Contents • Intro, Aerials & Maps • Zoning • Executive Summary

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Hospital Data Dictionary

HOSPITAL DATA DICTIONARY Texas Department of State Health Services EMS/Trauma Registry July 24, 2001 TABLE OF CONTENTS Definitions ii 2002 Data File Formats iii Respiratory Rate for Trauma Score 12 Revised Trauma Score 13 Sex 2 Patient Demographics Software Identification 31 Main Fields Systolic Blood Pressure 8 (*Shaded fields are required or Systolic Blood Pressure at Scene 21 conditionally required. See page Systolic Blood Pressure for Trauma Score 12 TDH Firm Number (EMS ID#) 24 number referenced for clarification) Time of Arrival 7 (Body Region) Injury Severity 18 Time of Arrival to First Hospital 28 (Body Region) Type of Injury 18 Time of Departure from First Hospital 29 Abbreviated Injury Scale 17 Time of Discharge or Death 15 Alcohol Level 8 Time of Dispatch 24 Alcohol Level Tested 8 Time of Injury 4 Billed Hospital Charges 20 Time of Leaving The Scene 25 Cause of Injury 4 Time of Scene Arrival 25 City of Residence 30 Time of Trauma Team Activation 30 Condition on Discharge 14 Total Reimbursement 20 County of Injury 4 Transfer Status (Is This a Transfer?) 27 County of Residence 5 Trauma Registry Number 1 Date of Arrival 7 Trauma Team Activation 30 Date of Arrival to First Hospital 28 Vehicle Extrication 26 Date of Birth 3 Verbal Response 10 Date of Departure from First Hospital 29 Verbal Response at Scene 22 Date of Discharge or Death 15 Date of Injury 3 Diagnoses 17 32 Diastolic Blood Pressure 8 Research Fields Eye Opening Response 11 Desired Fields 33 Eye Opening Response at Scene 23 Appendices Facility Number 2 Appendix A -Hospitals – see ID Numbers web First Hospital Number 27 Appendix B - EMS Providers -see ID Numbers web Glasgow Coma Score at Admission 11 Appendix C - County Code List………………. -

Mckinney TEXAS

OFFERING MEMORANDUM McKINNEY TEXAS Absolute NNN Lease Third-Fastest Growing City in the U.S. CONFIDENTIALITY AND DISCLAIMER The information contained in the following Marketing Brochure is proprietary and strictly confidential. It is intended to be reviewed only by the party receiving it from Marcus & Millichap Real Estate Investment Services of Florida, Inc. (“Marcus & Millichap”) and should not be made available to any other person or entity without the written consent of Marcus & Millichap. This Marketing Brochure has been prepared to provide summary, unverified information to prospective purchasers, and to establish only a preliminary level of interest in the subject property. The information contained herein is not a substitute for a thorough due diligence investigation. Marcus & Millichap has not made any investigation, and makes no warranty or representation, with respect to the income or expenses for the subject property, the future projected financial performance of the property, the size and square footage of the property and improvements, the presence or absence of contaminating substances, PCB’s or asbestos, the compliance with State and Federal regulations, the physical condition of the improvements thereon, or the financial condition or business prospects of any tenant, or any tenant’s plans or intentions to continue its occupancy of the subject property. The information contained in this Marketing Brochure has been obtained from sources we believe to be reliable; however, Marcus & Millichap has not verified, and will not verify, any of the information contained herein, nor has Marcus & Millichap conducted any investigation regarding these matters and makes no warranty or representation whatsoever regarding the accuracy or completeness of the information provided. -

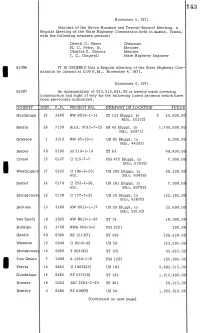

I 65386 65387 November 4, 197 1 Minutes of the Seven Hundred and Twenty-Second Meeting, a Regular Meeting of the State Highway C

