Pteg TSC Rail Infra Response Final.Pdf

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Investing for the Future

The new ScotRail franchise: good for passengers, staff and Scotland Improving your journey from door to door magazine Abellio ScotRail Investing for the future The Abellio Way Magazine – Abellio ScotRail special – Spring 2015 Travelling on the Forth Bridge and enjoying the wonderful view A northern gannet flying in front of Bass Rock SCOTRAIL SPECIAL - SPRING 2015 3 CONTENTS Ambitious plans and Abellio It is with enormous pleasure that I find myself writing 4 WE ARE ABELLIO the introduction to this special edition of The Abellio What can you expect from us? Way Magazine from my home in Edinburgh. When Abellio was granted the privilege of operating 6 JEFF HOOGESTEGER MEETS TRANSPORT Scotland’s rail services, I had no hesitation in making this my home. You may consider that a rather self- MINISTER DEREK MACKAY serving decision, after all who wouldn’t choose to live “This is an incredibly exciting period for transport in this beautiful country! However, as a Dutchman, it in Scotland” won’t surprise you that it was also a sensible business decision. 10 ABELLIO’S VISION FOR THE NEW The Scottish Government has ambitious plans to SCOTRAIL FRANCHISE transform its railways and I am grateful to them for Good for passengers, good for staff and choosing Abellio to assist in that purpose. We have many exciting and challenging plans for ScotRail, as good for Scotland you will read in this special edition, and it is my intention to work with the team wherever possible 13 WORKING TOGETHER FOR THE PASSENGER to deliver them. ScotRail and Network Rail Performance for passengers 14 BOOSTING TOURISM Living here, I will also be travelling by train most days to our new UK headquarters in Glasgow, and regularly Travel the Great Scenic Railways of Scotland using other parts of the ScotRail network. -

Glasgow – Edinburgh & N Orth Berw Ick / D Unbar

11812 ScotRail is part of the Published by (Textphone Service – for the hard of hearing) 18001 0800 2 901 912 OR 0800 2 901 912 Assisted Travel [email protected] 0344 0141 811 can contact Customer Relations on: general enquiries, telesales you all including For www.scotrail.co.uk ScotRail (please note, calls to this number may be recorded) 4803457 50 49 EnquiriesNational Rail Revised Abellio ScotRail Ltd. ScotRail Abellio Timetable National Rail Longniddry Drem Prestonpans network Calling at: Haymarket Musselburgh Wallyford TRAIN TIMES TRAIN 2016 to 7 August 20 March Glasgow – Edinburgh & Glasgow – Edinburgh North Berwick / Dunbar via Motherwell & Carstairs Glaschu – Dùn Èideann & Bearaig a Tuath / Dùn Bàrr taobh Thobar na Màthar & Chaisteal Tarrais Welcome to your new train timetable Station Facilities From 20 March to 7 August, Glasgow Queen Street High Level station will be closed to allow us Carluke P to carry out essential renewal, maintenance and preparatory enhancement work in the tunnel Carstairs P that leads to and from the station. The concrete track bed that runs the complete length of Drem U the tunnel will be replaced throughout this 20 week period. During this time longer distance Dunbar * S trains to/from Aberdeen and Inverness will be diverted to Glasgow Central High Level station. Edinburgh * S All other services that normally start/terminate at Glasgow Queen Street High Level station will Glasgow Central * S now run to/from Glasgow Queen Street Low Level. By carrying out this work now, it will allow for Haymarket S the introduction of electric trains on the route between Edinburgh and Glasgow Queen Street Longniddry U High Level from December this year. -

Firstgroup Plc Annual Report and Accounts 2015 Contents

FirstGroup plc Annual Report and Accounts 2015 Contents Strategic report Summary of the year and financial highlights 02 Chairman’s statement 04 Group overview 06 Chief Executive’s strategic review 08 The world we live in 10 Business model 12 Strategic objectives 14 Key performance indicators 16 Business review 20 Corporate responsibility 40 Principal risks and uncertainties 44 Operating and financial review 50 Governance Board of Directors 56 Corporate governance report 58 Directors’ remuneration report 76 Other statutory information 101 Financial statements Consolidated income statement 106 Consolidated statement of comprehensive income 107 Consolidated balance sheet 108 Consolidated statement of changes in equity 109 Consolidated cash flow statement 110 Notes to the consolidated financial statements 111 Independent auditor’s report 160 Group financial summary 164 Company balance sheet 165 Notes to the Company financial statements 166 Shareholder information 174 Financial calendar 175 Glossary 176 FirstGroup plc is the leading transport operator in the UK and North America. With approximately £6 billion in revenues and around 110,000 employees, we transported around 2.4 billion passengers last year. In this Annual Report for the year to 31 March 2015 we review our performance and plans in line with our strategic objectives, focusing on the progress we have made with our multi-year transformation programme, which will deliver sustainable improvements in shareholder value. FirstGroup Annual Report and Accounts 2015 01 Summary of the year and -

