. Unit Fam. Unit Club Ttl. Club Ttl. Student Leo Lion Young Adult District Number Club Name HH's 1/2 Dues Females Male Total Total Total Total District 324A8 26420 GUINDY 0 0 0 19 0 0 0 19 District 324A8 29825 MADRAS NANDAMBAKKAM 0 0 0 9 0 0 0 9 District 324A8 38224 MADRAS MAMBALAM 5 5 10 17 0 0 0 27 District 324A8 46672 MADRAS ROYAPURAM 3 4 5 60 0 0 0 65 District 324A8 49717 MADRAS DOVETON SQUARE 2 3 4 22 0 0 0 26 District 324A8 51004 MADRAS TEMPLE CITY 4 4 4 11 0 0 0 15 District 324A8 57250 MADRAS BALAJI AVENUE 3 3 7 4 0 0 0 11 District 324A8 57259 MADRAS SUN CITY 0 0 0 1 0 0 0 1 District 324A8 62740 MADRAS ANNAI 2 3 5 17 0 0 0 22 District 324A8 63077 MADRAS TECHNOCITY 4 5 14 45 0 0 0 59 District 324A8 65189 CHENNAI ANNA NAGAR TOWERS 13 20 16 25 0 0 0 41 District 324A8 68554 CHENNAI ROSES 4 4 4 20 0 0 0 24 District 324A8 77785 CHENNAI PRIME 1 1 1 14 0 0 0 15 District 324A8 98013 CHENNAI HEAVEN CITY 3 4 4 6 0 0 0 10 District 324A8 99966 CHENNAI GATEWAY 10 12 10 16 0 0 0 26 District 324A8 99967 CHENNAI METRO MATHUR 0 0 0 15 0 0 0 15 District 324A8 103357 CHENNAI SIKSHA 15 17 20 21 0 0 0 41 District 324A8 105316 CHENNAI GREEN CITY 0 0 1 2 0 0 0 3 District 324A8 105317 CHENNAI ACCORD 0 0 0 3 0 0 0 3 District 324A8 105318 CHENNAI STAR CITY 2 2 2 4 0 0 0 6 District 324A8 105320 CHENNAI ASPIRE 3 6 5 11 0 0 0 16 District 324A8 105321 CHENNAI ACCENT 0 0 5 14 0 0 0 19 District 324A8 105322 CHENNAI CHANDRAYAN 0 0 1 2 0 0 0 3 District 324A8 109044 CHENNAI PRINCE 4 5 7 22 -

15 Sub Ptt MSB-TBM-CGL DOWN WEEK DAYS

CHENNAI BEACH - TAMBARAM - CHENGALPATTU DOWN WEEK DAYS Train Nos 40501 40001 40503 40505 40507 40701 40509 Kms Stations CJ 0 Chennai Beach d 03:55 04:15 04:35 04:55 05:15 05:30 05:50 2 Chennai Fort d 03:59 04:19 04:39 04:59 05:19 05:34 05:54 4 Chennai Park d 04:02 04:22 04:42 05:02 05:22 05:37 05:57 5 Chennai Egmore d 04:05 04:25 04:45 05:05 05:25 05:40 06:00 7 Chetpet d 04:08 04:28 04:48 05:08 05:28 05:43 06:03 9 Nungambakkam d 04:11 04:31 04:51 05:11 05:31 05:46 06:06 10 Kodambakkam d 04:13 04:33 04:53 05:13 05:33 05:48 06:08 12 Mambalam d 04:15 04:35 04:55 05:15 05:35 05:50 06:10 13 Saidapet d 04:18 04:38 04:58 05:18 05:38 05:53 06:13 16 Guindy d 04:21 04:41 05:01 05:21 05:41 05:56 06:16 18 St.Thomas Mount d 04:24 04:44 05:04 05:24 05:44 05:59 06:19 19 Palavanthangal d 04:27 04:47 05:07 05:27 05:47 06:02 06:22 21 Minambakkam d 04:30 04:50 05:10 05:30 05:50 06:05 06:25 22 Tirusulam d 04:32 04:52 05:12 05:32 05:52 06:07 06:27 24 Pallavaram d 04:35 04:55 05:15 05:35 05:55 06:10 06:30 26 Chrompet d 04:38 04:58 05:18 05:38 05:58 06:13 06:33 29 Tambaram Sanatorium d 04:41 05:01 05:21 05:41 06:01 06:16 06:36 30 Tambarm a 05:10 d 04:50 05:30 05:50 06:10 06:25 06:45 34 Perungulathur d 04:56 05:36 05:56 06:16 06:32 06:56 36 Vandalur d 04:59 05:39 05:59 06:19 06:35 06:59 39 Urappakkam d 05:03 05:43 06:03 06:23 06:39 07:03 42 Guduvancheri d 05:07 05:47 06:07 06:27 06:43 07:07 44 Potheri d 05:11 05:51 06:11 06:31 06:47 07:11 46 Kattangulathur d 05:14 05:54 06:14 06:34 06:50 07:14 47 Maraimalai Nagar d 05:16 05:56 06:16 06:36 06:52 07:16 51 Singaperumal -

