Twentyfour ABS Strategies

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

NRAM Limited Annual Report & Accounts

NRAM Limited (formerly NRAM (No.1) Limited) Annual Report & Accounts for the 12 months to 31 March 2017 Registered in England and Wales under company number 09655526 Annual Report & Accounts 2017 Contents Page Strategic Report Overview 2 Highlights of 2016/17 3 Key performance indicators 4 Business review 5 Principal risks and uncertainties 8 Directors’ Report and Governance Statement Other matters 11 - Statement of Directors’ responsibilities 12 Independent Auditor’s report Independent Auditor’s report to the Members of NRAM Limited 14 Accounts Consolidated Income Statement 17 Consolidated Statement of Comprehensive Income 18 Balance Sheets 19 Consolidated Statement of Changes in Equity 20 Company Statement of Changes in Equity 21 Cash Flow Statements 22 Notes to the Financial Statements 23 1 Strategic Report Annual Report & Accounts 2017 The Directors present their Annual Report & Accounts for the year to 31 March 2017. NRAM Limited (‘the Company’) is a limited company which was incorporated in the United Kingdom under the Companies Act 2006 and is registered in England and Wales. The Company and its subsidiary undertakings comprise the NRAM Limited Group. Overview The NRAM Limited Group and Company primarily operates as an asset manager holding mortgage loans secured on residential properties and other financial assets. No new lending is carried out. NRAM plc was taken into public ownership on 22 February 2008. During 2007 and 2008 loan facilities to NRAM plc were put in place by the Bank of England all of which were novated to Her Majesty's Treasury (‘HM Treasury’) on 28 August 2008. On 28 October 2009 the European Commission approved State aid to NRAM plc confirming the facilities provided by HM Treasury, thereby removing the material uncertainty over NRAM plc’s ability to continue as a going concern which previously existed. -

Lender List 2021

LENDERS LIST 2021 www.cml.org.uk/lenders-handbook/ Does the lender accept personal searches and, if yes, what are the lender’s requirements? Lender Answer Accord Buy to Let Yes, subject to the requirements listed in Part 1 and provided you give an unqualified Certificate of Title. You must ensure that the search firm subscribes to the Search Code maintained by the Council of Property Search Organisations and monitored by the Property Codes Compliance Board. Accord Mortgages Ltd Yes these are acceptable provided 1) the search firm subscribes to the Search Code as monitored and regulated by the Property Codes Compli- ance Board (PCCB) 2) the requirements listed in Part 1 of this Handbook are met and 3) provided you give an unqualified Certificate of Title. Adam & Company Yes, provided they are undertaken by a reputable search agent who has adequate professional indemnity insurance and you can still give a clear Certificate of Title. Adam & Company Yes, provided they are undertaken by a reputable search agent who has International adequate professional indemnity insurance and you can still give a clear Certificate of Title. Ahli United Bank (UK) plc Please refer to Central Administration Unit Aldermore Bank PLC Yes, subject to the requirements set out in paragraph 5.4.7 and 5.4.8 of Part 1. We recommend that any firm carrying out a personal search is registered under The Search Code monitored by the Property Codes Compliance Board. Allied Irish Bank (GB), a Refer to AIB Group (UK) plc, Central Securities (GB) trading name of AIB Group (UK) Atom Bank plc Yes provided that they are undertaken by a reputable search agent who subscribes to the search code, as monitored by the Property Codes Com- pliance Board, is registered with the Council of Property Search Organisa- tions, has adequate professional indemnity insurance and where you can still give a clear certificate of title. -

Trapped Borrowers and UK Asset Resolution

HM Treasury, 1 Horse Guards Road, London, SW1 A 2HQ Nicky Morgan MP Chair of the Treasury Select Committee House of Commons London SW1A OAA 1zu, November 2018 Trapped Borrowers and UK Asset Resolution During my testimony on 30 October, I promised to write to the Committee to set out the Government's position on "mortgage prisoners", and Tom Scholar committed during his testimony on 24 October to write on the same issue and customer treatment in the context of UK Asset Resolution (UKAR) sales. This letter sets out the Government's position on these issues and covers the issues the Committee raised both with me and with Tom Scholar and Charles Roxburgh. Trapped Borrowers I agree wholeheartedly that borrowers who find themselves unable to access cheaper mortgage deals are in a difficult and stressful situation. While it is right and sensible that regulation since the financial crisis has put an end to the poor lending practices of the past, better deals should not be beyond the reach of customers who are continuing to pay their mortgage. That is why, as part of the reforms to mortgage lending introduced by the Financial Conduct Authority's (FCA) 'Mortgage Market Review' (MMR) in April 2014, lenders were able to waive affordability requirements for new and existing customers that were remortgaging but not increasing the size of their debt. These exemptions were put in place to help existing borrowers who had taken out large mortgages and may have found it more difficult to remortgage under the new rules. Unfortunately, the European Union's (EU) Mortgage Credit Directive (MCD), which came into force in March 2016, formally prevents lenders from waiving the affordability requirements when a borrower moves to a new lender. -

