Consolidating... on the Wings of Change

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Askari Bank Limited List of Shareholders (W/Out Cnic) As of December 31, 2017

ASKARI BANK LIMITED LIST OF SHAREHOLDERS (W/OUT CNIC) AS OF DECEMBER 31, 2017 S. NO. FOLIO NO. NAME OF SHAREHOLDERS ADDRESSES OF THE SHAREHOLDERS NO. OF SHARES 1 9 MR. MOHAMMAD SAEED KHAN 65, SCHOOL ROAD, F-7/4, ISLAMABAD. 336 2 10 MR. SHAHID HAFIZ AZMI 17/1 6TH GIZRI LANE, DEFENCE HOUSING AUTHORITY, PHASE-4, KARACHI. 3280 3 15 MR. SALEEM MIAN 344/7, ROSHAN MANSION, THATHAI COMPOUND, M.A. JINNAH ROAD, KARACHI. 439 4 21 MS. HINA SHEHZAD C/O MUHAMMAD ASIF THE BUREWALA TEXTILE MILLS LTD 1ST FLOOR, DAWOOD CENTRE, M.T. KHAN ROAD, P.O. 10426, KARACHI. 470 5 42 MR. M. RAFIQUE B.R.1/27, 1ST FLOOR, JAFFRY CHOWK, KHARADHAR, KARACHI. 9382 6 49 MR. JAN MOHAMMED H.NO. M.B.6-1728/733, RASHIDABAD, BILDIA TOWN, MAHAJIR CAMP, KARACHI. 557 7 55 MR. RAFIQ UR REHMAN PSIB PRIVATE LIMITED, 17-B, PAK CHAMBERS, WEST WHARF ROAD, KARACHI. 305 8 57 MR. MUHAMMAD SHUAIB AKHUNZADA 262, SHAMI ROAD, PESHAWAR CANTT. 1919 9 64 MR. TAUHEED JAN ROOM NO.435, BLOCK-A, PAK SECRETARIAT, ISLAMABAD. 8530 10 66 MS. NAUREEN FAROOQ KHAN 90, MARGALA ROAD, F-8/2, ISLAMABAD. 5945 11 67 MR. ERSHAD AHMED JAN C/O BANK OF AMERICA, BLUE AREA, ISLAMABAD. 2878 12 68 MR. WASEEM AHMED HOUSE NO.485, STREET NO.17, CHAKLALA SCHEME-III, RAWALPINDI. 5945 13 71 MS. SHAMEEM QUAVI SIDDIQUI 112/1, 13TH STREET, PHASE-VI, DEFENCE HOUSING AUTHORITY, KARACHI-75500. 2695 14 74 MS. YAZDANI BEGUM HOUSE NO.A-75, BLOCK-13, GULSHAN-E-IQBAL, KARACHI. -

S# BRANCH CODE BRANCH NAME CITY ADDRESS 1 24 Abbottabad

BRANCH S# BRANCH NAME CITY ADDRESS CODE 1 24 Abbottabad Abbottabad Mansera Road Abbottabad 2 312 Sarwar Mall Abbottabad Sarwar Mall, Mansehra Road Abbottabad 3 345 Jinnahabad Abbottabad PMA Link Road, Jinnahabad Abbottabad 4 131 Kamra Attock Cantonment Board Mini Plaza G. T. Road Kamra. 5 197 Attock City Branch Attock Ahmad Plaza Opposite Railway Park Pleader Lane Attock City 6 25 Bahawalpur Bahawalpur 1 - Noor Mahal Road Bahawalpur 7 261 Bahawalpur Cantt Bahawalpur Al-Mohafiz Shopping Complex, Pelican Road, Opposite CMH, Bahawalpur Cantt 8 251 Bhakkar Bhakkar Al-Qaim Plaza, Chisti Chowk, Jhang Road, Bhakkar 9 161 D.G Khan Dera Ghazi Khan Jampur Road Dera Ghazi Khan 10 69 D.I.Khan Dera Ismail Khan Kaif Gulbahar Building A. Q. Khan. Chowk Circular Road D. I. Khan 11 9 Faisalabad Main Faisalabad Mezan Executive Tower 4 Liaqat Road Faisalabad 12 50 Peoples Colony Faisalabad Peoples Colony Faisalabad 13 142 Satyana Road Faisalabad 585-I Block B People's Colony #1 Satayana Road Faisalabad 14 244 Susan Road Faisalabad Plot # 291, East Susan Road, Faisalabad 15 241 Ghari Habibullah Ghari Habibullah Kashmir Road, Ghari Habibullah, Tehsil Balakot, District Mansehra 16 12 G.T. Road Gujranwala Opposite General Bus Stand G.T. Road Gujranwala 17 172 Gujranwala Cantt Gujranwala Kent Plaza Quide-e-Azam Avenue Gujranwala Cantt. 18 123 Kharian Gujrat Raza Building Main G.T. Road Kharian 19 125 Haripur Haripur G. T. Road Shahrah-e-Hazara Haripur 20 344 Hassan abdal Hassan Abdal Near Lari Adda, Hassanabdal, District Attock 21 216 Hattar Hattar -