143 November 4, 197 1 Minutes of the Seven Hundred and Twenty-Second Meeting, a Regular Meeting of the State Highway Commission held in Austin, Texas, with the following members present: Dewitt C. Greer Chairman H. C. Retry, Jr. Member Charles E. Simons Member J. C. Dingwall State Highway Engineer 65386 IT IS ORDERED that a Regular Meeting oi the State Highway Com i mission be opened at 2:00 P.M., November 4, 1971. November 4, 1971 65387 An appropriation of $33,313,691.00 is hereby made covering construction and right of way for the following listed projects which have been previously authorized. COUNTY DIST. P.P. PROTECT NO. HIGHWAY OR TO CATION FUNDS Guadalupe 15 3240 RW 8015-1-15 ST 123 (Suppl. to $ 24,000.00 Min. 52152) Harris 26 7150 Acct. 9012-7-23 IH 45 (Suppl. to 1,700,000.00 Min. 62071) Grayson 1 3010 RW 45-19-1 US 82 (Suppl. to 6,000.00 Min. 44353) Jasper 20 5296 M 214-1-14 49,400.00 ST 63 Comal 15 0127 C 215-7-7 7,000.00 FM 475 (Suppl. to Min. 63916) I Washington 17 0222 C 186-6-20, US 290 (Suppl. to 59,300.00 etc. Min. 63436) Burnet 14 0174 C 252-2-26, US 281 (Suppl. to 7,000.00 etc. Min. 63786) Montgomery 12 0138 C 177-5-23 US 59 (Suppl. to 122,182.00 Min. 62878) Jackson 13 3220 RW 8013-1-17 US 59 (Suppl. to 22,600.00 Min. 59110) Van Zandt 10 3025 RW 8010-1-87 18,000.00 ST 19 Hidalgo 21 3728 RWA 669-3-5 200.00 FM 2221 Hardin 20 8326 RS 1513(7) 236,520.00 ST 326 Wharton 13 0249 C 89-8-49 253,585.00 US 59 Montgomery 12 9950 T 9033(2) 43,655.00 ST 105 Tom Green 7 2009 A 1364-1-8 195,245.00 FM 1223 Travis 14 9662 U 1068(23) 2,682,515.00 I US 183 Guadalupe 15 8265 RF 537(18) 1,212,490.00 ST 123 Nueces 16 0362 MC 2263-2-20 56,315.00 ST 301 Hartley 4 8266 RF 608(9) 1,032,010.00 US 54 (Continued on next page) November 4, 1971 65387 Con inued - COUNTY DIST. -

Collin County Historical Markers

Collin County Historical Commission Historical Markers Collin County has over Over 10 sites have been awarded 170 Texas State His t o r ic a l Markers Collin County Historical Markers Texas State Historical Markers The state of Texas has 2 kinds of historical markers – Recorded Texas Historic Landmark markers and Subject markers. An RTHL is given to a building that is historically important. Subject markers are for any event or subject that is historically significant. Applications are available at the Texas Historical Commission website - http://www.thc.state.tx.us/markerdesigs/madapply.shtml. The time period for applying is September 1 – November 15. All applications are done by computer and must go through the Collin County Historical Commission for initial approval. Cemeteries can apply for Historic Texas Cemetery Designation year-round. County Historical Markers The Collin County Historical Commission established the Collin County Historical Marker program to interpret, promote and protect historic and cultural resources located in Collin County that are worthy of preservation. Through the designation process, sites important to the county will be evaluated using established criteria and, if selected, marked for the education and enjoyment of citizens and visitors alike. Suggested County Markers Application Forms for County Markers Collin County Historical Commission Texas State Historical Markers By Community Allen: Allen Cemetery, Allen Station, Allen Melissa: First Baptist Church, Melissa Altoga: Altoga Cemetery, Stiff Chapel School, Melissa Cemetery, St. Paul Baptist Cemetery Church, Highland Cemetery, Stony Point Baptist Church and Cemetery, Melissa Anna: Coffman Cemetery, First Christian Christian Church, Scott-Barker House Church of Anna, Public Education, Sherle y Store, James Throckmorton, William Murphy: First Baptist Church, Maxwell Throckmorton, Collin McKinney Cemetery Homestead Nevada: Nevada Baptist Church, Nevada Blue Ridge: Blue Ridge Methodist Church, Cemetery, Prairie Grove Cemetery, Mt. -

