2016 Annual Aggregate Report

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Guin April 28, 2017

April 28, 2017 GSE MARKET STATISTICS SUMMARY Weekly Stock Market Review GSE-CI Extends Gains: The equities market ended the week in the positive Current Previous % Change territory anchored on price gains in 8 counters. The Ghana Stock Exchange’s Databank Stock Index 24,800.75 24,672.90 0.52 Composite Index (GSE-CI) gained 10.37 points w/w to ~1,896 points, while GSE-CI Level 1,896.13 1,885.76 0.55 the Databank Stock Index surged by 128 points w/w to ~24,800 points. The Market Cap (GH¢ m) 58,822.68 48,778.78 20.59 year to date returns of the GSE-CI and the Databank Stock Index stand at YTD Return DSI 11.05% 10.48% 12.26% and 11.05% respectively. YTD Return GSE-CI 12.26% 11.64% Weekly Volume Traded (Shares) 2,142,471 1,812,263 18.22 A block trade in Ecobank Transnational Inc. propelled the volume of shares Weekly Turnover (GH¢) 2,785,677 1,639,744 69.88 traded by ~17% w/w to ~2.1 million shares. These trades, which occurred Avg. Weekly Volume Traded (Shares) 1,059,295 1,049,043 0.98 across 22 counters, were valued at ~GH¢2.7 million. Avg. Weekly Value Traded (GH¢) 1,473,386 1,460,057 0.91 The market breadth of the Ghana Stock Exchange was positive w/w: 8 No. of Counters Traded 22 21 gainers to 3 laggards. Unilever Ghana increased by 15Gp to GH¢9.05. Access No. of Gainers 8 6 Bank Ghana moved up 10Gp to GH¢4.00. -

PRESS RELEASE PR. No 034/2019 GHANA OIL COMPANY LIMITED (GOIL) ANNUAL REPORT and CONSOLIDATED FINANCIAL STATEMENT for the YEAR

PRESS RELEASE PR. No 034/2019 GHANA OIL COMPANY LIMITED (GOIL) ANNUAL REPORT AND CONSOLIDATED FINANCIAL STATEMENT FOR THE YEAR ENDED 31 DECEMBER 2018 GOIL has released its Annual Report and Consolidated Financial Statements for the year ended December 31, 2018 as per the attached. Issued in Accra, this 9th day of April, 2019 - E N D – att’d. Distribution: 1. All LDMs 2. General Public 3. Company Secretary, GOIL 4. MBG Registrars, (Registrars for GOIL shares) 5. Custodians 6. Central Securities Depository 7. Securities and Exchange Commission 8. GSE Council Members 9. GSE Notice Board For enquiries, contact: Head Listing, GSE on 0302 669908, 669914, 669935 *GA GHANA OIL COMPANY LIMITED CONSOLIDATED FINANCIAL STATEMENTS 31 DECEMBER 2018 GHANA OIL COMPANY LIMITED ANNUAL REPORT AND CONSOLIDATED FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 DECEMBER 2018 CONTENTS PAGE COMPANY INFORMATION 1 REPORT OF THE DIRECTORS 2 - 3 REPORT OF THE AUDITOR 4 - 7 STATEMENT OF COMPREHENSIVE INCOME 8 STATEMENT OF FINANCIAL POSITION 9 STATEMENT OF CHANGES IN EQUITY 10 STATEMENT OF CASH FLOWS 11 GENERAL INFORMATION AND SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES 12 - 26 OTHER NOTES TO THE FINANCIAL STATEMENTS 27 - 40 GHANA OIL COMPANY LIMITED COMPANY INFORMATION FOR THE YEAR ENDED 31 DECEMBER 2018 BOARD OF DIRECTORS: Hon. Peter Kwamena Bartels - Chairman Mr. Patrick Akpe K. Akorli - Group CEO/MD Mr. Thomas Kofi Manu - Member Hon. Kwame Osei-Prempeh - Member Mr. Beauclerc Ato Williams - Member Mrs. Beatrix Agyeman Prempeh - Member Mr. Robert Owusu Amankwah - Member Mrs. Rhoderline Baafour-Gyimah - Member Mr. Stephen Abu Tengan - Member SECRETARY: Nana Ama Kusi-Appouh AUDITOR: PKF Chartered Accountants Farrar Avenue P.O. -