INDIAN OVERSEAS BANK Royapuram Branch 62/153 & 63/155 MS Koil Street Royapuram, Chennai

INDIAN OVERSEAS BANK Royapuram Branch 62/153 & 63/155 M S Koil Street Royapuram, Chennai – 600013 PH: 044-25953208 25952550 Email:[email protected] e-AUCTION SALE NOTICE FOR SALE OF IMMOVABLE PROPERTIES E-Auction Sale Notice for Sale of Immovable Assets under the Securitisation and Reconstruction of Financial Assets and Enforcement of Security Interest Act, 2002 read with proviso to Rule 8 (6) of the Security Interest (Enforcement) Rules, 2002. To 1.Mrs S Durga, 8B Meenakshi Bharathi Co Op garden, Moolachatram, Madhavaram Milk colony, Chennai 600 051 2.Mr. Kandhavel Rajaram, 8B Meenakshi Bharathi Co Op garden, Moolachatram, Madhavaram Milk colony, Chennai 600 051 Sir/Madam, Notice is hereby given to the public in general and in particular to the borrower (s) and guarantor (s) that the below described immovable property mortgaged/charged to the Secured Creditor, the constructive possession of which has been taken by the Authorised Officer of Indian Overseas Bank, Secured Creditor, will be sold on “As is where is”, “As is what is” and “Whatever there is” on 21.10.2020 for recovery of Rs 59,47,371.00 (Rupees Fifty Nine Lacs Forty Seven Thousands Three Hundred and Seventy One only) as on 30.09.2020 due to the Indian Overseas Bank, Secured Creditor from the borrower (s): 1. Mrs S Durga, 8B Meenakshi Bharathi Co Op garden, Moolachatram, Madhavaram Milk colony, Chennai 600 051 2. Mr. Kandhavel Rajaram, 8B Meenakshi Bharathi Co Op garden, Moolachatram, Madhavaram Milk colony, Chennai 600 051 The reserve price will be Rs. 23,00,000.00 and the earnest money deposit will be Rs. -