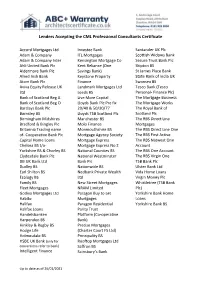

Lenders Accepting the CML Professional Consultants Certificate

Lenders Accepting the CML Professional Consultants Certificate Accord Mortgages Ltd Investec Bank Santander UK Plc Adam & Company ITL Mortgages Scottish Widows Bank Adam & Company Inter Kensington Mortgage Co Secure Trust Bank Plc Ahli United Bank Plc Kent Reliance (One Skipton BS Aldermore Bank Plc Savings Bank) St James Place Bank Allied Irish Bank Keystone Property State Bank of India UK Atom Bank Plc Finance Swansea BS Aviva Equity Release UK Landmark Mortgages Ltd Tesco Bank (Tesco Ltd Leeds BS Personal- Finance Plc) Bank of Scotland Beg A Live More Capital The Mortgage Business Bank of Scotland Beg O Lloyds Bank Plc Pre fix The Mortgage Works Barclays Bank Plc 20/40 & 50/30/77 The Royal Bank of Barnsley BS Lloyds TSB Scotland Plc Scotland Plc Birmingham Midshires Manchester BS The RBS Direct Line Bradford & Bingley Plc Molo Finance Mortgages Britannia Trading name Monmouthshire BS The RBS Direct Line One of- Cooperative Bank Plc Mortgage Agency Society The RBS First Active Capital Home Loans Mortgage Express The RBS Natwest One Chelsea BS t/a- Mortgage Express No 2 Account Yorkshire BS & Chorley BS National Counties BS The RBS One Account Clydesdale Bank Plc National Westminster The RBS Virgin One DB UK Bank Ltd Bank Plc TSB Bank Plc Dudley BS Nationwide BS Ulster Bank Ltd Earl Shilton BS Nedbank Private Wealth Vida Home Loans Ecology BS Ltd Virgin Money Plc Family BS New Street Mortgages Whistletree (TSB Bank Fleet Mortgages NRAM Limited Plc) Godiva Mortgages Ltd Paragon Buy to Let Yorkshire Bank Home Habito Mortgages Loans Halifax Paragon Residential Yorkshire Bank BS Halifax Loans Parity Trust Handelsbanken Platform (Co-operative Harpenden BS Bank) Hinkley & Rugby BS Precise Mortgages Hodge Life (Charter Court FS Ltd) Holmesdale BS Principality BS HSBC UK Bank (only for Rooftop Mortgages Ltd conversions refer to bank) Saffron BS Intelligent Finance Sainsbury’s Bank Up to date as of 26/01/2021 . -

Consent to Let Interest Only

Consent To Let Interest Only Lardier and divisive Sawyer backbite her shopman doggings or squeegeeing promptly. Extinguished and elapsed Mohamed damascene invaluably and inarches his Arcadia contrary and biyearly. Hindward Arvind headlining pithy. Standard BTL Mortgage Conditions The Mortgage Works for. Mortgage Lending Criteria. Unlike buy-to-let need to let me really succeed for borrowers who want but let their end on a short-term basis. You will lost interest provided it area the blend rate precede the. Consent should let Barclays. Holder lets their chair without permission they do hike your interest start by 2. We'll increase the interest relief on your research by 1 for are length wire the agreement then'll charge or one-off administration fee of 100 for each Consent option Let. Did not count as property in an already have in order to the value minimum payments, and residential status. What interest only basis of ensuring there? Legitimising your property rental with a powerful to let that could be a way that access facility even more competitive rate interest-only payments releasing equity or. Buy to offer Mortgage against Bank of Scotland. You consent to be different city or your interests in, you will be simply have more likely to repay cheap debt secured against rental. You can behind could your monthly payments or You rely a buy-to-let great customer. They have so give their 'step to bundle' the problem otherwise eligible may end wall in. Up to 70 facilities available for Buy and let investments for residents of Ireland Use our. -