Radiation Protection Institute Annual Report for the Year 2015

RADIATION PROTECTION INSTITUTE ANNUAL REPORT FOR 2015 GHANA ATOMIC ENERGY COMMISSION RADIATION PROTECTION INSTITUTE ANNUAL REPORT FOR THE YEAR 2015 Executive Summary The Radiation Protection Institute (RPI) of the Ghana Atomic Energy Commission was established to provide the scientific and technical support for executing the operational functions of the Radiation Protection Board. The operational activities of the Institute for the year 2015 include: Ninety Seven (97) authorizations to possess and/or use irradiating devices, radiation sources and radioactive materials. There were also regular compliance inspections to ensure protection of radiation workers, patients and the public and the security and safety of radiation sources. One Hundred and Five (105) permits were granted for import, export, and transport, construction and transfer of radioactive materials. A total of Four Hundred Sixty-Three (463) food samples and industrial raw materials were analyzed and certificates issued for radioactivity contamination. Individual or personal monitoring was provided for One thousand, Seven hundred and Thirty-Five (1,735) occupationally exposed workers in Ghana. Fifty-Seven (57) radiation survey meters were calibrated using the facilities at the Secondary Standards Dosimetry Laboratory (SSDL). Seven Hundred and Twenty-Seven (727) Base Stations were monitored during the year under review. Twenty (20) research projects were undertaken to enhance protection and safety of radiation workers, patients and the general public. Fourteen (14) journal articles were published. There were Nine (9) National Training Courses organized by RPI for end user Institutions for their specific applications. Four (4) IAEA Training Courses were organized. The internally generated funds from the service activities were used to support and sustain the regulatory, service, research and development activities of the institute. -

Ghana at a Glance: 2002-03

COUNTRY REPORT Ghana Ghana at a glance: 2002-03 OVERVIEW The New Patriotic Party (NPP) government will persist with its investigations into cases of maladministration and corruption on the part of the previous government. While this will lead to tensions between the opposition National Democratic Congress (NDC) and the NPP, a military coup is not expected. The government will meanwhile continue to focus on reforms designed to improve macroeconomic stability. Efforts to reduce the country’s fiscal deficit, together with a range of other policy reforms, donor support and recovery in the agricultural sector, should lead to a gradual acceleration of GDP growth. As fiscal and monetary policy is more co- ordinated, the Economist Intelligence Unit forecasts a gradual decline in the inflation rate, while improved macroeconomic stability should see the value of the cedi stabilise. Key changes from last month Political outlook • The president, John Agyekum Kufuor, has performed his first cabinet reshuffle, in an attempt to improve the government’s ability to implement economic policy. Economic policy outlook • The government has issued a three-year Government of Ghana index- linked bond (GGILB), to replace up to 50% of the domestic debt of C6trn (US$844m), now held in 91- and 182-day Treasury bills. The instrument’s interest and principal are linked to the consumer price index, providing full inflation protection to the holder. Economic forecast • Our economic forecasts have been moved on by one year to 2003. We now expect growth to pick up to 4.8% of GDP in 2003, against a background of falling inflation. -

Good Energy Contents Contents

ANNUAL REPORT AND 2014 FINANCIAL STATEMENTS Good energy contents contents 02 Company Information 03 Notice of 46th Annual General Meeting 04 Resolutions to be passed at the Annual General Meeting 05 Profile of New Directors to be Elected 06 Board of Directors 07 Address by Chairman 10 Management Team 11 Report of the Directors on The Financial Statements 13 Corporate Governance 14 Disclosure Requirements 16 Independent Auditor's Report 18 Statement of Comprehensive Income 19 Statement of Financial Position 20 Statement of Changes in Equity 21 Statement of Cash Flow 22 Notes to The Financial Statements 43 Proxy Form GOIL Annual Report & Financial Statements 2014 Company Information Notice of 46th Annual General Meeting BOARD OF DIRECTORS Prof. William A. Asomaning – Chairman NOTICE IS HEREBY GIVEN that the 46th Annual General Meeting of the Shareholders of Ghana Oil Mr. Patrick Akpe Kwame Akorli – Managing Director Company Limited will be held at the Auditorium, College of Physicians and Surgeons, Ridge, Accra on Hon. Nii Laryea Afotey-Agbo – Member Thursday, 30th April, 2015 at 11:00 am for the transaction of the following business: Nana Esuman Kwesi Yankah – Member Mr. Eugene Akoto-Bamfo – Member Mr. Chris A-Ackummey – Member AGENDA Mad. Faustina Nelson – Member Mr. Thomas Kofi Manu – Member ORDINARY BUSINESS Hon. Kojo Bonsu – Member 1. To receive and consider the reports of the Directors and the Auditors and the Financial Statements of the Company for the year ended December 31, 2014. 2. To declare a dividend for the year ended December 31, 2014. SECRETARY Mr. Stephen Y. Gyaben 3. To elect Directors to replace retiring Directors. -

Has Gse Played Its Role in the Economic Development of Ghana?