GHORT LINC \*J by 225 MILES Mmm

\'s\. 1 •• ' .;"T II I I I I I I I I I I I I I 1 I I I I I 1 I HH I I I I II I I I I I I II I I I I II I I 1 II THE IS THE GHORT LINC \*J BY 225 MILES mmm WHICH MEANS A DAY SAVED /"• i. BETWEEN it Chicago, St. Louj^, Kansas and Points East and North . **V' -AND- El Paso and the Gfeat Southwest .-. Passenger equipment consisting of New Sleeping and Chair Cars, Buffet Library and Smoker, runs through solid without change. "We Feed You" in DINING CARS in11mnniiiiiiiiiiini ii1111 [te^V> .Qfy&%'& /A^Q-I^S'^ ->».• -i- .;. t V I"!' II II I 111 Mill II I M I II I I 111 1 11.11 I I II I 1H II 111 1 I I MMI't " F. C. EARLE, MANAGER T. S. AUSTIN, SUPT. " "•" EL PASO, TEX. EL PASO. TEX. "•* CONSOLIDATED \ Kansas City Smelting 1 anil Refining Co. EL PASO SMELTING WORKS .•••;•.."• BUYERS OF , ORE, BULLION, MATTE AND ALL CLASSES OF FURNACE PRODUCTS. MANUFACTURERS OF I ALCHEMIST BRANDS BLUE VITRIOL, ZINC SULPHATE. + , EL PASO, TEXAS I BELGIAN BAKERY -••'..'" i v The only place in the City to | get FINE DESSERTS AND CAKES FOR WEDDINGS AND PARTIES !!•'HEALTH BREADS A SPECIALTY .:: • • - • i • MRS. J: GEli/IOETS, Proprietor 210 E. OVERLAND ~ TELEPHONE 310 111111 M 111111111111111111 MI 111111111111 n i u u i ii i'" I I II II llll III I I I II III I II 1 I 1 II IMI I II I I I I II II I II II II^ If W. -

United States Geological Survey

DEFARTM KUT OF THE 1STEK1OK BULLETIN OK THE UNITED STATES GEOLOGICAL SURVEY No. 19O S F, GEOGRAPHY, 28 WASHINGTON GOVERNMENT PRINTING OFFICE 1902 UNITED STATES GEOLOGICAL SURVEY CHARLES D. WALCOTT, DIRECTOR GAZETTEEK OF TEXAS BY HENRY G-A-NNETT WASHINGTON GOVERNMENT PRINTING OFFICE 1902 CONTENTS Page. Area .................................................................... 11 Topography and drainage..... ............................................ 12 Climate.................................................................. 12 Forests ...............................................................'... 13 Exploration and settlement............................................... 13 Population..............'................................................. 14 Industries ............................................................... 16 Lands and surveys........................................................ 17 Railroads................................................................. 17 The gazetteer............................................................. 18 ILLUSTRATIONS. Page. PF,ATE I. Map of Texas ................................................ At end. ry (A, Mean annual temperature.......:............................ 12 \B, Mean annual rainfall ........................................ 12 -ryj (A, Magnetic declination ........................................ 12 I B, Wooded areas............................................... 12 Density of population in 1850 ................................ 14 B, Density of population in 1860 -

Town Council Meeting February 10, 2015

Town of Prosper “a pyplace where everyone matters” Town Council Meeting Februaryy, 10, 2015 Town of Prosper “a pyplace where everyone matters” Agenda Item 1. Call to Order/Roll Call. Town of Prosper “a pyplace where everyone matters” Agenda Item 2. Invocation, Pledge of Allegiance, and Pled ge to th e T exas Flag. Town of Prosper “a pyplace where everyone matters” Salute to the T exas F lag Honor the Texas flag; I pledge allegiance to thee, Texas, one state under God , one and indivisible. Town of Prosper “a pyplace where everyone matters” Agenda Item 3. Announcements of upcoming events. Town of Prosper “a pyplace where everyone matters” Agenda Item 4. Consent Agenda Items pldlaced on the Consent AdAgendaare considered routine in nature and non- controversilial. The Consent AdAgendacanbeacted upon in one motion. Items may be removed from the CtConsent AdAgenda bby the request of CilCouncil Members or staff. Town of Prosper “a pyplace where everyone matters” Agenda Items 4a. 4a. Consider and act upon minutes from the following Town Council meetings. (RB) •Regular Meeting – January 27, 2015 •Town Council Strategic Planning Session – January 28, 2015 Town of Prosper “a pyplace where everyone matters” Agenda Items 4b. 4b. Consider and act upon approving the purchase of one backhoe loader for the Public Works Department, from RDO Equipment Company, through the Texas LlLocal GtGovernment PhiPurchasing Cooperative. (JC) Town of Prosper “a pyplace where everyone matters” Agenda Item 4c. 4c. Consider and act upon approving the purchase of one sewer camera, from Green Equipment Company, through the Houston-Galveston Area Council (HGAC) Cooperative Purchasing Program. -