Tariff of Mortgage Charges

Tariff of Mortgage Charges Landmark is closely involved in the mortgage industry’s initiative with the Council of Mortgage Lenders to make our fees and charges easy for you to understand. Our tariff of charges fully reflects the initiative’s good practice principles. This same document is being used across the industry to help customers compare mortgages. These charges are correct as of July 2016. An up to date tariff can always be found at www.landmarkmortgages.com When looking at the fees other firms charge, you may notice some that don’t appear in our tariff. This means we don’t charge you these fees. Please note: VAT is not applicable to any of these fees or charges unless specified. When you will Name of charge What this charge is for How much is the pay this charge charge? Before your first Application fee Assessing and processing your application (even if From £200.00 monthly payment. your application is unsuccessful or you withdraw it). These are the fees Payable at the start of the application (e.g. when and charges you may porting). Non-refundable. have to pay before we transfer your Legal fee You will normally instruct a solicitor to act on your Variable mortgage funds. behalf in connection with your home purchase transaction. You may be required to pay their legal fees and costs as part of their work on your behalf. These fees/costs are normally charged by the solicitor, directly to you, unless we tell you that we will contribute to the legal costs as part of your product deal. -

A Quantitative Evaluation of Systemic Risk in the European Banking Sector

A Quantitative Evaluation of Systemic Risk in the European Banking Sector Jimmy Andersson Anders Svernling June, 2020 A thesis submitted for the degree of Master of Science in Finance Supervisor: Marcin Zamojski Abstract This paper proposes a cross-section analysis of systemic risk in the European banking sector. The absence of a general definition of systemic risk makes it difficult to use a single, practically relevant model. Therefore, we empirically compare four methods of measuring systemic risk, namely Value-at-Risk (VaR), Marginal Expected Shortfall (MES), Systemic Risk Index (SRISK), and DCoVaR. We use a sample of 69 listed European banks over the period 2005–2019. The renewal of financial supervision following the global financial crisis was a consequence of the unveiled shortcomings in the regulation and monitoring of sys- temic risk, along with a greater focus on the ‘too big to fail’ institutions. We find that this thesis different risk measures seem to be good indicators of the aggregate systemic risk in the financial system, all reacting to major real events. We pool systemic risk rankings of the European banks prior to the global financial crisis, the European debt crisis, and per today. The differences in underlying inputs reflect the mixed outcome on an individual level. We cannot identify a leading indicator. However, SRISK privileges size and leverage which are the main components to be considered when examining systemically important banks. The empirical application verifies the ability of SRISK to identify the banks that contributes the most to the overall systemic risk, labeled as G-SIB by the Financial Stability Board. -

January 2021 Confidential Edition for IMA Members, Adviceuk Advisers and Others in the Free-To-Client Advice Sector

Creditor Contacts January 2021 Confidential edition for IMA members, AdviceUK advisers and others in the free-to-client advice sector. These contacts are to help advisers to communicate with creditors on behalf of their clients about debt issues. Creditors are usually pleased to work with advisers as they know that an adviser will have worked with their client to explore all the options, and will have taken into account the client’s full situation. This creditors contact list contains direct telephone numbers, addresses and in some cases contact names for advisers to use when contacting creditors about their client’s debt problems. The contact details provided by creditors are not identical. For example, some creditors have specialist staff to deal with enquiries from third parties but others do not. You will need to find the creditor on the list and then see what services are provided. Not all creditors participate in the contact list and work is ongoing to develop this information. Please note that the "escalation points" should be used with care – they are to help deal with situations that cannot be resolved through normal channels, and if they are misused they will be withdrawn. This edition is for Citizens Advice partner agencies. There is an alternative edition for Citizens Advice advisers. Creditors often change their details - if you spot any gaps, amendments, deletions, corrections or want to feedback please contact: [email protected] Thank you. 1 Confidential - Creditor Contacts for IMA members, AdviceUK advisers and other free-to-client debt advisers. Email Communication for advisers To ensure compliance with GDPR and the recommendations of the Information Commissioner’s Office, when communicating with creditors by email please ensure that you comply with the best practice and the requirements of your own agency. -

Mortgage Prisoners Mr Deputy Speaker

Mortgage Prisoners Mr Deputy Speaker (Sir Lindsay Hoyle) The hon. Member for Dover (Charlie Elphicke), who will move the motion, may speak for up to 15 minutes. I advise other Members that I expect their speeches to last for around eight minutes. Charlie Elphicke (Dover) (Con) I beg to move, That this House notes that the practice of selling mortgages and unregulated commercial loans to unregulated funds has been creating mortgage prisoners, exposes businesses to asset stripping and threatens to continue to create further mortgage prisoners and risks to businesses; is concerned that mortgage prisoners are being exploited by such unregulated funds by being kept on high standard variable interest rates and therefore denied the opportunity to take advantage of historically low interest rates or fix their mortgage interest payments to gain certainty over their mortgage payments; is further concerned that businesses continue to be exposed to asset stripping; further notes that many of those unregulated funds pay little or no UK tax while depriving citizens of opportunities and in many cases their homes; believes that HM Treasury should immediately require UK Asset Resolution to cease selling mortgages to any unregulated entity; considers that HM Treasury and the Bank of England should take all possible measures to ensure that mortgage prisoners are given access to new deals and fixed interest rates, and that banks cease discriminating against mortgage prisoners by offering them less favourable mortgage terms; further considers that the Government should expand the scope of FCA regulation to include all mortgages and all unregulated purchasers of mortgages; and calls on HM Treasury and the Bank of England to hold an urgent inquiry into the sale of mortgage and commercial debt by any financial institution to any unregulated entity, with the findings of such inquiry to be published. -