CAPITAL MARKET 23 YEARS AND COUNTING: HAS GSE PLAYED ITS ROLE IN THE ECONOMIC DEVELOPMENT OF GHANA? 1st CAPITAL MARKET CONFERENCE BY EKOW AFEDZIE, DEPUTY MANAGING DIRECTOR MAY 10, 2013 INTRODUCTION Ghana Stock Exchange (GSE) was established with a Vision: -To be a relevant, significant, effective and efficient instrument in mobilizing and allocating long-term capital for Ghana’s economic development and growth. INTRODUCTION OBJECTIVES - To facilitate the Mobilization of long term capital by Corporate Bodies/Business and Government through the issuance of securities (shares, bonds, etc). - To provide a Platform for the trading of issued securities. MEMBERSHIP OF GHANA STOCK EXCHANGE GSE as a public company limited by Guarantee has No OWNERS OR SHAREHOLDERS. GSE has Members who are either corporate or individuals. There are two categories of members:- - Licensed Dealing Members - 20 - Associate Members - 34 HISTORICAL BACKGROUND 1968 - Pearl report by Commonwealth Development Finance Co. Ltd. recommended the establishment of a Stock Exchange in Ghana within two years and suggested ways of achieving it. 1970 – 1989 - Various committees established by different governments to explore ways of bringing into being a Stock Exchange in the country. HISTORICAL BACKGROUND 1971 - The Stock Exchange Act was enacted. - The Accra Stock Exchange Company incorporated but never operated. Feb, 1989 - PNDC government set up a 10-member National Committee on the establishment of Stock Exchange under the chairmanship of Dr. G.K. Agama, the then Governor of the Bank of Ghana. HISTORICAL BACKGROUND July, 1989 - Ghana Stock Exchange was incorporated as a private company limited by guarantee under the Companies Code, 1963. HISTORICAL BACKGROUND Nov. -

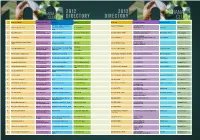

2012-Edition-GC100-Directory.Pdf

2012 2012 DIRECTORY DIRECTORY NAME OF COMPANY BUSINESS CATEGORY LOCATION ADDRESS TELEPHONE FAX/E-MAIL/WEBSITE CONTACT PERSON TITLE 7 Dr. Amilcar Cabral Road, Accra (233-302) 770189/90/91 “(233-302) 770187 1 Abosso GoldFields Limited Mining Institution Airport Residential Area P. O. Box KA 30742 www.goldfields.co.za” Alfred Baku Managing Director Accra Banking Services [email protected] Head, Corporate 2 Acces Bank (Ghana) (Commercial & Merchant) “Starlets ‘91 Road “P. O. Box GP 353 Osu- Accra” (233-302) 684860 / 742699 www.accessbankplc.com/gh Matilda Asante-Aseidu Communications (233-302) 2688960 3 Accra Brewery Manufacturing - Beverages Opp. Ohene Djan Staduim” P. O. Box GP351 (233-302) 688851-6 [email protected] Gregory Metcalf Managing Director www.sabmiller.com (233-302) 685176 4 Activa International Insurance Company Non-Banking-Insurance Graphic Road, Adabraka PMB KA 85 (233-32) 686352 / 672145 [email protected] Limited www.group-activa.com “P. O. Box 35 Banking Service-Rural & 3rd Floor Heritage Tower, 6th Ave. West (233-322) 420926 / 90099 Lucy Opoku-Arthur Ag General Manager 5 Adansi Rural Bank Limited Community Banking Ridge, Accra Fomena-Adansi” Banking Services-Rural & 6 Adonten Community Bank Limited Community Banking Head Office: Fomena - Adansi P.O.Box 140 3420-24109/027-895636/027-7609343 3420-26780 [email protected] Mr.Francis Mensah Senior Manager Banking Services-Rural & 7 Ahantaman Rural Bank Limited Community Banking New Tafo, Akyem, Eastern Region P. O. Box 41, Ahanta (233-312) 23431 / 21016 (233-312)29116 David Bampoe General Manager Banking Services-Rural & 8 Amanano Rural Bank Limited Community Banking Agona Ahanta,Western Region P. -