Great Britain Passenger Rail: the Current Expected Timetable

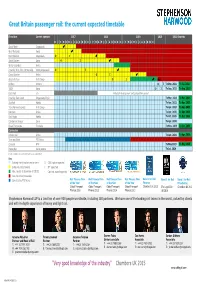

Great Britain passenger rail: the current expected timetable Franchise Current operator 2017 2018 2019 2020 2021 Onwards DJFMA MJJASONDJFMA MJJASONDJFMA MJJASOND South West Stagecoach West Midlands Govia East Midlands Stagecoach O I South Eastern Govia O I Wales & Borders Arriva InterCity W.C./W.C. Partnership Virgin/Stagecoach O I Cross Country Arriva OI Great Western First Group OI Apr. Chiltern Chiltern OITo Dec. 2021 To Jul. 2022 TSGN Govia O I To Sep. 2021 To Sep. 2023 East West n/a Potential development and competition period InterCity East Coast Stagecoach/Virgin To Mar. 2023 To Mar. 2024 ScotRail Abellio To Apr. 2022 To Apr. 2025 TransPennine Express First Group To Apr. 2023 To Apr. 2025 Northern Arriva To Apr. 2025 To Apr. 2026 East Anglia Abellio To Oct. 2025 To Oct. 2026 Caledonian Sleeper Serco To Apr. 2030 Essex Thameside Trenitalia To Nov. 2029 To Jun. 2030 Concession London Rail Arriva To Apr. 2024 To Apr. 2026 Tyne and Wear PTE Nexus Crossrail MTR To May 2023 To May 2025 MerseyRail Serco/Abellio To Jul. 2028 Based on publicly available information as at 1 April 2017 Key Existing franchise/concession term O OJEU notice expected Extension/direct award I ITT expected Max. length at discretion of DfT/TS Contract award expected New franchise/concession Operated by PTE Nexus Rail Finance Firm Rail Finance Firm Rail Finance Firm Rail Finance Firm Band 1 for Rail Band 1 for Rail Band 1 for Rail of the Year of the Year of the Year of the Year Finance Franchising Global Transport Global Transport Global Transport Global Transport Chambers UK 2015 The Legal 500 Chambers UK 2017 Finance 2016 Finance 2015 Finance 2014 Finance 2013 UK 2016 Stephenson Harwood LLP is a law firm of over 900 people worldwide, including 150 partners. -

Scotrail Franchise – Franchise Agreement

ScotRail Franchise – Franchise Agreement THE SCOTTISH MINISTERS and ABELLIO SCOTRAIL LIMITED SCOTRAIL FRANCHISE AGREEMENT 6453447-13 ScotRail Franchise – Franchise Agreement TABLE OF CONTENTS 1. Interpretation and Definitions .................................................................................... 1 2. Commencement .......................................................................................................... 2 3. Term ............................................................................................................ 3 4 Franchisee’s Obligations ........................................................................................... 3 5 Unjustified Enrichment ............................................................................................... 4 6 Arm's Length Dealings ............................................................................................... 4 7 Compliance with Laws................................................................................................ 4 8 Entire Agreement ........................................................................................................ 4 9 Governing Law ............................................................................................................ 5 SCHEDULE 1 ............................................................................................................ 7 PASSENGER SERVICE OBLIGATIONS ............................................................................................. 7 SCHEDULE 1.1 ........................................................................................................... -

Class 150/2 Diesel Multiple Unit

Class 150/2 Diesel Multiple Unit Contents How to install ................................................................................................................................................................................. 2 Technical information ................................................................................................................................................................. 3 Liveries .............................................................................................................................................................................................. 4 Cab guide ...................................................................................................................................................................................... 15 Keyboard controls ...................................................................................................................................................................... 16 Features .......................................................................................................................................................................................... 17 Global System for Mobile Communication-Railway (GSM-R) ............................................................................. 18 Registering .......................................................................................................................................................................... 18 Deregistering - Method 1 ............................................................................................................................................ -