IBFT- Account Number Formats

IBFT- Account Number Formats Allied Bank Please enter Allied Bank Account Number by following the layout below: Total Digits of Account Number: 13 or 20 Digits Format Example: BBBBAAAAAAAAA or BBBBAAAAAAAAAAAAAAAA BBBB = 4 Digit Branch Code, AAAAAAAAA = 9 Digit Account Number, AAAAAAAAAAAAAAAA = 16 Digit Account Number Apna Microfinance Bank Please enter Apna Microfinance Bank Account Number by following the layout below: Total Digits of Account Number: 16 Digits Format Example: BBBBAAAAAAAAAAAA BBBB = 4 Digit Branch Code, AAAAAAAAA = 12 Digits Askari Bank Please enter Askari Bank Account Number by following the layout below: Total Digits of Bank Account Number: 14 Digits Format Example: BBBB = 4 Digit Branch Code, AAAAAAAAAA = 10 Digit Account Number Branchless Banking Account # Always consist of 11 digits Mobile Number. Al-Baraka Please enter Bank Al-Baraka total digits of account Number: Total Digits of Account Number: 13 Digits Bank Alfalah Please enter Bank Alfalah Account Number by following the layout below: Conventional A/C#: Total Digits of Account Number: 14 Format Example: BBBBAAAAAAAAAA BBBB = 4 Digit Branch Code, AAAAAAAAAA = 10 Digit Account Number Islamic A/C#: Total Digits of Account Number: 18 Digit Format Example: BBBBAAAAAAAAAAAAAA BBBB = 4 Digit Branch Code, AAAAAAAAAAAAAA = 14 Digit Account Number Branchless Banking Account # : Always consist of 11 digits Mobile Number. Bank Al-Habib Please enter Bank Al-Habib Account Number by following the layout below: Total Digits of Account Number: 17 Digit Format -