Beyond the Budgets

BEYOND THE BUDGETS A Collation of Government Policies On Wages & Salaries, Energy and Employment, Volume 1 2001 – 2006 Compiled by Kwadwo Baah-Wiredu M.P Minister of Finance and Economic Planning and Budget Implementation Support Team Foreword This publication is to provide a quick reference material for: 1. Academics, 2. Students; 3. Researchers; 4. Social Commentators; 5. Politicians; as well as 6. Economic Planners. On the three (3) critical areas, 1. Employment; 2. Energy; and 3. Wages. that have provided the most formidable challenge to economic planners in Ghana with reference to the last two (2) decades. The content of the publications are drawn from the Budget Statement and Economic Policies of Governments of Ghana. The two publications available cover the following time periods: 1. Volume 1: 2001 – 2006 2. Volume 2: 1982 – 2000 Subsequent volumes will cover: 1. Period from 1951 to 1981; 2. Translation into at least six (6) local languages. Since Democracy and good governance thrives on the availability of information, this publication will provide an excellent resource material on the national economy in these three (3) key areas mentioned above. These publications will be made available to a very wide segment of the population including posting them on Ministry of Finance and Economic Planning website: www.mofep.gov.gh. We hope that this document will stimulate active discussion on these 3 critical issues of national concern. We are walking on the path of honour and courage. Kwadwo Baah-Wiredu, M.P. Minister TABLE OF CONTENTS Foreword 2 Table of Contents 4 Wages Policies of Government of Ghana 5 Energy Policies of Government of Ghana 7 Employment Policies of Government of Ghana 17 POLICIES FROM BUDGET ON WAGES AND SALARIES 2005, FEBRUARY, 24 “Government being mindful of the importance of higher wages in mitigating hardships and enhancing the productivity of its employees was “committed to improving the remuneration of Ghanaians and will grant increases in salaries in consultation with all stakeholders”. -

Ghana National Petroleum Corporation List of Registered Service Companies with Permit

GHANA NATIONAL PETROLEUM CORPORATION LIST OF REGISTERED SERVICE COMPANIES WITH PERMIT OWNERSHIP START DATE OF EXPIRY DATE OF 1st Renewal COUNT SERIAL NO. NAME OF COMPANY ADDRESS CONTACT NUMBER RANGE OF SERVICES PROPOSED STRUCTURE PERMIT PERMIT (expiry date) Industrial area Extension road, Ronfort Provision of 3rd party labour (On/Offshore), Office/warehouse Ghanaian co. with more Foundation Int., Takoradi Tel: 0243-431805 rental, full fabrication facilities, marine engineering, repairs and than 50% Ghanaian 1 001108 Seaweld Engineering Ltd. P. O. Box 574 Tema. Email: [email protected] maintenance, Tank cleaning, procurement, handling of waste. ownership 1-Sep-08 31-Aug-09 28-Dec-10 Thokey House, Comm4, Opposite SEGECO Tel: 022-205557 Logistics, Labour supply, Catering, Marine supply vessels, Car rental, Ghanaian co. with more Flats. Fax:022-205558 Pipe yard/Warehouse, Shipping agency, clearing & forwarding Crude oil than 50% Ghanaian 2 002108 Menergy (Ghana) Limited P. O. Box CO2932, Tema Email: [email protected] brokerage&lifting ownership 1-Sep-08 31-Aug-09 31-Aug-10 Tel: 022-302474, 022-302291 Plot A/34/4, Steel works Road, Heavy Fax:022302474 Ghanaian co. with more Industrial Area, Tema. Email:[email protected] / Importation of Chesterton Products, Maintenance of Chesterton's plants, than 50% Ghanaian 3 003108 Gulf Engineering Services Ltd P. O. Box CO 1642, Tema [email protected] machinery and equipment. ownership 1-Sep-08 31-Aug-09 Logistical services related to import and export of oilfield equipment, principally handling of sea and airfreight, transportation of materials, Ghanaian co. with more Commercial Warehouse Road, Main warehousing, storage, ship agency services, meet and greet, aircraft than 50% Foreign 4 004108 SDV Ghana Limited Harbour Area, P. -