2020 12 12 Small Busines Grant Invoice #11

Collin CARES Small Business Grant Program Invoice # 11 Businesses Approved for Payment on December 21 Requested Local Business Owner ‐ Invoice Proposal ID Proposal Title Amount Grant $Trial Amount First Name Business Owner ‐ Last Name Business Owner ‐ Title Address of Business Briefly describe your type of business and products and/or services that you provide.If you have more than one location, please explain. #11 262581 #1 cleaners 20000 0 20000 Nabil Khan Owner 3198 parkwood blvd suite #3 Laundry & dry cleaning with no plant ,only pick up #11 249496 3296Corporation (Simply Elegant 5000 0 443 Anthony Richardson President 216 Belford Street North, Anna, TX, 75409 We are an event planning company that provides event planning services for clients including weddings, private events/socials, etc. Celebrations and Events) #11 262540 farmers insurance you cai agency 25000 0 6980 you cai agency owner 555 republic dr #116. Plano TX 75074 Our business is selling insurance products such as auto, home, life insurance. #11 257876 Alva Edgar France,Jr. (DBA) Internet 25000 0 13520 Alva France Owner 4303 Springhill Estates, Allen, Texas, 75002‐5784 Internet Marketing and Web Design Services #11 262116 Alyssa Lan Phu 5000 0 3789 Alyssa phu Owner 2600 Network Blvd Suite 130, Frisco Tx 75034 I am an insurance broker. I provided auto/home/fire/renter/life/liability/disability/long term care. #11 260733 American Signs LC 25000 0 25000 Mike Perkins CEO 6205 Chapel Hill Blvd, Suite 500, Plano, TX 75093 The businesss provides commercial signage project management to businesses, as well as designs and manages the production of channel letters, monument signage, pylon and pole signs and other sign projects. -

Dorothy Joyce Kissinger April 26, 1930 - July 31, 2012

PHONE: (972) 562-2601 Dorothy Joyce Kissinger April 26, 1930 - July 31, 2012 Dorothy Joyce Kissinger, age 82, of Weston, Texas passed away July 31, 2012 with her daughter, Cynthia Ann Hendricks. Dorothy was born April 26, 1930 in Celina, Texas to Lester W. Dickerson and Clara C. (Tucker) Dickerson. On December 19, 1946 she married Hubert Loyd Kissinger in Rhea Mills, Texas. Dorothy was a faithful, active servant of the following churches, Cliff Temple Baptist Church in Dallas, First Baptist Church in McKinney, Georgetown Baptist Church in Pottsboro and currently the First Baptist Church in Weston. She was a member of the Eastern Star, McKinney Chapter #518, the Weston Women’s Group and the Ladies Auxiliary to the Veterans of Foreign Wars, Post #7873. Dorothy retired from the United States Postal Service. She worked for the Post Offices in Dallas and Denison, Texas. She was an avid outdoorsman and was known as the family leader. She was instrumental in the lives of her grandchildren and great-grandchildren. She is survived by her daughters, Linda Rankin and husband, Chuck of Frisco, Texas, Debbie Reyno and husband, Michael of Weston, Texas; son-in-law, Chuck Hendricks of Houston, Texas; brothers, Myron Dickerson and wife, Sis of Ft. Worth, Texas, Verlin Ray Dickerson and wife, Betty of El Paso, Texas, and Bobby Dickerson and wife, Pat of Houston, Texas; grandsons, Stephen Barnett of Celina, Texas, Rocky Rankin of Austin, Texas, Brian Hendricks of Houston, Texas and Collin Rankin of Los Angeles, California; granddaughters, Katie Spurgers of Missouri City, Texas, Christine Rankin of Austin, Texas and Samantha Hendricks of Denton, Texas; great-grandchildren, Zoie, Zane, Dakota, Zeke, Sophia; sister-in-law, Dollie Kissinger of Dallas, Texas and many other nieces, nephews and other loved ones. -

Svbordinate Lodges, I.O.O.F

DIRECTORY OF SVBORDINATE LODGES, I.O.O.F. Class HS5ia. Book . T^S Copyright N° COPYRIGHT DEPOSIT DEDICATED TO THE MEMORY OF THOMAS WILDEY THE FOUNDER OF THE NDEPENDENT ORDER OF ODD FELLOWS ON THE CONTINENT OF NORTH AMERICA PRICE, $1.SO NET ^5?is^-^^^ DIRECTORY Subordinate lodges OF THE INDEPENDENT ORDER OF ODD FELLOWS ON THE CONTINENT OF NORTH AMERICA COMPILED AND, PUBLISHED BY GEORGE H. FULLER. GRAND SECRETARY. OF MASSACHUSETTS. THE GRAND LODGe! I. O. O. FM S15 TREMONT STREET. BOSTON 1913 Copyright. 1913. by George H. Fuller THE UNITED STATES OF AMERICA Caustic-Claflin Company, Printers harvard Square Cambridge, Massachusetts ©CJ.A347588 It PREFACE THIS book contains the name, number and location of approximately 17,500 Subordinate Lodges of the Independent Order of Odd Fellows on the Conti- nent of North America, revised to March 20, 1913. The copy was furnished by the Grand Secretaries of the fifty- six Grand Lodges in the United States of America and Dominion of Canada. It is the purpose of the Directory to aid lodges in com- municating one with another. A message transmitted by mail as first-class matter, bearing the name, number and location of any lodge, will be delivered without additional address on the part of the writer. For example, a letter addressed to California Lodge, No. 1, I.O.O.F., San Fran- cisco, California, will be delivered to said lodge, the Post- master at San Francisco supplying the necessary informa- tion as to post-office box or street address of the lodge or Recording Secretary thereof. -