SNO APP.No Name Contact Address Reason 1 AP-1 K

SNO APP.No Name Contact Address Reason 1 AP-1 K. Pandeeswaran No.2/545, Then Colony, Vilampatti Post, Intercaste Marriage certificate not enclosed Sivakasi, Virudhunagar – 626 124 2 AP-2 P. Karthigai Selvi No.2/545, Then Colony, Vilampatti Post, Only one ID proof attached. Sivakasi, Virudhunagar – 626 124 3 AP-8 N. Esakkiappan No.37/45E, Nandhagopalapuram, Above age Thoothukudi – 628 002. 4 AP-25 M. Dinesh No.4/133, Kothamalai Road,Vadaku Only one ID proof attached. Street,Vadugam Post,Rasipuram Taluk, Namakkal – 637 407. 5 AP-26 K. Venkatesh No.4/47, Kettupatti, Only one ID proof attached. Dokkupodhanahalli, Dharmapuri – 636 807. 6 AP-28 P. Manipandi 1stStreet, 24thWard, Self attestation not found in the enclosures Sivaji Nagar, and photo Theni – 625 531. 7 AP-49 K. Sobanbabu No.10/4, T.K.Garden, 3rdStreet, Korukkupet, Self attestation not found in the enclosures Chennai – 600 021. and photo 8 AP-58 S. Barkavi No.168, Sivaji Nagar, Veerampattinam, Community Certificate Wrongly enclosed Pondicherry – 605 007. 9 AP-60 V.A.Kishor Kumar No.19, Thilagar nagar, Ist st, Kaladipet, Only one ID proof attached. Thiruvottiyur, Chennai -600 019 10 AP-61 D.Anbalagan No.8/171, Church Street, Only one ID proof attached. Komathimuthupuram Post, Panaiyoor(via) Changarankovil Taluk, Tirunelveli, 627 761. 11 AP-64 S. Arun kannan No. 15D, Poonga Nagar, Kaladipet, Only one ID proof attached. Thiruvottiyur, Ch – 600 019 12 AP-69 K. Lavanya Priyadharshini No, 35, A Block, Nochi Nagar, Mylapore, Only one ID proof attached. Chennai – 600 004 13 AP-70 G. -

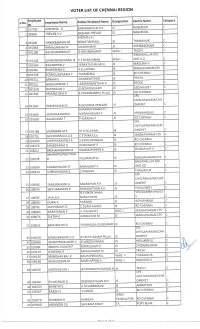

Voter List Chennai Region.Pdf

VOTER LIST OF CHENNAI REGION Employee Name Designation Centre Name Category S.No. Employee Name Father/Husband ID NAGERCOIL I 0t7t8c SOBHANA. O SANKARAPILLAI P.K IS NAGERCOIL L u)v)oL THEVAN.K.V KRISHNA THEVAR JS MICHAEL S / L JS THANJAVUR 3 09104J VANAKKAMARY M SEBASTIAMMAL ts KUMBAKONAM L 4 09108A RAMALINGAM M MANICKAM K C WAG- I TRICHY 5 091168 RAVICHANDRAN.G G.GOVINDASAMY )II\€AI\ALLU C WAG- I AND ICD 6 091338 CHANDRASEKARAN .N K S NARAYANAN K. JS MADURAI.II c 7 19146D RAJENDRAN.V VENKATACHALAM JS MADHAVARAM CFS L 8 091481 SUBRAMANI E. A.ELLAPPAN RO CHENNAI L c 091508 SOMASUNDARAM T IHAMBURAJ JS a JS TRICHY 1C 091511 SANKAR S SWAMINATHAN A lq ERODE 11 09152J NAGALAKSHMI L LAKSHMIKANTHAN a S UDUMALPET t2 09153G NATARA.JAN V S.GOVINDASAMY RO CHENNAI c RENUKA DEVI P K.PADMANABHA PILLAI JS 09154E Lr) CH ITLAPAKKAM/CH R OMEPET L t4 09159F RAMANUJAM G R.GOVINDA IYENGAR JS oHanvRt-trueAM.P / (- D JS MANNARGUDI 15 09160K SIVAPRAKASAM D MARAHADHAM L THURAIRAJ P JS RO CHENNAI _LC 09163D RAJAKUMAR T I F\ CH ITLAPAKKAM/CH R JS OMEPET 17 09178B VIKRAMAN M.S M D SELVARA.J S MADHAVARAM CFS L 18 091791 GOVTNDARAJULU.E ETHIRAJULU S RO CHENNAI 19 09180D LAKSHMIKANTHA P ;.PANDURANGAN C S S RO CHENNAI 2C 10815D DHANDAPANI D URAISAMY IS THANJAVUR-II c 21 t0821.J RADHAKRISHNAN G 3ANGADHARAN R C lrt Rtrt RP OO ttl G OTHAI. VIADHAVARAM CFS a 22 10823E D PUSHPAVATHI S )lNbAI\ALLUK ALL IS \ND ICD L 23 10839A KANNUSWAMY.R RAMASAMY V a 24 108424 SUBRAMANIAN.S .RANGAN JS lruarutnvun F\ :HITLAPAKKAM/CHR OMEPET L 25 10854E YAMUNA RANI.A ANANDHAN P.R JS I IS PUDUCHERY 26 10857K SEETHARAMAN R RAMANATHAN A.K. -