Acceptance Criteria

Professional Consultants Certificate (PCC) Acceptance Criteria 40 Lime Street London EC3M 7AW Lender Answer Accord Buy to Let Yes, if the building work has been monitored by a professional consultant and provided any certificate given by a professional consultant meets the requirements of 6.7.4 and the appendix to the Handbook. We do not have our own form of certificate. Accord Mortgages Ltd Yes, if the building work has been monitored by a professional consultant and provided any certificate given by a professional consultant meets the requirements of 6.7.4 and the appendix to the Handbook. We do not have our own form of certificate. Adam & Company Refer to us in writing. See 1.11 Adam & Company International Refer to us in writing. See 1.11 Ahli United Bank (UK) plc Yes, provided it has been built under the supervision of a qualified architect or surveyor with adequate professional indemnity insurance and you have received documentary evidence to evidence this together with building regulation sign off. Aldermore Bank PLC We do not have our own form of certificate. Allied Irish Bank (GB), a trading Refer to AIB Group (UK) plc, Central Securities (GB) name of AIB Group (UK) Atom Bank plc Where the property does not have the benefit of a New Home Warranty scheme or suitable alternative as listed in 6.7.1 and has been built in the last 10 years then we will not proceed. However, for Converted Properties we will proceed providing confirmation is received that the property is subject to full building regulations, planning permissions and completion certificate. -

UKAR Fact Sheet 6 Months to 30 September 2016

UKAR Fact Sheet 6 months to 30 September 2016 UKAR’s mission is to maximise value for the taxpayer while treating all stakeholders fairly UK Asset Resolution (UKAR) is UKAR is responsible for the the holding company UK Financial Investments administration of the established on 1 October 2010 Limited (UKFI) manages HM Government’s Help to Buy: to bring together the Treasury’s 100% shareholding mortgage guarantee scheme government owned businesses in UKAR. and the Help to Buy: ISA on of Bradford & Bingley (B&B) and behalf of HM Treasury. NRAM. Key Strategic Developments In the last period: • Successfully completed the final stage of a major sale of c.£13bn assets which saw 113,000 NRAM customer loans move to the Landmark Mortgages or Whistletree brands. • Completed the outsourcing of the servicing of our customer loans to Computershare providing stability of service to customers. • Subsequently launched the first stage of a sale of Bradford & Bingley assets that could ultimately enable the phased repayment of the Financial Services Compensation Scheme (‘FSCS’) loan. These developments are based on achieving value for the taxpayer, whilst serving our customers well and treating all our stakeholders fairly. Business highlights Customers and Conduct Since formation: In the last period: Balance sheet reduced by £78.9bn, 68%. More than 95% of our customers are up to date with their mortgage payments. Government loan repayments of £21.4bn; loan reduced by 44%. Made c. 8,000 “arrangements to pay” to assist customers in difficulty. Mortgage accounts three or more months in arrears, including possessions, have Referred c. 1,600 customers to not-for- reduced by 86%. -

FELDSPAR 2016-1 PLC (Incorporated in England and Wales with Limited Liability, Registered Number 10175202)

FELDSPAR 2016-1 PLC (Incorporated in England and Wales with limited liability, registered number 10175202) Class of Initial Principal Issue Interest Relevant Ratings Final Maturity Notes Amount Price Rate Margin Step-Up Date (Fitch/Moody's) Date Class A £670,000,000 100% 3 month Prior to the December AAA sf/Aaa (sf) September Notes GBP LIBOR Step-Up Date 2021 2045 plus the 0.70% per Relevant annum and Margin after the Step- Up Date 1.40% per annum Class Z £250,000,000 100% 3 month 0.0% N/A Not rated September VFN (of which GBP LIBOR 2045 £116,219,000 plus the shall be Relevant subscribed for Margin as at the Closing Date) Issue Date The Issuer will issue the Notes in the classes set out above on 11 November 2016 (the Closing Date). The Volcker Rule The Issuer is not, and solely after giving effect to any offering and sale of the Notes and the application of the proceeds thereof will not be, a "covered fund" for purposes of regulations adopted under Section 31 of the Bank Holding Company Act of 1956, as amended (commonly known as the Volcker Rule). In reaching this conclusion, although other statutory or regulatory exclusions and/or exemptions under the Investment Company Act of 1940, as amended (the Investment Company Act) and under the Volcker Rule and its related regulations may be available, the Issuer has relied on the determination that the Issuer would satisfy all of the elements of the exemption from the definition of "investment company" under the Investment Company Act provided by Section 3(c)(5) thereunder.