18-12-2018.Pdf

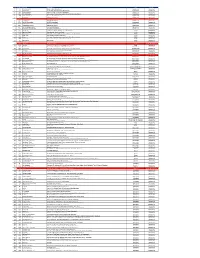

SUPREME COURT OF PAKISTAN AND PRIME MINISTER OF PAKISTAN'S DIAMER BHASHA AND MOHMAND DAM FUND ACCOUNT LIST OF DONOR FOR 19 DEC-18 RECEIPT Bank Depositor Name Amount AL BARAKA BANK (PAKISTAN) LTD MUHAMMAD FAROOQ 200 AL BARAKA BANK (PAKISTAN) LTD Total 200 Allied Bank Limited JAVID AHMED 100,000 Allied Bank Limited TARIQ 50,000 Allied Bank Limited MNA FARRUKH KHAN 50,000 Allied Bank Limited GHULAM MUHAMMAD 35,000 Allied Bank Limited KHALIDA MEMON 30,000 Allied Bank Limited AASIM 25,000 Allied Bank Limited IMRAN 20,000 Allied Bank Limited AHSAN MEHMOOD CHUGHTAI 20,000 Allied Bank Limited QASWAR AZAM 20,000 Allied Bank Limited NADIA IQBAL DAR 20,000 Allied Bank Limited MIRZA ADEED ALI BAIG 20,000 Allied Bank Limited SHAHRYAR 15,000 Allied Bank Limited SAADSHARIF 13,180 Allied Bank Limited muhammad ud din 13,000 Allied Bank Limited RASHID 11,000 Allied Bank Limited AMIR USMAN 10,000 Allied Bank Limited M IMRAN 10,000 Allied Bank Limited ABDUL HAMEED KHAN 10,000 Allied Bank Limited SAHIR MEHMOOD 9,200 Allied Bank Limited MUHAMMAD AYAZ 6,500 Allied Bank Limited KALIM BIN RAFIQUE 6,000 Allied Bank Limited MUHAMMAD ASGHAR 5,000 Allied Bank Limited adnan 5,000 Allied Bank Limited TOBA MALIK 5,000 Allied Bank Limited MUNAWARSULTANA 5,000 Allied Bank Limited ASHRAF ALI 5,000 Allied Bank Limited BILAL 3,500 Allied Bank Limited ABDUL GHAFOOR 3,000 Allied Bank Limited SHAHIDHUSSAINQURESHI 3,000 Allied Bank Limited SAEEDA NASREEN 3,000 Allied Bank Limited ANSAR MEHMOOOD 2,000 Allied Bank Limited AFTAB SAB 2,000 Allied Bank Limited IDRESS 2,000 Allied -

Lt Gen Tariq Khan, HI (M) (Retd), Is Chief Executive & Managing

Lt Gen Tariq Khan, HI (M) (Retd) Lt Gen Tariq Khan, HI (M) (Retd), is Chief Executive & Managing Director of Fauji Fertilizer Company Limited, FFC Energy Limited and Fauji Fresh n Freeze Limited and also holds directorship on the Boards of following: Fauji Fertilizer Bin Qasim Limited Askari Bank Limited Fauji Foods Limited Philip Morris (Pakistan) Limited Fauji Meat Limited FFBL Foods Limited FFBL Power Company Limited Thar Energy Limited Pakistan Maroc Phosphore S.A. He is Chairman of Sona Welfare Foundation (SWF) and Fertilizer Manufacturers of Pakistan Advisory Council (FMPAC) and member of the Board of Governors of Foundation University, Islamabad. The General was commissioned in Pakistan Army in April1977 with the coveted Sword of Honour. During his illustrious service in the Army, he had been employed on various prestigious command, staff and instructional assignments including command of a Strike Corps. He is a graduate of Command and Staff College Quetta and National Defence University Islamabad. He also holds Master Degree in War Studies. He has served on the faculty of Command and Staff College Quetta and National Defence University Islamabad. Since his retirement, he is on the honorary faculty of renowned institutions including National Defence University as a senior mentor. The General possesses vast experience as adviser to the leading corporate entities. He has been awarded Hilal-e-Imtiaz (Military) and is also the first Pakistan Army General who has been conferred upon the U.S ‘Legion of Merit’ by the U.S Government for his meritorious services as a senior representative at U.S CENTCOM in Tampa, Florida. -

Annual REPORT 2011 SILKBANKT

ANNUAl REPORT 2011 SILKBANKT Notice of AGM & Auditors' Review 35 Auditors' Report 39 Financial Statements 43 Six Years' Rnancial Highlights 44 Statement of Financial Position 50 Profit & Loss Account 51 Statement of Comprehensive Income 52 Vision & Mission 02 Cash Row Statement 53 Message from Chairman 04 Statement of Changes in Equity 54 President & CEO's Review 06 Notes to the Financial Statements 55 Senior Management Committee 09 Statement of Written-off Loans 100 Profiles of Board of Directors 13 Achievements & CSR 103 Corporate Information 17 Additional Shareholders' Information 110 Directors' Report 21 Pattern of Share Holdings CDC & Physical 111 Statement of Compliance with 29 Branch Network 114 the Code of Corporate Governance Foreign Correspondents 116 & Statement of Internal Control Proxy Form 119 To be the leader in premier banking, trusted by customers for accessibility, service and innovation; be an employer of choice creating value for all stakeholders In the aftermath of the economic slowdown since 2008, Non-Performing Loans (NPLs) have dampened the profitability dynamics of commercial banks. I am pleased to advise you that contrary to the banking industry trend, your Bank managed to register a significant reduction in NPLs, in each consecutive year since the takeover by the new management. An NPL reduction by the Special Assets Management team of Rs. 3.398 billion and a Provision Reversal of Rs. 1.829 billion was recorded for the year 2011. The Real Estate Asset Management team (REAM) also supported the Special Assets Management team by successfully selling off various properties held as OREO (Other Real Estate Owned), during the year. -