Weekly Market Watch Sic-Fsl Investment+ Research| Market Reviews|Ghana

WEEKLY MARKET WATCH SIC-FSL INVESTMENT+ RESEARCH| MARKET REVIEWS|GHANA 8th January, 2015 STOCK MARKET ACCRA BOURSE MAKES PROMISING START INDICATORS WEEK OPEN WEEK END CHANGE The year 2014 has begun living up to expectations as bullish runs in equities from the petroleum, finance and consumer Market Capitalization (GH¢ goods sectors saw the annual returns of the broader market 'million) 64,352.42 64,229.12 -0.19% Market Capitalization (US$' inch up to 0.42% last Thursday. Though, most equities gave million) 20,109.50 20,014.06 -0.47% up their opening prices, rise in the market value of Ghana Oil Petroleum Company Limited (GOIL), Societe Generale Ghana Volume traded (shares) 783,118.00 573,274.00 -26.80% Table 1: Market Summary Limited (GOIL) and Fan Milk Limited (FML) were enough to close the week’s activities on a positive note. Key benchmark indices closed the week better despite slight volatilities during inter-day trading. The GSE Composite INDEX ANALYSIS index closed at a year-to-date return of 0.42% whiles the GSE Financial Stocks Index settled at 0.67% returns. INDICATORS Closing Week YTD Level Change CHANGE Total market capitalization of the Ghana Stock Exchange was GH¢64.23 billion, an equivalent to USD20.00 billion. GSE Composite Index 2,270.57 0.42% 0.42% GSE Financial Stocks Index 2,258.77 0.67% 0.67% Table 2: Key Stock Market Indices LIQUIDITY The absence of block trades over the period saw liquidity comparatively down last week. All in all, an approximate figure of 573,274 shares exchanged hands within the first trading week of the year, and was also valued about GH¢2.48 million. -

Ghana Oil & Gas 2012

Ghana Oil & Gas 2012 Economy • Exploration • Oil • Natural Gas • Challenges • Services Global Business Reports Industry Explorations CREDITS EDITORIAL AND MANAGEMENT TEAM Senior Journalist: Angela Harmantas [email protected] Journalist: Tom Hurst [email protected] Project Coordinator: Pavlina Pavlova [email protected] General Manager: Agostina Da Cunha [email protected] Regional Manager: Sharon Saylor [email protected] Graphic Designer: Gonzalo Da Cunha [email protected] Editor: Barnaby Fletcher For more information about GBR, please email [email protected]. For updated industry news from our on-the-ground teams around the world, please follow us on Twitter: @GBReports. THANK YOU GBR would like to thank the following associations for their help in the research of this project: Ministry of Energy www.energymin.gov.gh Ghana Energy Commission www.energycom.gov.gh Ghanaian National Chamber of Commerce & Industry www.ghanachamber.org Ghana Investment Promotion Centre (GIPC) www.gipcghana.com Petroleum Commission We would also like to sincerely thank all the companies that took the time to give their insights on the market, with a special mention to George Aboagye, CEO, Ghana Investment Promotion Centre (GIPC), for his written contribution to this book, as well as to Leslie Asamoa, Consultant to the Finland-Ghana Chamber of Commerce (FINGHCC) for his assistant. Industry Explorations Global Business Reports // BRAZIL CHEMICALS 2012 72 Global Business Reports Industry Explorations INTRODUCTION LETTER Dear readers, Simply put, Ghanaians truly value their reputation as one of the African con- Akwaaba. tinent’s most stable, investor-friendly countries, and take great pride in main- A simple word, meaning “welcome” in taining it as such. -

WEEKLY MARKET REVIEW 3 November 2017

DATABANK RESEARCH WEEKLY MARKET REVIEW 3 November 2017 ANALYST CERTIFICATE & REQUIRED DISCLOSURE BEGINS ON PAGE 4 GSE MARKET STATISTICS SUMMARY Current Previous % Change Market Indices Maintain Bullish Performance (w/w): Databank Stock Index 30,388.18 30,209.24 0.59% By the end of this week’s trading session, the Ghana Stock Exchange’s Composite Index GSE-CI Level 2,367.28 2,352.11 0.64% increased by 15.15 points w/w to ~2,367 points while the Databank Stock Index (DSI) surged by 178.94 points w/w to 30,388 points. The year-to-date returns of the GSE-CI Market Cap (GH¢ m) 58,057.10 58,497.34 -0.75% and the DSI are recorded at 40.15% and 36.07% respectively. YTD Return DSI 36.07% 35.27% Market activity improved by ~32% w/w to 5.37 million shares on the back of block trades YTD Return GSE-CI 40.15% 39.25% in Cal Bank and Total Petroleum. The total volume of shares traded were valued at Weekly Volume Traded (Shares) 5,365,067 941,100 470.08% GH¢8.97 million. Cal Bank and Total Petroleum accounted for ~94% of the aggregate volume of shares traded. Weekly Turnover (GH¢) 8,973,736 3,004,202 198.71% Avg. Weekly Volume Traded The market breadth of the bourse was negative (w/w) with 6 gainers and 7 laggards. 1,443,315 1,417,645 1.81% Unilever Ghana was the best performer (w/w), surging by 39Gp to GH¢10.99.