Tamil Nadu – MDMK – DMK

Refugee Review Tribunal AUSTRALIA RRT RESEARCH RESPONSE Research Response Number: IND34864 Country: India Date: 7 May 2009 Keywords: India – Tamil Nadu – MDMK – DMK This response was prepared by the Research & Information Services Section of the Refugee Review Tribunal (RRT) after researching publicly accessible information currently available to the RRT within time constraints. This response is not, and does not purport to be, conclusive as to the merit of any particular claim to refugee status or asylum. This research response may not, under any circumstance, be cited in a decision or any other document. Anyone wishing to use this information may only cite the primary source material contained herein. Questions 1. Is there any information available about the death of Mr Elumalai Naicker, Secretary of the MDMK party for Chennai, and who may have been responsible for his death? 2. Is there any information available on a disturbance at an MDMK rally at Marina Beach, Chennai, in the days prior to the killing of Mr Elumalai Naicker? Background note on source availability Very little news was published electronically in India prior to the late 1990s. Even services like the Factiva subscription news database hold very few Indian press articles from the period before the mid 1990s. For this reason, detailed information on Indian press coverage of events which have taken place beyond the recent decade can be very difficult to locate. RESPONSE 1. Is there any information available about the death of Mr Elumalai Naicker, Secretary of the MDMK party for Chennai, and who may have been responsible for his death? A number of reports were located which referred to the killing of an Marumalarchi Dravida Munnetra Kazhagam (MDMK) leader, Elumalai Naicker, in the suburb of Royapuram in Madras (as Chennai was then known); according to one report the “incident had occurred a few days after a rally taken out by the party”. -

Chengalpattu to Beach Train Timing Pdf

Chengalpattu to beach train timing pdf Continue chengalpattu to the time of the beach train, the time of the local chengalpattu train, railway station chengalpattu, chengalpattu on the beach electric train timings, chengalpattu on the beach local train timings PDF, chengalpattu on the beach local trains timing PDF, chengalpattu in Chennai beach local trains timing, chengalpattu in Chennai beach train timing, chengalpattu in Chennai beach train timing, chengalpat , chengalpattu beach train timings, chengalpattu chennai beach train timings, chengalpattu fast train timings, chengalpattu station, chengalpattu on the beach, chengalpattu on the beach emu train timings, chengalpattu on the beach fast train timings, chengalpattu on the beach train timings on Sunday, chengalpattu on the beach, chengalpattu on the beach, chengalpattu in Chennai train timing, chengalaltu train, chengalpattu train, chengalpattu train, chengalpattu train, chengalpattu train - chennai beach to the time of the fort chennai train, chennai beach to the time of the chennai park train, chennai beach egmore, chennai train time to the time of the chennai chetpat train, chennai beach to the train time of the nungambakkam, the chennai beach to the time of the kodamba train. , Chennai beach to saidaoet train time, Chennai beach, to guidy train timing, chennai beach to st thomas mounts train time, chennai beach to palavantangal train time, chennai beach to train time minabakkam, chennai beach to tirusulam train timing, chennai beach to pallavaram train time, chennai beach to train -