Financial Highlights Quarter & Half Year Ended June 30, 2020 Askari Bank Limited – Basic Info

Financial Highlights Quarter & Half Year ended June 30, 2020 Askari Bank Limited – basic info Commencement of operations April 1992 Sponsors Fauji Foundation Group (71.91%) Entity Rating AA+(by PACRA) Market capitalization - Rupees in billion 21 Market share of deposits 4.65% Branches / sub branches - in Pakistan 535 (including 94 islamic branches) Cities / towns covered 162 International presence Wholesale branch in Bahrain Rep.office in Beijing,China Customers 1.45 million Employees 7,955 Head office / Registered office Islamabad / Rawalpindi Askari Bank Limited – Corporate Brief 1 Balance Sheet – as of June 30, 2020 (Rupees in million) Dec. '19 Jun. '20 YTD ASSETS Cash, bank bal. & lendings 91,332 70,152 -23% Investments - net 305,436 404,482 32% Advances - net 372,914 407,871 9% Fixed & other assets 63,527 64,370 1% Total Assets 833,208 946,875 14% LIABILITIES Borrowings 51,188 89,251 74% Deposits & other accounts 679,299 734,088 8% Subordinated debts 9,992 15,991 60% Other liabilities 50,473 56,783 13% Total Liabilities 790,952 896,113 13% EQUITY Share capital 12,603 12,603 0% Reserves & un-app. profit 25,353 28,574 13% Surplus on reval. of assets 4,300 9,585 123% Total Equity 42,256 50,762 20% Book value per share - Rupees 33.5 40.3 20% Askari Bank Limited – Corporate Brief 2 Profit & Loss – Quarter & half year ended June 30, 2020 (Rupees in million) Profit & Loss Q2 '19 Q2 '20 QoQ HY '19 HY '20 YoY Mark-up earned 15,945 20,805 30% 30,207 42,458 41% Mark-up expensed 10,807 12,230 13% 19,350 28,041 45% Net Interest Income (NII) 5,138 -

Annual Report for the Year Ended December 31, 2012 Cover Concept

Annual Report for the year ended December 31, 2012 Cover Concept In today’s challenging environment, we face unprecedented uncertainties across a range of issues. Yet, we still believe that real success lies in always moving ahead; in the relentless pursuit of solutions. At Askari Bank, we believe in leading the way forward. Our fundamental aim is to integrate our offerings with the changing lifestyles of our valued customers – so that we can better assist in their banking needs and also help in shaping their future. On our cover this year, we express our long- standing conviction – of thinking ahead and banking forward. Annual Report of Askari Bank Limited for 2012 Contents 02 21 Years of Banking Unconsolidated Financial Consolidated Financial 04 Vision & Mission Statements of Askari Bank Statements of Askari Bank 06 Our Thinking 08 Products & Services Limited Limited and its Subsidiaries 12 Corporate Philosophy 16 Corporate Information 63 Statement of Compliance 131 Auditors’ Report to the 17 Entity Ratings 65 Review Report to the Members 18 Directors’ Profile Members 132 Consolidated Statement of Financial 22 Board Committees 66 Auditors’ Report to the Position 24 Management Committees Members 133 Consolidated Profit and Loss 26 Notice of 21st Annual General Meeting 68 Unconsolidated Statement of Financial Account 28 Management Position 134 Consolidated Statement of 69 Unconsolidated Profit and Loss Account Comprehensive Income 29 Organogram 70 Unconsolidated Statement of 135 Consolidated Cash Flow 30 Corporate Social Comprehensive -