Scotrail's Top Ten Busiest Trains

transport.gov.scot ScotRail’s Top Ten Busiest Trains Report May 2018 ScotRail’s top ten busiest trains Transport Scotland 1. The train counts process – introduction 1.1 The data in this Ten Busiest Trains publication has been derived from a mix of manual snapshot counts and Automated Passenger Counts (APC). Fitment of Automatic Passenger Counting (APC) equipment has been completed across 40% of the fleet, and this will allow ScotRail better to manage its train fleet efficiently going forward, as the equipment provides more frequent and accurate passenger loading data. 1.2 It is a requirement of the Franchise Agreement that the Franchisee shall undertake a minimum of four counts per year, once automated passenger counting equipment has been installed (with the exception of the Class 314 trains, where the equipment has not been fitted as they are due to go off-lease at the end of the year; therefore, manual counts are still undertaken). Previously, all passenger counts was undertaken via manual ‘snapshot’ surveys which were undertaken annually. 1.3 ScotRail’s franchise obligation is to use reasonable endeavours to allocate its train fleet and resources in the most effective way, to provide passengers with a reasonable expectation of a seat within 10 minutes of boarding a train, and to minimise any forecast overcrowding. The exception is on non-stop train journeys between Glasgow Central and Paisley Gilmour Street. This is because a journey between those two stations is served by 8 trains per hour in either direction, with a journey time of ten or eleven minutes. 1.4 The passenger carrying capacity for each service and passenger numbers are incorporated into a Train Plan which ScotRail is obliged to prepare and submit to Transport Scotland for consideration & approval, for each timetable change in May and December. -

Great Britain

Thurso Georgemas Junction Wick Helmsdale Great Britain Lairg Tain Invergordon Garve Arriva Trains Dingwall Wales c2c Nairn Forres Elgin Keith Caledonian Achnasheen Inverness Sleeper Strathcarron Huntly Chiltern Plockton Railways Stromeferry Kyle of Lochalsh Inverurie CrossCountry October 2016 Aviemore East Midlands Trains ScotRail Dyce Eurostar Kingussie Grand Central Spean Aberdeen Great Airport services: Heathrow Express, Stansted Express, Gatwick Express Glenfinnan Bridge Northern Mallaig CrossCountry Limited service* Fort Blair Atholl Virgin Trains Stonehaven Greater William East Coast Anglia ScotRail Great Not all lines shown in London area Rannoch Caledonian Montrose Western Sleeper denoted by area within grey line Pitlochry Railway Arbroath Hull Trains Tyndrum London Underground Circle Line Oban Perth Island Line Dalmally Crianlarich Glasgow Underground Gleneagles Dundee London Midland Dunblane Leuchars London Overground Airport interchange Arrochar & Tarbet Stirling Ferry Alloa Merseyrail Larbert Kirkcaldy Railair coach link with Heathrow Airport Dunfermline Northern Garelochhead ScotRail Inverkeithing Falkirk ScotRail Grahamston EDINBURGH Helensburgh Upper Balloch Waverley Polmont Southern Milngavie North Berwick Train Open Helensburgh Central Lenzie Operating Access Falkirk Bathgate Dunbar Southeastern Dumbarton Central High Companies Operators Maryhill Cumbernauld Haymarket Westerton Springburn Berwick-upon-Tweed South West Trains Train operating companies in roman Partick Queen Street Airdrie Galashiels TfL Rail Open access -

Rail Ops Map

Thurso Wick Helmsdale 2016 Great Britain Lairg National Rail Elgin Passenger Operators Dingwall Inverness Thirty-third edition (December 2015) Kyle of Lochalsh Aviemore Aberdeen Abellio Greater Anglia Abellio Mallaig Arriva Trains Wales Arriva Trains UK Ltd Caledonian Sleeper Serco Group plc Chiltern Railways Arriva Trains UK Ltd Fort William Pitlochry CrossCountry Trains Arriva Trains UK Ltd c2c National Express Group plc East Midlands Trains Stagecoach Group plc Eurostar Eurostar International Ltd Dundee Oban Crianlarich Perth First Hull Trains First Group plc/Renaissance Trains First TransPennine Express First Group plc/Keolis SA Govia Thameslink Railway Go-Ahead Group plc/Keolis SA (Thameslink, Great Northern, Southern, Gatwick Express) Cardenden Grand Central Railway Arriva Trains UK Ltd Stirling Alloa Kirkcaldy North Berwick Balloch Great Western Railway First Group plc Gourock Milngavie Dunbar Heathrow Connect First Group plc/BAA Cumbernauld Drem Wemyss Bay Glasgow Bathgate Heathrow Express BAA Airdrie Edinburgh Largs London Midland Go-Ahead Group plc/Keolis SA Berwick upon Tweed Neilston Carstairs East London Overground Arriva Trains UK Ltd/MTR Corporation Ltd Ardrossan Kilbride Harbour Larkhall Merseyrail Serco-Abellio Lanark Tweedbank Northern Rail Serco-Abellio Chathill ScotRail Abellio Ayr South West Trains Stagecoach Group plc Southeastern Go-Ahead Group plc/Keolis SA TfL Rail TfL/MTR Corporation Ltd (Crossrail from 2018 ) Virgin Trains Virgin Group Ltd/Stagecoach Group plc Dumfries Virgin Trains East Coast Stagecoach Group -