Hour of Arrival (HHARHOSP) 00-23

HOSPITAL DATA DICTIONARY Texas Department of Health Trauma Registry July 24, 2001 TABLE OF CONTENTS Definitions ii 2002 Data File Formats iii Pre-existing Conditions………………………... 17 Patient Demographics Injury Severity Score…………………….……. 18 Trauma Registry Number……………………... 1 (Body Region) Injury Severity……….……….. 18 Patient’s Name……………………….………... 1 (Body Region) Type of Injury…….…………... 18 Patient’s Social Security Number………….….. 1 Facility Number………………………..……… 2 Patient Hospital Cost Medical Record Number………………………. 2 Payor Category……………..………………….. 19 Race …………………………………………… 2 Billed Hospital Charges………….……………. 20 Gender ……..……….………….…………….. 2 Total Reimbursement……………….…………. 20 Date of Birth…………………………………... 3 Prehospital Data Date of Injury……….…………..……………... 3 Respiratory Rate at Scene……………………... 21 County of Injury………………..……………… 4 Systolic Blood Pressure at Scene……………… 21 Cause of Injury…………………..…………….. 4 Motor Response at Scene……………………… 22 Time of Injury…………………..……………... 4 Verbal Response at Scene……………………... 22 County of Residence…………..………………. 5 Eye Opening Response at Scene.……..……….. 23 Place of Injury…………………..……………... 5 Glasgow Coma Score at Scene…………..……. 23 Hospital Admission Transport Date of Arrival………………………………… 7 TDH Firm Number………………….………… 24 Time of Arrival………………………………... 7 Time of Dispatch….………………………….... 24 Alcohol Level Tested………………………….. 8 Time of Scene Arrival……….………………… 25 Alcohol Level………………...……………….. 8 Time of Leaving Scene…………….………….. 25 Systolic Blood Pressure…………...…………... 8 Vehicle Extrication……………….……….…... 26 Diastolic -

HOSPITAL DATA DICTIONARY FINAL DRAFT Texas Department Of

HOSPITAL DATA DICTIONARY FINAL DRAFT Texas Department of Health Trauma Registry December 2, 1999 Acknowledgements Special recognition is due to the Trauma Registry Workgroup members who devoted time and effort toward the development of the hospital data dictionary. Their commitment and hard work are greatly appreciated. Workgroup members include Larry Baggett (Baptist St. Anthony’s Hospital), Phyllis Blanco (Medical Center), Mike Clark (Hermann Hospital), Maggie Crawford (University Medical Center in Lubbock), Michelle Drum (Covenant Medical Center), Judy England (East Texas Medical Center), Gary Kesling (University of Texas Medical Branch), Jim Lyons (Falls County EMS), Cathy McMahon (Covenant Medical Center), Marjorie Mellott (Val Verde Regional Medical Center), Jim Owen (Brooke Army Medical Center), and Charlene Seale (Northwest Texas Health Care System). Special thanks also goes to the Texas Department of Health /Bureau of Emergency Medical Services staff for their involvement with the Workgroup: Tracy Cotner-Pouncy, Brian Haschke, Kathy Perkins, and Carol Wright. Texas Trauma Registry staff include: Jennifer Hunteman (Program Administrator), Dale Cherry (Research Specialist), Andy Blum (Trauma Registry Specialist) and David Zane (Director, Injury Epidemiology and Surveillance). Special acknowledgement goes to Texas hospitals, other state trauma registries, and the American College of Surgeons for providing data dictionaries: Brackenridge Hospital, Children's Medical Center, Parkland Hospital, National Trauma Data Bank (American College of Surgeons), Maryland Trauma Registry, Oregon Trauma Registry, Pennsylvania Trauma Systems Foundation, and Washington Trauma Registry. Data Dictionary Development Process The hospital data dictionary was developed by the Trauma Registry Workgroup. This fifteen member group was formed in May 1999 to address various trauma registry issues including the development of the data dictionary.