Askari-AR-2014.Pdf

For Askari Bank, our relationship with our clients is what matters the most. It is the foundation of our core belief – Pak Watan Hai Apni Jaan (Our Pakistan, Our Pride) – which has guided us through the last twenty- three years. In our cover, we pause and reflect on the essence of what makes us who we are. As Pakistanis, our indomitable spirit is our greatest strength; which has helped us endure and thrive in the most uncertain times. Today, it has become the stepping stone behind our illustrious journey – the enduring bond that unites and defines us for the past we share and the future we wish to create. Annual Report of Askari Bank Limited for 2014 CONTENTS 02 23 Years of Banking Unconsolidated Consolidated 03 Key Financial Highlights 04 Vision and Mission Financial Financial Statements 05 Pakistan’s Profile Statements of of Askari Bank 06 Products & Services Askari Bank Limited and its 10 Corporate Information Limited Subsidiaries 48 Statement of Internal Controls 12 Notice of 23rd Annual General 135 Auditors’ Report to the Meeting 49 Statement of Compliance Members 18 Management 51 Review Report to the Members 136 Consolidated Statement of 19 Organogram 52 Auditors’ Report to the Financial Position Members 20 Chairman’s Message 137 Consolidated Profit and Loss 54 Unconsolidated Statement of Account 21 President’s Review Financial Position 138 Consolidated Statement of 25 Corporate Social Responsibility 55 Unconsolidated Profit and Loss Comprehensive Income 26 Value Added Statement Account 139 Consolidated Cash Flow 27 Financial Review -

Final March 2013

Report for the quarter ended March 31, 2013 banking forward Contents Corporate Information 1 Directors' Review 2 Condensed Interim Unconsolidated Statement of Financial Position 3 Condensed Interim Profit and Loss Account 4 Condensed Interim Unconsolidated Statement of Comprehensive Income 5 Condensed Interim Unconsolidated Cash Flow Statement 6 Condensed Interim Unconsolidated Statement of Changes in Equity 7 Notes to the Condensed Interim Unconsolidated Financial Information 8 Islamic Banking Business - Statement of Financial Position 20 Islamic Banking Business - Profit and Loss Accounts 21 Condensed Interim Consolidated Statement of Financial Position 23 Condensed Interim Consolidated Profit and Loss Account 24 Condensed Interim Consolidated Statement of Comprehensive Income 25 Condensed Interim Consolidated Cash Flow Statement 26 Condensed Interim Consolidated Statement of Changes in Equity 27 Notes to the Condensed Interim Consolidated Financial Information 28 Corporate Information Board of Directors Lt. Gen. Javed Iqbal - Chairman Lt. Gen. (R) Tahir Mahmood Malik Riffat Mahmood Mr. Zafar Alam Khan Sumbal Dr. Bashir Ahmad Khan Mr. Ali Noormahomed Rattansey, FCA Mr. Shahid Mahmud Mr. Muhammad Riyazul Haque Mr. Wazir Ali Khoja Mr. Khawaja Jalaluddin Roomi Mr. M. R. Mehkari - President & Chief Executive Audit Committee Dr. Bashir Ahmad Khan - Chairman Mr. Ali Noormahomed Rattansey, FCA Mr. Wazir Ali Khoja Khawaja Jalauddin Roomi Chief Financial Officer Mr. Saleem Anwar, FCA Company Secretary Mr. M. A. Ghazali Marghoob, FCA Auditors KPMG Taseer Hadi & Co. Chartered Accountants Legal Advisors RIAALAW Advocates & Corporate Counsellors Shariah Advisor Dr. Muhammad Tahir Mansoori Registered / Head Office AWT Plaza, The Mall, P.O. Box No. 1084, Rawalpindi - 46000, Pakistan. Tel: (92 51) 906 3000 Fax: (92 51) 927 2455 E-mail: [email protected] Registrar & Share THK Associates (Pvt) Limited Transfer Office Ground Floor, State Life Building No. -

Of 8 S# Branch Code Branch Name Branch Adress City/Town 71 165 Gilgit Branch Main Bazar Airport Road Gilgit Gilgit 72 731 Ranai Road, Chillas Shop No