Glasgow – Edinburgh Via Shotts Glaschu Taobh Shotts

11260 ScotRail is part of the Published by (Text Relay Service – for the hard of hearing) 18001 0800 2 901 912 OR 0800 2 901 912 Disabled Assistance 0845 601 5929 scotrailcustomer.relations@firstgroup.com Relations Customer ScotRail 08457 55 00 33 ScotRail Telesales www.scotrail.co.uk ScotRail (please note, calls to this number may be recorded) 08457 48 50 49 National Rail Enquiries First ScotRail Ltd. ScotRail First National Rail network ES M I T – Dùn Èideann N I A R Calling at: Fauldhouse West Calder Livingston South Hailes Wester Slateford A BETTER WAY TO GO. TO A BETTER WAY T 18 May – 13 December 2014 Glasgow – Edinburgh via Shotts Glaschu taobh Shotts Welcome to your new train timetable Station Facilities All trains in this timetable are ScotRail services operated by First, except where otherwise Addiewell U stated. Enhancements include : Monday to Friday peak time services between Aberdeen and Bellshill S Inverurie; additional Monday to Saturday services between Glasgow and Oban; through trains Breich U between Balloch, Dalmuir and Cumbernauld; additional Monday to Friday services between Cambuslang S Glasgow and Ayr; through trains between Edinburgh and Ayr via Carstairs; additional hourly Carfin U Monday to Saturday services between Glasgow and Gourock and an additional Monday to Friday Cleland U early morning service from Wemyss Bay to Glasgow. On Sundays, enhancements include : Curriehill U additional services between Glasgow and Aberdeen; a later train from Glasgow to Wemyss Bay in Edinburgh * S the evening; an extra lunchtime train from Glasgow to Ardrossan Harbour offering an improved Fauldhouse U Campbeltown ferry connection and the introduction of Sunday services at Ardrossan Town, Glasgow Central * S Anderston and between Glasgow, Maryhill and Anniesland. -

First Scotrail Reducing Sickness Absence and Promoting a Healthy Workforce

First Group – First ScotRail Reducing Sickness Absence and promoting a healthy workforce Introduction First ScotRail is the largest regional train operating company in the UK covering the widest geographical area. First ScotRail holds the franchise to operate 95% of passenger rail service within Scotland as well as the Caledonian Sleeper services between Scotland and London. The company has integrated staff wellbeing into its human resources strategy since 2006. A key aim has been to manage employee health more proactively, reducing sickness absence due to stress, musculoskeletal injuries and lifestyle-related factors such as poor diet. Background First ScotRail had no defined people policy during the first year of the franchise, which commenced in October 2004. A range of issues and concerns were noted: A workforce with an 80% majority of males, which had led to an entrenched “macho” culture where change was not readily embraced – and the promotion of healthy lifestyles was not taken seriously. In addition, the workforce is ageing and a large majority of staff are with the railways from leaving school until retirement - as evidenced in very low staff turnover. Sickness absence levels were high at 6.2% in 2006/7. The main reasons for sickness absence were musculoskeletal and mental health problems. First ScotRail set out to proactively address all these issues. Most of their employees are shift workers and First ScotRail took action to help and support staff in achieving good work life balances and positive wellbeing at their workplaces. As a lot of families work within the company, they also chose to tackle poor lifestyle choices within the family setting as well as the workplace. -

The New Scotrail Franchise: Your Roadshow February – March 2015

The new ScotRail franchise: your roadshow February – March 2015 Hosted by: members of the Abellio ScotRail mobilisation team 2 Welcome to the Abellio family! Abellio UK Abellio Germany Abellio The Netherlands Abellio Scandinavia 20,000 employees 1.7m passengers every day 2,786 train vehicles 1,487 buses 236 trams 3 What do we stand for? Our strategic foundations • the customer is king • we think from door-to-door • we work throughout Europe • we are cost conscious • we make the difference together • we care for our environment 4 What Transport Scotland want Their priorities for delivery: • improved connections across Scotland and internationally • better journey times, better reliability, quality and accessibility • increased safety, more innovation • continuously improving performance and organisation • low-carbon technology and infrastructure; reduced emissions 5 Why our bid won Together we’re going to be in the spotlight! • Dutch best practice and innovation • growing the off-peak by 72% • our community focus and growing local economies • the new trains • the way we work • national rail network experience from Holland – biennial rail summit 6 How we want to make a difference Ini%aves & The Abellio investments Leadership Way Journey Disrupon %mes and RTR Partnership Colleagues working A naonal railway that Economic Customers Scotland’s growth proud of 7 Our initiatives and investments Our stations: improving the customer experience • 10 staffed information desks • CCTV investment – coverage at all stations; more monitors; upgraded cameras