Nodal Contacts

BHARAT SANCHAR NIGAM LIMITED O/o PGM S, 40-E, CIPET ROAD TVK INDUSTRIAL ESTATE, GUINDY-32 LR.NO: PGM/S/2019-20/ENLISTING FTTH VENDORS/ DT 02.05.2019 Sub: Enlisting of FTTH Partners with BSNL UnderRevenue Share Business Model-reg. BSNL, Chennai Telephones, is in the Process of Enlisting New Vendor Agencies for providing Voice & Broadband Services thru Optical Fibre Cable Connectivity to Individual Homes (FTTH) on Revenue Share Basis (50:50) Interested Agencies with Valid License / Minimum One Year Experience are requested to submit their willingness for Entering into Business Agreement with BSNL in this regard. Eligibility Criteria: 1. Registered Builder 2. Registered Residential Welfare Association 3. Local Cable Operators (LCOs) / Multi Service Operators (MSOs) with valid license 4. Infrastructure Providers-1 (IP-1) / Virtual Network Operators (VNOs) with valid license 5. Existing Cable Operators, Firms working for OFC laying, Broadband Provisioning & Maintenance and other firms working in Telecom field etc. (A company incorporated under the company Act 1956, or Proprietorship/ Partnership firms) Coverage Area: Exchanges / Postal Pincodes, Covered under South and West Areas inChennai Telephones District, as Annexed. Nodal contacts I. South Business Area No. Name Designation Mobile No. Mail ID 1 A.Kalaiselvi AGM 9444979100 2 R.Petchimuthu SDE 9444995599 [email protected] 3 S.Mathiprakasam SDE 9444971900 4 D.Aravind SDE 9444040368 II. West Business Area No. Name Designation Mobile No. Mail ID 1 ShanthiRamani AGM 9445395353 2 Chandra -

(Unani) Practitioner List As on 31-08-2016

1 TAMIL NADU BOARD OF INDIAN MEDICINE ELECTION – 2016 (UNANI) PRACTITIONER LIST AS ON 31-08-2016 S.No Name & Address 2 1 Dr. SYED KHALEEFA THULLAH, B.U.M.S, 16327, N.No. 358, S/o. Syed Niamathulla Sahib 49, Bharathi Salai, Triplicane, Chennai - 600 005. 2 Dr. AZEEZUR RAHMANAZAMI, B.U.M.S, 24418 S/o. Moulana Mohamed Maman Sahib. No.2, Small Mosque Street, Poonamallee, Chennai - 600 056 3 Dr. HAKIM SYED IMAMUDDIN AHMED. B.U.M.S., 24450,N.No.262 S/o. Hakim Syed Muslihuddin Ahmed. A22, T.V.K.Street, M.M.D.A.Colony, Chennai - 600 106. 4 Dr. HAKEEM GIYASUDDIN AHMED, B.U.M.S., 24511,N.No.206 S/o. Muneeruddin Ahmed. Old No. 489, New No. 50, N.S.K. Nagar, Arumbakkam, Chennai - 600 106. 5 Dr. QUAZI ABUL HASANATH, Tabeeb-E-Kamil, 27279, N.No.267 S/o. Hakeem Masood Ahmed. No.97/A, Jamath Road, Noorullahpet, Vaniyambadi, Vellore District - 635 751. 6 Dr. SYED ABDUL MANNAN, Tabeeb-E-Kamil, 24513, N.No.187 S/o. Syed Abdur Rahaman. C-Type, No.3/142, SIDCO Nagar, Villivakkam, Chennai - 600 049. 7 Dr. SHAIK MADAR SAHIB, Tabib-I-Kamil, 24542, N.No.251 S/o. Shaik Kareem Sahib. Flat No.12, R.B.Paradise, No.26, Manickkam Street, Choolai Chennai-600 112. 8 Dr. ABDUL KHUDDUS AZAMI.Tabib-I-Kamil, 24563,N.No.369 S/o. S. Mohammad Abdul Aziz Azami No.90/14, P-Block, M.G.R 5th Street, M.M.D.A Colony,Arumbakkam,Chennai - 600106 9 Dr.