S# Branch Code Branch Name Branch Adress City/Town 1 24 Abbottabad Branch Mansera Road Abbottabad Abbottabad 2 312 Sarwarabad, Abbottabad Sarwar Mall, Mansehra Road Abbottabad Abbottabad 3 345 Jinnahabad, Abbotabad PMA Link Road, Jinnahabad Abbottabad Abbottabad 4 721 Mansehra Road, Abbotabad Lodhi Golden Tower Supply Bazar Mansehra Road Abbottabad Abbottabad 5 721A PMA Kakul Abbottabad IJ-97, Near IJ Check Post, PMA Kakul, Abbottabad. Abbottabad 6 351 Ali Pur Chatha Near Madina Chowk, Ali Pur Chattha Ali Pur Chattha 7 266 Arifwala Plot # 48, A-Block, Outside Grain Market, Arifwala Arifwala 8 197 Attock City Branch Ahmad Plaza Opposite Railway Park Pleader Lane Attock City Attock 9 318 Khorwah, District Badin survey No 307 Main Road Khurwah District Badin Badin 10 383 Badyana Pasrur Road Badyana, District Sialkot. Badyana 11 298 Bagh, AJ&K Kashmir Palaza Hadari Chowk BAGH, Azad Kashmir BAGH AJK 12 201 Bahawalnagar Branch Grain Market Minchanabad Road Bahawalnagar Bahawalnagar 13 305 Haroonabad Plot No 41-C Ghalla Mandi, Haroonabad District Bahawalnagar Bahawalnagar 14 390 Grain Market, Model Town-B, Bahawalpur Plot No. 112/113-B, Model Town-B, Bahawalpur Bahawalpur 15 134 Channi Goth Bahawalpur Uch Road Channi Goth Tehsil Ahmed Pur East Bahawalpur 16 269 UCH Sharif, District Bahawalpur Building # 68-B, Ahmed Pur East Road, Uch Sharif, Distric Bahawalpur Bahawalpur 17 25 Noor Mahal Bahawalpur 1 - Noor Mahal Road Bahawalpur Bahawalpur 18 261 Bahawalpur Cantt Al-Mohafiz Shopping Complex, Pelican Road, Opposite CMH, Bahawalpur Cantt Bahawalpur 19 750 IBB Circular Rd Bhawalpur Khewat No 38 Ground & First floor Aziz House Rafique Sabir Building Circular Road Bahawalpur Bahawalpur 20 258A Bannu Cantt Shop No. -

Atms (Operational/Closed)

S. No. ATM ID Location ATM Address City Status 1 24 Abt Abbottabad Mansera Road Abbottabad Abbottabad Operational 2 312 Sarwar Mall Sarwar Mall, Mansehra Road Abbottabad Abbottabad Operational 3 345 Abt Jinnahabad PMA Link Road, Jinnahabad Abbottabad Abbottabad Operational 4 721 Ibb Abbottabad Lodhi Golden Tower Supply Bazar Mansehra Road Abbottabad Abbottabad Operational 5 1024 CMH Abbottabad Mansera Road Abbottabad Abbottabad Operational 6 1721 Abt Kakool 1 Abbottabad Kakool 1 Abbottabad Operational 7 2024 Amc Abbottabad Mansera Road Abbottabad Abbottabad Under Maintenance 8 2721 Abt Kakool 2 Abbottabad Kakool 2 Abbottabad Operational 9 3721 Ibb BRC Abbottabad Ibb BRC Abbottabad Abbottabad Operational 10 4721 Abt Kakool 3 Abbottabad Kakool 3 Abbottabad Operational 11 5721 Abbottabad Kakool 4 Abbottabad Kakool 4 Abbottabad Operational 12 6721 CSD SHOP PMA KAKUL CSD SHOP PMA KAKUL Abbottabad Operational 13 3024 FF CENTRE ABBOTTABAD FF CENTRE ABBOTTABAD Abbottabad Operational 14 131 Kam Kamra Cantonment Board Mini Plaza G. T. Road Kamra. Attock Operational 15 149 Pgh Pindi Ghaib Main Katcheri Road Pindi Gheb Attock Operational 16 197 Attock City Ahmad Plaza Opposite Railway Park Pleader Lane Attock City Attock Operational 17 252 Fateh Jang Main Rawalpindi Road, Fateh Jang Attock Operational 18 333 Khour POL Khour Company,Khour,Tehsil Pindi Gheb, District Attock Attock Operational 19 344 Hassanabdal Near Lari Adda, Hassanabdal, District Attock Attock Operational 20 1131 Kam Hazroo Kam Hazroo Attock Operational 21 1737 Ibb Hassan Abdal Ibb